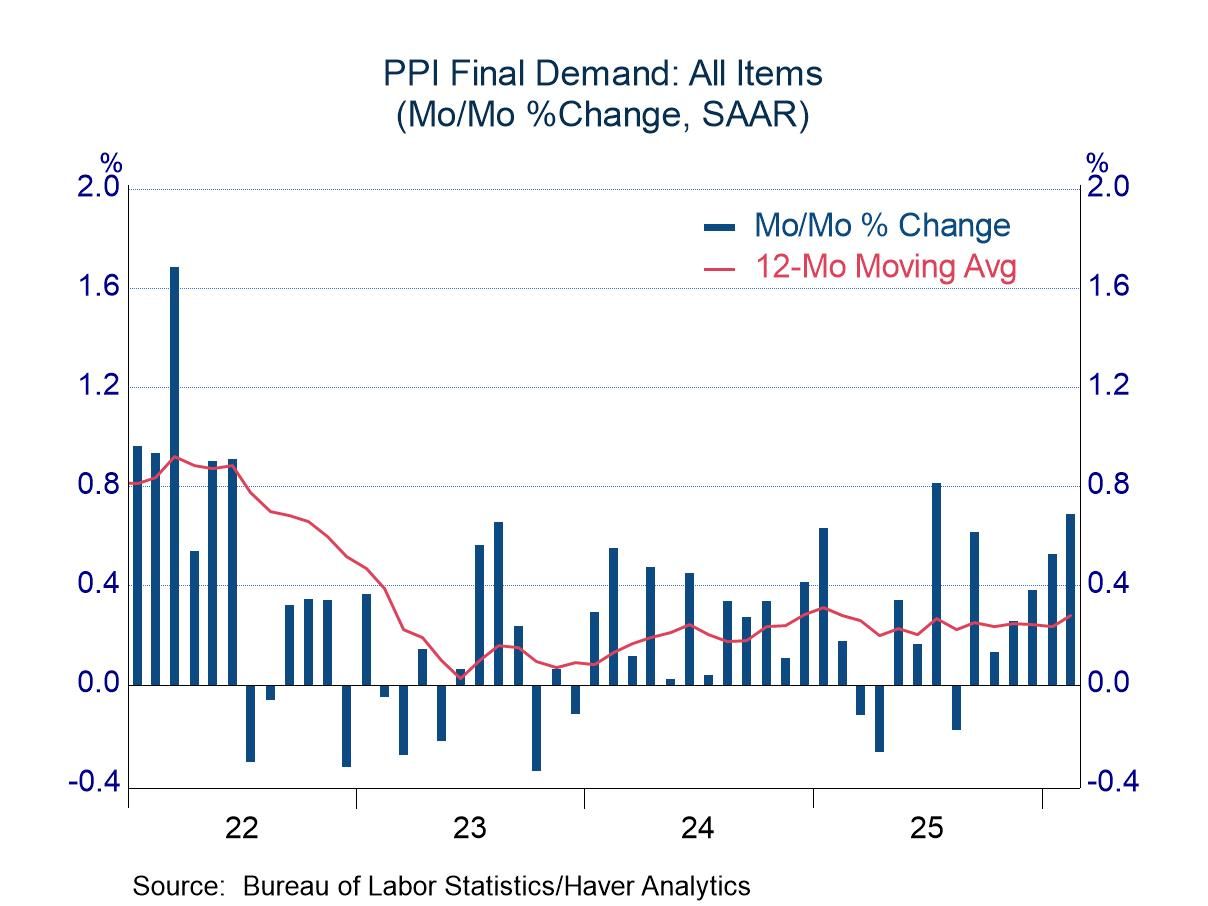

- The volatile food and energy components jumped...

- ...But other items also showed upward pressure.

USA| Mar 18 2026

USA| Mar 18 2026February PPI: Troubling Inflation Figures

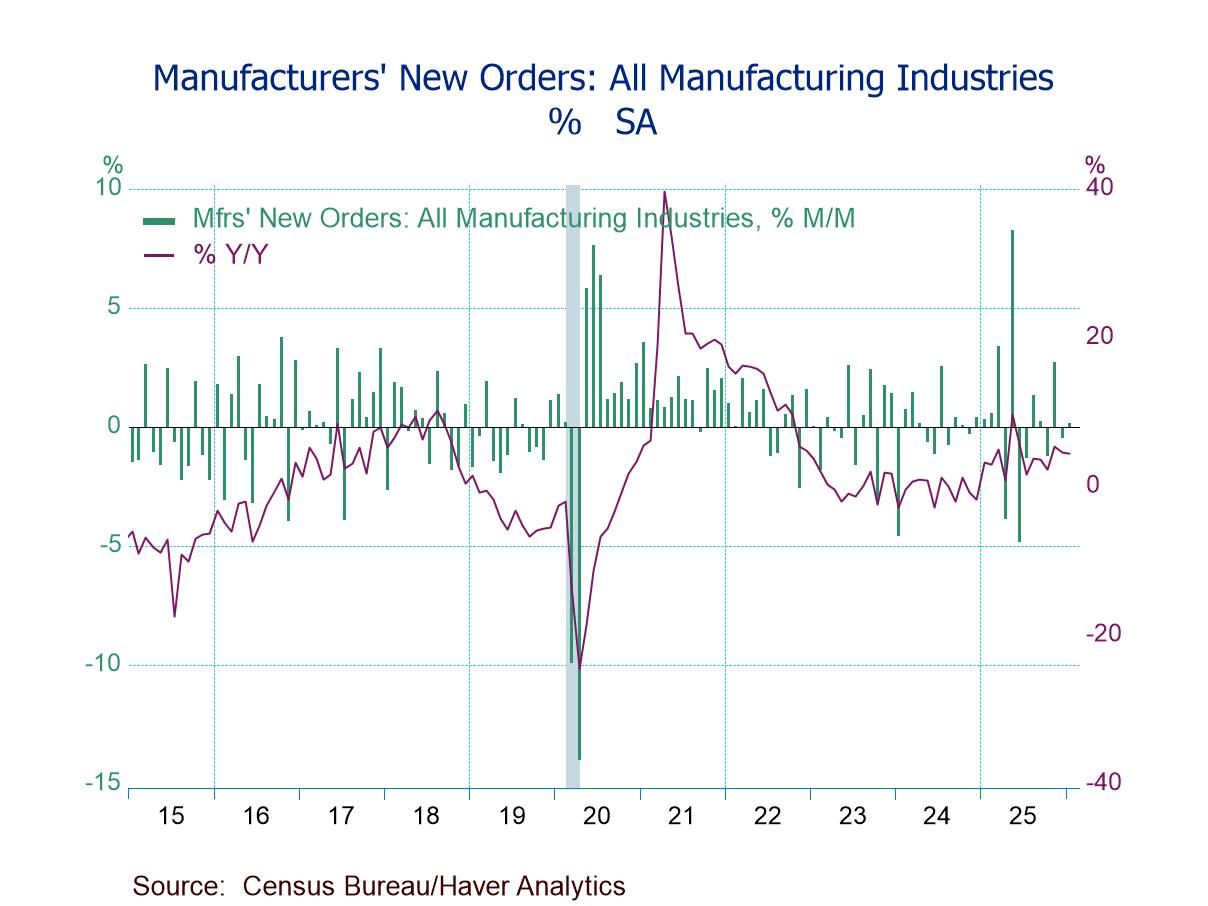

- January factory orders +0.1% m/m (+4.4% y/y); second m/m gain in three months and 7.7% above the Jan. ’24 low.

- Durable goods flat; nondurable goods orders +0.3% m/m; shipments +0.5% m/m.

- Transportation orders -0.8% m/m, led by a 23.8% plunge in defense aircraft orders.

- Unfilled orders +0.8%, the sixth straight m/m rise.

- Inventories +0.1%, the third consecutive m/m increase.

USA| Mar 18 2026

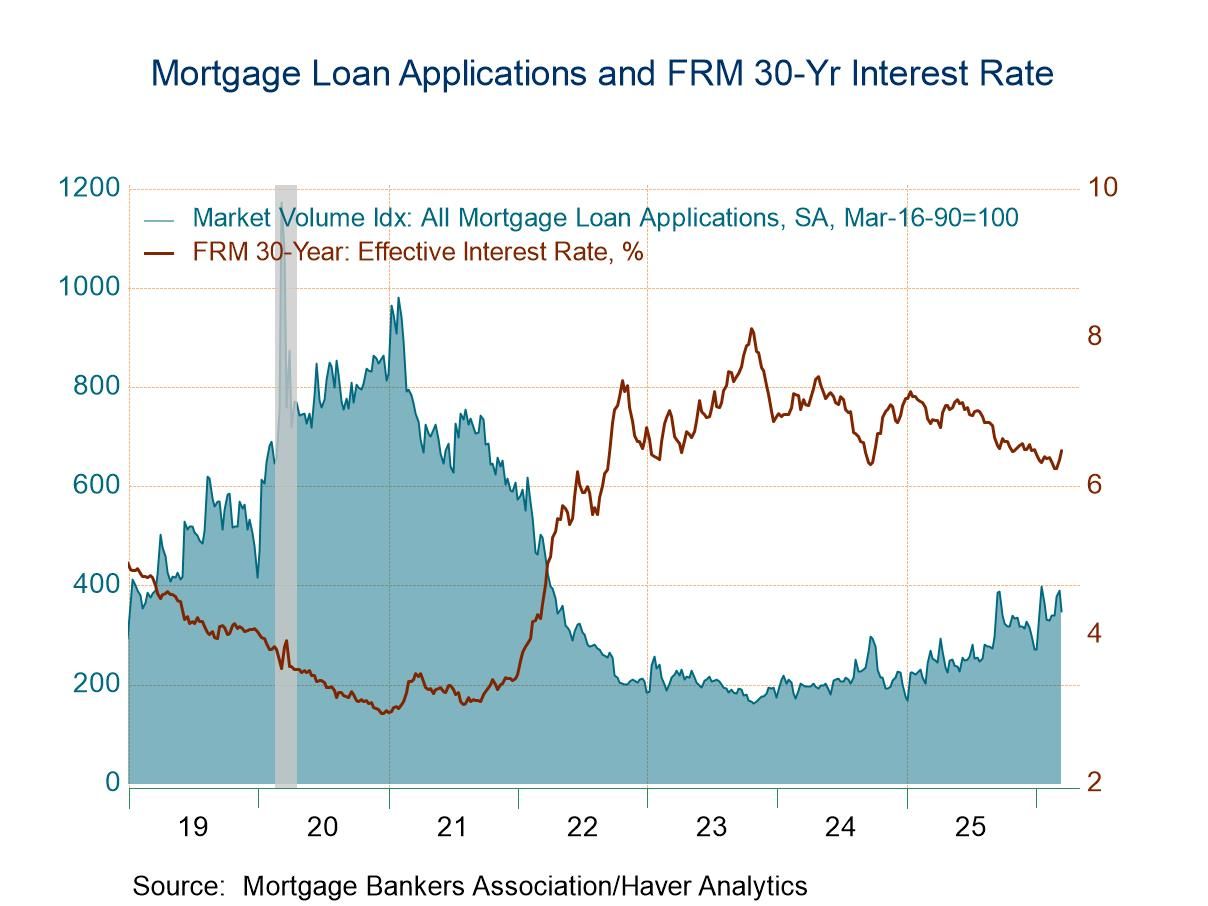

USA| Mar 18 2026U.S. Mortgage Applications Dropped in the March 13 Week

- Applications for loans to purchase edged up, while applications for loan refinancing plummeted.

- Effective interest rate on 30-year fixed loans rose 12bps to 6.48%.

- Average loan size declined.

Germany| Mar 17 2026

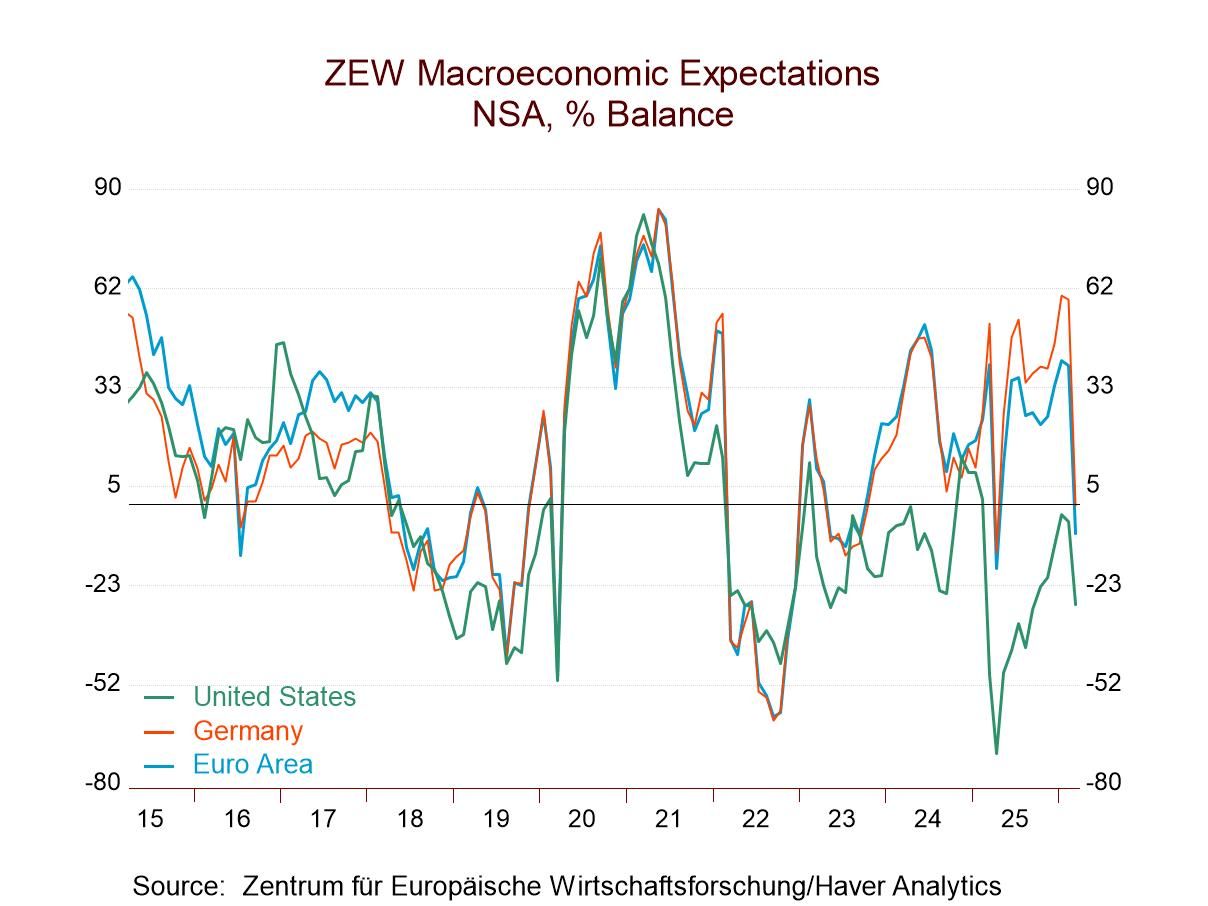

Germany| Mar 17 2026Germany’s ZEW Survey Sours

The ZEW survey, which is a survey of German financial experts, showed a weakening in March as the economic situation deteriorated sharply in the wake of the start of the war in Iran. For the euro area, the reading dropped to -29.9 in March from -13.6 in February; for Germany, the reading surprisingly improved a slight bit to -62.9 from -65.9; for the United States, a positive reading of 4.5 was still posted; however, it was down significantly from +19.6 in February. China’s reading fell to -33.7 from -31.5. The rank standings for these readings on data back to late-1992 for most reporters, but only back to April 2021 for China, shows the euro area at a reading near its median over this span. While Germany and the U.S. are substantially below their medians, with percentile standings near 30% for Germany and near the 40th percentile for the U.S. China logs a stronger queue standing above its median at 68.3%.

Macro expectations fell more clearly and sharply for all the reporters in March. For Germany, the drop was to -0.5 in March from +58.3 in February, while the U.S. drop was to -28.7 from -5.1 in February. China’s drop was to -15.8 from +13.1 in February. The standings for these March readings place China at a 1.7 percentile standing, the U.S. at a 16.1 percentile standing, and Germany at a 25.1 percentile standing. All of them are quite weak in the lower quartile of their respective queues of data.

With oil prices jumping sharply, inflation expectations have simply skyrocketed on the month. For the euro area, the reading that was near 0 in February jumped to 79 in March. For Germany, a reading of -2.3 in February surged to 79.2 in March. For the U.S., an inflation expectation of 43.1 in February nearly doubled to 80.4 in March. For China, a February reading of 10.5 ran up to 56.0 for March. The queue percentile standings for the March readings rose to the 98th percentile for the euro area, Germany, and the U.S., while China's standing also moved up strongly to its 93rd percentile, when ranked over a shorter period extending back to April 2021.

With inflation going up, short-term interest rate expectations rose as well. Those expectations rose in the euro area, the U.S., and China. For each of these reporters, there was a significant increase in the short-term rate expectations. The euro area expectation survey value has a standing in its 70.9 percentile, China’s standing is at its 55th percentile, while the U.S. standing is still below its median at its 22.4 percentile.

Long-term rate expectations moved up in all areas as well, with Germany's new reading having a 66.8 percentile standing, China at a 75th percentile standing, and the U.S. at a 59th percentile standing. Each one of these is above its historic median. Long-term expectations are elevated.

