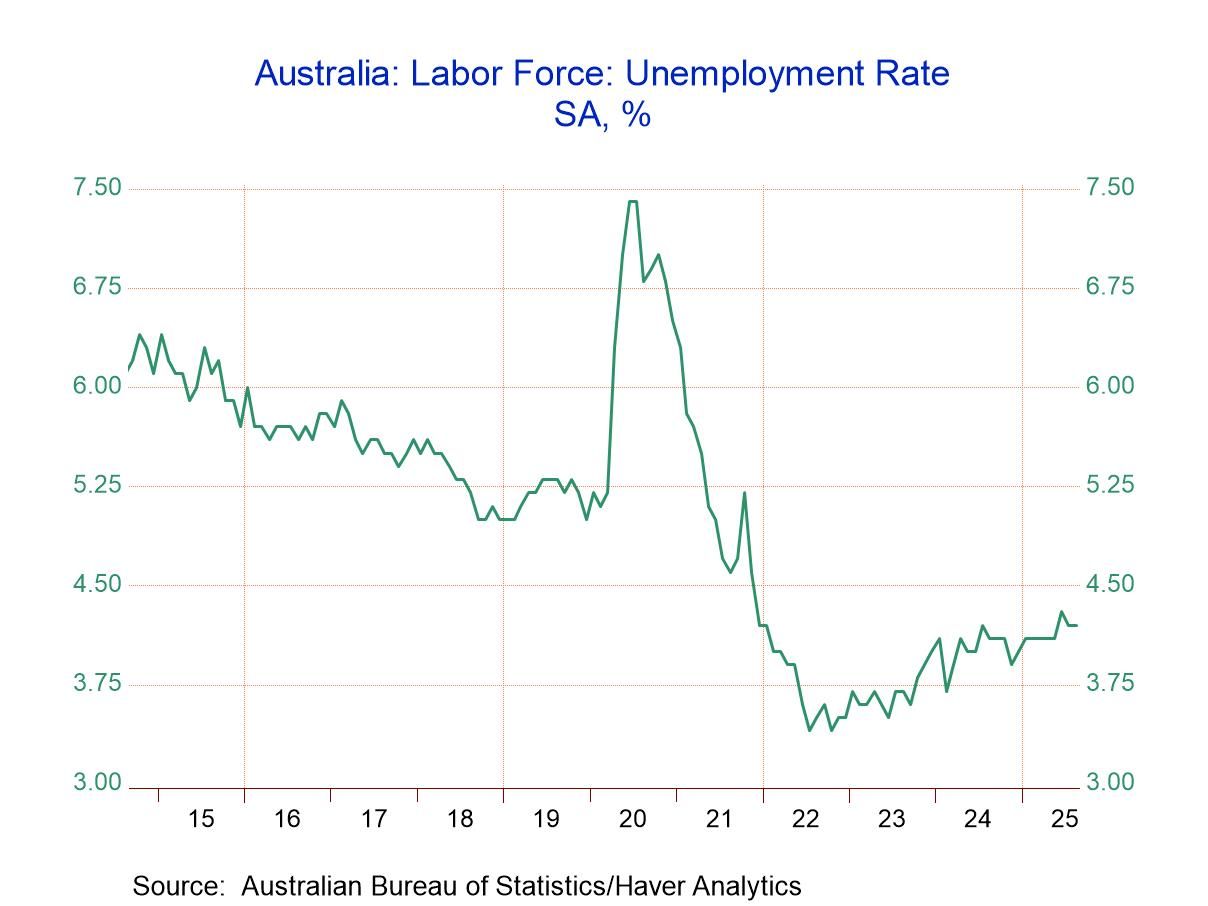

Unemployment in Australia in August remained low, standing at 4.2%, the level it dropped to in July. June brought a rise in unemployment to 4.3% after posting 4.1% in May. However, at 4.2% the unemployment rate in Australia is low, since about 2000 the unemployment rate has been lower only about 16% of the time.

The labor force participation rate in August fell to 66.8 from 67.0 where it had been for the previous several months. The participation rate, however, is high on historic comparison at about the 95th percentile; the participation from people ages 15 to 64 is even higher with a 97.7 percentile standing on the participation rate of 80.6%.

However, employment gains in Australia have been slowing. The year-over-year gain is 1.5%, over six months, employment speeded up, gaining a pace of 1.9% at an annual rate, but over three months the growth rate for employment has fallen to a sharply lower 0.6% annualized.

Australia's labor force fell by 0.5% in August after rising robustly in previous months. The labor force was rising by 1.6% over 12 months, at a 2.2% annual rate over six months and at a 1.3% annual rate over three months. There's been some variability in labor force growth, but it still seems to be relatively solid. The year-over-year growth rate, however, has a ranking only in its 33 percentiles historically back to the year 2000- a lower one-third standing.

