Canadian CPI Trends Show Little Change

Inflation around the world appears to be rather similarly behaved Canada is a very close trading partner of the United States and so we might expect that there would be a little more connection between the prices in Canada and in the US and possibly we can learn something about the upcoming US CPI report by looking at the just-released Canadian CPI report.

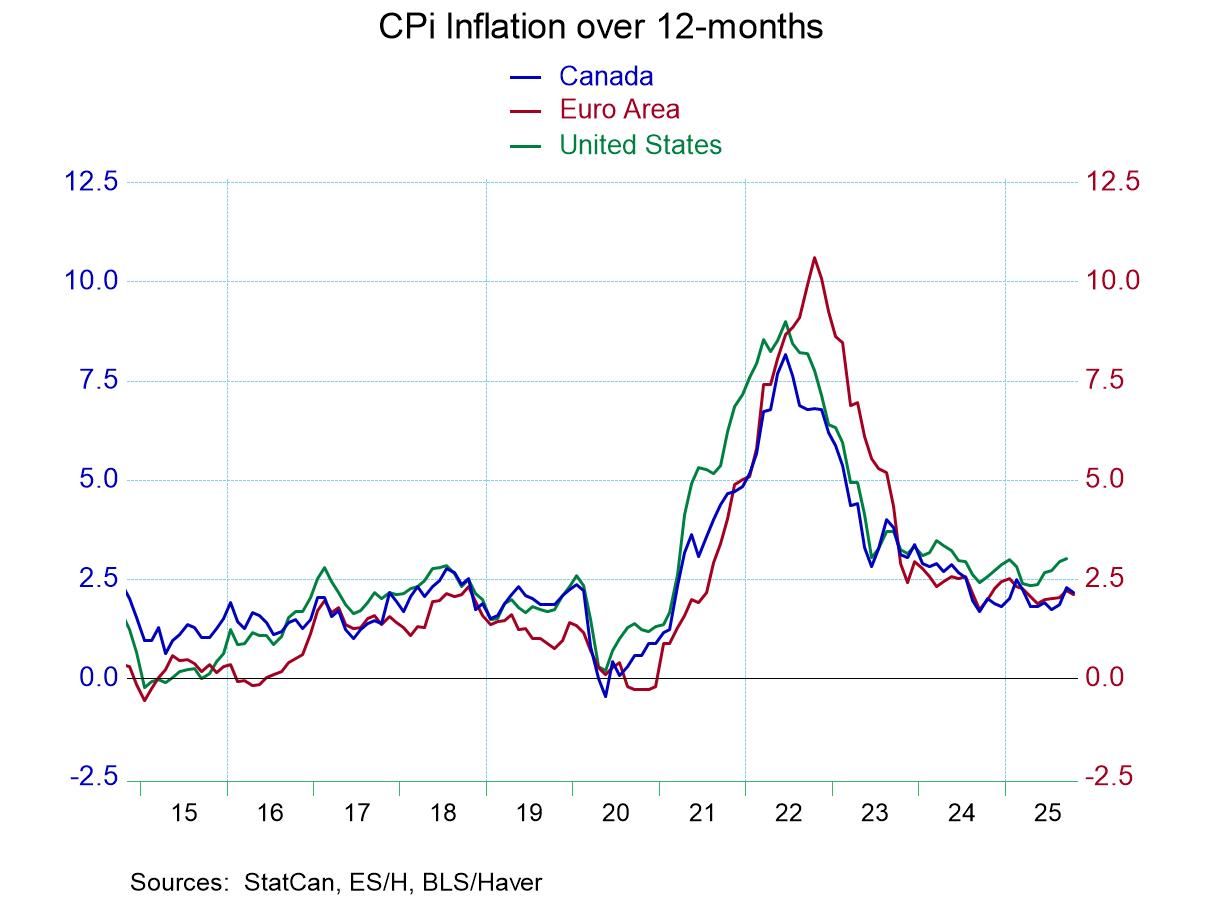

Canadian inflation is highly correlated with inflation in the US. The US and Canadian CPI's have a correlation of 0.97 on annual percentage changes. Canada's CPIx measure has a correlation with the US headline CPI of 0.94 and the Canadian core inflation rate has the correlation with US core inflation rate of 0.94. All of these measured against year over year inflation. Clearly with a good deal of trade and a long common border prices in the US and Canada have a chance to mix it up and affect one another and create some degree of homogeneity. However, none of that is really perfect. Despite the strong correlation between headline inflation and core inflation between the US and Canada, Canada's core CPI and the US core CPI have a correlation based on month-to-month changes of less than 0.2 Using an R-squared metric.

