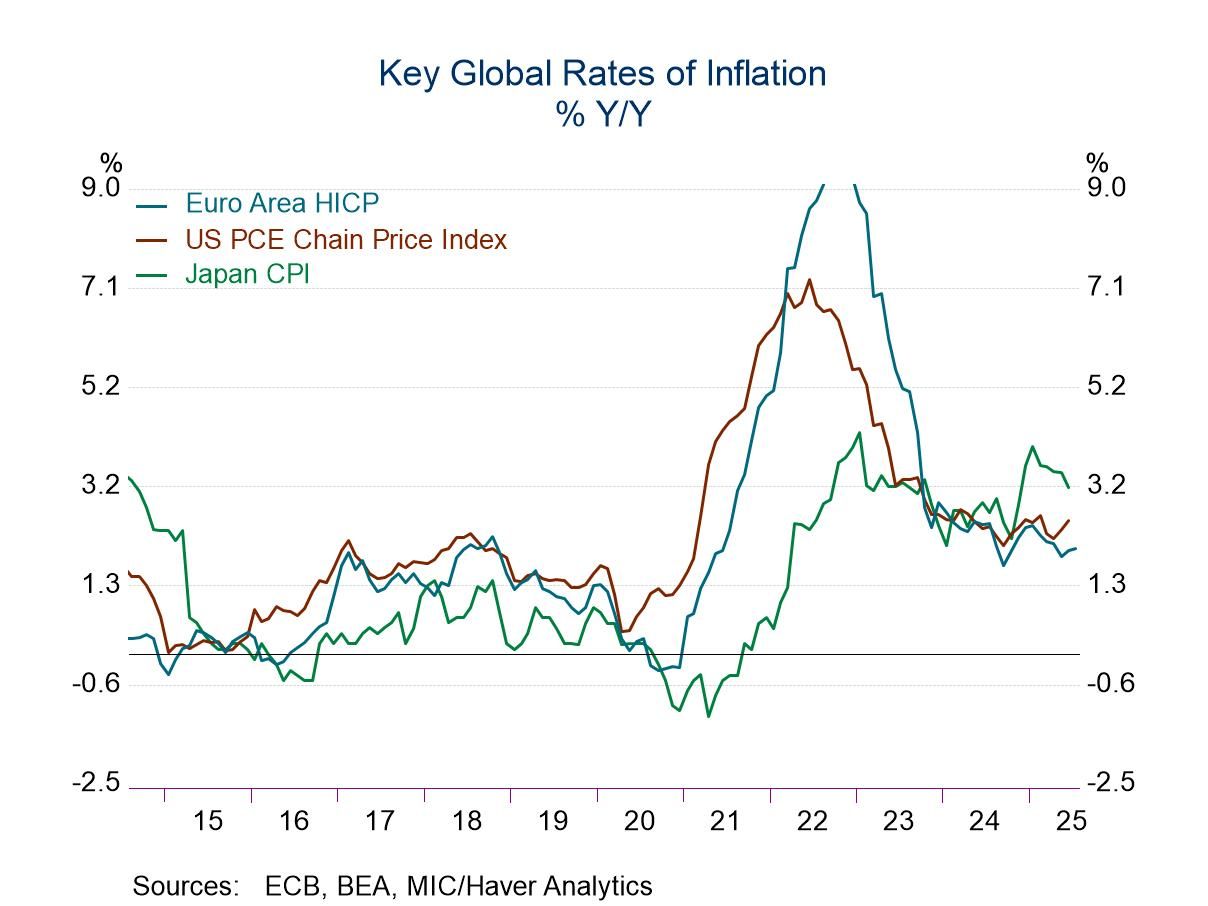

As more updated inflation data continue to post, we can look back at EMU historic inflation performance and try to gain some perspective. Since the euro area went to single currency status and set a program in motion for replacing domestic currencies (whose exchange rates were by then locked) with the euro-currency unit, there has been a lot of shifting of inflation and in relative prices among members. In the early days, there was a lot of concern about that and about entry level inflation commitments in the community.

On a to-date basis, despite the recent loss of control over inflation (in the wake of COVID and the Russian invasion of Ukraine) which the ECB has now mostly – but not fully- contained, core inflation in the EMU still runs hot and does so somewhat broadly. Still, headline inflation in the euro area has run at a compounded annual rate of 2.1% since January 1999, very close to its original 2% commitment.

Current headline inflation rates among early reporting and early EMU members (11-countries) show year-on-year inflation at 2.4% or higher in six of them- highest at 3.5% in Austria.

Since currencies were bound together and blended into the euro in January 1999, price levels among these members have risen in differing magnitudes, ranging from 92% in Luxembourg to 63% in France. That leaves a lot of potential for competitiveness gaps between those countries depending on the industries that most responsible for the price-level rise differences.

Price levels have risen more slowly than for the EMU overall in France, Finland, Ireland, Germany, and Italy. When the EMU was first being implemented, there were massive and chronic inflation differences between hard money countries like Germany, the Netherlands, Finland and a few others. The Mediterranean countries including France, Spain, Portugal, Italy, and Greece had typically run much higher rates of inflation. However, after over a quarter century in the cauldron of monetary singularity, we find that Spain and Portugal have averaged inflation rates of 2.4% and 2.2% while the EMU has averaged a pace of 2.1% during the period. Italy has averaged 2.1%. These are tightly clustered results.

The Monetary Union has had its difficulties, its tensions, its debt crises, and has withstood an influx of migrate that created tensions in the area (an influx that cost former EU member the U.K. its membership). But in the end, current inflation rates are mostly in alignment and so do not seem to display much more variation that the sorts of inflation rate difference you see among various states within the United States. The worst start-to-date inflation performance is in Luxembourg at 2.5% -and that probably matters the least since it is a financial center and does not compete much in manufacturing.

The far-right hand column in the table ‘memorializes’ history by showing the largest divergence between German inflation and each member over this history back to 1999. The current largest one-year inflation rate gap with Germany is Austria at 1.5% but after that it is Spain at 0.6% and then Portugal, Luxembourg, and Belgium -all at 0.5%. These gaps bear no relationship to the historic annual discrepancies as large as 28%. Four countries have their largest discrepancy with Germany annual inflation at over 20%; the others are greater than 15% but less than 20%.

For reference, I include the United States and the United Kingdom at the bottom of the table. They are two peas-in-a-pod with aggregate price levels rising over 90% each over this period. We can see the impact of that on the dollar’s value as well as on the value of the pound sterling over this period. If exchange rates are locked (as in the EMU), domestic prices are forced to rationalize themselves in the domestic economy. If exchange rates are left to fluctuate, the pressure on the domestic price level to adjust is alleviated because the exchange rate can adjust instead. Forcing adjustments in prices through a domestic chain of events is usually more painful than undergoing exchange rate change and, the later, simply change all prices in unison at least those for tradeable goods.

Asia

Asia