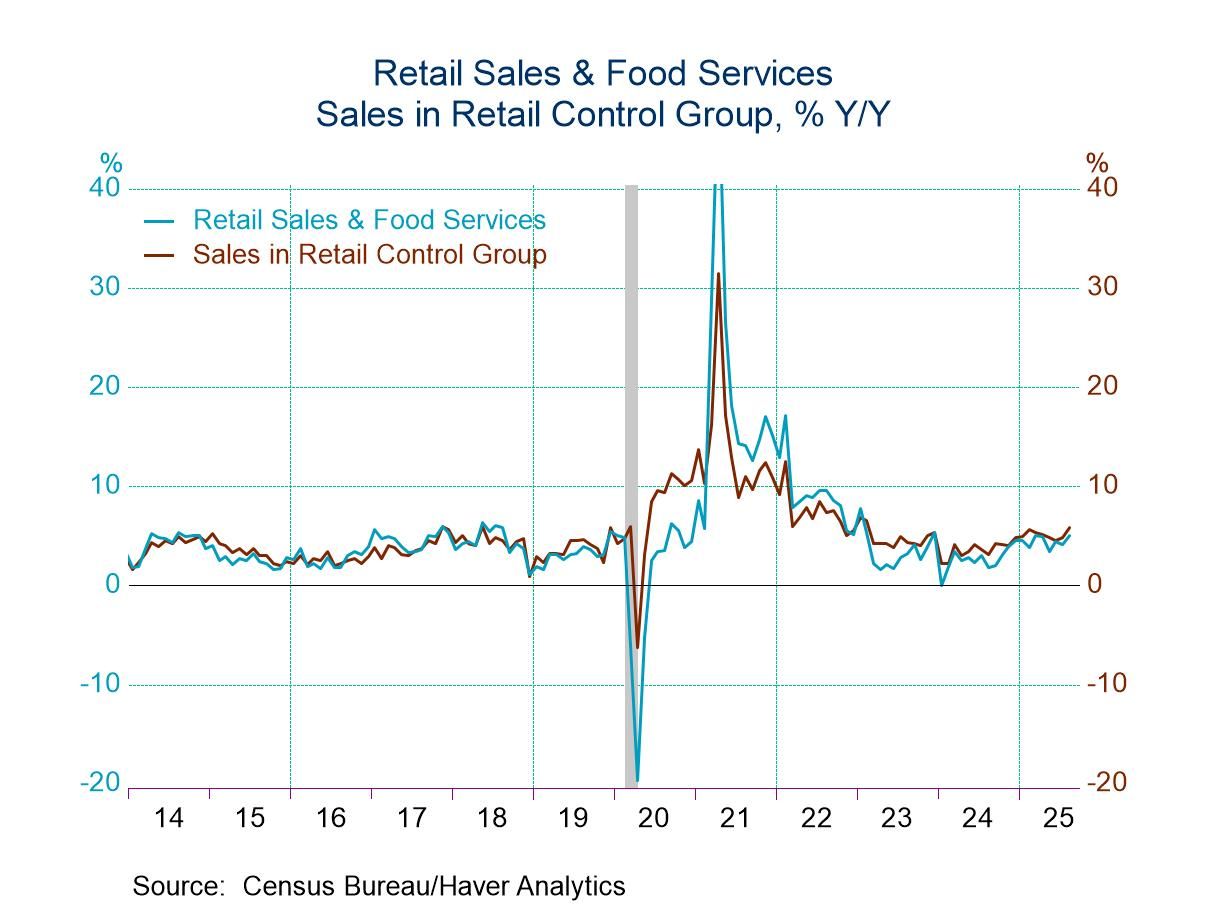

In terms of the overall economy, retail sales have picked up; some of this is inflation. The growth rate for retail sales over three months is 7.1%; over 12 months it's 4.9%. Headline inflation grew by 2.8% over 12 months, but it's rising over three months at a stronger 4.2% annual rate. Inflation excluding volatile measures has been relatively stable over three months, six months, and 12 months. However, it picked up quite considerably in June, rising at a very rapid double-digit pace.

Australia's low and consistent unemployment rate is in step with what's going on internationally. Globally there is stability or some small backtracking on unemployment gains made since COVID. In the European Monetary Union, we're looking at unemployment rates consistently low over 12 months, 3 months, and 6 months at a historically low level. Japan's unemployment rates are consistent and low near historically low levels as well. In the United States and in the United Kingdom, unemployment rates are relatively stable. The U.K. shows some drift up in its unemployment rate. But both the U.S. and the U.K. have unemployment rates that have been lower only about 30% of the time.