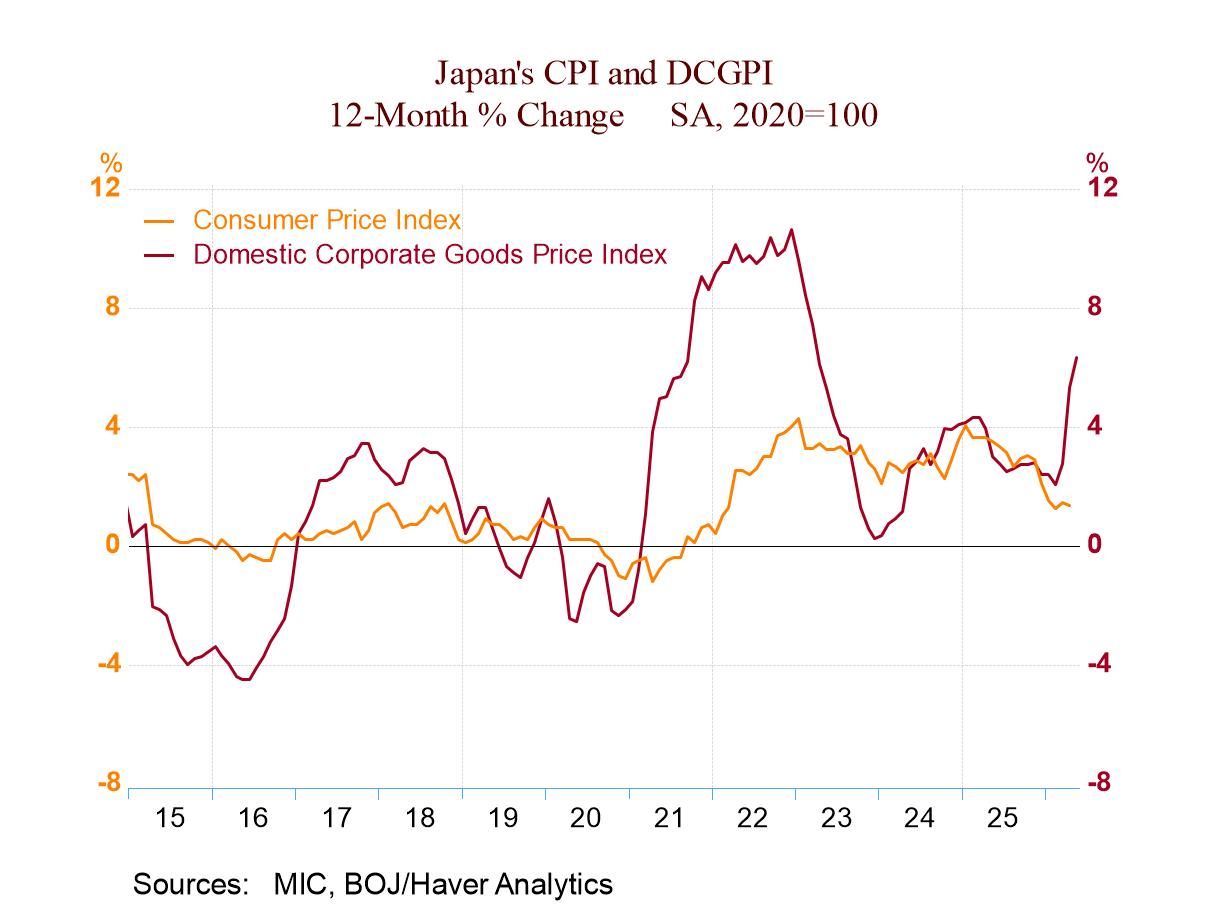

Once again, we are seeing Japan’s PPI creating a separation from the CPI. Both the CPI and PPI were trending lower before the attack on Iran. The CPI has better maintained its downtrend, but the PPI has been blasted higher. In 2021, there was also a huge spike in the PPI that the CPI did not follow immediately, although the CPI eventually responds, rising in a much more muted way.

These behaviors caution us from thinking that the CPI is going surge in step with the PPI but also warn us not to expect this gain to be ignored by the CPI. There will be a lagged response.

The PPI explosion is really strong, with the three-month annualized increase in the PPI and manufacturing prices both approaching 20%. Both measures are up at a much more muted 6% to 6.5% over 12 months, so the acceleration has been strong and sudden.

The table also shows lagged data that re-express the PPI trend to put it on the same timeline as Japan’s CPI and the U.S. and EMU PPIs. The PPI in the EMU has surged in line with the gains seen in Japan. However, in the U.S., the PPI has accelerated from a gain of 2.4% over 12 months to an annual rate rise of just 7.8% over three months.

But in Japan, the CPI and core CPI gauges have continued to temper their rises, using data through April and looking at sequential growth pressures on Japan’s CPI. It’s quite amazing!

Japan imports its oil and so would seem quite vulnerable to oil price spikes. However, because it is vulnerable, Japan takes steps to assure its supply and control its oil costs by arranging long-term contracts. That has helped to contain the impetus of surging global oil prices. Globally, oil (Brent, in dollars) is off sharply in May after turning slightly lower in April. Sequentially, Brent prices are up 44.4% over 12 months, up at a 110.2% annual rate over six months, and still up at 187.6% annualized rate over three months.

The table also shows some simple correlations with Brent prices. It demonstrates that the correlation between PPI prices of various sorts and Brent ranges from 0.4 to 0.5. But the correlation to Japan’s CPI price metrics is negative. So far, Japan’s CPI has been true to those results.

The Bank of Japan continues to struggle with its own view of the inflation risk. It is wary of damaging the economy but also concerned about allowing the door open to inflation because of its massive debt-to-GDP ratio. The BOJ is going to remain on inflation watch for some time.

Asia

Asia