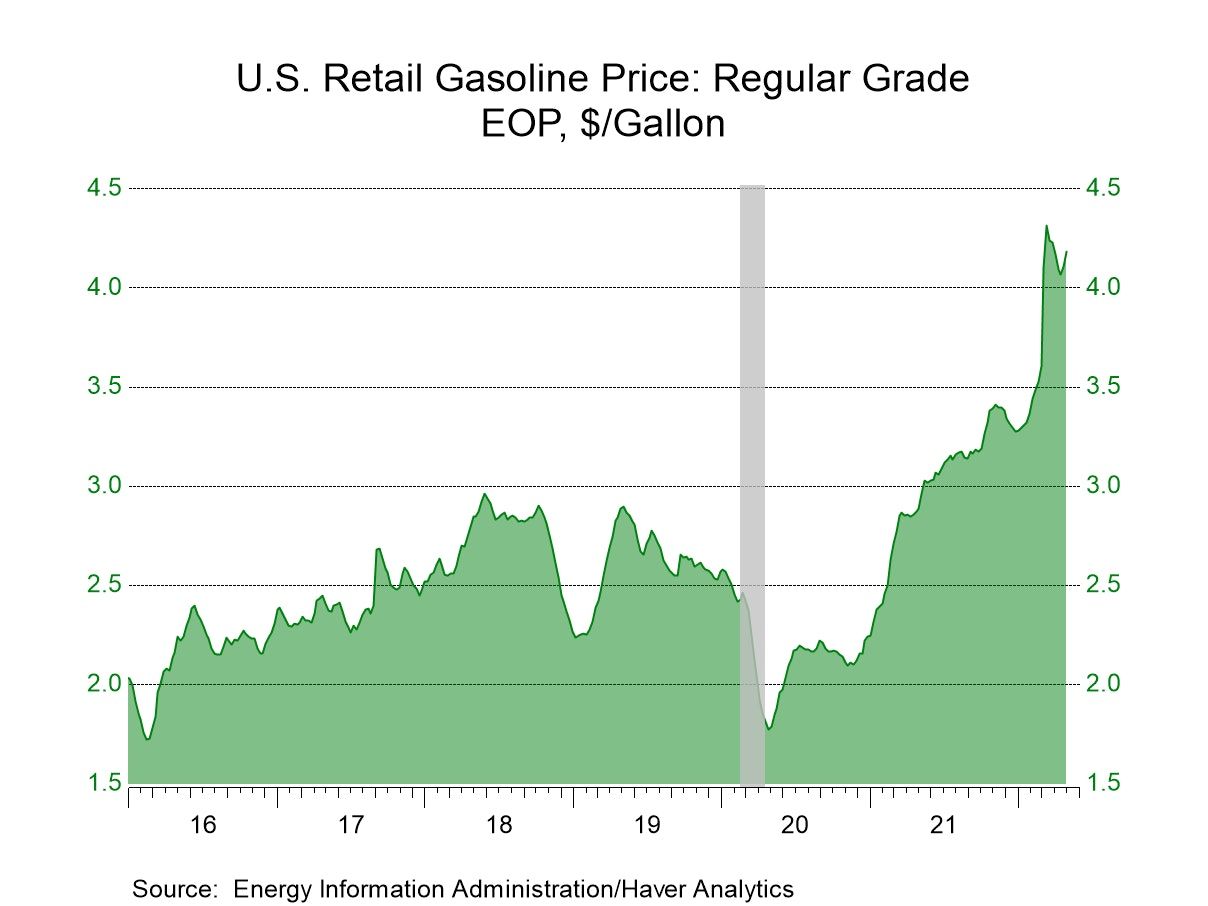

- Gasoline prices increase sharply.

- Crude oil prices ease.

- Natural gas prices fall.

USA| May 03 2022

USA| May 03 2022U.S. Energy Prices Are Mixed

by:Tom Moeller

|in:Economy in Brief

China| May 02 2022

China| May 02 2022China's PMIs Weaken Sharply

China continues to post weak and weakening PMI numbers in April. The manufacturing index fell to 47.4 in April from 49.5 in March. This marks the second month in a row that the manufacturing index is below 50, indicating that manufacturing activity is contracting in China. China's nonmanufacturing index fell extremely sharply to 41.9 from March's 48.4. This is also the second month in a row that nonmanufacturing (an amalgamation that includes the services and construction sectors) shows a decline in activity for that joint sector.

The drop in manufacturing in April was relatively sharp. Over the last 15 years, there are only ten months in which the manufacturing index fell more sharply in one month than it did in April. Nonmanufacturing fell by 6.5 points in April, marking it as the second largest decline in the history of this index going back to 2007. The largest nonmanufacturing decline came when COVID struck in 2020; in February of that years the manufacturing sector fell in one month by 24.5 points...of course, it also rebounded by 22.7 points the very next month.

These statistics tell us that the ongoing assessment of these two sectors in China is weak and that the near-term weakness has become more intense. China continues to suffer some great difficulties on the economic front because of its decision to continue to pursue a zero COVID policy. The zero COVID policy refers to a policy goal in China to eliminate COVID. China has no tolerance for any infection whatsoever.

While the rest of the world is learning to live with COVID and with infections, to manage hospitalizations and illnesses, as well as to develop treatments, China's policy of complete intolerance and of shutting the economy down and literally fencing people into the places that they live so that they cannot mingle with other uninfected people is having dramatic impact on the economy and creating extreme distress among people in China.

Despite the extreme unpopularity of this program, China shows no signs whatsoever or backing off it and - quite the contrary – its leaders seem to be even more committed to the goal as time passes. China is pursuing this strange strategy of lockdowns and isolations and it is employing so much testing that it has stopped administering inoculations of the vaccine.

The new strains of COVID have proved to be far more transmissive than the earlier strains of COVID but not as dangerous and certainly not as lethal as the earlier strains. This explains why the rest of the world has found that it can make some sort of peace with the virus by controlling it and dealing with outbreaks when they occur.

An added problem here is that this is the well-known coronavirus. Science knows it is a class of virus prone to developing variants. As a result of this tendency to develop changes, it has been very difficult to develop truly effective vaccines against COVID. However western medicine has discovered vaccines and treatments that were developed for the earlier strains of COVID that generally have some usefulness in combating some of the later strains that have developed even though the vaccine may become less effective overtime. The vaccines are not very 'vaccine-like' as they only can stop infection for a brief period of time immediately after inoculation. That protection wears off quickly and then, people who are double vaccinated and boosted, can still get infected- but they have less risk of extreme illness or death.

China's approach to COVID has left it with a manufacturing PMI that shows a steady slide; its 12-month average slips to a lower six-month average and to a lower three-month average with a particularly sharp plunge in April. The nonmanufacturing index also shows the same sequential set of declines that are even clearer and more substantial with an even larger plunge in April.

