Global| Sep 02 2025

Global| Sep 02 2025Inflation in Europe Shows Mild Pressure

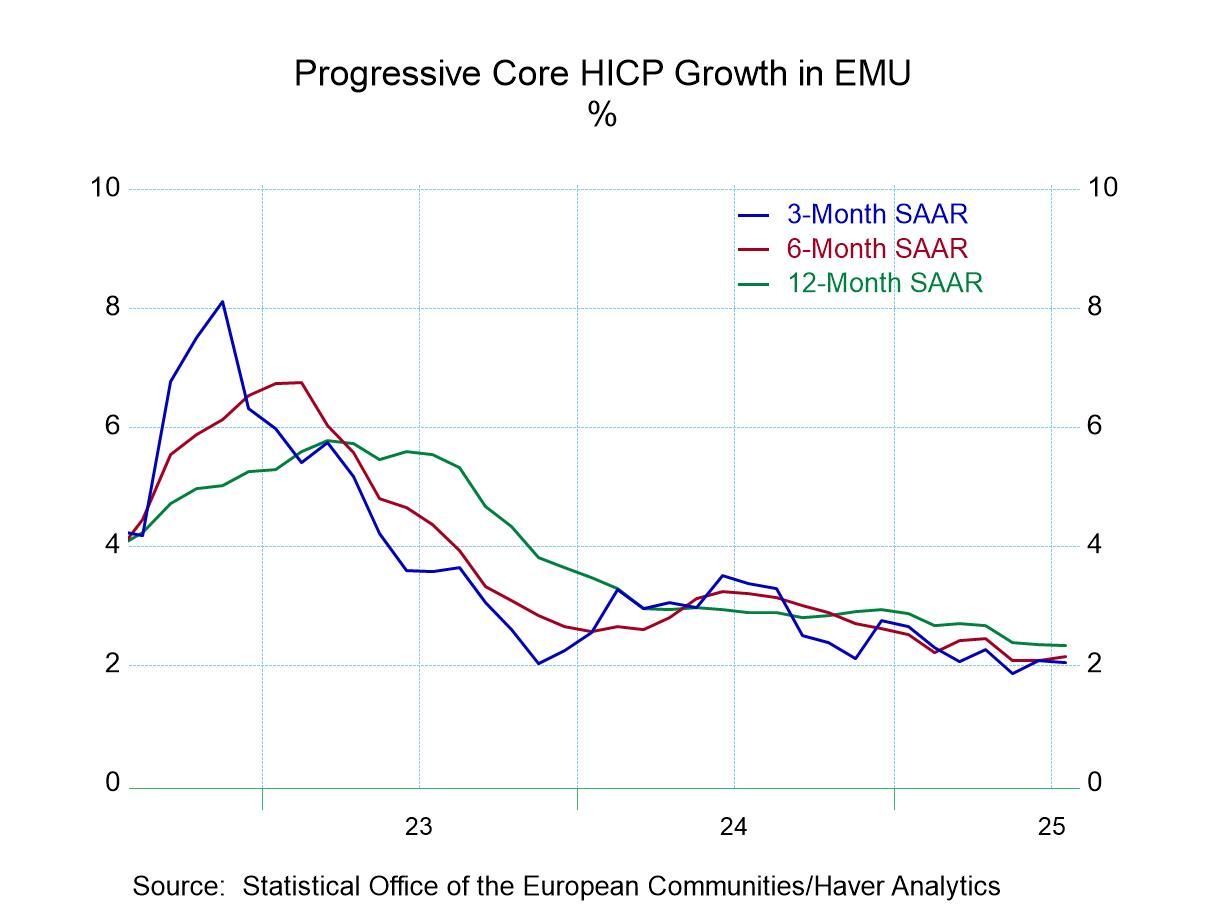

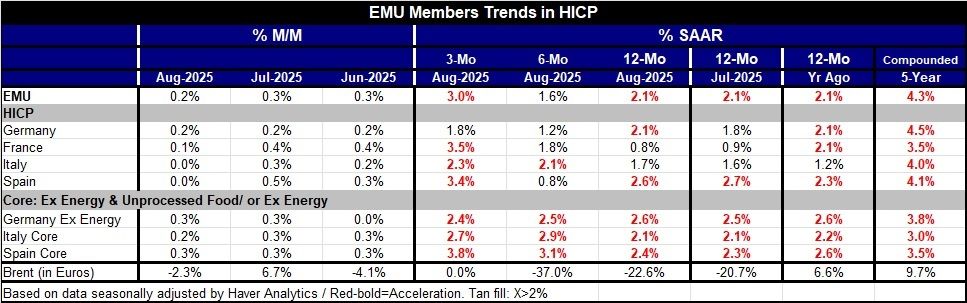

Inflation in August was well behaved; the headline series with the monetary union posted a gain of 0.2% after 0.3% gains in each of the previous months. Still those increases mean that the three-month inflation rate is at 3% compared to 2.1% over 12 months. Stop headline inflation has grown moderately hot in the monetary union.

Across countries the largest EMU members has so well-behaved inflation in August, with Germany up 0.2%, France up 0.1%, and Italy and Spain both unchanged. However, inflation in the previous two months was a bit stronger leaving three-month inflation rates for France, Italy, and Spain over 2%. Over six months only Italy is over 2% and that's barely, and over 12 months only Spain is substantially above the 2% mark.

Core inflation in the monetary union is where the elusiveness and stubbornness is for the three large economies that report core inflation. Germany actually reports ex-energy inflation. Italy and Spain report core inflation. They're all showing increases of 0.3 and 0.2 over the last two months. Over three months German ex-energy inflation is running at a 2.4% annual rate with Italy's core at 2.7% and Spain's core at 3.8%. Over 12 months German ex-energy inflation is up at a 2.6% annual rate, compared to a 2.4% annual rate for Spain’s core and Italy’s core that that is nearly on the money at a 2.1% annual rate.

The 12-monht inflation rate is marginally worse for headline and core rates across this group of countries in August compared to July. For the EMU, the headline is the same at 2.1%. Even though shorter measures show some pressure building, 12-month inflation is marginally lower in August 2025 than in August 2024 for headline and core measures in the large countries.

However, there has been no sense of controlled inflation recently as all averages are clearly excessive with the average five-year reading at a low of 3% for core inflation in Italy to a five-year average high of 4.5% in Germany. This legacy for inflation is still a problem for some although central bankers around the world are trying to dismiss it as a past event; however, no one's quite sure whether inflation is really over the hump and going back to normal for good.

This keeps monetary policy somewhat complicated; at the same time the global geopolitical scene is in turmoil, and it's always hard to make monetary and fiscal policy when there are national security risks especially when there's a war percolating at your border. Internationally the goods sectors – manufacturing- remain weak although there's evidence that global trade has showed some spunk at least in terms of the Baltic dry index which is undergoing some moderate firmness. In the United States, despite the fact that the Fed has not hit its inflation target in 4 ¼ years, the central bank still seems to be finding its way to rate cuts possibly as soon as this month. All that simply points out that it's a very different world than what it has been with central banks willing to cut rates with inflation over the top of the target having been over the top of its target for an extended period of time. This suggests to me that central bank credibility means something different or possibly that there is such a perception of the global economic environment that investors don't really feel that central banks are that important… sort of like deciding that your neighborhood is so safe; it doesn't matter if you lock the doors at night until of course it does matter. But then it’s too late.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief