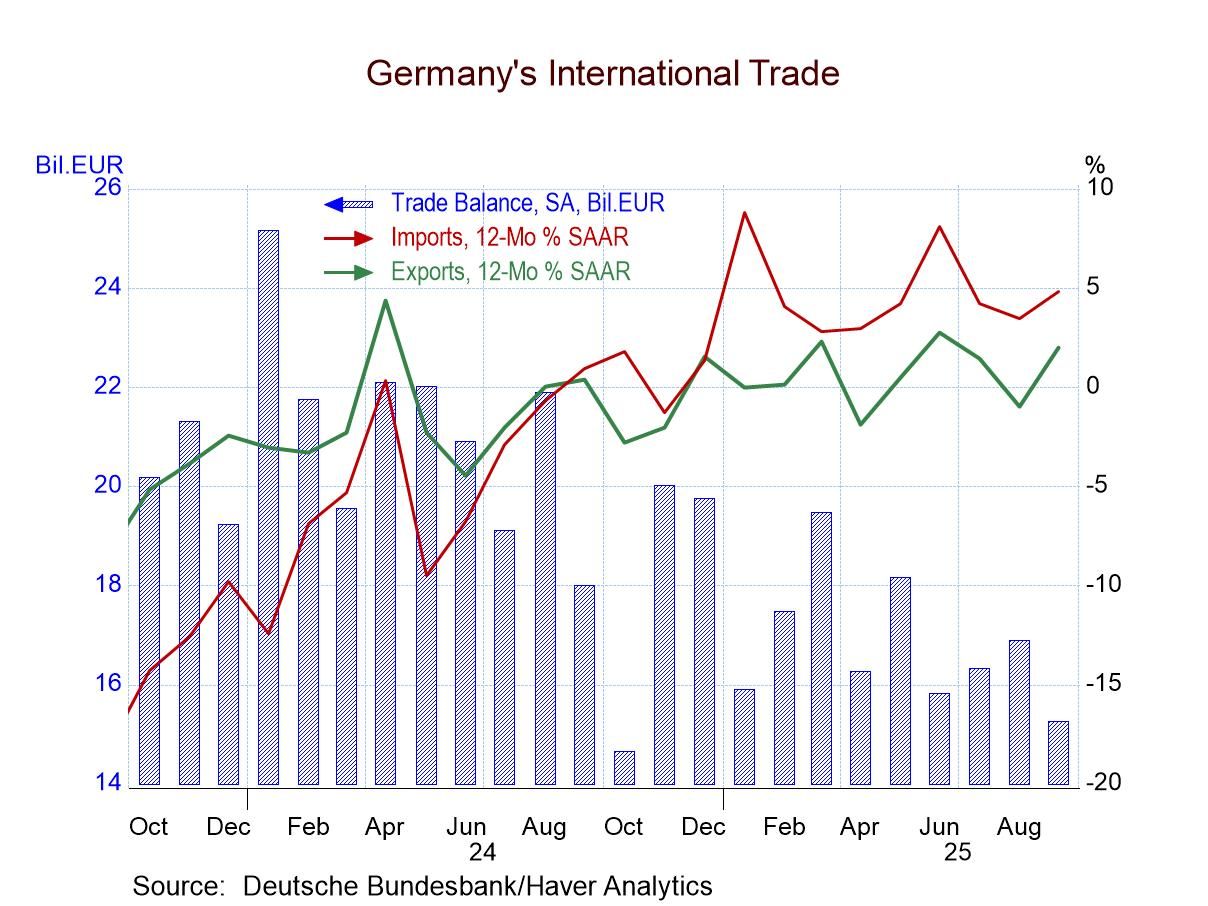

The chart provides a good overview for German trade trend. The table breaks trade trends down by categories and provides growth rates on shorter horizons of 3 months, 6 months and 12 months. But the chart depicts the overarching trends well. It shows the German surplus being diminished on a gradual path and not altogether in a clear monotonic fashion. Export and import lines on the chart move mostly sideways (horizontal). The export line is below the import line since late last year. These two series plots on the right-hand scale and they depict growth rates (year-over-year). So sideways movements mean roughly steady growth. Exports have been growth steadily year-over-year at a weak pace that on occasion has been a decline in terms of their year-on-year value. Generally, the green line is in positive territory. The red import line has been stronger, indicating somewhat better, steadier import growth over the period.

While exports had a good September, export growth sequenced from 12-months to 6-months, to 3-months has been weakening. Imports also put in a strong September but are showing some erosion from 12-month to 6-months to 3-months in terms of annualized rates of growth. Still, import growth rates remain quite strong and consistent; the sense of erosion is clear but also moderate – it’s a moderate erosion in progress for imports.

Capital goods exports from Germany are improving- this observation is based on lagged data with a one-month lag built in. But consumer goods and vehicle exports are slowing and rather sharply- likely as a result of U.S. tariffs.

Import side trends, with the same lag, are not as clear cut. Capital goods imports are growing, and motor vehicle imports are improving and accelerating. Consumer goods imports have erratically slowed.

Real exports and imports on sequential lagged data show exports contracting on most horizons while imports generate consistent positive growth in real terms. There is a big difference in these two trends expressed in real terms.

On balance, German trade trends are shifting. The trade balance is gradually eroding. Change is in play.

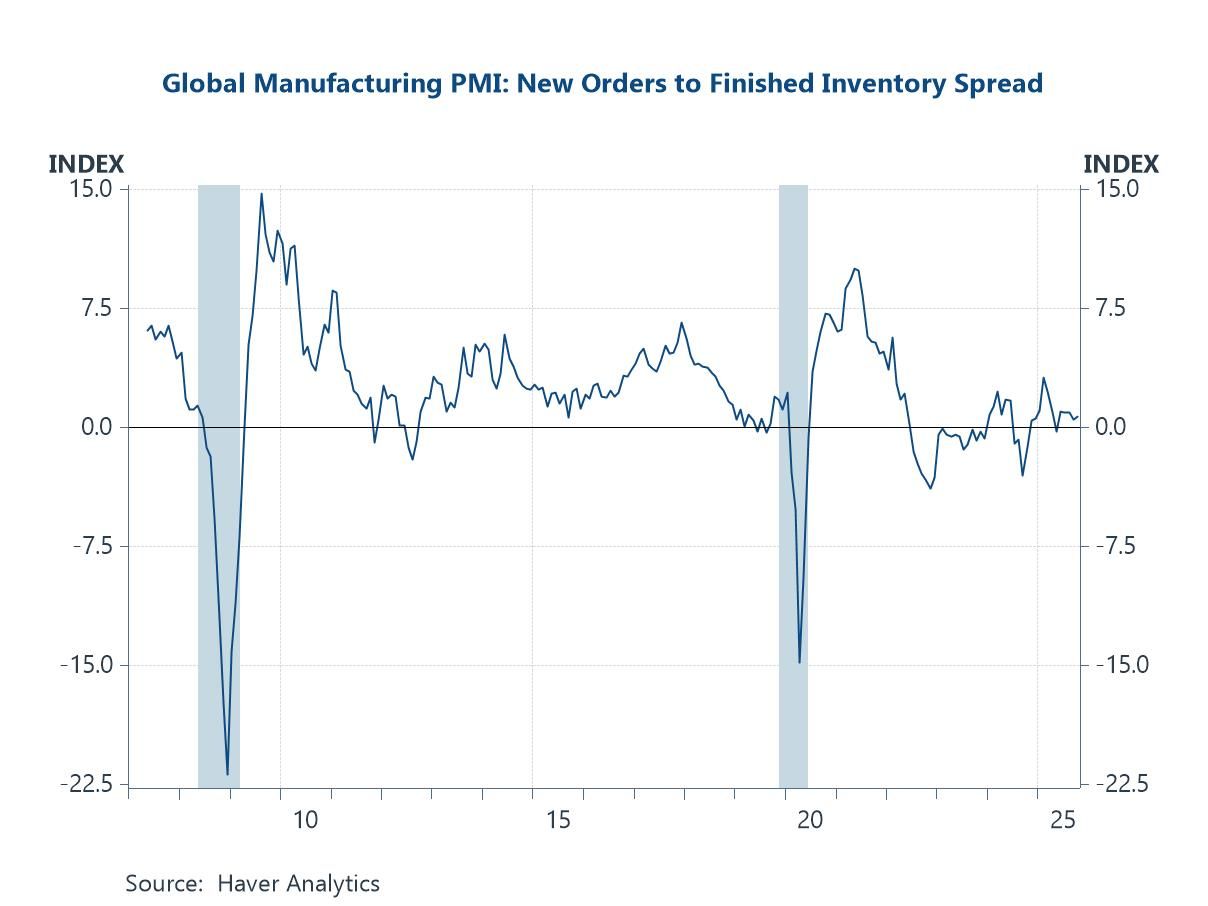

Global

Global