Global| Sep 03 2025

Global| Sep 03 2025S&P Composite PMIs Improve in August

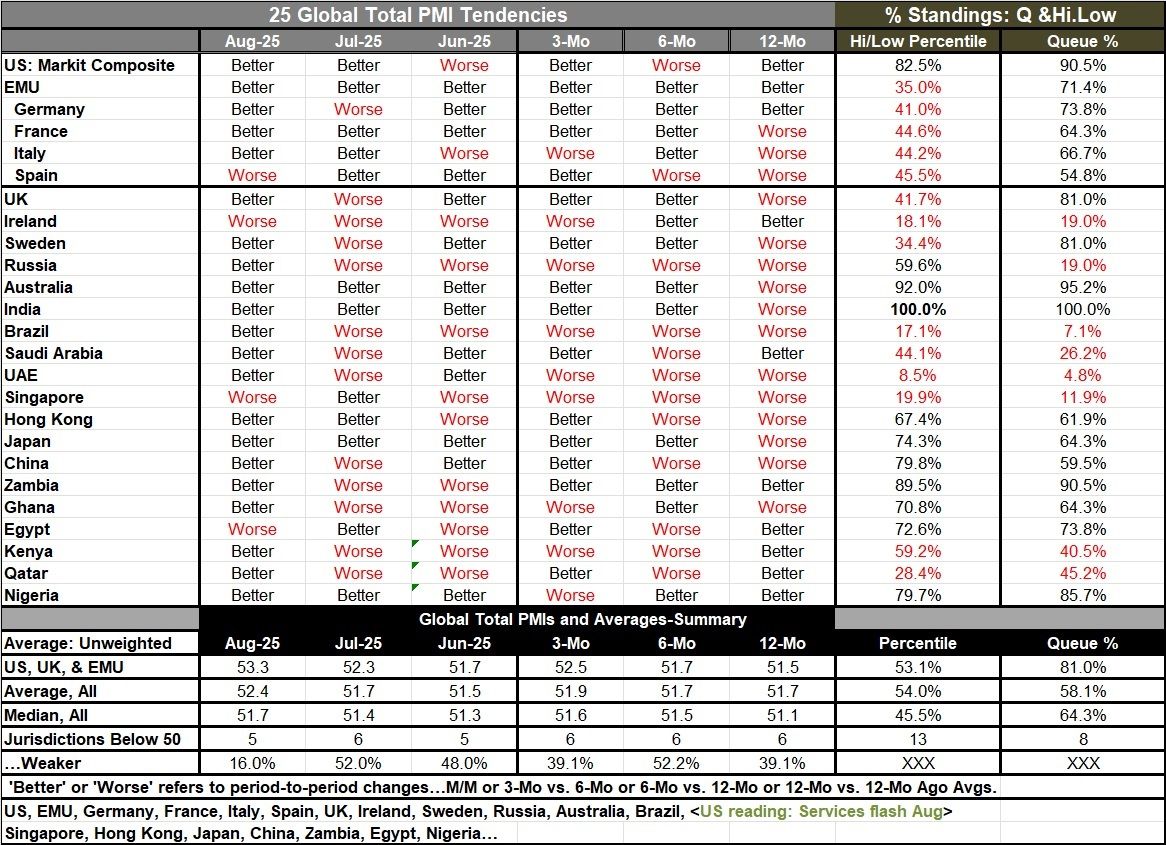

The S&P composite PMIs in August have advanced broadly with only four of 25 reporters showing weaker conditions in August compared to July. In July 13 of these same reporters showed worsening conditions and in June 12 reporters showed worsening conditions. August is a marked turnaround for this survey. One caveat is that the U.S .data in this report continued to use the preliminary services estimate because the final U.S. estimate is not yet available.

Over three months compared to six months, 9 of 25 reporters show worsening conditions. Over six months compared to 12 months, 12 of 25 reporters showed worsening conditions. Over 12 months compared to a year ago, 15 reporters out of 25 showed worsening conditions. There has been a progression in terms of the breadth for reporting countries that are showing improvement in addition the overall average. It has improved slightly from 51.7 over 6 and 12 months to 51.9 over 3 months. The medians have improved from 51.1 over 12 months to 51.5 over 6 months to 51.6 over 3 months, a slightly clearer progression toward better results. Still, both of them are on fairly thin margins of improvement. However, June to August the averages and medians show a little bit more movement and a little more progression to better readings.

The statistic that is perhaps most encouraging is the one about the percentage of reporters that are weaker in August; only 16 were weaker compared to July; in July 52% were weaker compared to June, but in June 48% were weaker compared to May. Looking at the broader progressive period, 39.1% are weaker over 3 months, 52.2% are weaker over 6 months compared to 39.1% weaker over 12 months. The proportion of reporters weakening over these horizons is moderate on the order of 40% to 50%- tending to readings below 50%.

The queue percentile standings show only 8 reporters out of 25 have standings below their median since January 2021.

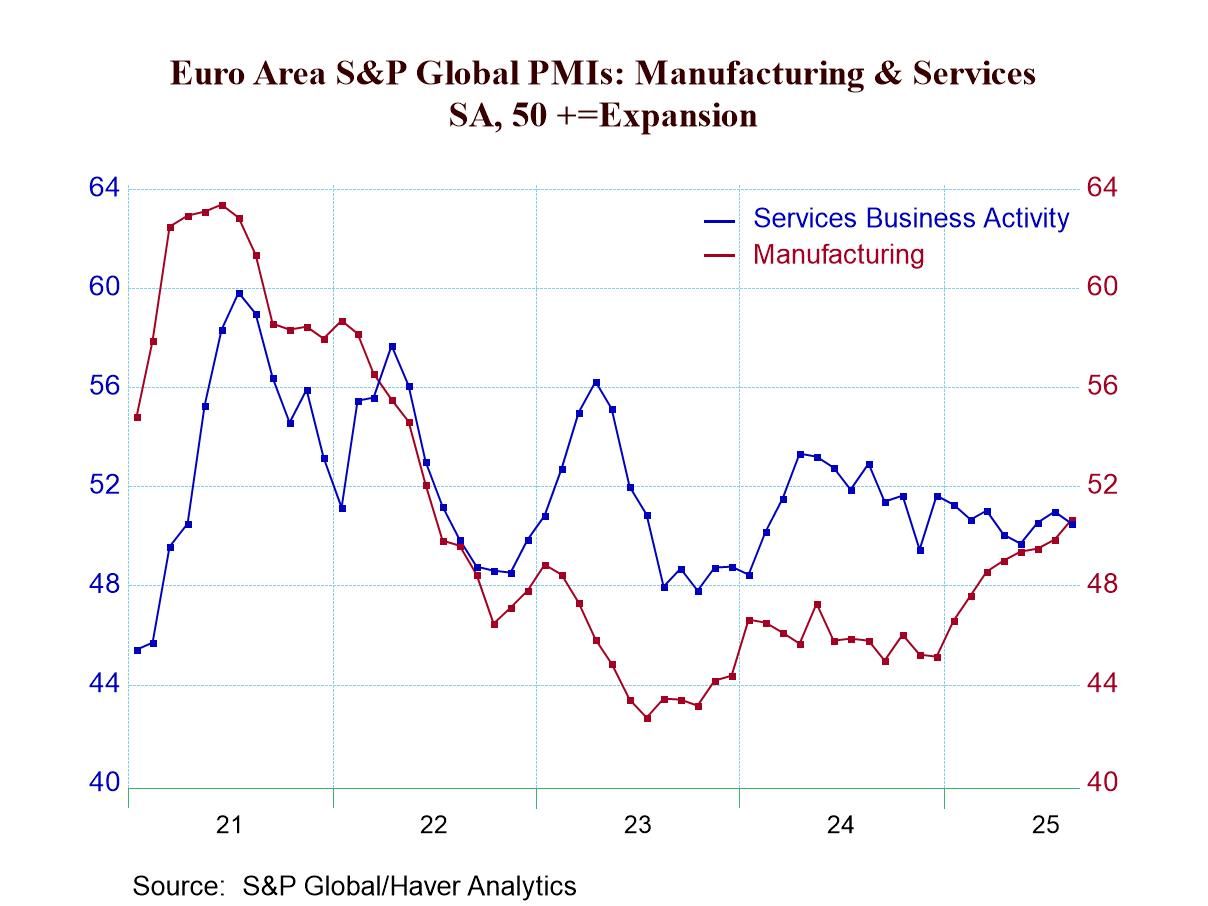

The chart on top depicts separately the services business activity index for the euro area versus the euro area manufacturing PMI. While the services readings have been relatively stable - perhaps trending slightly to weakness from earlier in the year - manufacturing PMIs have been improving consistently and strongly. At first it was thought that this was manufacturing activity that was ramping up to try to create output to export before U.S. tariffs went into effect, but since the tariff deadline has come and gone, manufacturing has continued to stay strong and to further strengthen. This is an unexpected and impressive trend.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief