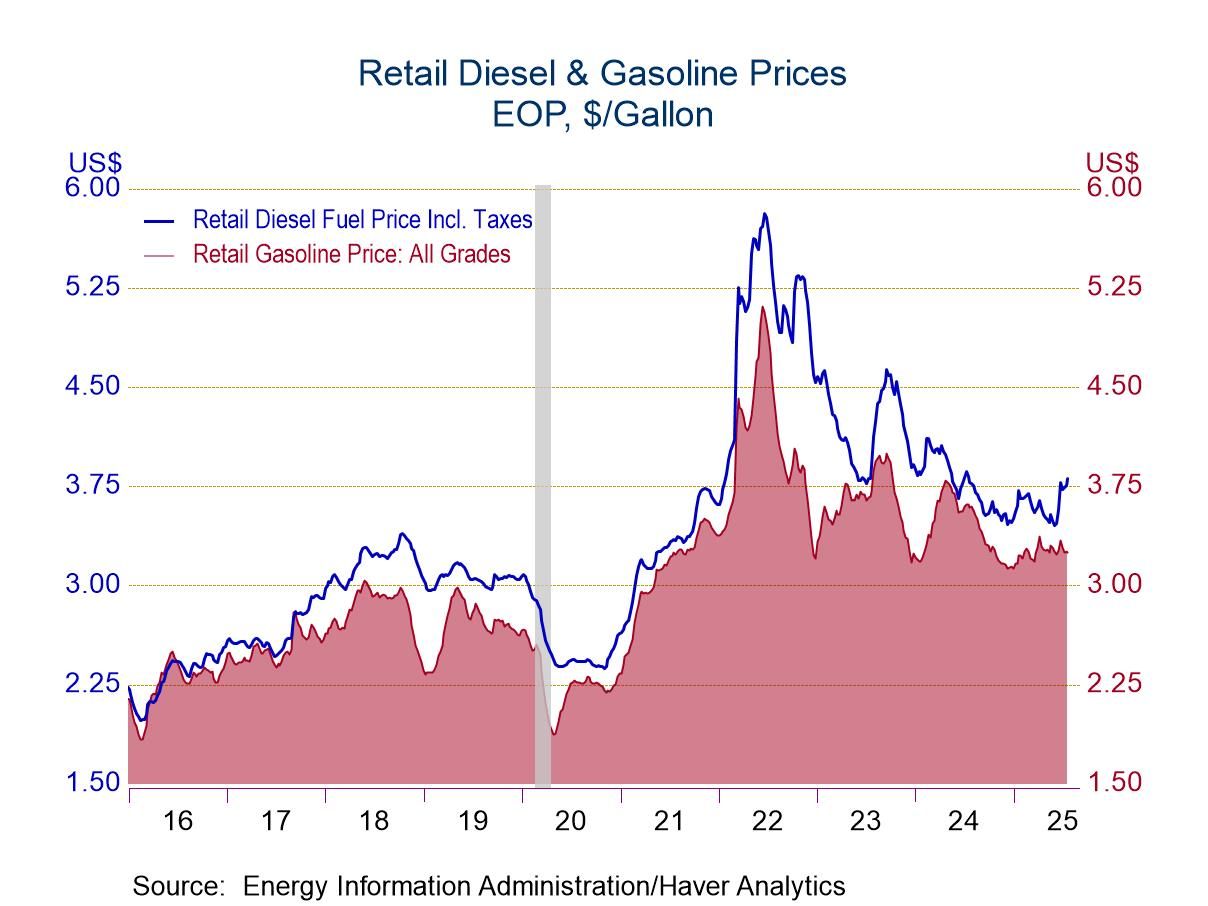

- Gasoline prices hold steady.

- Crude oil prices decline.

- Natural gas prices strengthen.

USA| Jul 22 2025

USA| Jul 22 2025U.S. Energy Prices Are Mixed in Latest Week

by:Tom Moeller

|in:Economy in Brief

- Prices movement by category is mixed.

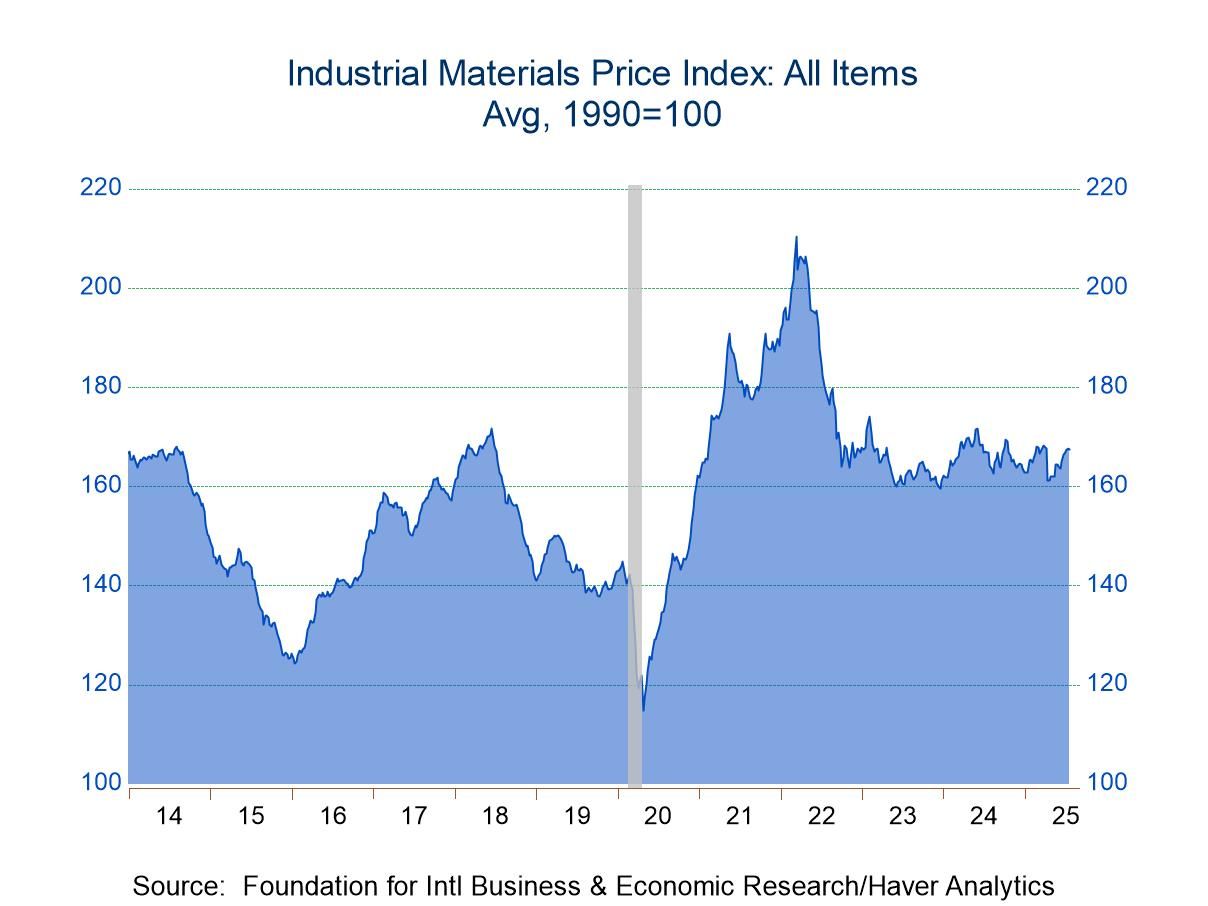

- Lumber & metals prices strengthen.

- Crude oil prices decline.

by:Tom Moeller

|in:Economy in Brief

USA| Jul 18 2025

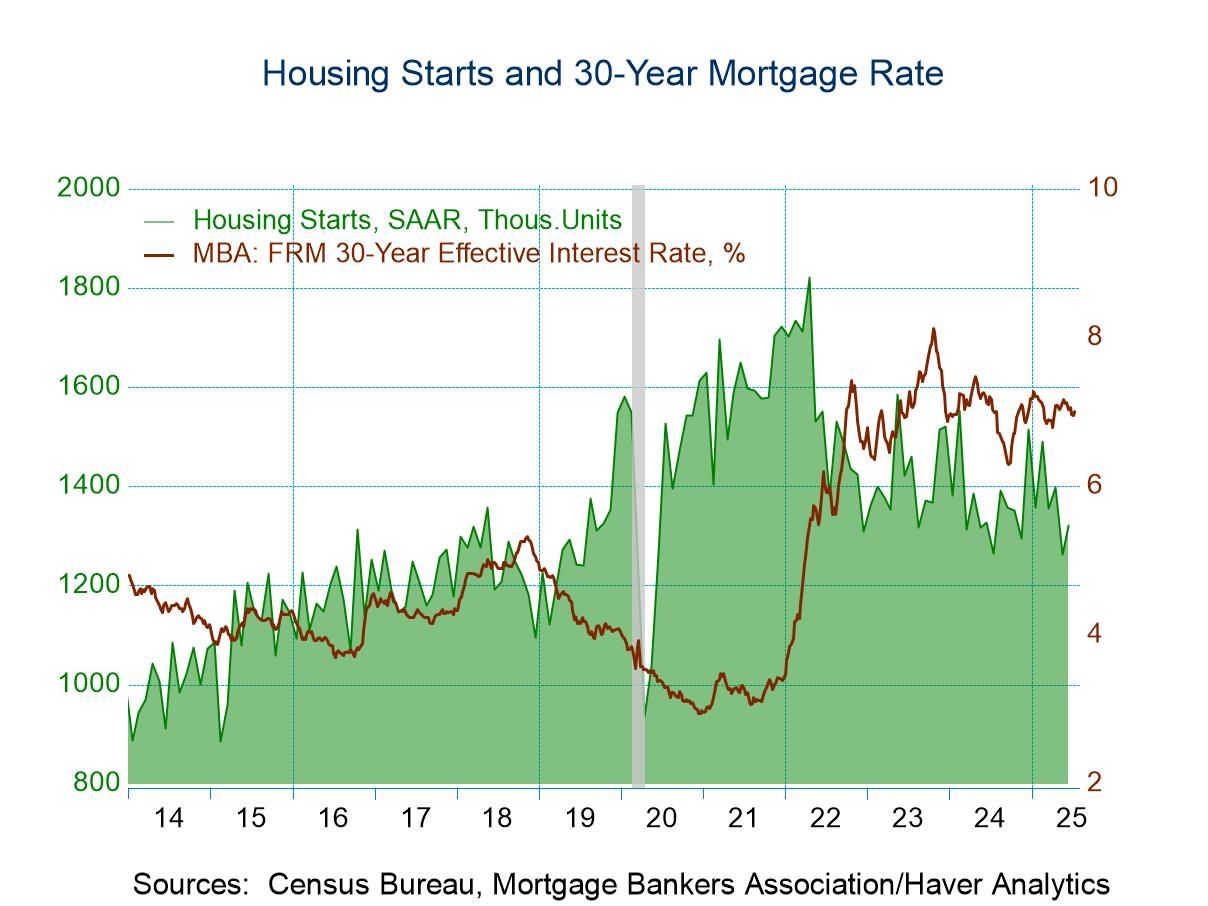

USA| Jul 18 2025U.S. Housing Starts Rebound in June

- Increase recovers half of prior month’s drop.

- Multi-family starts surge but single-family starts fall.

- Building permits rise negligibly after two months of decline.

by:Tom Moeller

|in:Economy in Brief

Japan| Jul 18 2025

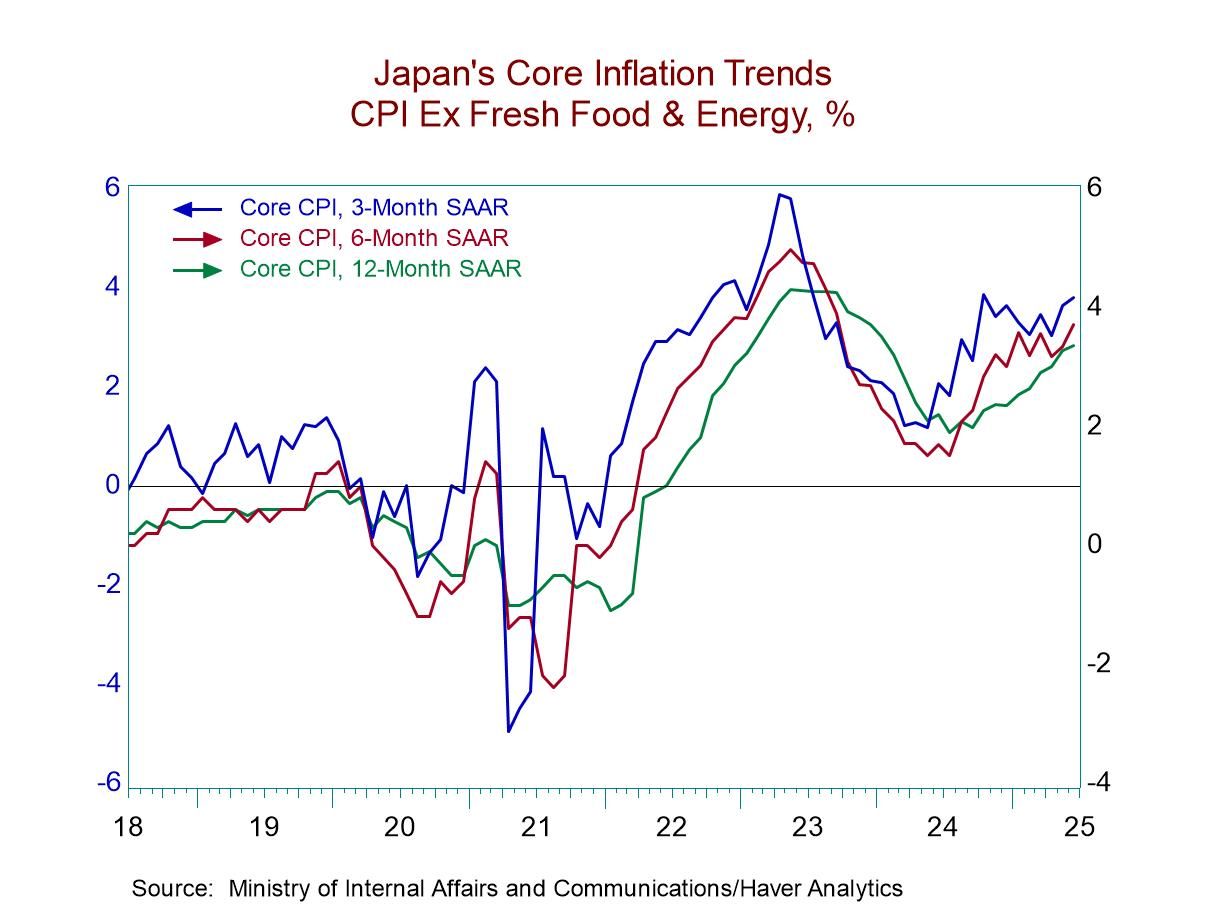

Japan| Jul 18 2025Japan’s Ex-Fresh-Food Ex-Energy Inflation Runs Hot

No one will be critical of Japan’s efforts to free itself of its torpor into disinflation and deflation that it suffered for many years. The Bank of Japan struggled long and hard to remove the contraction in prices from its economy since falling prices can have a pernicious effect on growth and investment. Japan still faces challenges: it has a contracting population and faces dealing with tariff demands from the United States as negotiations on that front continue to drag and have become harder to settle than Japan had expected. Despite the current inflation overshoot, on data back to January 2011, Japan’s to-date inflation is only averaging 1%; that is still well below its 2% target and ample reason for the Bank of Japan to continue to move carefully to corral inflation especially if inflation has stopped accelerating – as it seems to have done. Against this background, we look at Japan’s CPI report.

Current inflation: June Japan has dispatched deflation and currently faces an inflation problem. In June, the BOJ’s preferred gauge for the CPI excluding fresh foods & energy rose 0.4% month-to-month for the second month in a row; it rose by 0.2% in April. Japan’s headline inflation rate seems to have fallen into line A traditional ‘core reading’ excluding all food & energy flies under the BOJ’s target pace. But the BOJ’s preferred inflation gauge shows a 3.4% rise over 12 months and then gains at a pace of 3.7% over both six months and three months. All of those numbers are too hot to handle.

Line-items Education costs in Japan are falling sharply and sequentially. Medical care costs are deescalating too. And while food & beverage prices continue to overshoot, 2% by a wide margin, the pace of total food & beverage inflation has been falling. No broad category has steadily accelerating inflation. But the BOJ’s preferred gauge of inflation, a specialized core measure excluding energy & fresh foods, sees inflation ramping up and staying high over three months and six months.

Diffusion/breadth Among the eight major categories, year-on-year inflation has accelerated compared to where it was one-year ago in four of the eight. Inflation is above the 2% benchmark for four of eight categories as well.

Acceleration or not... The chart on sequential inflation for the BOJ’s preferred core gauge shows that this measure has accelerated since August or December of last year and since then has more or less marked time oscillating without any clear trend.

USA| Jul 17 2025

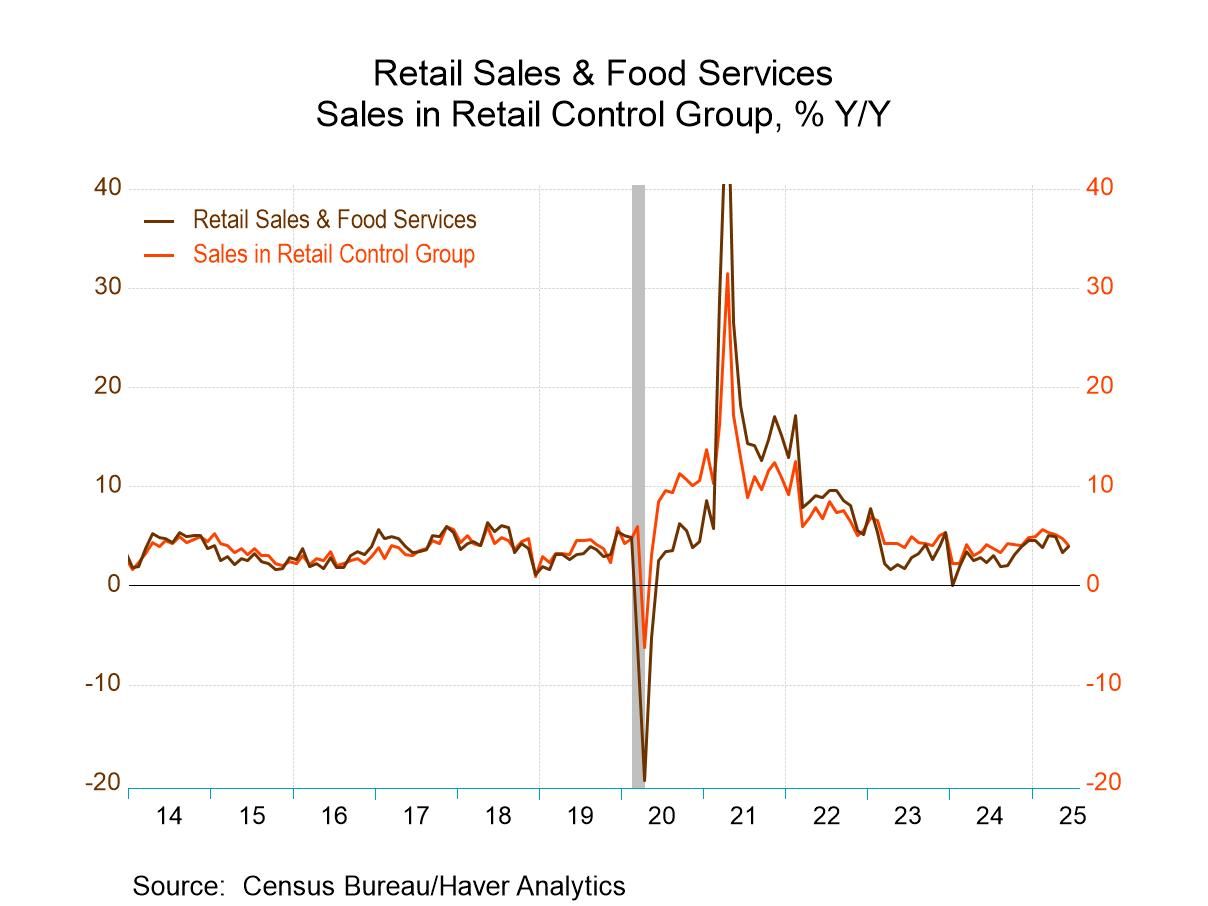

USA| Jul 17 2025U.S. Retail Sales Rebound in June

- Increase led by surge in sales excluding autos.

- Nonauto sales also improve.

- Sales in the control group (used to estimate PCE) strengthen.

by:Tom Moeller

|in:Economy in Brief

USA| Jul 17 2025

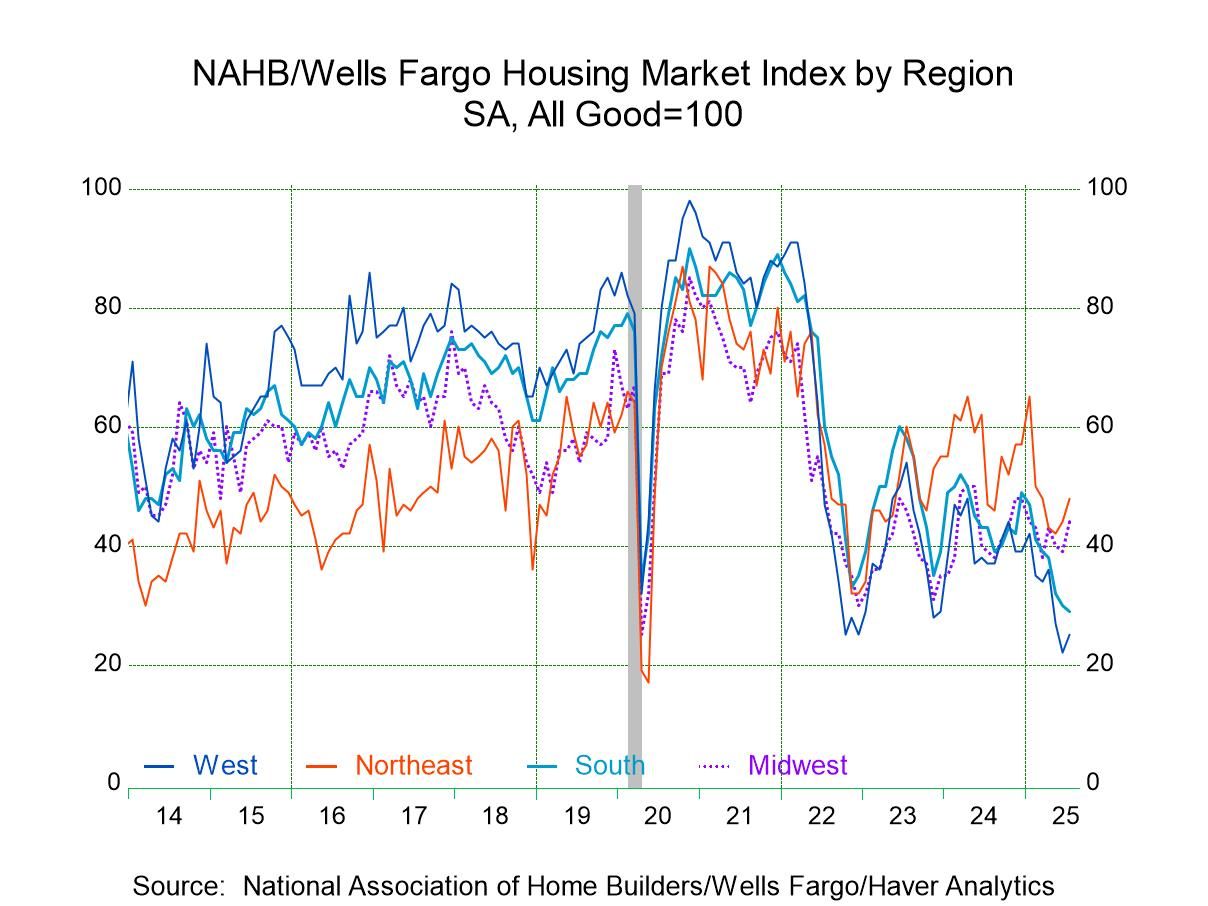

USA| Jul 17 2025U.S. Home Builder Index Improves in July

- Increase follows two months of decline.

- Two of three components rise.

- Regional indexes are mixed.

by:Tom Moeller

|in:Economy in Brief

USA| Jul 17 2025

USA| Jul 17 2025U.S. Philly Fed Manufacturing Index Jumps in July

- The headline index jumped nearly 20 points, led by strong performances by both orders and shipments.

- However, ISM-adjusted composite slipped a bit, indicating that the jump in the headline index was not widely supported by the components.

- Delivery times shortened markedly while both prices paid and prices received indexes posted significant gains.

by:Sandy Batten

|in:Economy in Brief

USA| Jul 17 2025

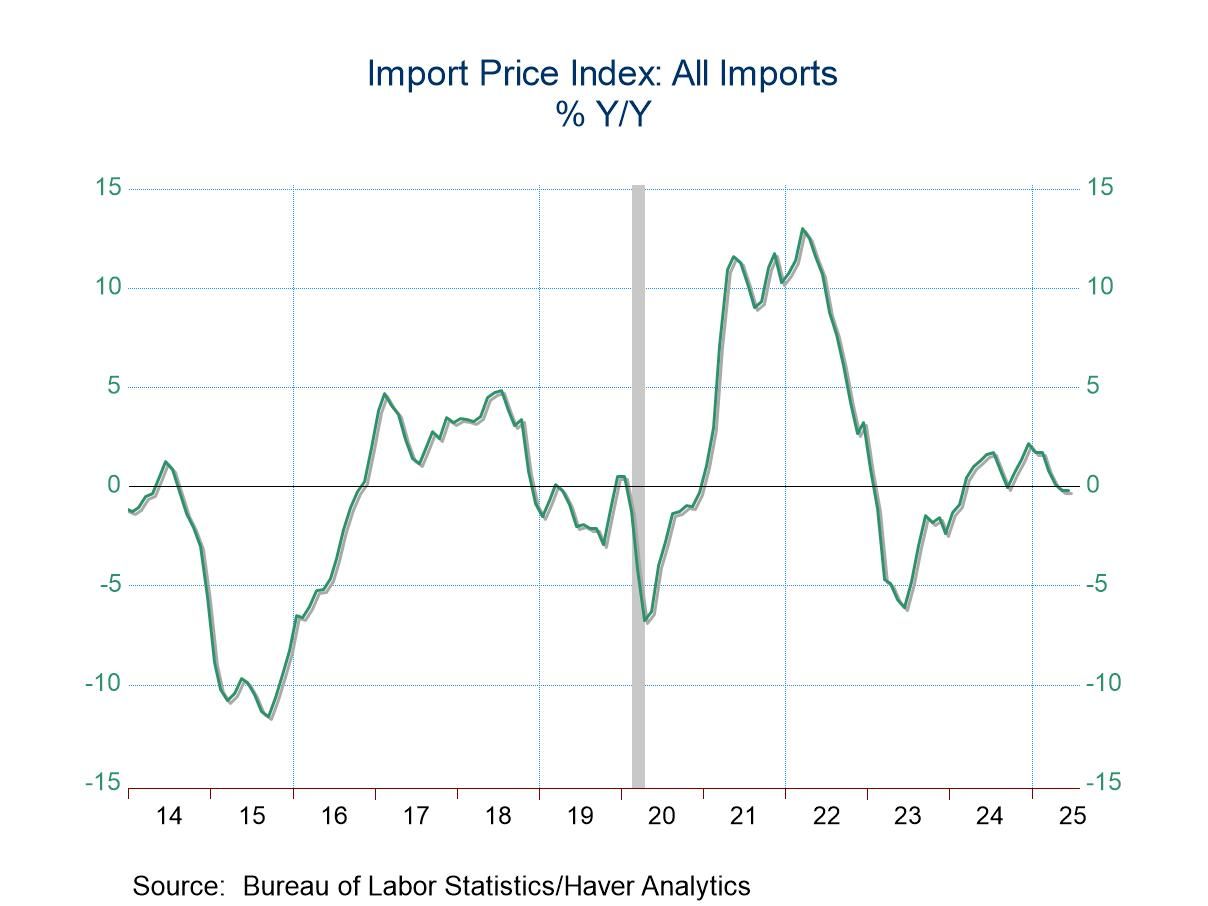

USA| Jul 17 2025U.S. Import Prices Edged Up and Export Prices Rebounded in June

- Import prices edged up in June from May but fell from a year ago.

- Higher prices for nonfuel imports more than offset lower prices for fuel imports in June.

- Export prices jumped more than expected, nearly reversing May’s decline.

- Prices rose for both agricultural and nonagricultural exports.

by:Sandy Batten

|in:Economy in Brief

- of2735Go to 94 page