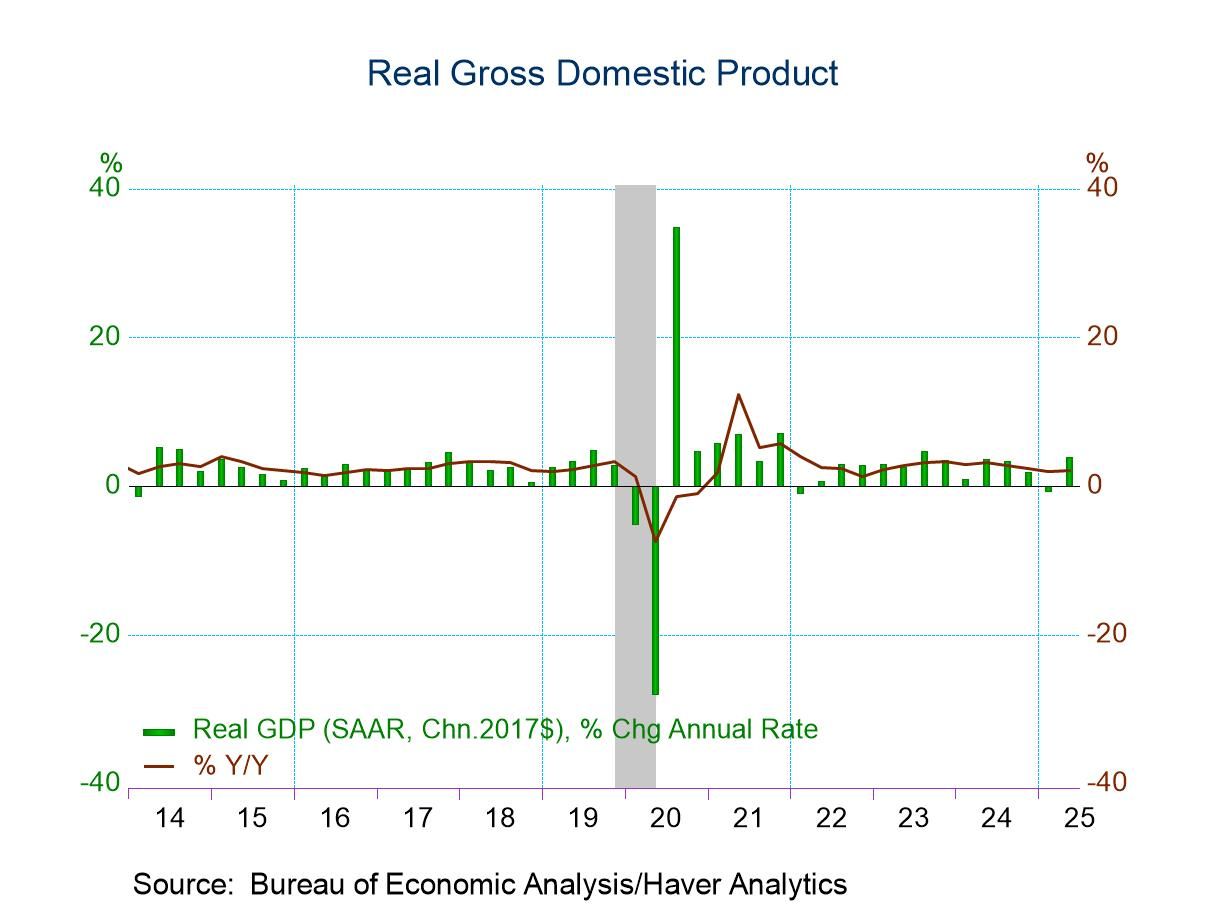

- Real GDP advanced at a 3.8% saar in Q3 in the third estimate, up from 3.3% in the second estimate and 3.0% in the advance report.

- Stronger consumer spending and business fixed investment were the major factors behind the upward revision.

- Meaningful upward revisions to measures of aggregate demand.

- Small upward revision to GDP and PCE inflation.

- Annual benchmark revision benign; annual real GDP growth from 2019 to 2024 was unrevised at 2.4%.

USA| Sep 25 2025

USA| Sep 25 2025Resilient Consumer Propels Upward Revision to Q2 2025 GDP Growth

by:Sandy Batten

|in:Economy in Brief

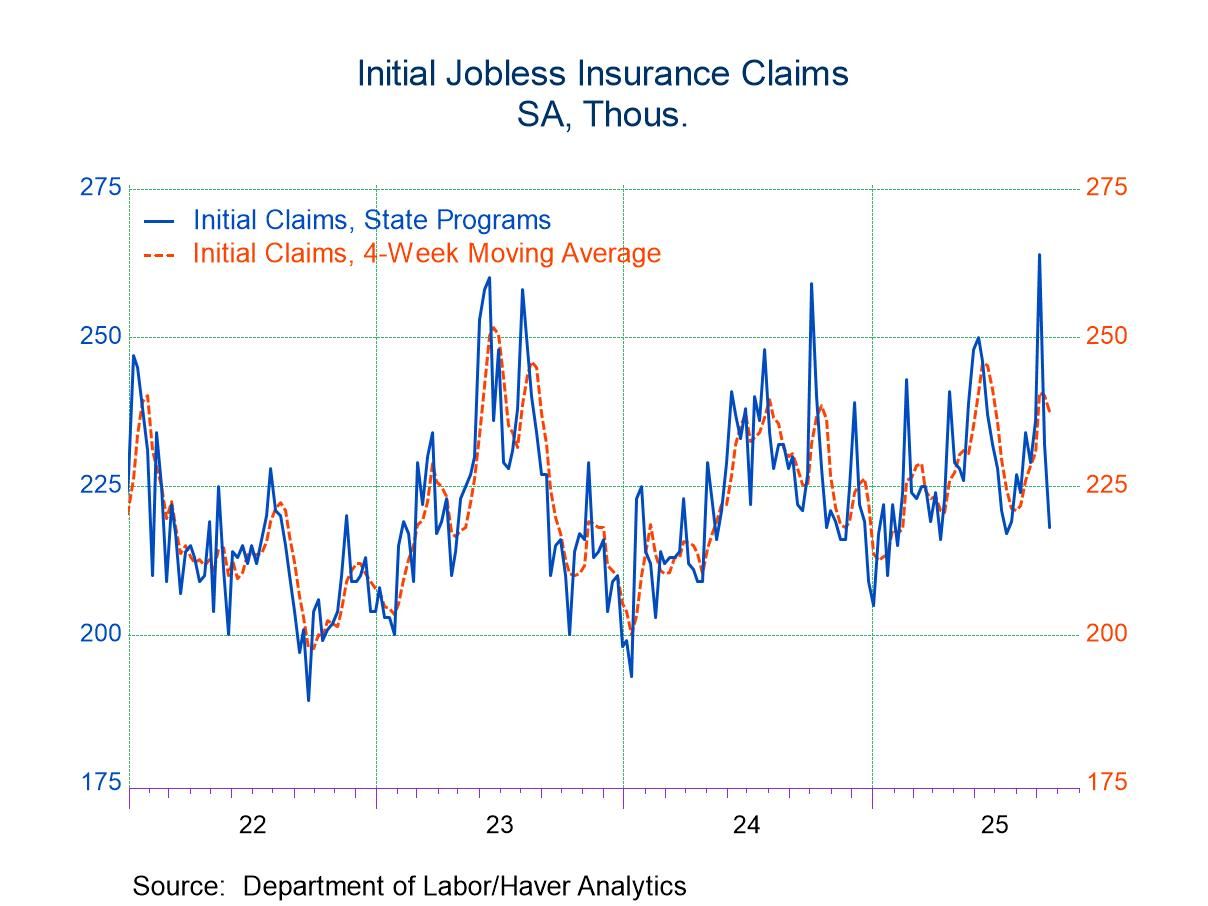

- Initial claims declined 14,000 in latest week.

- Continuing claims edged down slightly.

- Insured unemployment rate holds steady.

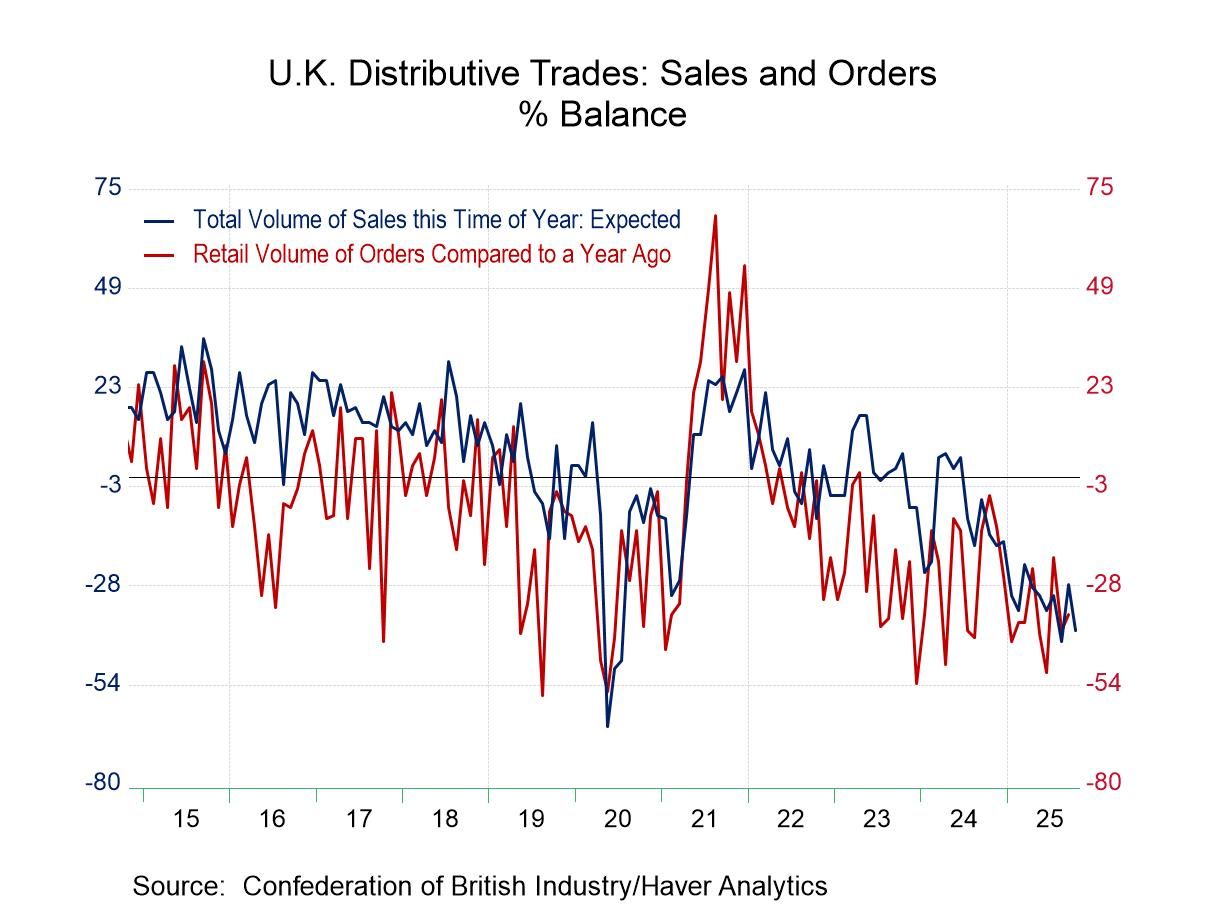

United Kingdom| Sep 25 2025

United Kingdom| Sep 25 2025U.K. Distributive Trades: Mixed with a Worsened Outlook

The Confederation of British Industry report shows some improvement and deterioration in the same month; retailing improves while wholesale survey worsens sharply. The look-ahead to October for retailing weakens sharply while there was mixed performance in the outlook for wholesaling. The report doesn't do much to clarify the outlook.

Current Sales: Current sales compared to a year ago improved to -29 in September from -32 in August. Orders compared to a year ago also improved to -36 from -40. These improvements still leave the monthly reading levels worse than their respective 12-month averages although sales at the time of year are significantly better than their 12-month average. The queue percentile standings for these metrics of sales are all weak, the only element in the report that is strong, or firm is for the stock to sales comparison, and that is usually a negative indicator.

Sales Expectations: The expectations in October for sales dropped sharply to a -36 reading from -16 in September, orders dropped to -38 from -32 in September while sales ‘for the time of year’ plunged to -43 from -20. Each one of these readings is weaker than its 12-month average. Historic standings are even weaker than for the current sales and orders metrics, with sales for a year ago with a 4.9 percentile standing and sales ‘for the time of year’ at an even weaker 1.4 percentile standing, rarely ever weaker. The current vs. the outlook signals are crossed.

Current Wholesaling: Worse performance in the current readings while the outlook for the next month is mixed marks the overview of the wholesale trade arm of the distributive sales report. Sales adjusted for the time of year and orders and sales compared to a year ago all deteriorate. Each one of these readings is not only weak month-to-month but each is weaker than its respective 12-month average. And the queue rankings are all in the lower tenth percentile range.

Wholesaling Expectations: The outlook shows mixed performance for sales compared to a year ago, improving to -22 in October from -26 in September; orders deteriorated to -41 from -38 in September. Sales ‘for the time of year’ barely ticked weaker in October. Readings are weaker than their respective 12-month averages as well, except for year-ago sales. The percentile standings for the three categories range from a ‘high’ percentile standing at its 14th percentile for sales compared to a year ago, while the other two metrics show rankings that are below their 5th percentiles in their historic queue of values – an extremely weak showing.

Summing up: Clearly the survey shows a mixed view of retail and a general worsening as well as a mixed-up picture between current performance vs. what is expected for next month. While there is little consistency in this survey in terms of monthly changes, what is crystal clear is that conditions - no matter where, or when, assessed - are very weak. Perhaps it is reports like this one that are keeping the Bank of England on hold instead of battling inflation with growth looking like it might give way at any moment.

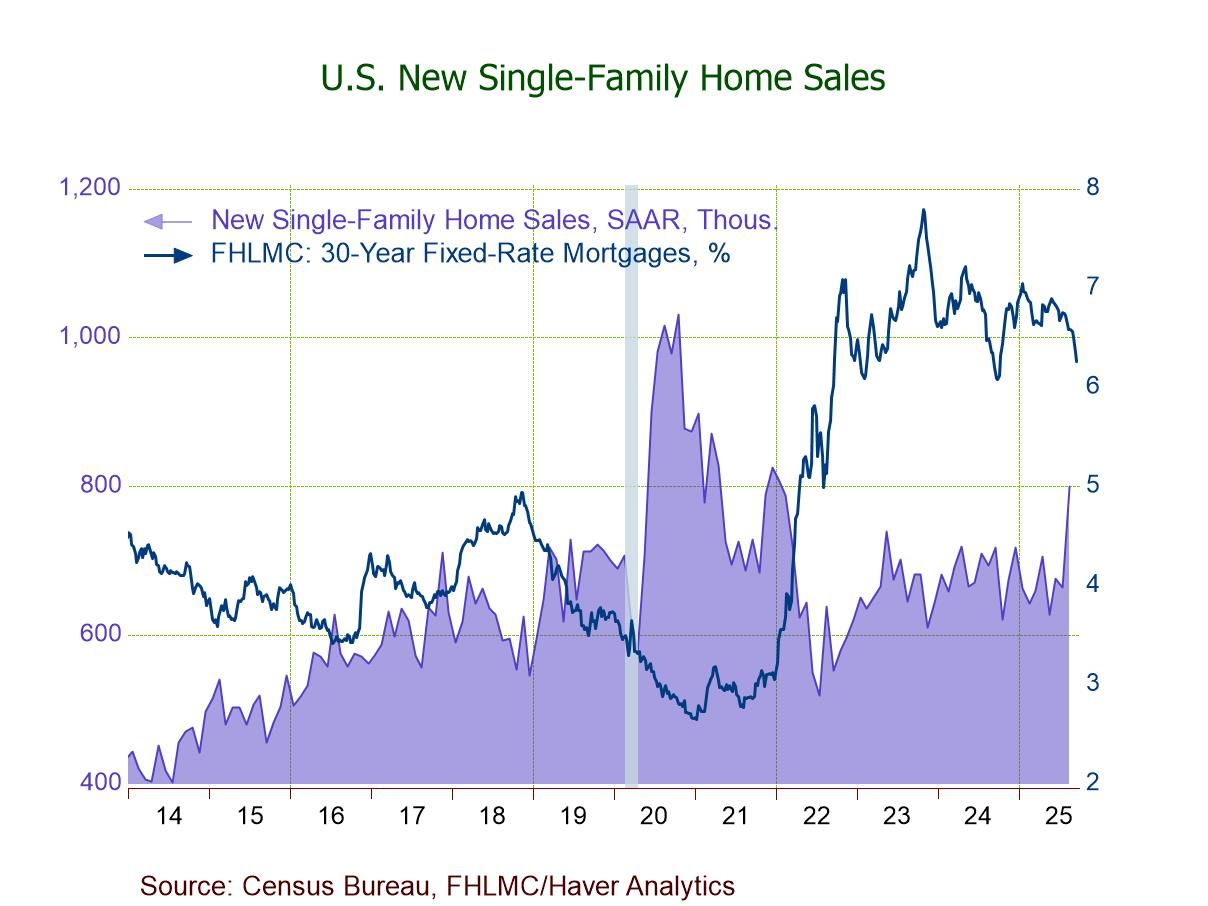

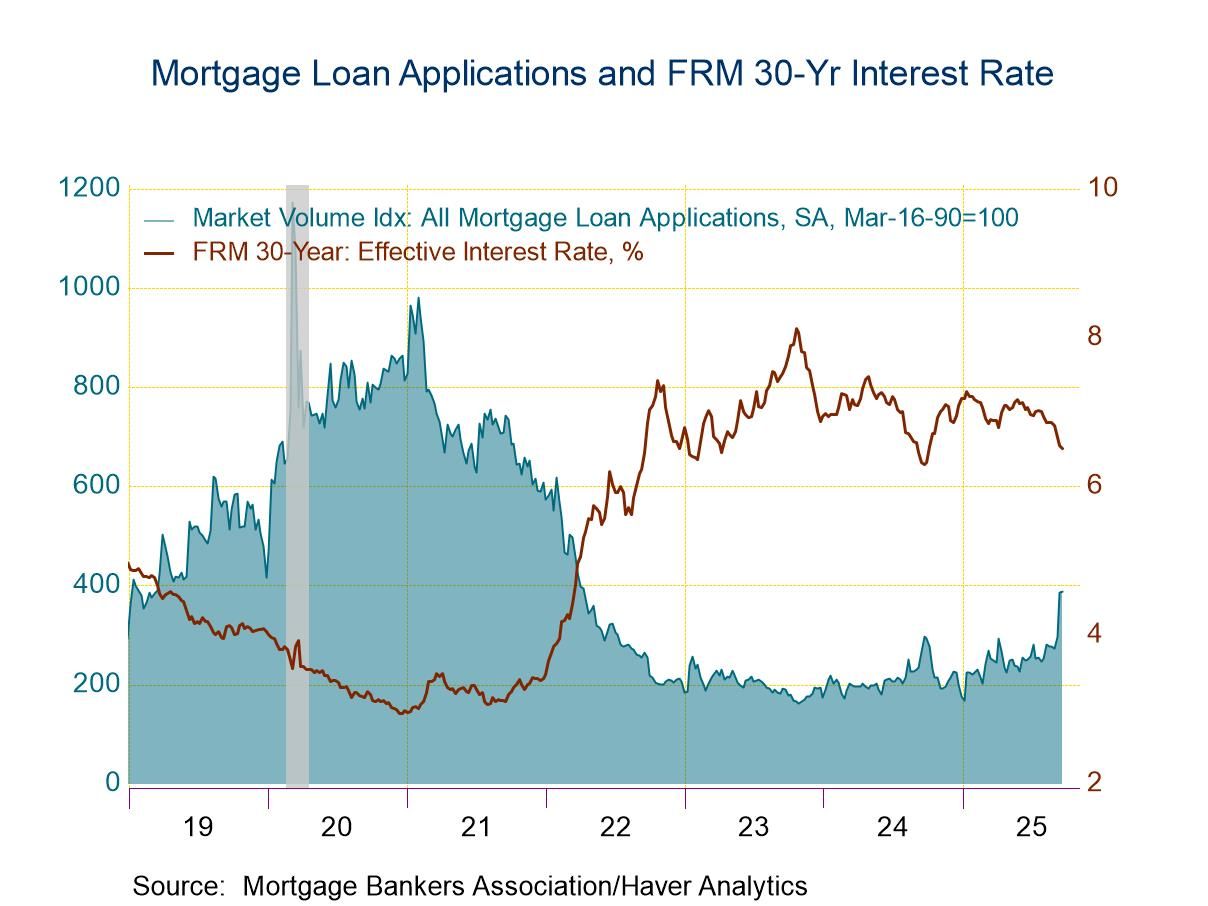

USA| Sep 24 2025

USA| Sep 24 2025U.S. New Home Sales Surge in August Amid Lower Mortgage Rates

- August sales +20.5% (+15.4% y/y) to 800,000; largest m/m gain in 3 yrs.; highest level since Jan. '22.

- Sales up m/m in all four regions; sales down y/y only in the West (-5.7% y/y).

- Median sales price at a 3-month-high $413,500; avg. sales price at a 3-year-high $534,100.

- Months' supply of new homes for sale drops to 7.4 mths., lowest since July '23.

- Purchase loan applications edge up 0.3% w/w, and refinancing loan applications rise 0.8% w/w jump.

- Effective interest rate on 30-year fixed-rate loans falls to 6.15%, the lowest since September 2024.

- Average loan size decline.

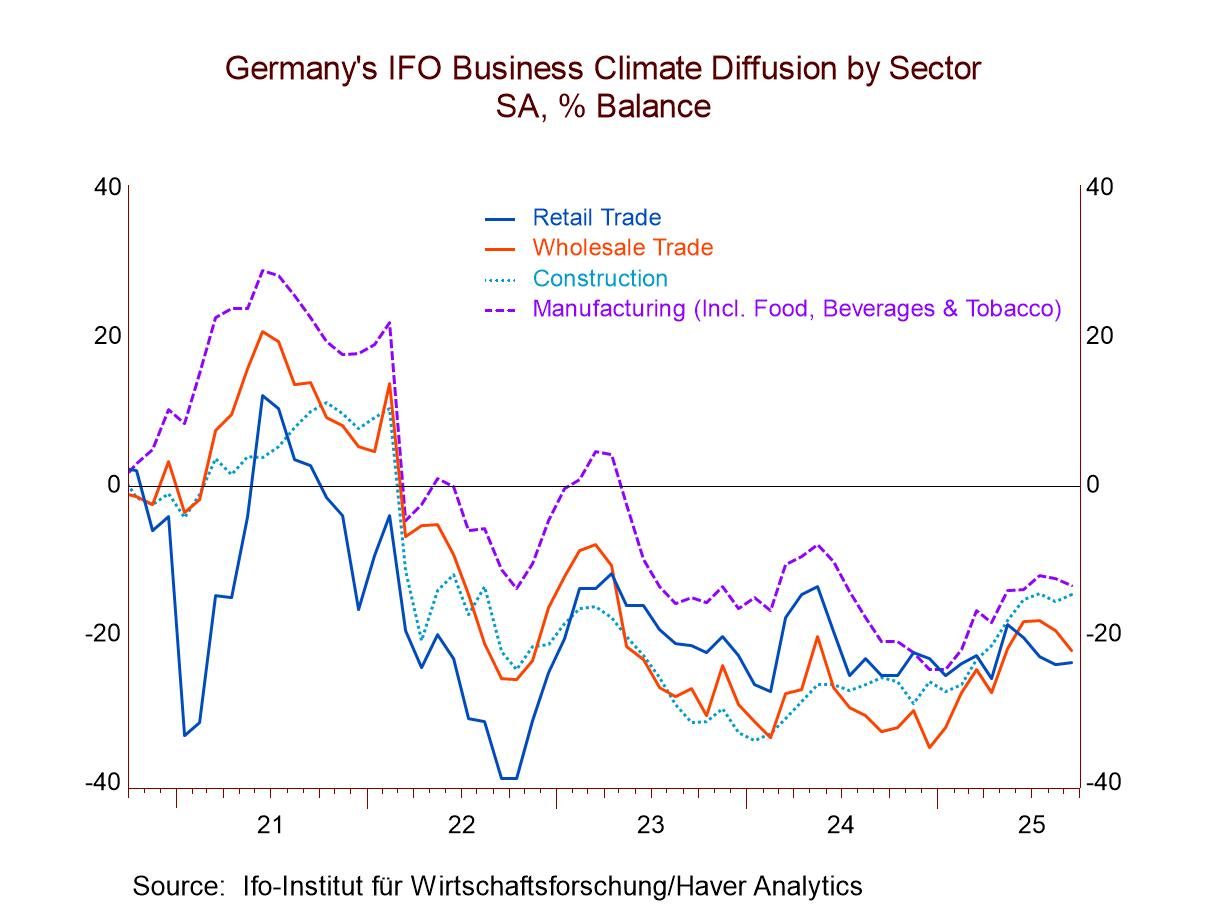

Germany| Sep 24 2025

Germany| Sep 24 2025IFO Survey Setback in Germany

The IFO climate survey deteriorated in September, falling to -15.6 from -15.1 in August. The wholesale reading showed a deterioration, as did manufacturing and then services. Construction and retailing improved slightly. The climate all-sector ranking is at its 20.7 percentile. Even weaker is the ranking for services at 7.9% and the ranking for manufacturing at 15.1%. Only the construction sector has a ranking above 50%, which places it above its median value. Wholesale and retailing both have rankings in the 21st percentile.

Current conditions in September fell to a diffusion reading of -4.7 from -3.1 in August. The slippage was in manufacturing, wholesaling, and services once again with construction improving slightly and retailing improving to -17.8 from -19.7. The queue standing rankings have the all-sector current index in its 10.8 percentile. The individual sectors all have a higher ranking than that. The lower overall ranking reflects the confluence of weak rankings across sectors that is unusual. Manufacturing has a 13-percentile standing, services have a 12-percentile standing, with retailing at a 41.7 percentile standing and once again construction has a standing above its 50th percentile at the 60.4 percentile mark.

The expectations’ all-sector index falls to -11.9 in September from -8.3 in August; that drop is troubling because this is a forward-looking metric not simply a current assessment. The rank standing for expectations is in its 19.7 percentile, about the same ranking as for climate and above the current all-sector ranking. Retailing logs a 13-percentile standing, services are at a 15-percentile standing, and wholesaling at a 19.9, nearly 20-percentile standing. Manufacturing is at a 26.9 percentile standing with construction at a 43-percentile standing. All the metrics are below their 50th percentile in expectations, marking all of them below their historic medians on data back to 1993.

There is a far-right hand column that also presents ranking statistics. These are rankings since February 2022 since the invasion of Ukraine by Russia. For expectations, we see that after the invasion rankings are currently showing a lot of uplift although ominously the services sector, which is the job creating sector has only a 56.8 percentile standing; that compares to the all-sector expectation standing at its 84th percentile. Looking at climate the all-sector index is at 54.5%. That is much stronger than on the full data set back to 1993. The 54.5 percentile standing is supported by strong readings out of construction and wholesaling vs. weak greetings from retailing and services. But these weak rankings are still stronger than for the full sample. Readings for September current conditions on this shorter period remain about the same as for the full sample – except that retailing and services are much weaker.

Overall, the September IFO is disappointing and weaker. The performance of expectations is disturbing. These are going to be developments to watch in the coming months especially to see if expectations make a recovery.

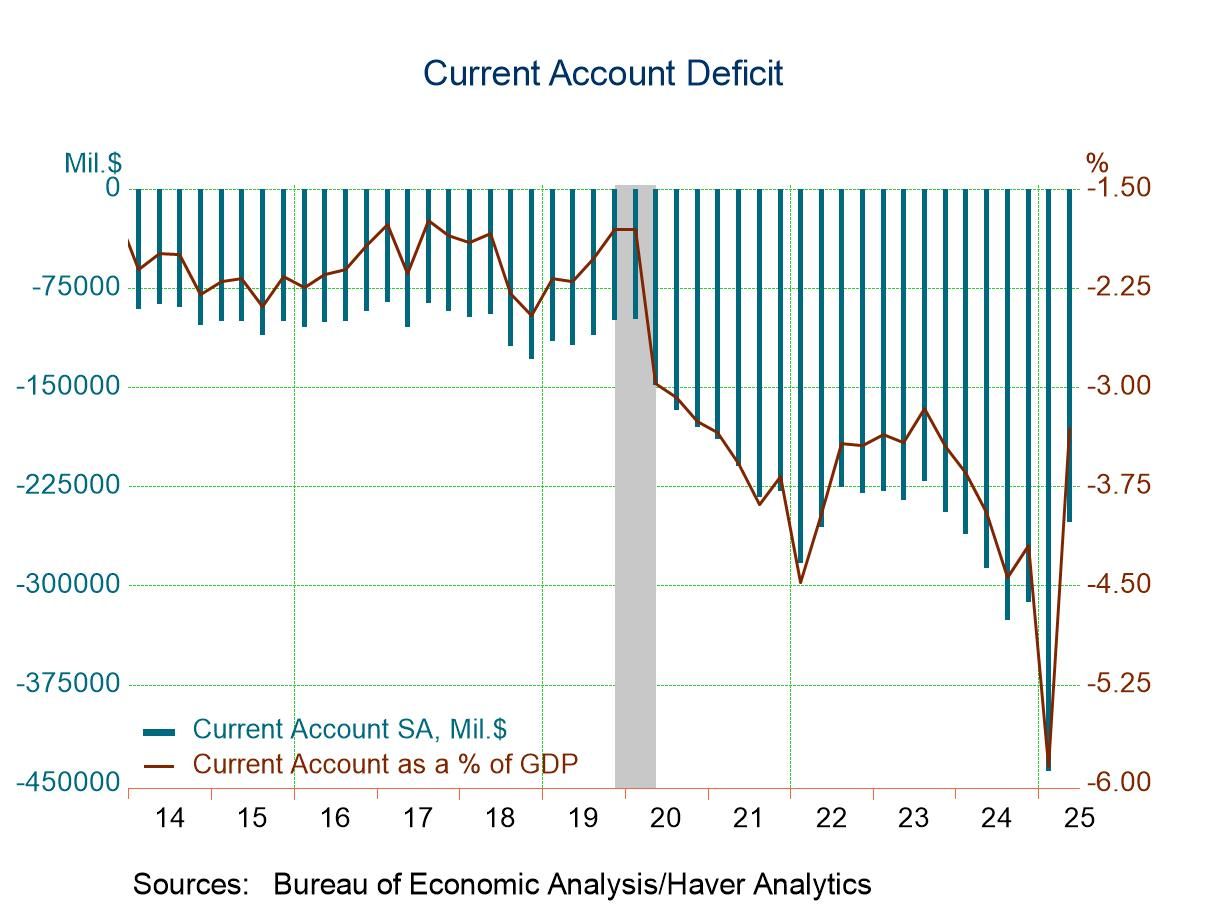

USA| Sep 23 2025

USA| Sep 23 2025U.S. Current Account Deficit Narrows Markedly in Q2 2025

- Goods deficit narrows to smallest since Q4 2023 as goods imports declined 18.4% q/q, reversing the surge in Q1.

- Services surplus narrowed slightly from record high in Q1.

- Balance on primary income remained in deficit, a rare occurrence. Secondary income deficit narrowed marginally.

- Net financial-account transactions were -$406.9 billion in the second quarter, reflecting net U.S. borrowing from foreign residents.

by:Sandy Batten

|in:Economy in Brief

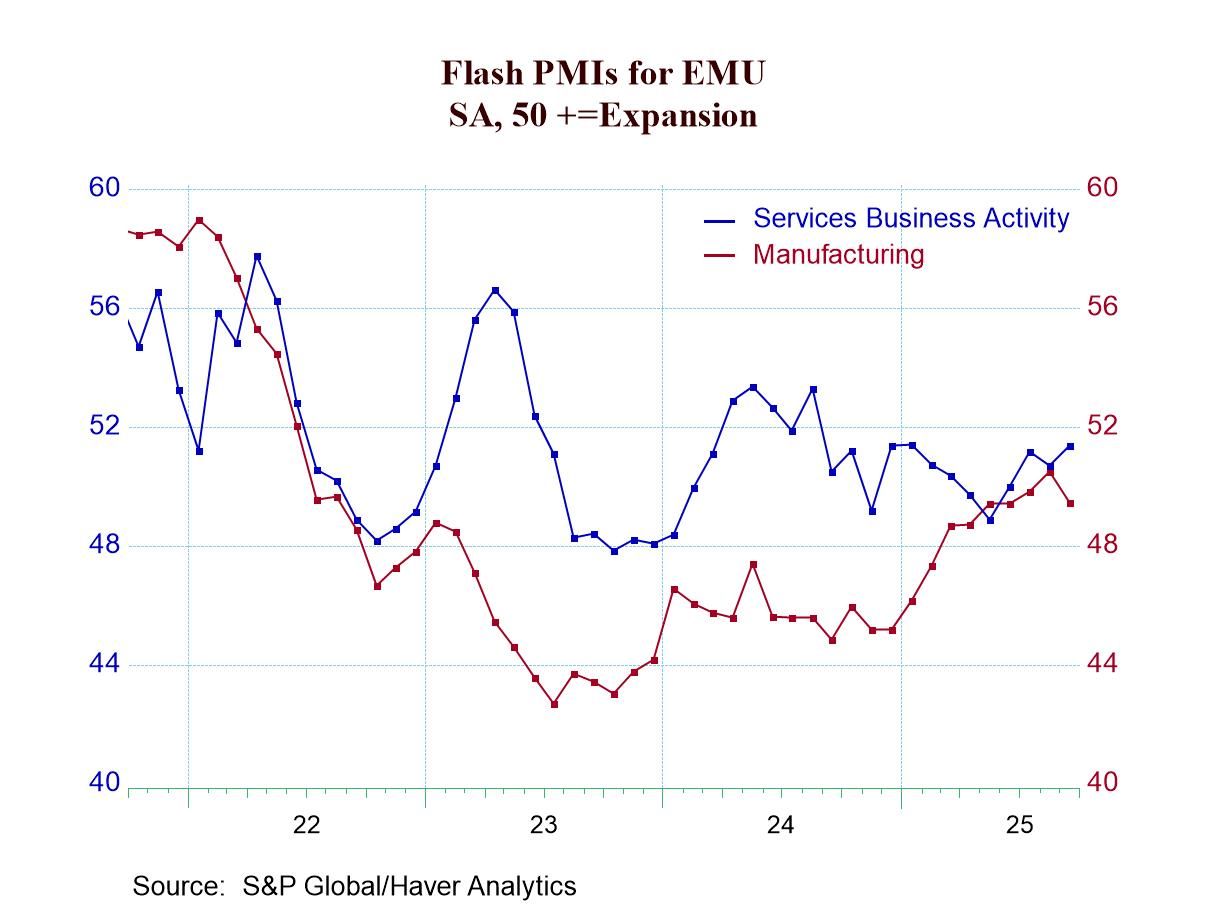

Global| Sep 23 2025

Global| Sep 23 2025Global PMI Weakness in September Despite Trending Progress

The S&P PMIs for September show more backtracking than they show progress, although over three months even in terms of up-to-date monthly data, the trends show uptrends (among 21 calculations of 3-month changes only three show setbacks). Weakening is shown in the service sector in the United States, India, and Australia while in the United Kingdom, France, Germany, and in the European Monetary Union (EMU) services sectors were getting stronger. In September, manufacturing weakened in the EMU, Germany, France, the United Kingdom, Australia, and India with only the U.S. showing improvement. Japan, a country that usually contributes to the early PMI flash survey, is not included this month in the early S&P release.

Sequential trends Over three months, we see broad strengthening across these reporting countries with Australia showing weakness across all three measures. India shows a composite weakening and a manufacturing weakening and France demonstrates manufacturing weakness. All the other 3-month metrics show strengthening. Using only the hard data and ignoring the up-to-date flash data that remained preliminary, there is still relatively broad strengthening over three months and six months. Over six months, the composite PMIs are strengthening everywhere except in Australia and in the United States with manufacturing improving broadly everywhere except in Australia, India, and in the U.K. Over 12 months, strengthening is also extremely broad with the United Kingdom an exception showing weakening on all three metrics- and with all the other metrics showing strengthening, except for services in Germany (17 out of 21 improve over 12 months).

Standings The queue percentile standing data show a proliferation of readings above the 50-percentile mark placing them above their medians on data back to January 2021; the exceptions are the U.K. with sub-median weakening in all three sectors and in the United States with a sub-par services readings but one that is barely below its median (at 49.1%!). France checks in with sub-median services and composite readings.

The outlook The chart at the top of this report makes a clear positive statement about the ongoing trend improvement. With the Federal Reserve in the U.S. having turned back to an easing cycle for interest rates even with inflation excessive, central banks may be ready to take a risk with stimulus. While inflation remains over target and may even be slightly accelerating, the pace of acceleration is very slight in the U.S. and largely the same conditions prevail globally. The current inflation overshoot faced by most central banks is modest; although in the case of the U.S., it has missed its inflation target for 4 1/2 years in a row-that should be worrisome but the Fed has pressed ahead with a rate cut and seems to favor even more.

The average results for the PMI readings sequentially for 12-months, 6-months and 3-months show steady improvement. The sequential readings are based on only hard data available through August. The more recent monthly data (far right hand column on changes) show June to September improvement for the composite index and for services averages with manufacturing slightly weaker.

The report on the month is slightly weaker, but the trending results are still encouraging. And if there is a new global easing cycle in train, growth will improve further even with the challenge of war remaining in place between Russia and Ukraine.

- of2736Go to 74 page