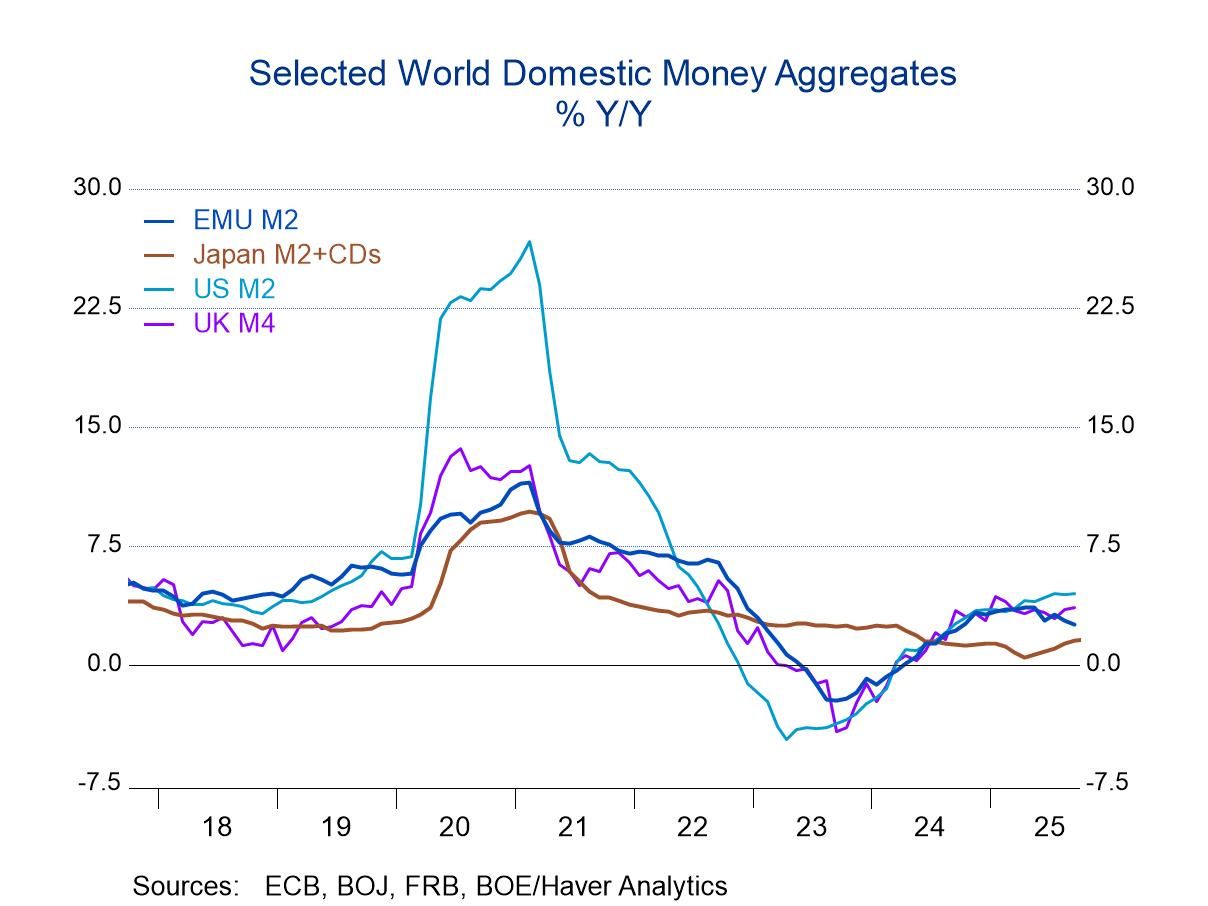

Global

GlobalGlobal money supply growth boomed during COVID. Then growth ‘busted,’ decelerating sharply with the United States, the United Kingdom, and the European Monetary Union all showing monetary contraction to some degree throughout 2023. The only country to buck this trend was Japan which had a more modest boost in money supply during COVID and then more modest growth rates that decelerated and continued to gravitate toward near zero growth, until recently, when Japanese money supply started to accelerate very slightly.

Euro Area Recent trends show nominal money growth in the euro area decelerating slightly from a 2.5% growth rate over 12 months to growth rates around 2% or a bit lower over three months and six months. Monetary union private credit has also decelerated from a growth rate of 2.4% over 12 months to 1.7% over six months and to a 1.3% annual rate over three-months.

United States, United Kingdom, and Japan Nominal money supply growth in the U.S. remains fairly steady, growing 4.5% over 12 months and an annual rate of 5 to 5.4% over three months and six months. The U.K. nominal money supply growth is 3.5% over 12 months, 2.8% at an annual rate over six months and 3.6% at an annual rate over three months. Japan's M2 plus CDs has been stepping up its growth from 1.6% over 12 months to a 2% pace over six months to 4% at an annual rate over three months. Nominal money supply growth is mostly fluctuating between steady and stronger across these monetary center countries.

Real balances in EMU Real money balances, however, are looking significantly weaker. In the European monetary Union, real M2 grows 0.3% over 12 months and then its growth rate slips to -0.6% at an annual rate over both three months and six months. Private credit in the euro area rises by 0.1% over 12 months, declines by 0.5% at an annual rate over six months, and declines at a 1.3% annual rate over three months. Real credit is weakening.

More real balances In the U.S., real money supply growth is fluctuating, growing at 1.4% over 12 months, stepping up to 2.3% over six months and back to a 1.4% annual rate over three months. U.K. real money balances are simply shrinking at a -0.6% annual rate over 12 months and a -0.7% annual rate over three months. In Japan, real money balances are actually accelerating; real money growth is -1.3% over 12 months, which rises to plus 0.4% over six months with an annual rate of 2.9% at an annual rate over three months.