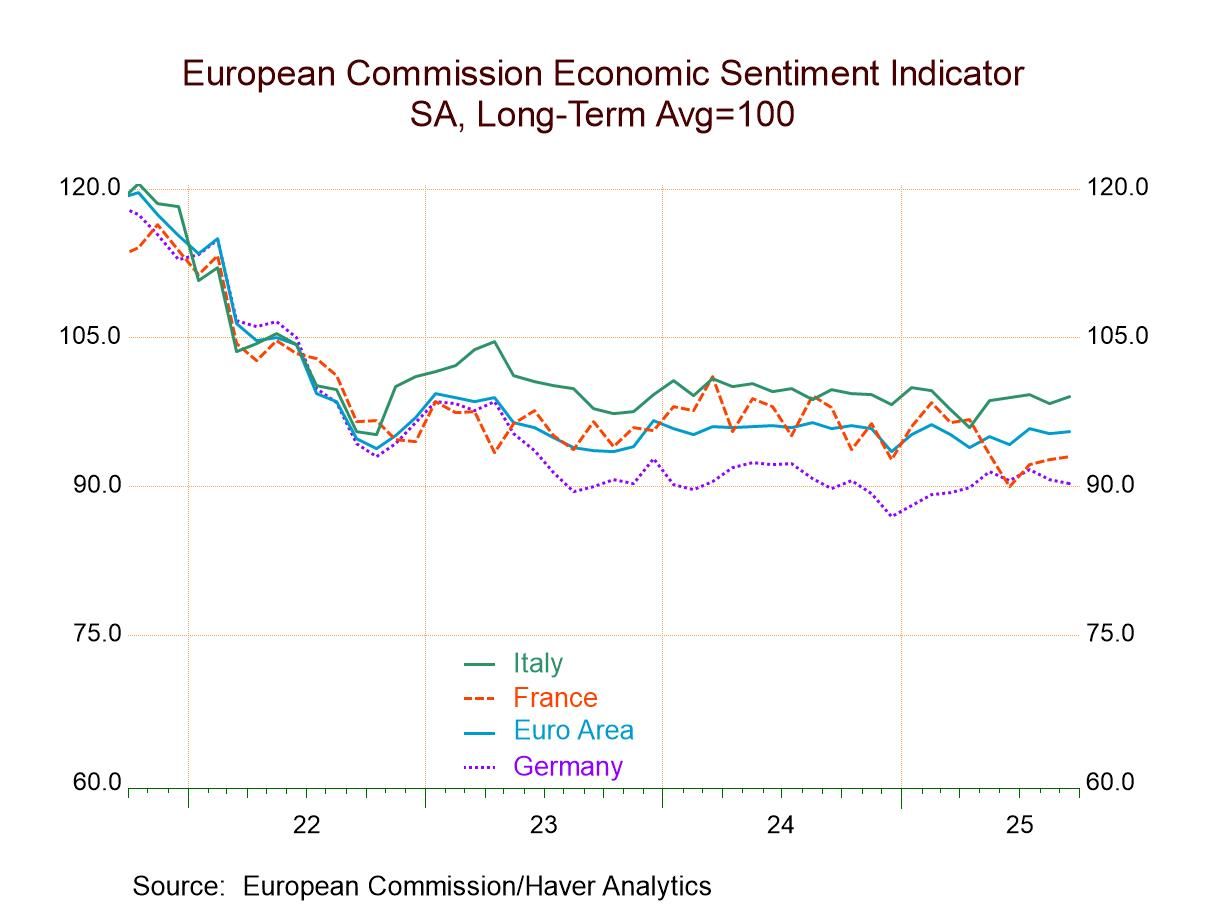

The European Monetary Union indexes for September showed slight uptick to 95.5 from 95.3 in August. However, at 95.5 the September reading was still below the July reading of 95.8, but it was above the June reading of 94.2. EU sentiment indexes have been moving sideways since the end of 2022 without much trend.

All the components except for construction rank and roughly their respective 20th to 30th percentiles of their historic queues of data. The exception is construction, where the sector has a 74.6 percentile standing and retailing with a nearly 46-percentile standing, leaving it marginally below its median. However, the industrial sector ranking is at its 26-percentile, services rank at their 27th percentile and consumer confidence is at its 20th percentile. On the whole that’s a collection of quite weak readings: one firm, one marginal and three weak.

Compared to January 2020 before COVID struck, all the sectors and the aggregate index are lower by about 8 to 10 points over the five-and-one-half-year period. The exception is the industrial sector, which is lower by only five points.

National sentiment monthly showed eight declines in September, compared to seven declines in August and only five month-to-month declines in July.

The sector rankings for large country industrial sentiment shows they're all ranking below 50% except for Spain. Spain also has the only above 50-percentiel standing for consumer confidence at a strong 96.5 percentile. Retailing has two of the large economies ranking above 50%: Italy and Spain. No service sector readings for the large economies are even close to neutral. Construction, however, ranks above the 50% mark in three of four large economics and in France, where it falls short and has a ranking that is still at its 45th percentile. Weakness is broadly shared across EMU sectors for the large and small alike.

The services sector weakness in the EMU is quite important because it's a job producing sector. It’s no coincidence that consumer confidence and services in the EMU have the lowest standings. The outlook for the monetary union is going to depend a lot on how the forces of inflation develop as well as how the war in Ukraine develops. In the meantime, U.S. budget politics could rile markets, and we are told that China is trying to dazzle the Trump Administration with a trade deal if it backs off support of Taiwan independence. Both of these are potentially global market moving events that are in flux.

Asia

Asia