USA| May 02 2022

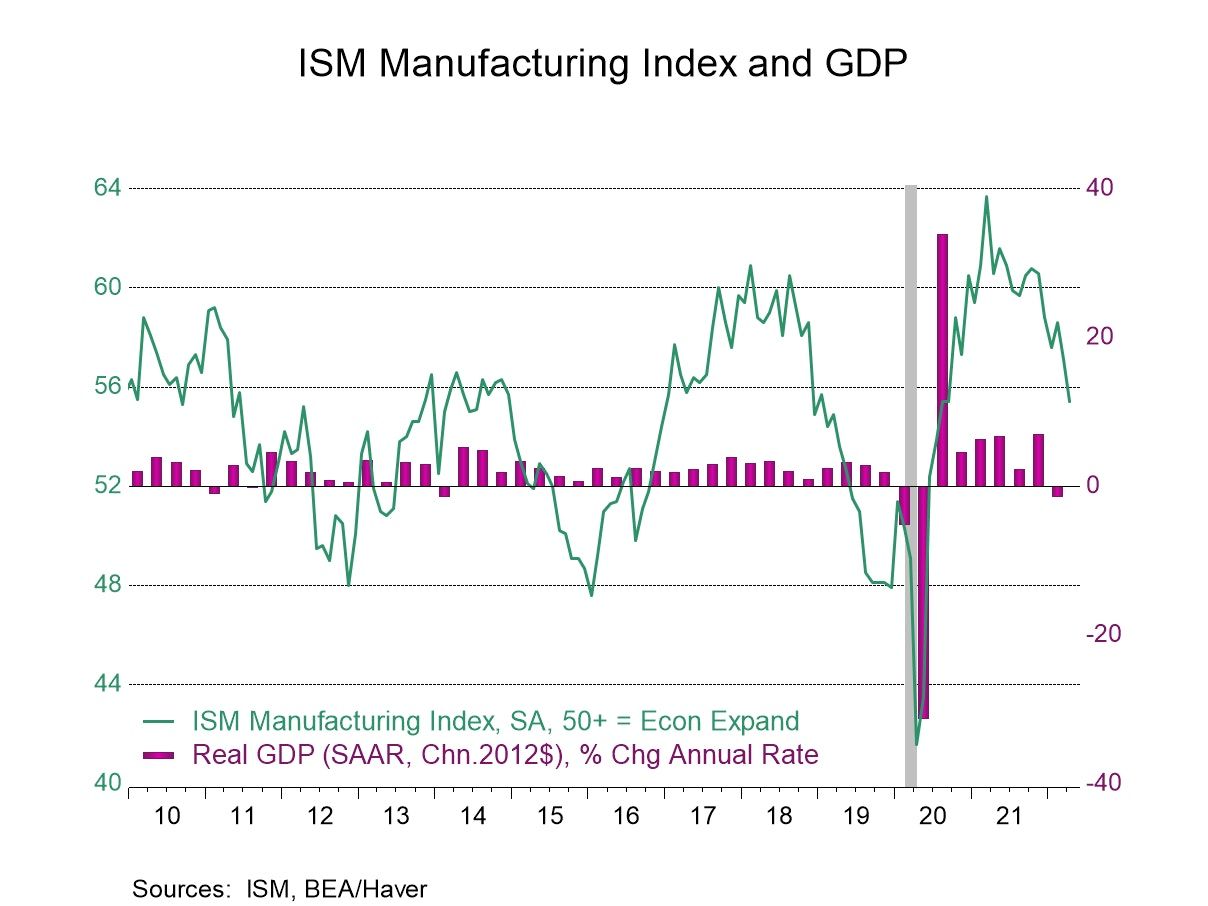

USA| May 02 2022U.S. Manufacturing Activity Continues to Soften in April

- Index level reaches lowest level since September 2020.

- Component declines are broad-based.

- Prices paid ease.

by:Tom Moeller

|in:Economy in Brief

USA| May 02 2022

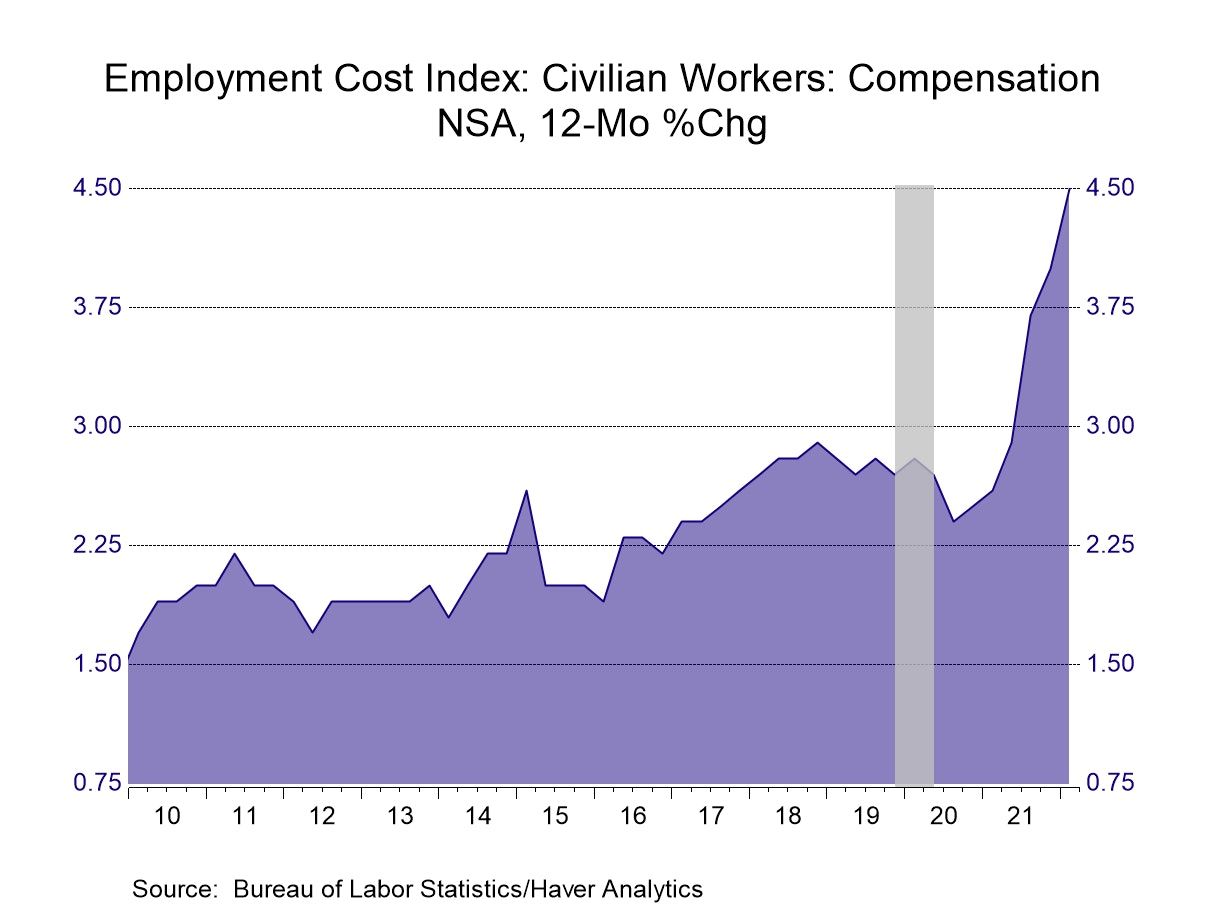

USA| May 02 2022U.S. Employment Costs Accelerate in Q1'22

- Wage and salaries improve.

- Benefits skyrocket.

by:Tom Moeller

|in:Economy in Brief

USA| Apr 29 2022

USA| Apr 29 2022U.S. Personal Spending Surges With Higher Prices in March

- Gasoline leads nominal spending but falls in real terms.

- Core price inflation eases m/m.

- Wage & salary growth remains firm.

by:Tom Moeller

|in:Economy in Brief

USA| Apr 29 2022

USA| Apr 29 2022U.S. Chicago Business Barometer Falls Back in April

- 56.4 in April vs. 62.9 in March; widespread drops in index components.

- Production is at the lowest level since July 2020.

- Employment remains below 50, indicating contraction for five straight months.

- Price paid continues to be at an elevated level.

Global| Apr 29 2022

Global| Apr 29 2022EMU GDP Continues Strong Year-on-Year Pace

European Monetary Union (EMU) GDP growth logged a 0.8% gain in the first quarter of 2022 after rising by 1.2% in the fourth quarter of 2021. Both are annualized quarterly rates of expansion. The year-over-year growth rate in the first quarter of 2022 sits at 5%. This growth rate is substantially because of the extremely strong growth rates of over 9% logged in the third quarter of 2021 and the second quarter of 2021.

Beginning with Q2 2022 data, these very strong growth rates are going to begin to fall out of the year-over-year calculation and, at that point, we will start looking at annualized European growth rates that are going to be a little bit more like the annualized quarterly rates that we see in the table below. For the last two quarters, for example, we are seeing GDP average something more like 1% at an annual rate. However, having two quarters out of four with quarterly growth rates over 9% right now pushes the annual rise in GDP up very strongly.

The annual growth rate for the EMU shows 5% growth in the first quarter of 2022, up from 4.7% in the fourth quarter of 2021 and from 4.1% in the third quarter of 2021. That compares to a second quarter year-over-year growth rate at a 14.6% in the second quarter of 2021.

Obviously, what we're seeing now is the transition away from those COVID-affected growth rates. Comparisons with the weak readings of GDP during the period of COVID are falling by the boards; however, the strong rates posted in the expansion after the COVID recession are still embedded in the year-over-year calculations. They are still affecting substantially the year-over-year growth rates; meanwhile, the last two quarters are showing us European growth that is coalescing at a 1% annual rate

Yet, even with these lower growth rates of GDP, inflation in Europe continues to flare strongly. The European Central Bank still has a job to do. And based on the way GDP is evolving, it doesn't look like the excessive growth rate in GDP is to be blamed for the inflation pressures that have developed in Europe and have lingered. Supply chain problems, war, food scarcity and other industrial dislocations appear to be at work.

Among the early six reporting European Monetary Union members, only Portugal is really knocking down eyepopping growth rates. Portugal had first quarter 2022 GDP growth at a 10.8% annualized rate, up from a 7% pace in the fourth quarter and that compares to an 11.2% pace and the third quarter of 2021. However, two EMU members, France and Italy, log GDP declines in the first quarter with France's quarterly GDP declining at a 0.2% annualized rate and Italy's GDP declining at a 0.7% annualized rate.

The four largest EMU members (Germany, France, Italy, and Spain) grew at a pace of 0.3% annualized in the first quarter of 2022 and that compares to a 2.1% annual rate in the fourth quarter of 2021. For the rest of EMU, growth in the first quarter came in at 2.1% pace compared with a decline at a 1.4% annual rate in the fourth quarter of 2021. Both the four largest economies and the rest of the EMU had extremely strong rates of growth and the third quarter of 2021.

Year-over-year growth rates for the countries in the table are still quite strong. For the most part, they were in the 90th percentile or higher in their queue of annual growth rates back to late-1997. The exception is Germany whose growth rate is only at the 85.9 percentile; that's a minor exception although it is the European Monetary Union's largest economy.

USA| Apr 28 2022

USA| Apr 28 2022FRB Kansas City Manufacturing Index Slips But Remains Elevated

- April decline led by orders and shipments.

- Expected conditions also fell, for the first time in four months.

- Inflation indicators continued to rise.

by:Sandy Batten

|in:Economy in Brief

- of102Go to 70 page