U.S. Home Builders Index Edges Higher in November

by:Tom Moeller

|in:Economy in Brief

Summary

- Overall reading is highest in six months.

- Current sales traffic improves; prospective sales backpedal.

- Index is mixed throughout the country.

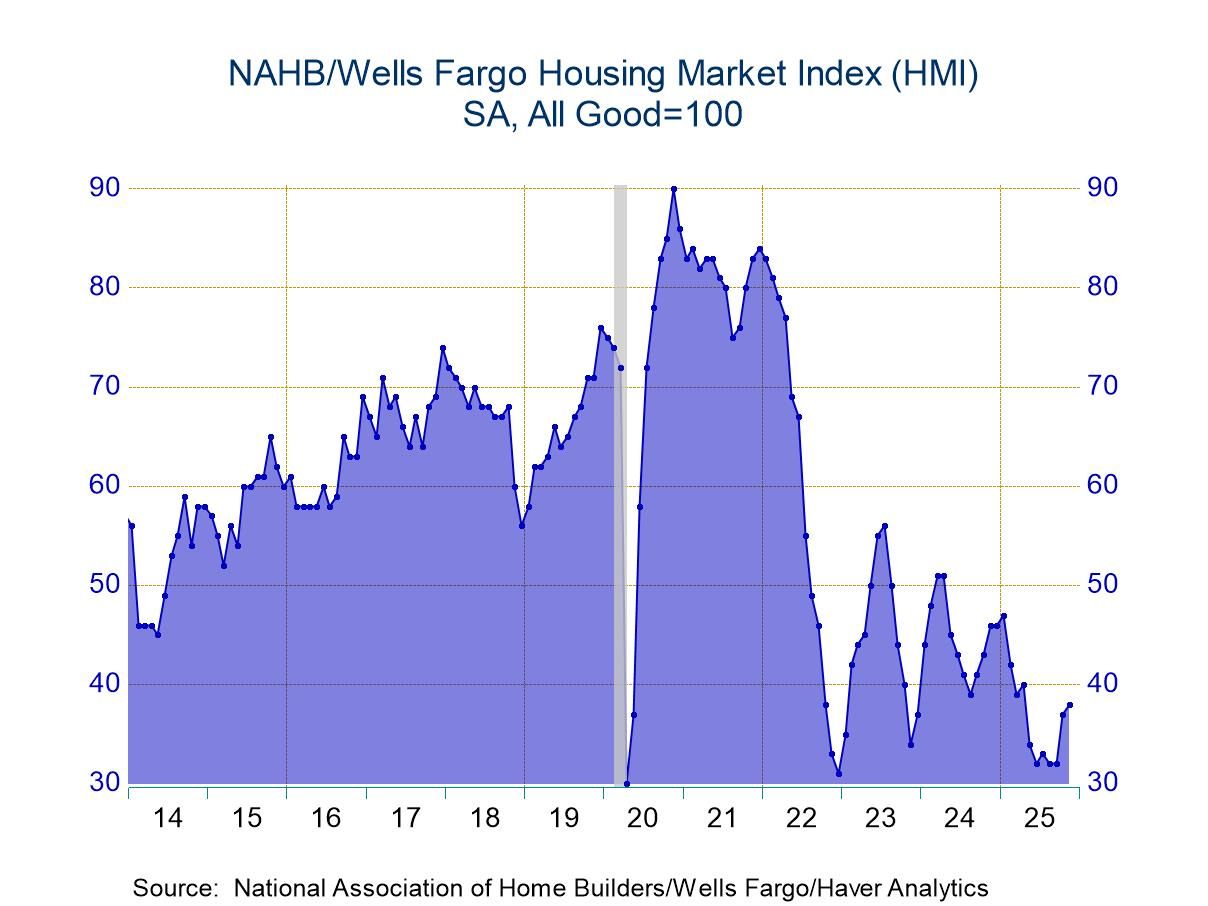

The Housing Market Index, compiled by the National Association of Home Builders/Wells Fargo, rose 2.7% (-17.4% y/y) to 38 in November after surging 15.6% in October and holding steady in September. The latest reading was the highest since April, but remained below the break-even point of 50 where it’s been since May of last year. The index also remains under a July 2023 high of 56 and a November 2020 peak of 90.

The rate on a 30-year fixed rate mortgage averaged 6.23% in the first two weeks of November versus 6.25% during all of October. It was 6.24% last week and remained below the high of 7.79% in the last week of October 2023, according to Freddie Mac.

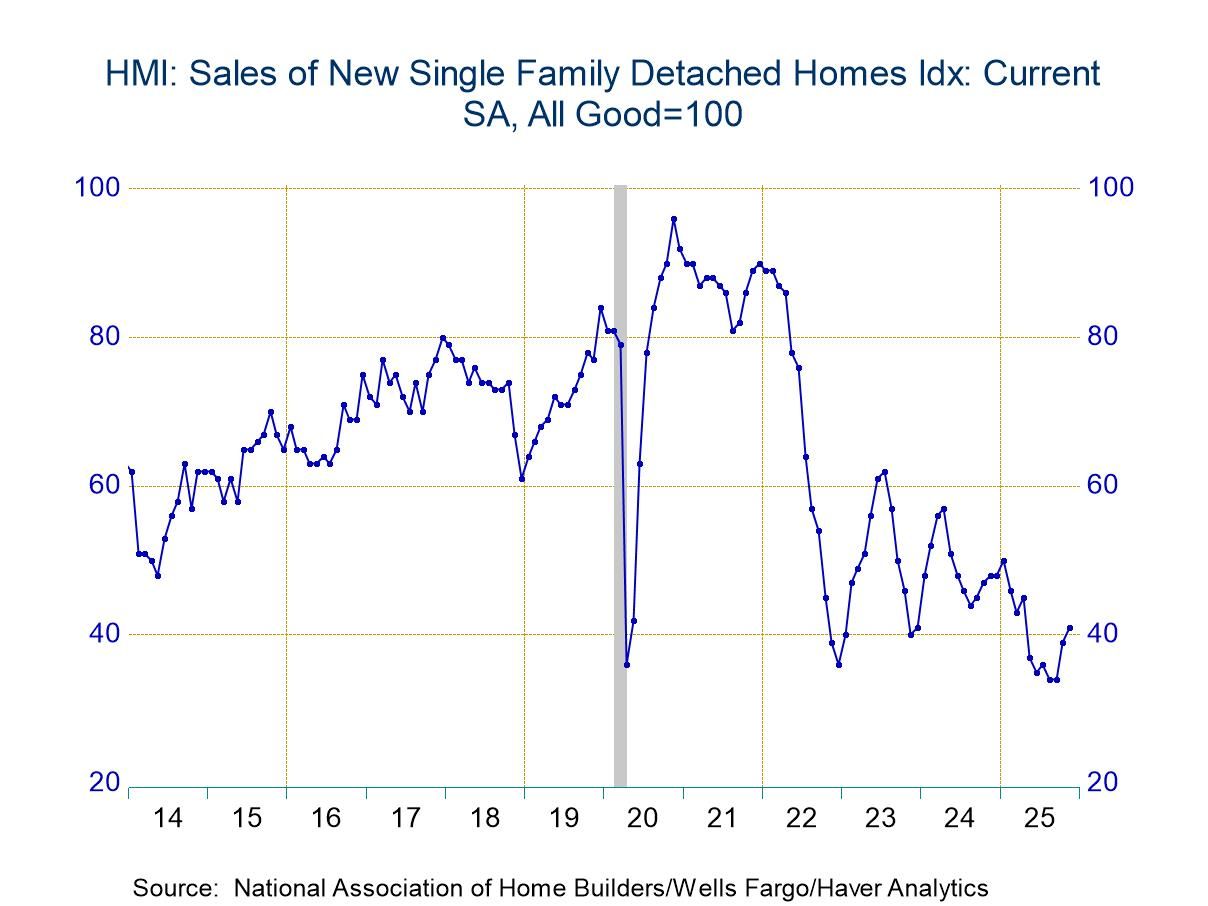

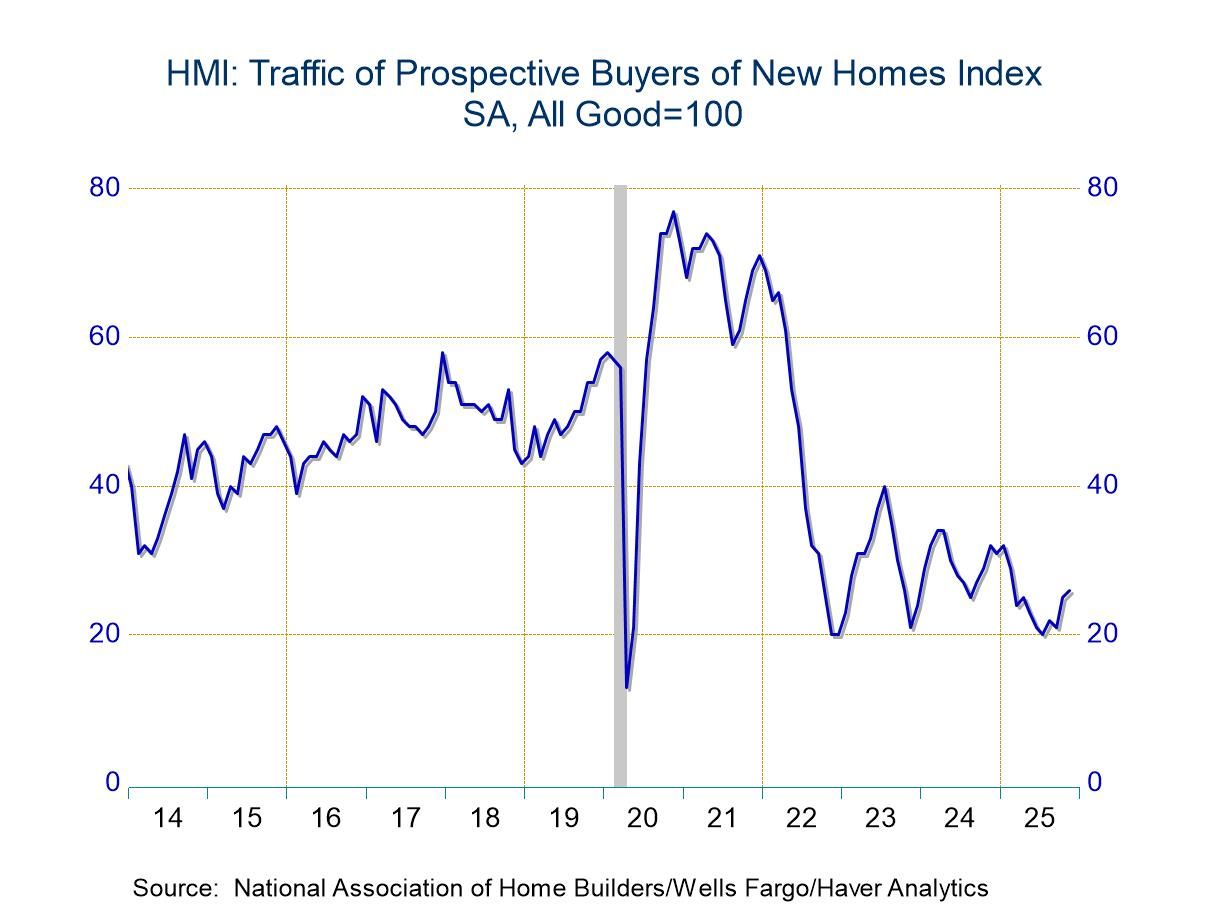

The single-family home sales measure rose 5.1% (-14.6% y/y) this month to 41, a seven-month high, after rising 14.7% in October. The prospective sales in six months measure fell 5.6% (-19.0% y/y) to 51, after rising 20.0% in October. The traffic of prospective buyers’ index rose 4.0% (-18.8% y/y) to 26 in November, after rising 19.0% in October.

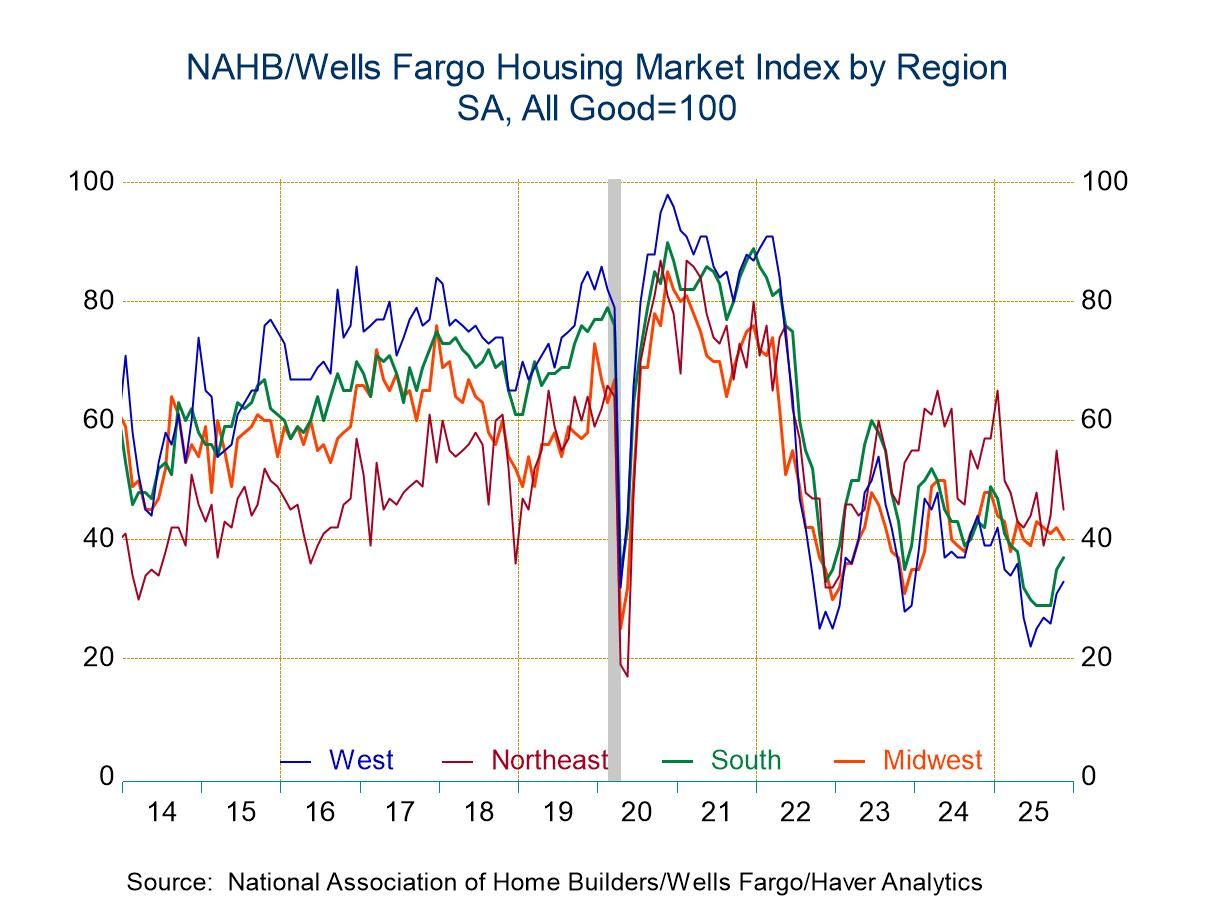

Housing activity was uneven this month across the country. The sales index in the South rose 5.7% (-11.9 y/y) to 37 after increasing 20.7% in October. In the West, the index increased 6.5% (-15.4% y/y) to 33 after rising 19.2% in October. The sales index in the Northeast fell 18.2% (-21.1% y/y) to 45 after rising 25.0% in October. In the Midwest, the sales index declined 4.8% (-16.7% y/y) to 40 after rising 2.4% in October.

The NAHB has compiled the Housing Market Index since 1985. It reflects survey questions which ask builders to rate sales and sales expectations as "good," "fair" or "poor" and traffic as "very high," "average" or "very low." The diffusion indexes with values over 50 indicating a predominance of "good"/"very high" readings. In constructing the composite index, the weights assigned to the individual index components are: 0.5920 for single-family detached sales, present time, 0.1358 for single-family detached sales, next six months, and 0.2722 for traffic of prospective buyers. The regional indexes run back to December 2004.

These data are included in Haver's SURVEYS database.

The Case for Continuing Rate Cuts from Fed Governor Christopher J. Waller can be found here.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief

Global

Global