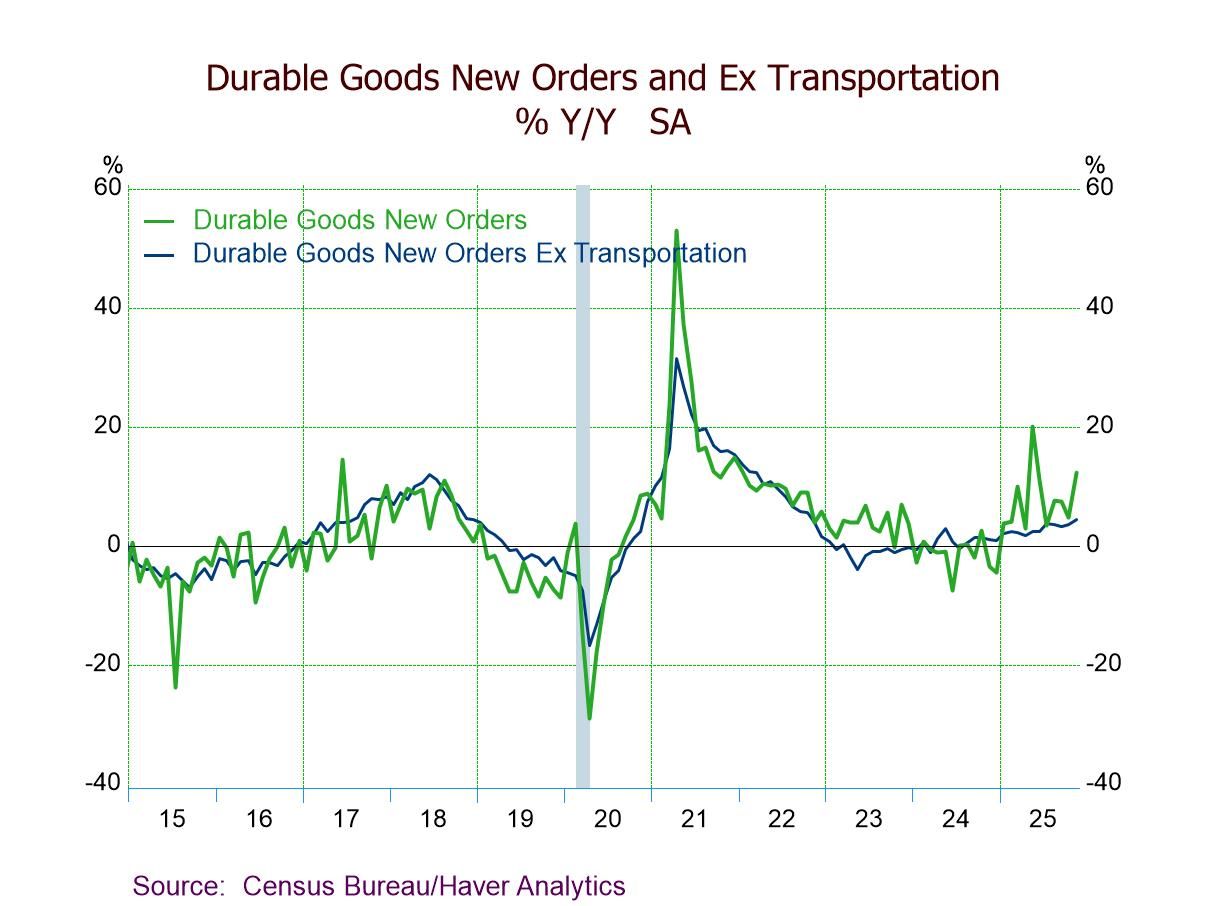

- Headline orders +5.3% (+12.3% y/y) in Nov., third m/m rise in four months.

- Nondefense aircraft orders surge 97.6% m/m vs. a 17.8% Oct. drop.

- Transportation orders rebound 14.7% m/m; orders ex transportation rise 0.5%.

- Core capital goods shipments +0.4%, sixth m/m gain in seven months, adding to Q4’25 momentum.

- Durable goods shipments -0.2%; unfilled orders +1.3%; inventories +0.2%.

Germany| Jan 26 2026

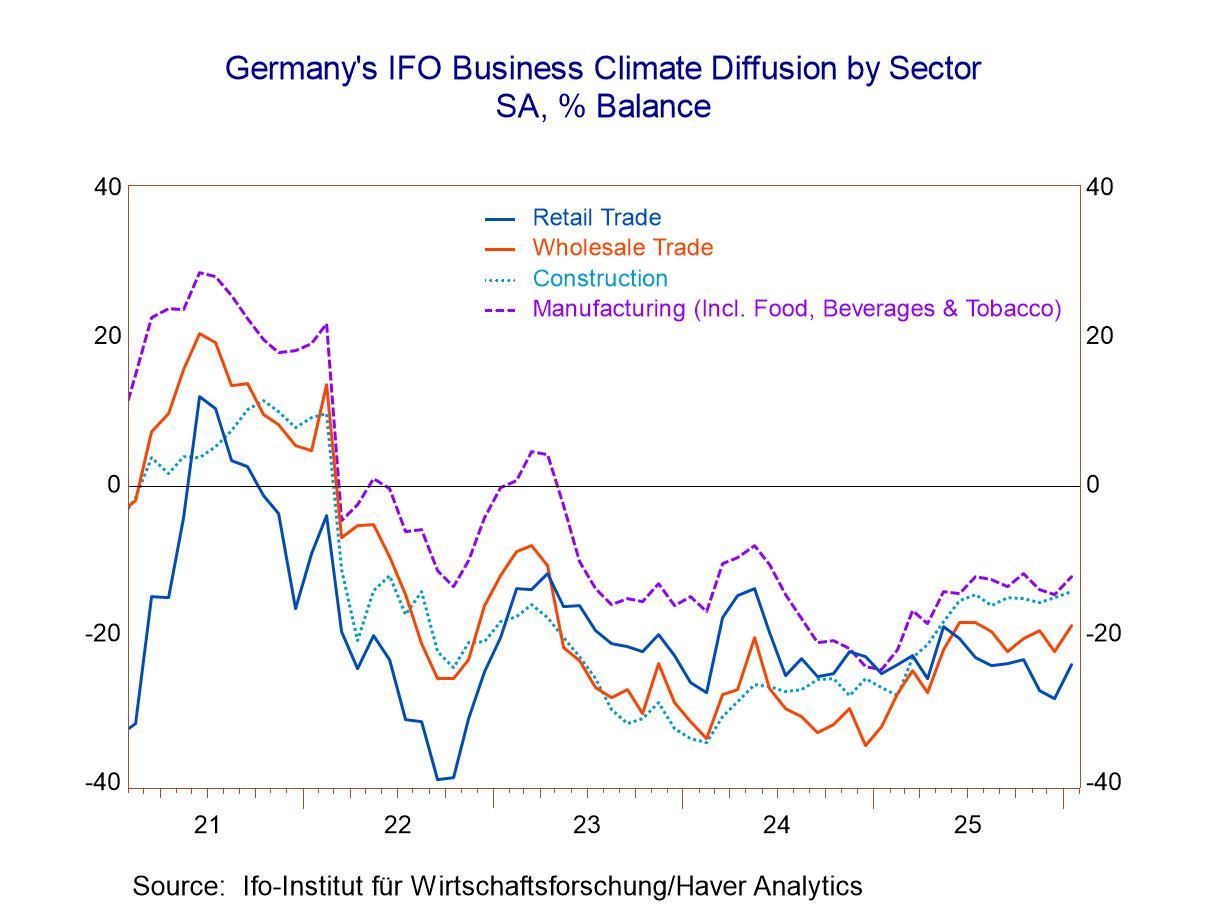

Germany| Jan 26 2026IFO Readings for Germany Mostly Waffle; Services Lag

Germany’s IFO readings in January show a bit more strength in the climate reading, nearly unchanged current conditions, and nearly unchanged expectations. These readings that tend toward small changes or unchanged readings are - and have been - characteristic of the IFO survey for most of 2025 where the various sector readings basically made some improvement through about the first quarter of the year and then pretty much flatlined for the rest of the year. Growth Dynamics in Germany have become fairly stagnant. The question is when something will occur that will light a fire under growth or, more unfortunately, send the economy back into a tailspin.

The climate readings on long-dated rankings are all weak with only one reading for construction above its 50th percentile and data back to 1993. However, on a shorter timeline looking at conditions just since February 2022 that marks the invasion of Ukraine, we have the climate reading at a 63.8 percentile standing, construction at an 89.4 percentile standing and wholesaling at a 72.3 percentile standing. Manufacturing also manages a positive standing at its 55.3 percentile.

Month-to-month in January, there are small changes afoot across the five sectors and all of them show some modest improvement except for services that backtrack slightly moving from a reading of -2.1 in December to -2.6 in January.

Current conditions show almost no change at all with a -4.8 reading in January compared to a -4.9 reading in December. Across sectors in January, there's about a two-point improvement in manufacturing, a small improvement in construction and more sizable improvement in wholesaling, a small improvement in retailing, and a step back for services.

For current conditions, the percentile standings on the long-view to 1993, again, show only construction with a reading above its 50th-percentile - that is, above its historic median - at 61.6%. The all-sector reading has only a 11.9 percentile standing which is quite weak and generally weaker than the individual sectors. That fact simply underpins the notion of how this coincident-weakness across all the sectors is unusual because the all-sector index has a weaker ranking than any of the individual industries or sectors on the long timeline. On the shorter timeline, construction, again, is at a 59.6 percentile reading, above its 50th percentile, wholesaling comes close at a 48.9 percentile, reading retailing is exceptionally weak at a 4.3 percentile reading, and services are at a 10.6 percentile rating also quite weak. The current index is dominated by weakness.

Expectations in January show a step back for the overall reading and that's based on weakness in services. There are nearly 3-points of improvement in manufacturing, unchanged readings in construction, a slight improvement in wholesaling, a sizeable 6-point improvement in retailing, and a weaker reading from services, which back off by half a point on the month. The percentile standings when data are ranked over the long period to 1993 show everything below the 50th percentile; all rankings are below their historic medians on that timeline. However, when compared to February 2022, marking the invasion of Ukraine, all of the readings are above their 50th percentile, generally in about the 80th or 90th percentiles, except for services that only manage a ranking in the 55th percentile.

Asia| Jan 26 2026

Asia| Jan 26 2026Economic Letter from Asia: Forecasts, Chips, and Polls

This week, we take stock of key developments across Asia. The IMF’s latest outlook delivered several positive growth revisions, with India once again seen at the forefront of regional expansion, while China is still seen unlikely to reach a 5% growth target this year should it be adopted (chart 1). Between China and the US, a clear divergence in trade strategies persists. China has continued to pivot toward Asia to sustain relatively robust export growth, while the US has turned inward—effectively narrowing its trade deficit in line with President Trump’s objectives (chart 2). Within Asia, trade ties with China have become increasingly two-way, as China’s share as an export destination has risen steadily over the past decades to rival that of the US for many economies (chart 3).

In the AI space, notable developments emerged following reports that Chinese authorities may soon formally allow domestic tech firms to import Nvidia’s H200 chips. The news could provide a boost to US tech equities, although broader geopolitical risks remain a possible resurgent drag on sentiment (chart 4). Turning to Japan, last week’s Bank of Japan (BoJ) meeting left policy rates unchanged, as expected. However, the BoJ’s latest outlook report delivered upgrades to both growth and inflation forecasts—developments that could pave the way for further monetary tightening (chart 5), albeit likely only after near-term uncertainties, most notably upcoming snap elections, have passed. Ahead of the polls, the yen and Japanese government bonds have come under sustained pressure (chart 6), though short sellers may become more cautious given the risk of official intervention.

The IMF’s World Economic Outlook The International Monetary Fund (IMF) unveiled its updated forecasts last week in its World Economic Outlook (WEO) publication. On growth, World GDP growth for 2026 was revised up by 0.2 ppts to 3.3%, driven by a surge in technology investment, including AI. China and India each saw a 0.3 ppt upgrade to their growth forecasts, while Japan and South Korea received more modest 0.1 ppt upgrades. Within Asia, India continues to be seen as the region’s growth leader (chart 1). By contrast, despite the IMF upgrade, China is still not expected to reach 5% growth this year should it re-adopt such a target, though there has been some discussion of a lower target range of 4.5–5%. On the downside, only a handful of economies saw downgrades; in Asia, the Philippines stands out with a 0.1 ppt downward revision to 5.6% for the year.

Global| Jan 23 2026

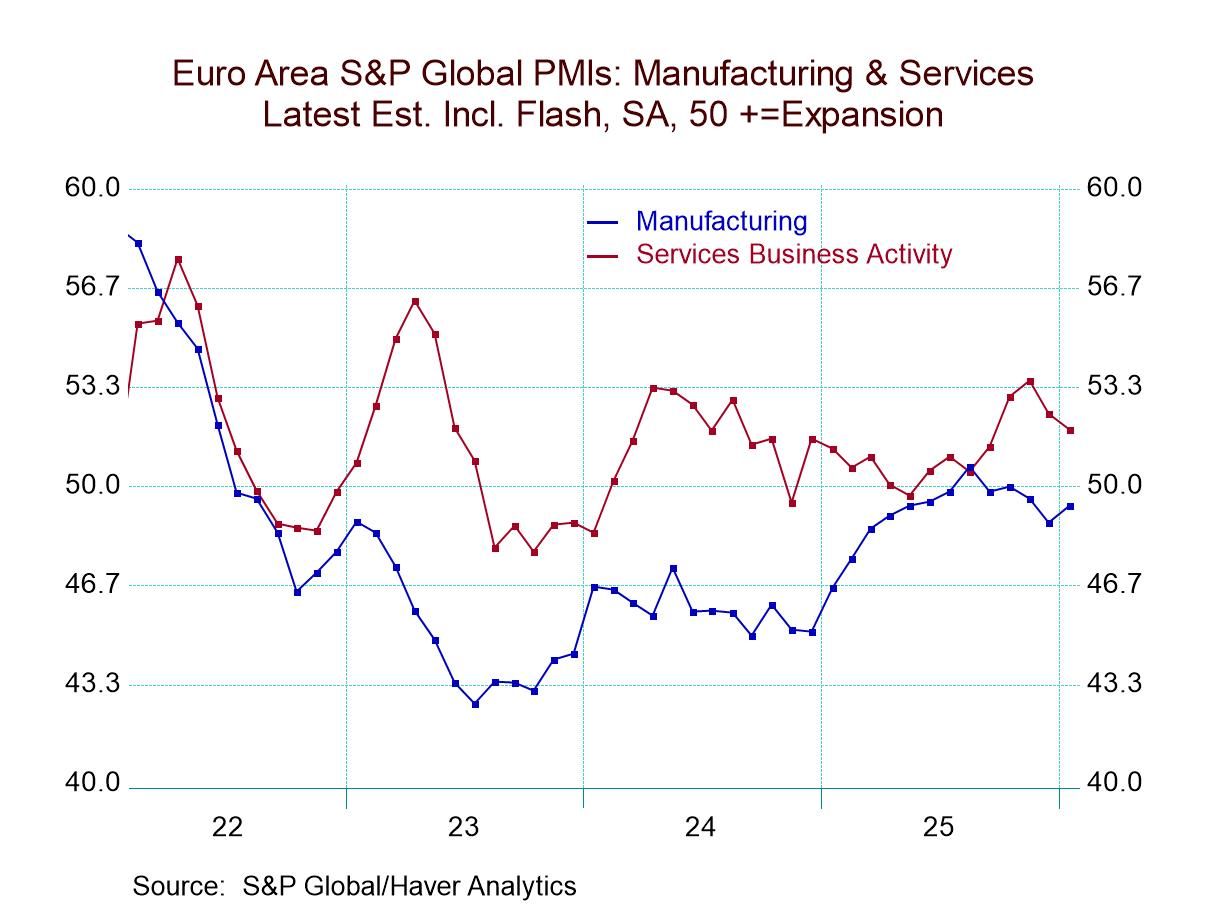

Global| Jan 23 2026S&P Flash PMIs Rebound But Emit No Clear Signal

The S&P PMIs for January show flash readings that indicate broadly stronger conditions across the early reporters in this table. Exceptions are the European Monetary Union as a whole with its composite reading weaker and France with its composite reading weaker, but Germany, the United Kingdom, Japan, Australia, India, and the United States all have composite readings that are stronger month-to-month in January. With these eight countries, there are 24 readings in each period, three for each country: a composite, one for manufacturing, and one for services. Among these 24 readings, only five of them were weaker month-to-month in January. Of course, this follows a December when only 6 of the readings were stronger month-to-month.

The sequential readings, that we calculate only off hard data (which means that calculations are done from December backward) are still mixed. Substantially weaker conditions period-to-period are reported comparing three-months to six-months. Over three months, only nine of the 24 readings are stronger whereas over six months only one of the 24 readings is weaker when compared to the 12-month average. Over 12 months, the average is stronger than it was one-year ago in 15 of the 24 readings.

Only the United States and France have service sectors that are below their medians over this period back to 2022. Only France and India have composite readings that are below their respective medians over this period. But by comparison, there are very strong composite readings as well. There is a 91-percentile standing on the composite in Australia, an 87-percentile standing in Japan and the United Kingdom. The German composite has a 79-percentile standing.

The recent data have been running sporadically hot and cold, making it difficult to make sense out of what's happening. But broadly, it's clear that the PMIs in the European Monetary Union have been working their way higher and this is the general theme.

For the 8 reporters in the table back to January 2022, all of them except India show weaker manufacturing readings in January 2026 than what they showed in January 2022. But January 2022 was, of course, part of the COVID recovery move. Manufacturing in the European Monetary Union slipped from its high point over this period to its low point around mid-2023.

Global| Jan 22 2026

Global| Jan 22 2026Charts of the Week: Seeing Green

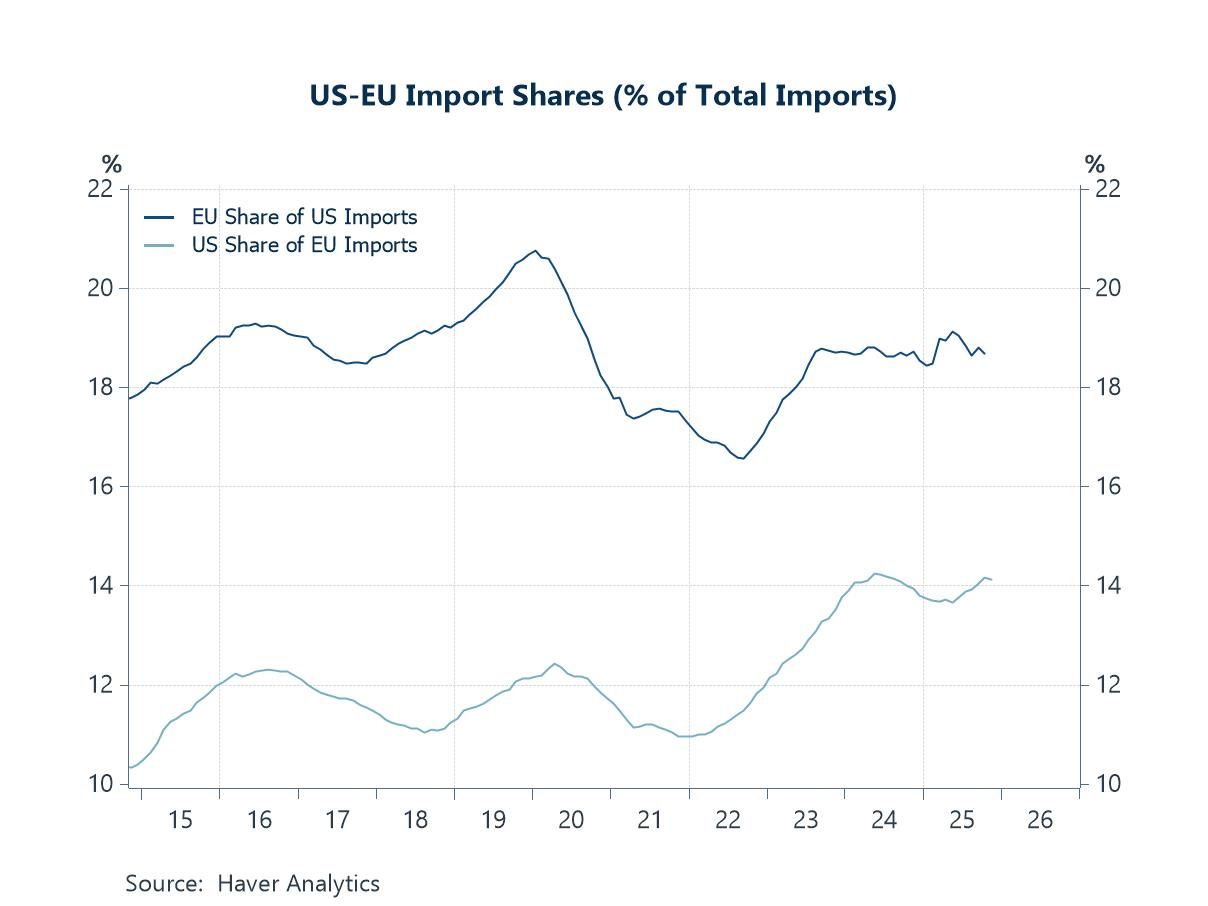

This week’s data and market moves have been framed by an abrupt escalation in geopolitical tensions surrounding Greenland, which has served as a catalyst for broader financial unease rather than a standalone shock. The episode has sharpened investor focus on US policy predictability, amplifying concerns already evident in the charts on EU–US trade exposure, where tariff threats risk feeding directly into confidence effects and capital flows. At the same time, recent turbulence in Japanese government bonds appears to have been an underappreciated driver of the sell-off in US Treasuries, highlighting how global capital reallocation—rather than geopolitics alone—has contributed to higher US yields. These forces intersect with growing questions around the durability of US monetary credibility, as inflation expectations have shown signs of decoupling from traditional oil-price anchors, raising the sensitivity of markets to any perceived constraints on the Federal Reserve. Beyond the US, UK data delivered a modest upside surprise in headline inflation, with persistent services and wage pressures reinforcing a cautious policy backdrop for the Bank of England. In China, meanwhile, Q4 GDP growth of 4.5% y/y kept full-year expansion aligned with the government’s target, but continued weakness in the property sector remains a significant drag on investment and household confidence. Taken together, the week’s developments point to a global outlook increasingly shaped by geopolitical risk, capital-flow dynamics and domestic structural constraints, rather than by straightforward cyclical momentum alone.

by:Andrew Cates

|in:Economy in Brief

USA| Jan 22 2026

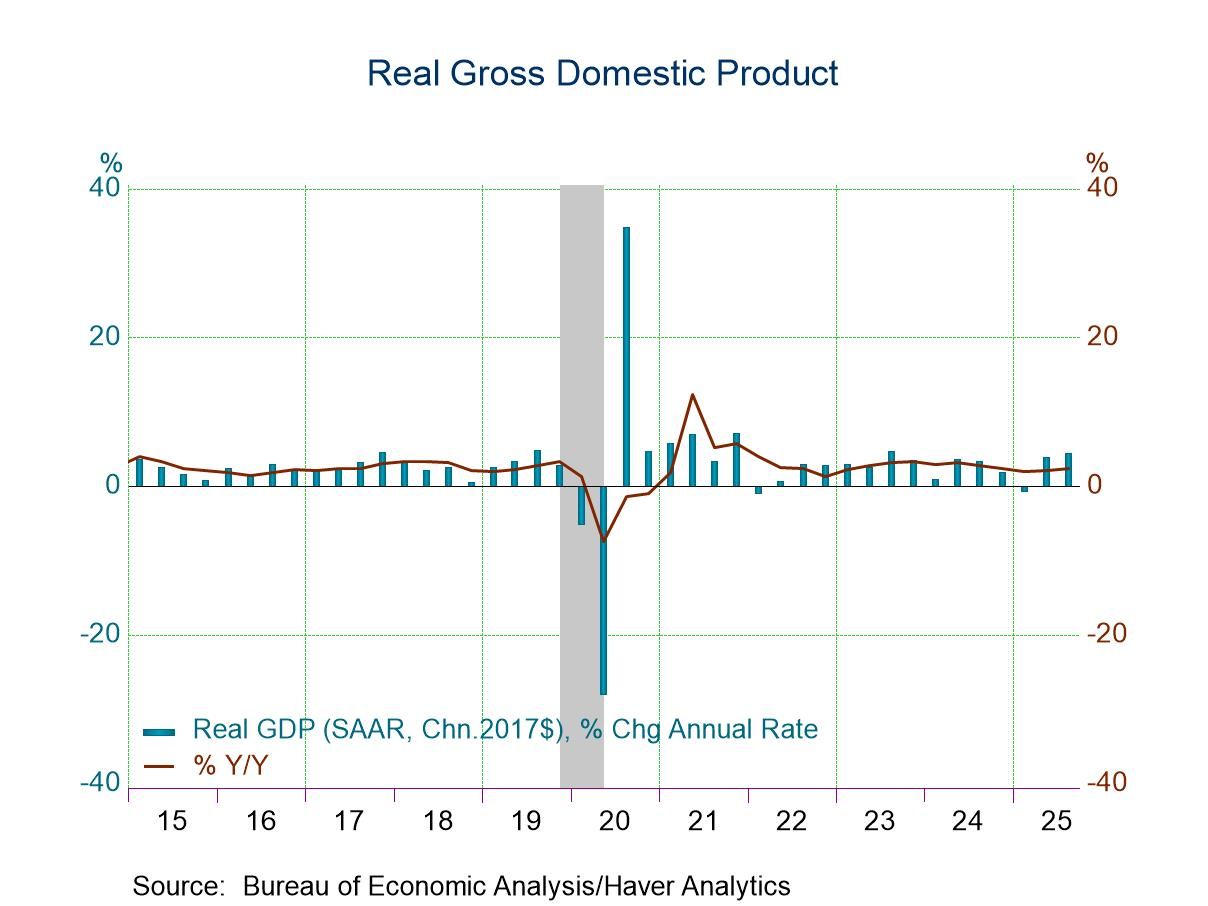

USA| Jan 22 2026U.S. Q3 GDP Growth Revised Slightly Faster

- Real GDP grew 4.4% q/q saar in Q3 2025, up slightly from 4.3% previously reported.

- The modest upward revision was due mostly to slightly stronger nonresidential fixed investment, a larger increase in exports and a smaller decrease in inventories.

- Growth of domestic demand remained solid in Q3 but was revised down 0.1%-point.

- GDP and PCE inflation were unrevised at 3.8% and 2.8%, respectively. Both are meaningful accelerations from Q2.

by:Sandy Batten

|in:Economy in Brief

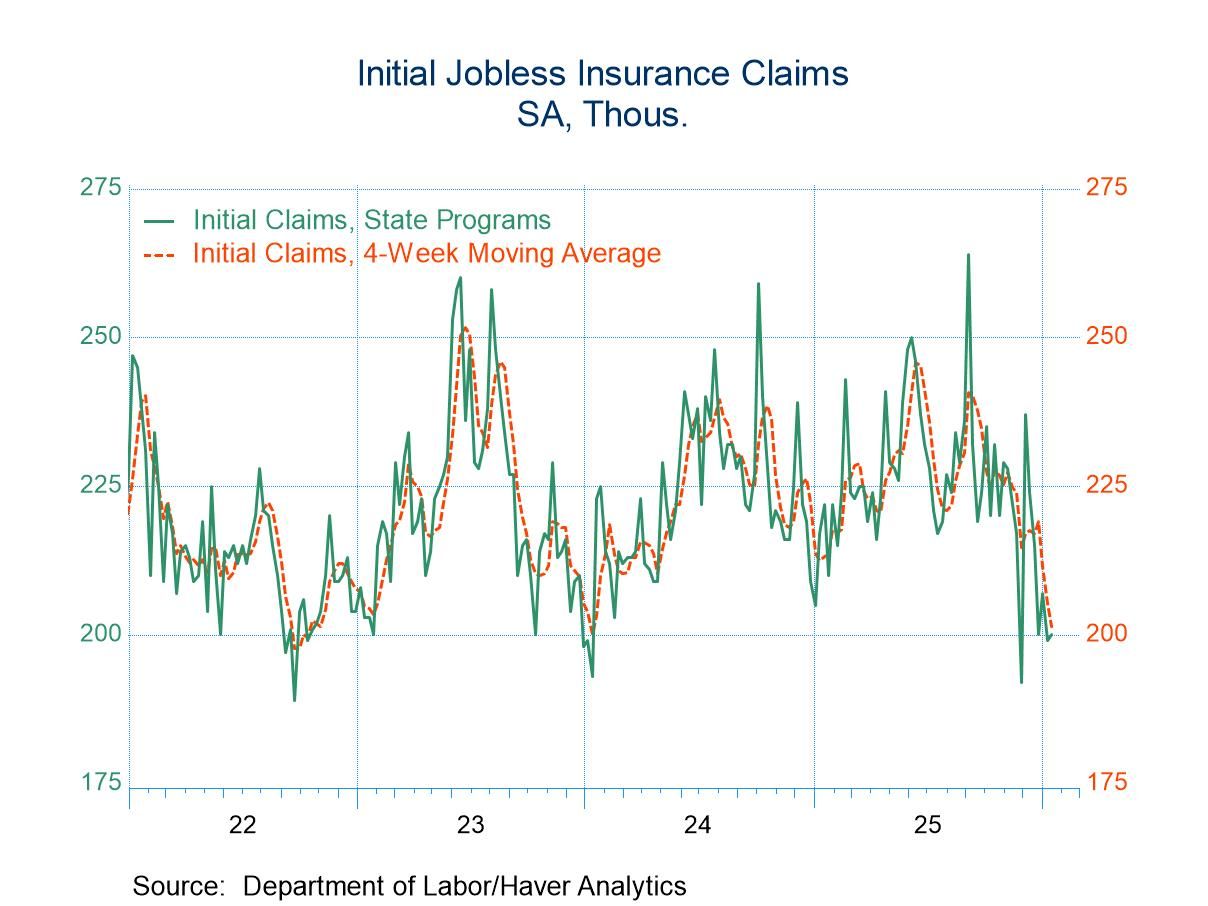

Initial claims for unemployment insurance edged up 1,000 to 200,000 in the week ending January 17, from 199,000 in the week ending January 10, revised from 198,000. The four-week moving average of initial claims was 201,500 in the January 17 week, down 3,750 from 205,250 in the January 10 week, revised from 205,000, and reaching the lowest level for this average since January 13, 2024, when it was 200,000.

Federal government employees initially filed 1010 (NSA) jobless insurance claims in the week ended January 10, after filing 646 (NSA) claims in the week ended January 3.

The total number of unemployment insurance beneficiaries – also known as “continuing claims” –decreased by 26,000 to 1.849 million in the week ended January 10 from 1.875 million in the week ending January 3, revised from 1.884 million. The four-week moving average was 1.871 million in the latest week, down from 1.887 million in the January 3 week, revised from 1.889 million. The insured unemployment rate remained at 1.2% in the week of January 10, unchanged from previous 6 weeks.

Federal government employees’ continuing benefits claims were 12,977 (NSA) in the week ending January 3, from 12,803 (NSA) in the week of December 27.

The insured unemployment rate varied greatly across individual states and territories. In the week ending January 3, the highest unemployment rates were in Rhode Island (3.27%), New Jersey (3.17%), Washington (2.85%), Minnesota (2.75%), Massachusetts (2.74%), Oregon (2.37%), Connecticut (2.31%), Montana (2.26%), California (2.21%), and Alaska (2.06%). The lowest rates were in Florida (0.29%), North Carolina (0.40%), and Louisiana (0.43%). Rates in other notable states include New York (2.28%), Pennsylvania (2.23%), Illinois (2.21%), and Texas (1.14%). These state data are not seasonally adjusted.

Data on weekly unemployment claims are from the Department of Labor itself, not the Bureau of Labor Statistics. They begin in 1967 and are contained in Haver’s WEEKLY database and summarized monthly in USECON. Data for individual states are in REGIONW back to December 1986.

Belgium| Jan 22 2026

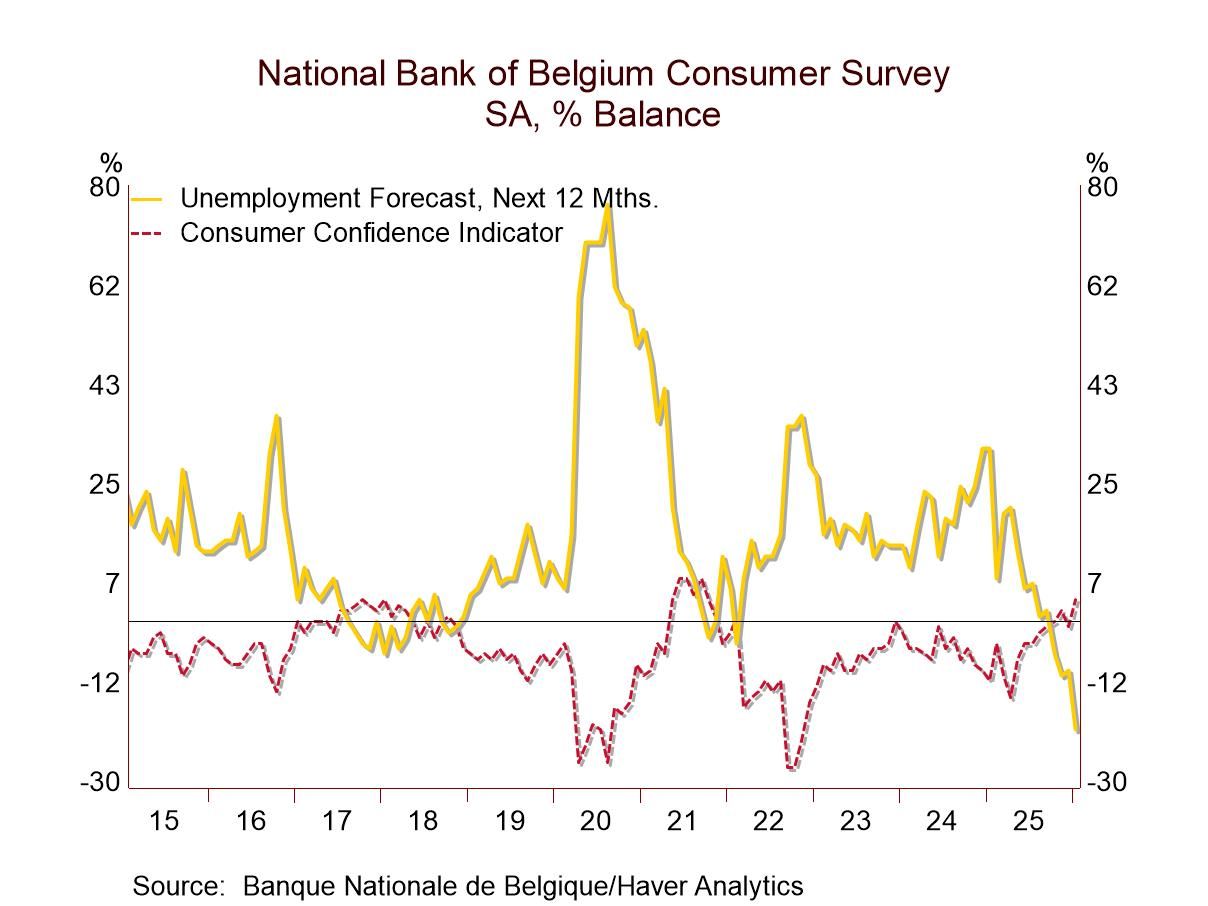

Belgium| Jan 22 2026Belgian Consumer Confidence Up and Strong; Fear of Unemployment at 35-Year Low! Is That Possible?

The National Bank of Belgium index for January 2026 rose to +4 from -1 in December, stronger than its November 2025 reading of +2. The survey value is exceptionally strong, lying in the top 6% of all observations back to 1991, even as the survey contains significant variations that range from strong to quite weak across its various components. What is most notable is that the index itself is extremely high-ranking; the current situation appraisal is also quite high-ranking; and, that the forecast for unemployment embedded in this survey is at a 35-year low. Considering current circumstances, against the events of the last 35 years, that's a rather remarkable finding especially considering the world situation.

The times, they are a changin’ was Dylan 50 years early? These have been remarkable times in a number of different ways with a clear transition from the circumstances of the post-war period under way. The solidarity of the NATO alliance is clearly in a situation in flux, revealed since Russia invaded Ukraine. Prior to that, the Europeans had resisted putting more money into the NATO pot as the United States had been frantically asking them while it funded most of the security umbrella. Now, in the wake of these new events, and with the changes to the global stage wrought by climate shifting, the U.S. finds Greenland to be a more important piece on the geopolitical chess board and wants to have more say there in order to protect its own flank as Arctic ice packs recede. This is after a period when NATO basically failed to engage in the front-line protections of its own doorstep that the U.S. had thought were necessary. Not surprisingly, the U.S. found that whole episode unsatisfactory and is now reluctant to give up control to NATO of what it regards as the protection of its own back door for the area around Greenland. But at last, Europe and the U.S. appear to have a deal or the makings of one, so, stay tuned. Maybe all civility is not lost.

Geopolitical shifts meld with economic issues to change the landscape Geopolitical shifts are part of the problem because geopolitics and economics help shape one another. And there has been a great deal of economic turmoil as well. The U.S., after reassessing the Post War order, is bringing back to life tariffs, in order to try to get economic leverage after running 33 consecutive years of current account deficits under what people want to call a free trade system. The U.S. finds itself with a still very overvalued dollar and in a situation where its current account deficits are poised to continue to run high and perhaps get higher. Economists say tariffs are not the solution, but maybe they ARE the wake-up call that will lead to a solution? Europeans have also shifted to embracing a larger and larger government sector and ever larger fiscal deficits and more fiscal debt while absorbing migrants. This is constraining its ability to have any kind of a flexible macroeconomic policy and is a severe problem already for the U.K. and France. And these changes are wreaking havoc with what has been a very solid post-war Atlantic alliance.

Views change But the changes that the U.S. has pushed on to the system from its geopolitical adventurism to its use of tariffs and other strong rhetorical comments have led economists to focus on the elevation of uncertainty in the economic system. Elevating uncertainty has an adverse impact on the economy and on growth. I mentioned this with the obvious caveat that this warning by economists seems to have been completely wrong. U.S. growth has turned out to be quite resilient and even strong. It is not the only adamant position that has proved to be wrong and malleable. Despite the reality of climate change, the view that once took carbon as the main and unequivocal climate change agent, itself is shifting. Opposition to carbon has dwindled, more as the U.S. is embracing nuclear power. Artificial intelligence is becoming a strong bet for stronger growth in the future, and this explains why there have been so many shifting views on energy since artificial intelligence requires massive amounts of energy and would make it impossible to make progress on carbon and to push ahead with the AI agenda at the same time. So, instead of delaying AI, the view on carbon had to go. So much for ‘science.’

Why are Belgians so satisfied? The finding that in Belgium consumer confidence has risen sharply in this environment and fears of unemployment are the lowest they've been in 35 years is another shocking development in this pantheon of incredible and shocking changes. As the above discussion points out, a lot is changing and NATO is at odds with the U.S., its lynchpin. Yet, there is no clear increase in uncertainty in Belgium, while they maybe more in Brussels.

The Belgian Survey: strong despite waffles Belgians do not read the economic situation over the next 12 months as that strong at a reading of -29 on the survey; it has weakened over the last few months, and the economic situation assessment is only at its 8.3 percentile, an extremely weak standing. Price trends are the opposite; they have eased somewhat in the recent months, but over the next 12 months the assessment still has a top 14-percentile evaluation. It is in this context that the unemployment forecast, which is the lowest in 35 years, emerges as surprising. The environment to make major household purchases over the next 12 months is only a mid-range at a 45.7 percentile standing. And people rate their financial situation over the next 12 months slightly better than at the end of last year but at only a 34.2 percentile standing. However, the appraisal of the current situation moved up sharply in January and has a 97.7 percentile standing, which is extremely strong.

- of2725Go to 36 page