Well, it might be somewhat comforting to look at Canadian inflation, and I think it's giving some guidance for the US. That would only be true over a long period of time, but it probably doesn't provide much guidance for us in terms of what we can expect from the month-to-month changes.

While Canada's correlation with US inflation is high it's correlation with inflation in Japan it's only 0.33: only 1/3 of the variants in these two indicators is in common. In terms of the Euro-Area the correlation is less than -0.1, which tells us the correlation is negative and extremely small and of course not statistically significant.

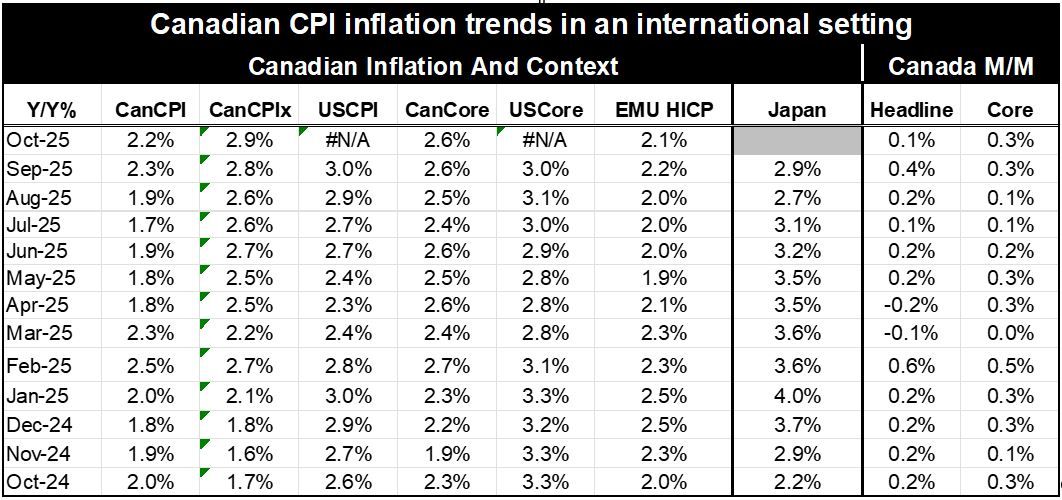

The Canadian CPIx measure shows inflation pretty flat at around 2.6% over 3 months and over 12 months. Canada's 6-mo CPI measure accelerates from 2.2% over 12-months to a 2.6% annual rate over 6-months to a 3% pace over three months. US inflation on these horizons essentially replicates what's presented by Canada's CPI X based on existing data. However, the R-squared association between the three month annualized percent change in the Canadian CPI versus the US CPI shows that they share about half of the same variation with an R-squared of about 0.5. And on this comparison Canada’s and US’ recent inflation trends appear to be highly similar.

The Bank of Canada looks at inflation using several different metrics and it also looks at inflation relative to a range unlike the US, leading to a much more measured discussion of what inflation is and how it's performing.

The decision by the Fed in the US to stick with a simple point forecast at this point is something that probably cannot be changed, at least not until the central bank is able to show that it can hit that target consistently. Even so, the Fed has not showed a great appetite for trying to express inflation in terms of a target band. However, when the Fed changed its framework agreement it did adopt something called flexible average inflation targeting (FAIT) which never really described for us or explained what it was and it has a set that approach aside I think to the pleasure of most economists.

There continues to be buzzing and differences of opinion over what the inflation target should be in the US. However, the international standard has been set at 2 per cent and at this point adopting a number different than that doesn't seem to make a lot of sense. Adopting 2% with some flexibility might make some sense but, of course, the Fed is already doing that as it's allowed a 4 1/2-year overshoot of its inflation target as it continues to cut rates. This decision, however, does not amount to a change in the Fed’s inflation targeting but rather to a set of decisions that appears to be losing the Federal Reserve credibility. Meanwhile, the Bank of Canada, operating with the range and having had much the same kind of access that the Fed has had in hitting and missing its inflation target midpoint, has emerged from this period with its credibility largely intact.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief