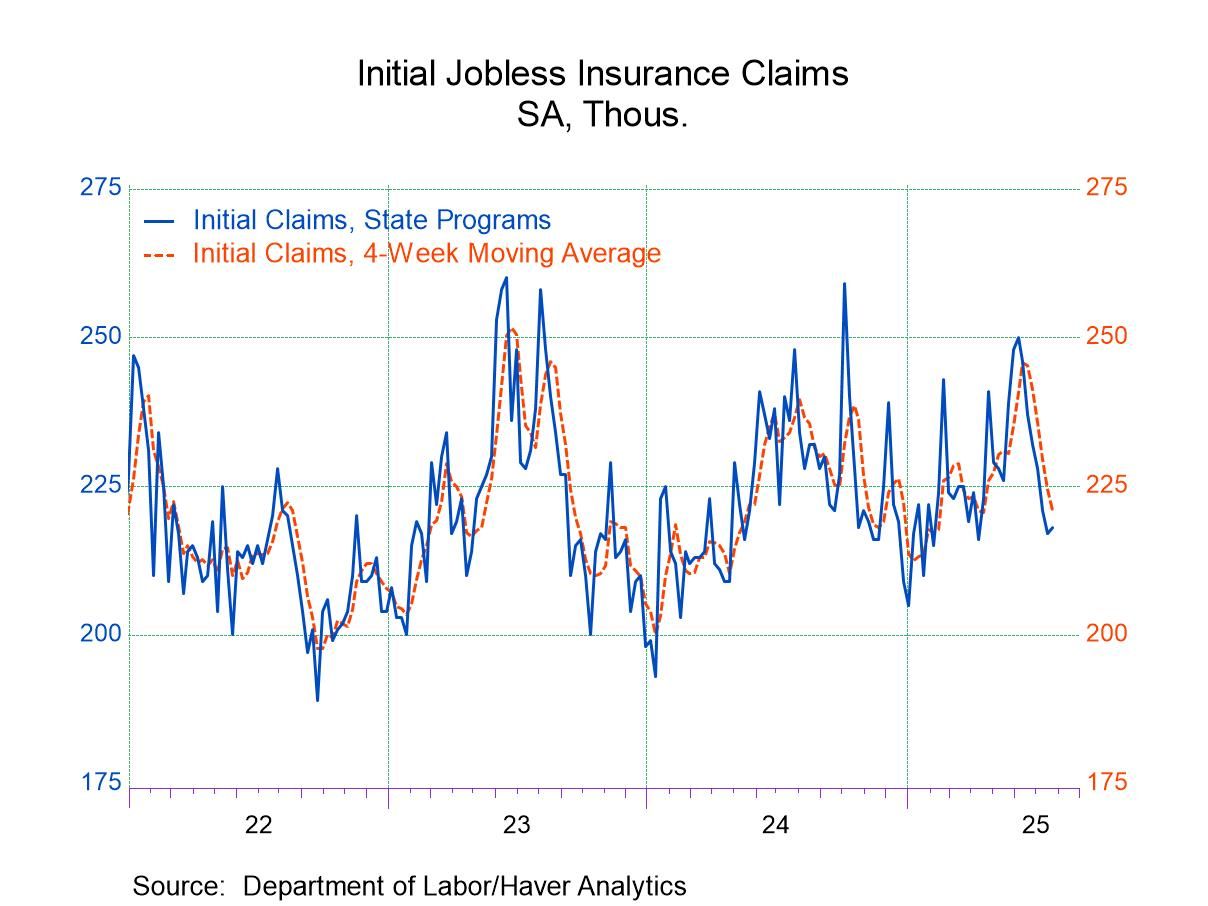

- Initial claims edged up in the July 26 week after six consecutive declines.

- Continuing claims were unchanged in the July 19 week.

- Insured unemployment rate was unchanged for the eighth consecutive week.

Europe| Jul 31 2025

Europe| Jul 31 2025Unemployment in EMU

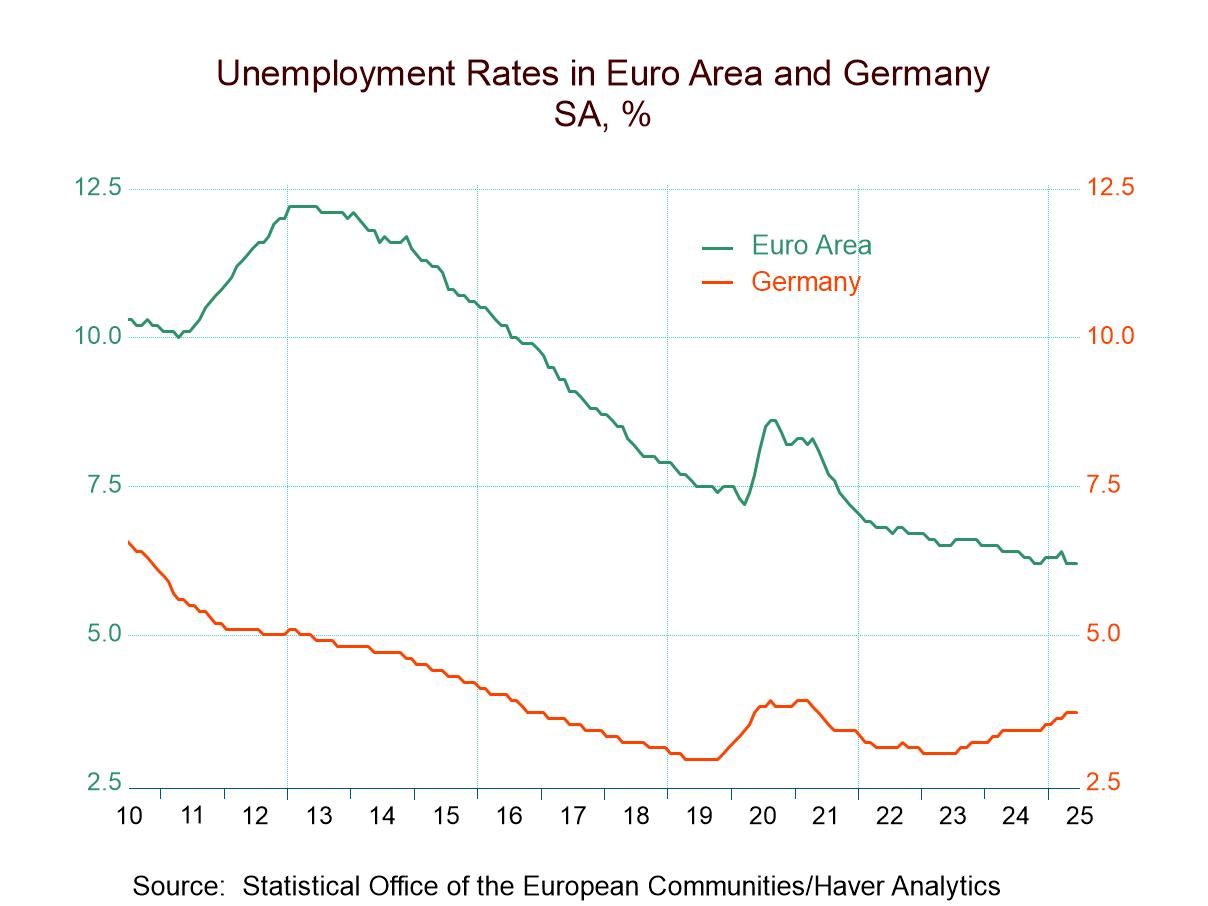

The overall EMU-wide and EU-wide unemployment rates were steady in June. For the EMU the rate is 6.2% and for the EU the rate is at 5.9%. According to data back to January 2020, the EMU rate has been this low or lower 1.3% of the time while the EU rate has been this low or lower 2.6% of the time. The EU rate at 5.9% is just above its all-time low (of 5.8%) on this horizon while the EMU rate remains at 6.2%, which is its all-time low on this horizon.

In June, four of twelve reporting EMU members logged month-to-month drops in their unemployment rates against only two where unemployment rates rose. This compares to May when seven members reported lower rates of unemployment. In April, nine reported unemployment rate drops.

Sequential data over 12 months, six months and three months show unemployment rates falling in six of 12 EMU members, over all three horizons: three-months, six-months, and twelve-months.

Among the 12 reporting members in the table, only three have unemployment rates above their respective medians since 2000 (rankings above 50%) in this period.

Elsewhere the U.S. unemployment rate fell in the month and was otherwise stable over the past year. The U.K. claimant rate of unemployment has snake higher beginning in May. Japan’s unemployment rate remains anchored at 2.5%. Among these three countries, the U.K. has an unemployment rate above its historic median at 62.7%.

European growth has been slow as the emerging GDP data for 2025-Q2 are confirming. But the labor market in Europe remains very solid. Inflation seems to be winding down in Europe. Europe may even be in for some growth turbulence because of the new U.S. tariff policy. However, for now, the labor market looks quite solid, and growth remains the orders of the day even if it is slow.

USA| Jul 30 2025

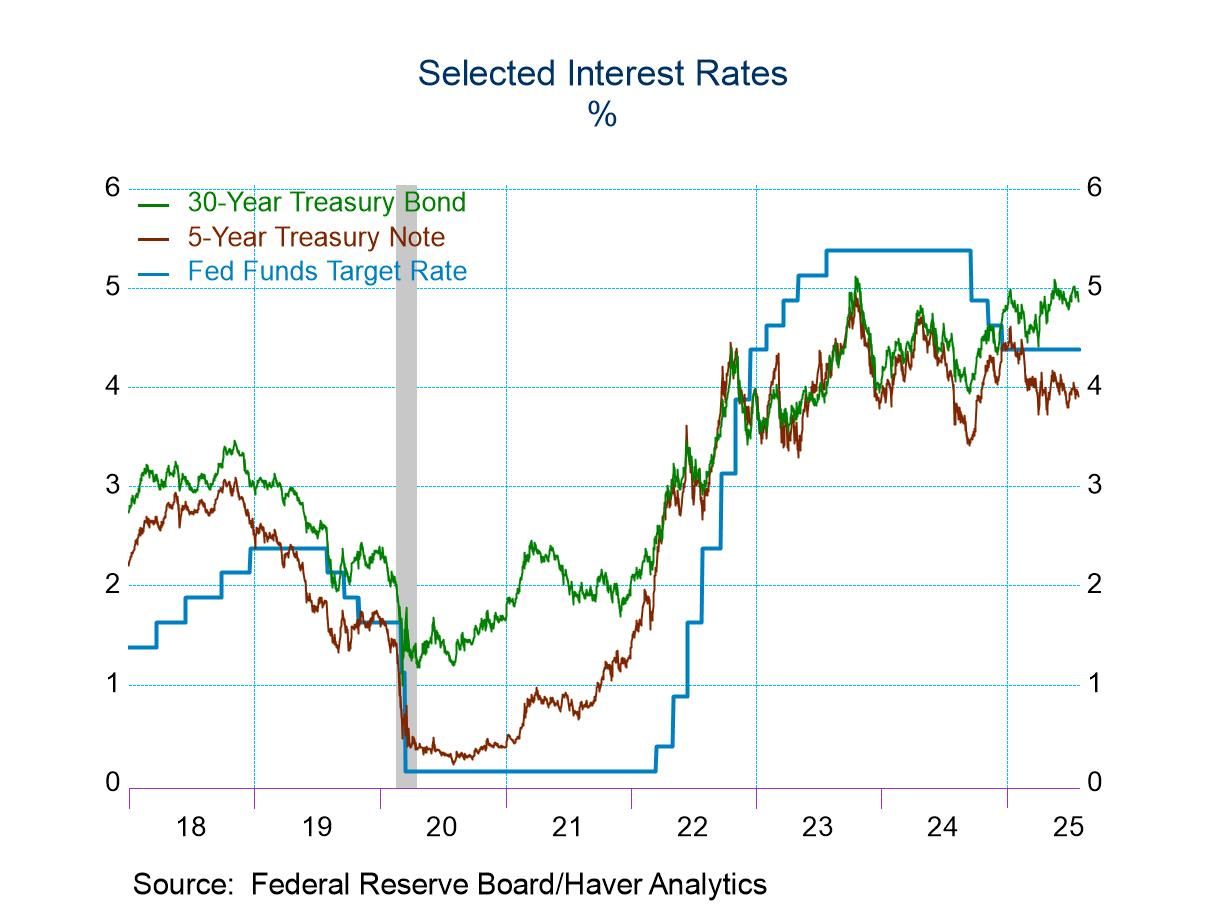

USA| Jul 30 2025FOMC Targeted Funds Rate Range Is Unchanged

- FOMC holds funds rate target at late-December level.

- Decision was not unanimous with two FOMC members voting for a 25 basis point cut.

by:Tom Moeller

|in:Economy in Brief

USA| Jul 30 2025

USA| Jul 30 2025U.S. GDP Q2’25 Shows More Growth, Less Inflation

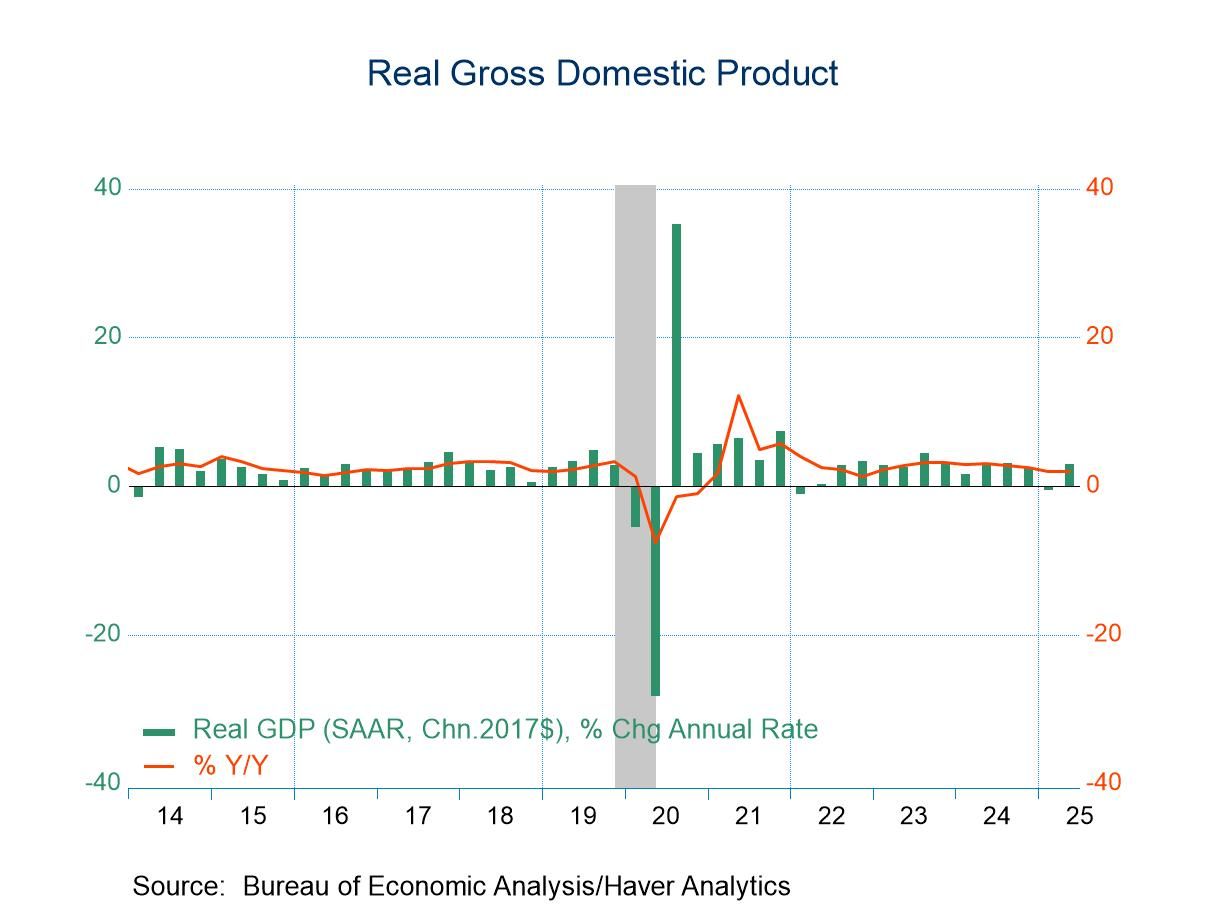

- Q2 GDP growth more than makes up deterioration in Q1.

- Consumer spending picks up while trade gap deterioration reverses.

- Price index gain roughly halves.

by:Tom Moeller

|in:Economy in Brief

USA| Jul 30 2025

USA| Jul 30 2025U.S. ADP Employment Rebounds in July

- Private payrolls increased 104,000 in July after a 23,000 decline in June.

- Goods-producing jobs rose 31,000, and service-producing jobs rose 74,000.

- Job stayer wage growth moderated further.

by:Sandy Batten

|in:Economy in Brief

USA| Jul 30 2025

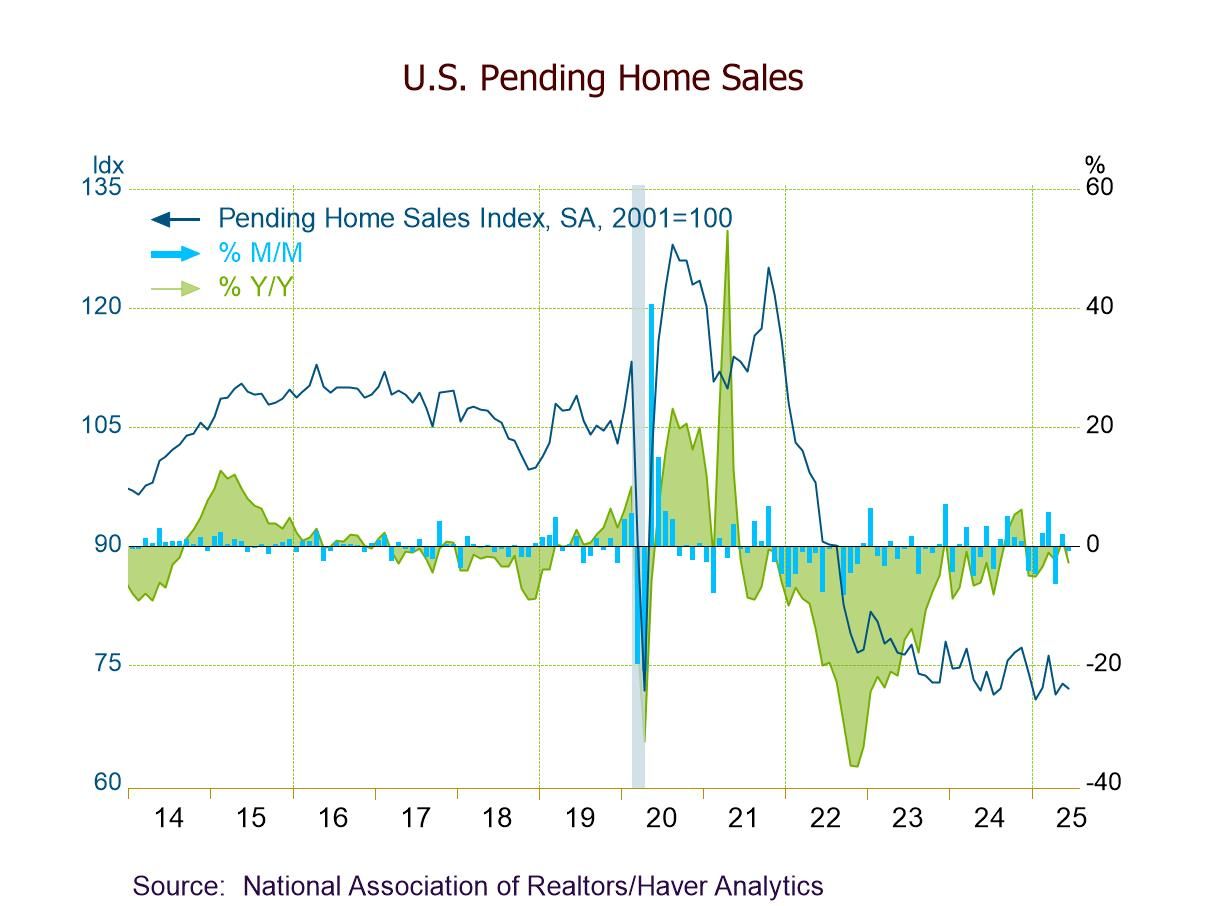

USA| Jul 30 2025U.S. Pending Home Sales Decline in June

- PHSI -0.8% (-2.8% y/y) in June vs. +1.8% (+1.1% y/y) in May.

- Home sales down m/m in three of four major regions but up m/m in the Northeast (+2.1%).

- Home sales down y/y in the Midwest, South, and West; flat y/y in the Northeast.

USA| Jul 30 2025

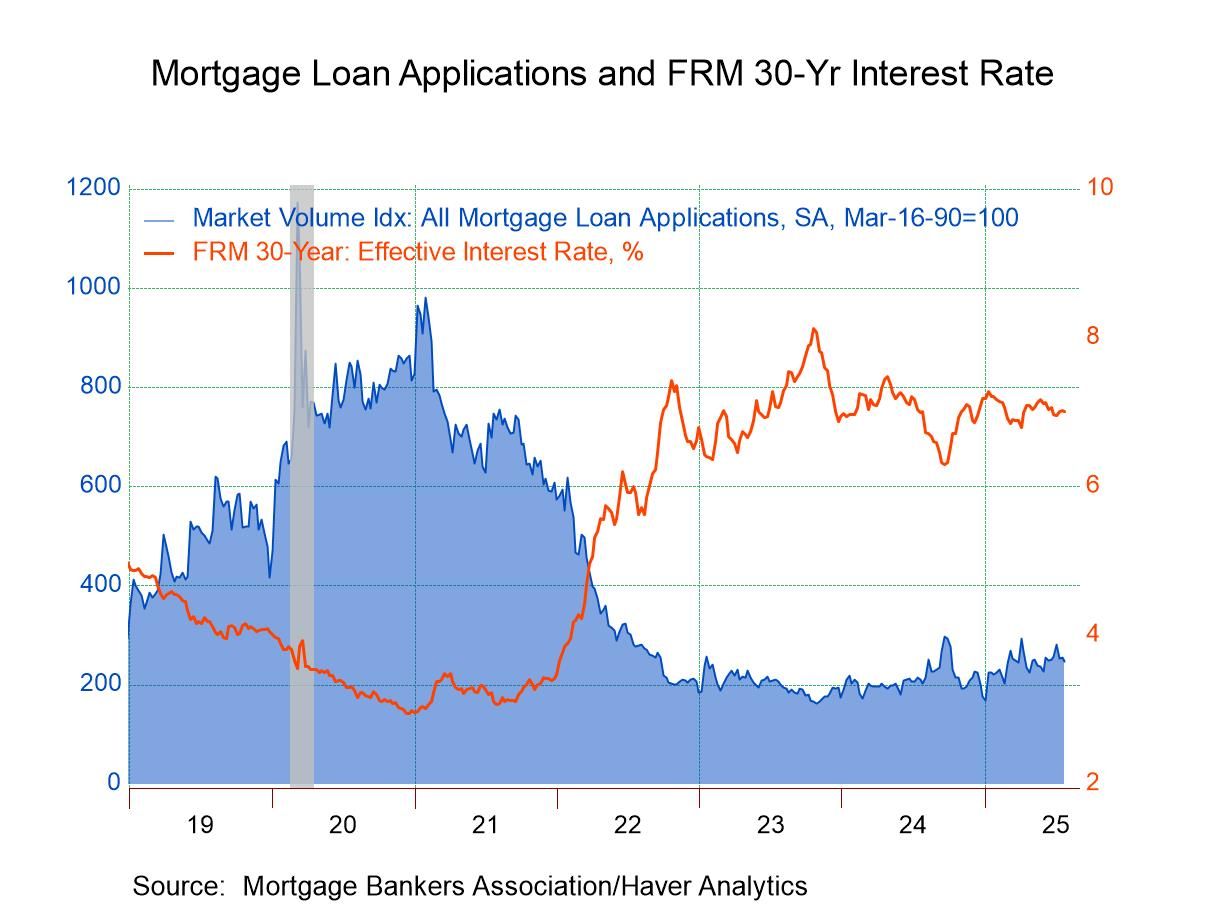

USA| Jul 30 2025U.S. Mortgage Applications Edged Lower Last Week

- Purchase applications and loan refinancing fell in latest week.

- Effective interest rate on 30-year fixed-rate loan declined minimally.

- Average loan size edged up in latest week.

Europe| Jul 30 2025

Europe| Jul 30 2025EMU GDP Slows; But It Creeps Ahead at a Slightly Sub-standard Pace

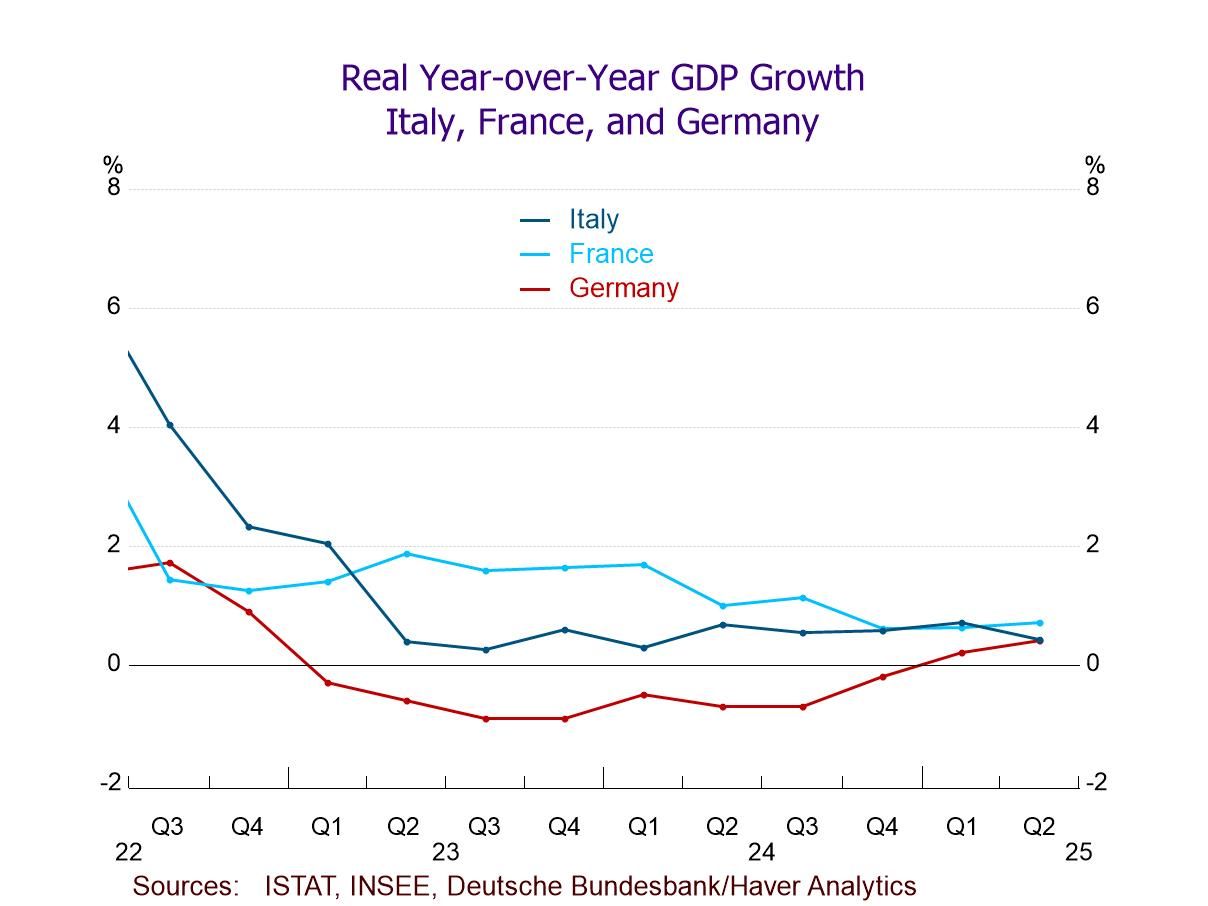

GDP growth in the European Monetary Union slowed to an annual rate of 0.4% in the second quarter of 2025 after logging a very solid 2.3% growth rate in the first quarter. Year-over-year growth has slipped to 1.4% in the second quarter compared to a 1.5% year-over-year pace in the first quarter; however, the second quarter year-over-year growth rate is still a little ahead of the fourth quarter pace in 2024 when it grew by only 1.3% and it is stronger than the third quarter of 2024 when it grew at a 1% pace. While EMU GDP growth has slowed quarter-to-quarter, the year-over-year pace has a moderate ranking. The pace ranked on all growth rates since 1997 leaves the year-over-year pace of 1.4% at a 42.4 percentile standing; that's below its median for the period (the median occurs at a ranking of 50%). However, it's not that short of the median and it indicates that growth is moderately slower than it's been over the past period back to 1997.

Growth by Size The Four Largest: The four largest economies in the monetary union grew at a 0.5% annual rate in the second quarter, compared to 1.2% in the first quarter and 0.8% in the fourth quarter of 2024. The four largest EMU economies (Germany, France, Italy, and Spain) have GDP-weighted growth of 0.8% over four quarters, the same as in Q1. That growth rate ranks in its 37th percentile, well below its median pace since 1997.

The Rest: The ‘rest of EMU’ grew at a ‘technically positive’ annual rate of 0.1% in 2025-Q2. That slow-crawl is quite weak, but it follows a 5.3% pace in Q1. The rest of EMU grows at a very solid 3% pace year-over-year in 2025-Q2 and logs 3.0% or better growth rates for three quarters in a row. The year-over-year pace ranks in the top one-third of all growth rates for the rest of EMU group since 1997-Q4. While the Q2 pace is very slow, in context, it does not seem to be an issue.

EMU Median Growth: The median growth rate for all of EMU is considerably weaker overall than the growth for the Rest of EMU. In 2025-Q2, however, the median pace is 0.7%, down from 1.1% in Q1. The year-on-year pace over the past four quarters for the EMU has been gradually slowing and is at 1.1% year-over-year pace in 2025-Q2. That growth rate for all of EMU is weaker than the ranking for the large countries as well as for the rest of EMU.

Compared to the U.S. Growth in the U.S. jumped to 3% in Q2 and logged a year-on-year pace of 2.0%. The U.S. logs the third strongest year-on-year pace in the table for Q2. Still, compared to its own historic experience, the U.S. growth rate ranks poorly in its 31.8 percentile, the lower third of its historic queue of growth rates. In relative terms, only two EMU member countries in the table rank lower.

- of2735Go to 91 page