Stock markets in all areas weakened in March compared to February, with most showing declines of about 50% or so in this survey. The queue standings for the new readings are all in the lower 25th percentile of their respective data queues. Some of them are significantly lower, such as Germany, which stands only in its 9th percentile. On balance, the attack in Iran has been a game-changer for economic perceptions and expectations. Markets are wary. And everyone knows the centerpiece is the Strait of Hormuz. But that does not make it much easier to handicap the future.

USA| Mar 16 2026

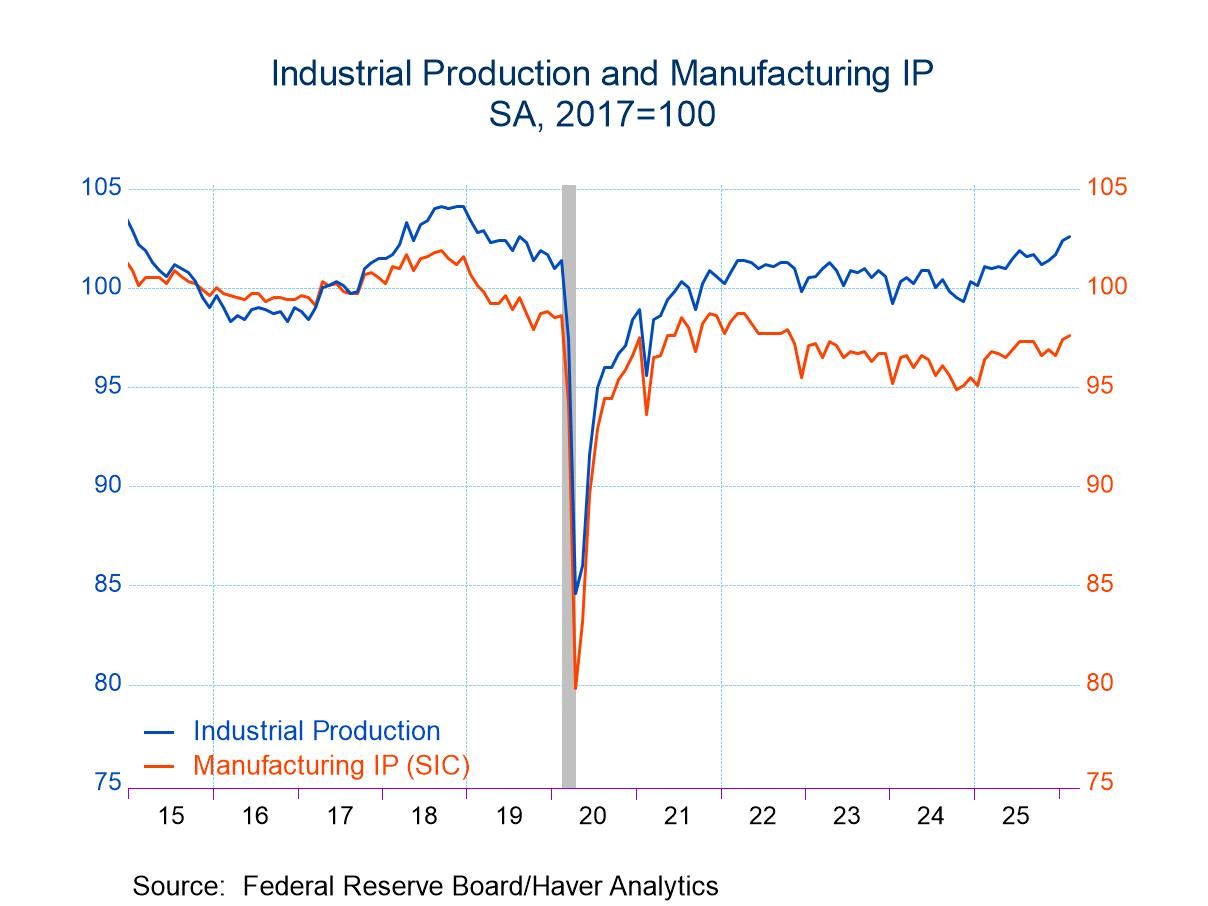

USA| Mar 16 2026U.S. Industrial Production Edged Up in February

- Total industrial output increased 0.2% m/m in February, slightly larger than expected.

- There was no revision to January, but there were small upward revisions to November and December.

- Manufacturing output increased 0.2% m/m, mining rose 0.8%, while utilities production slid 0.6% m/m.

- The headline rate of capacity utilization was unchanged in February and remained well below its long-term average.

by:Sandy Batten

|in:Economy in Brief

Canada| Mar 16 2026

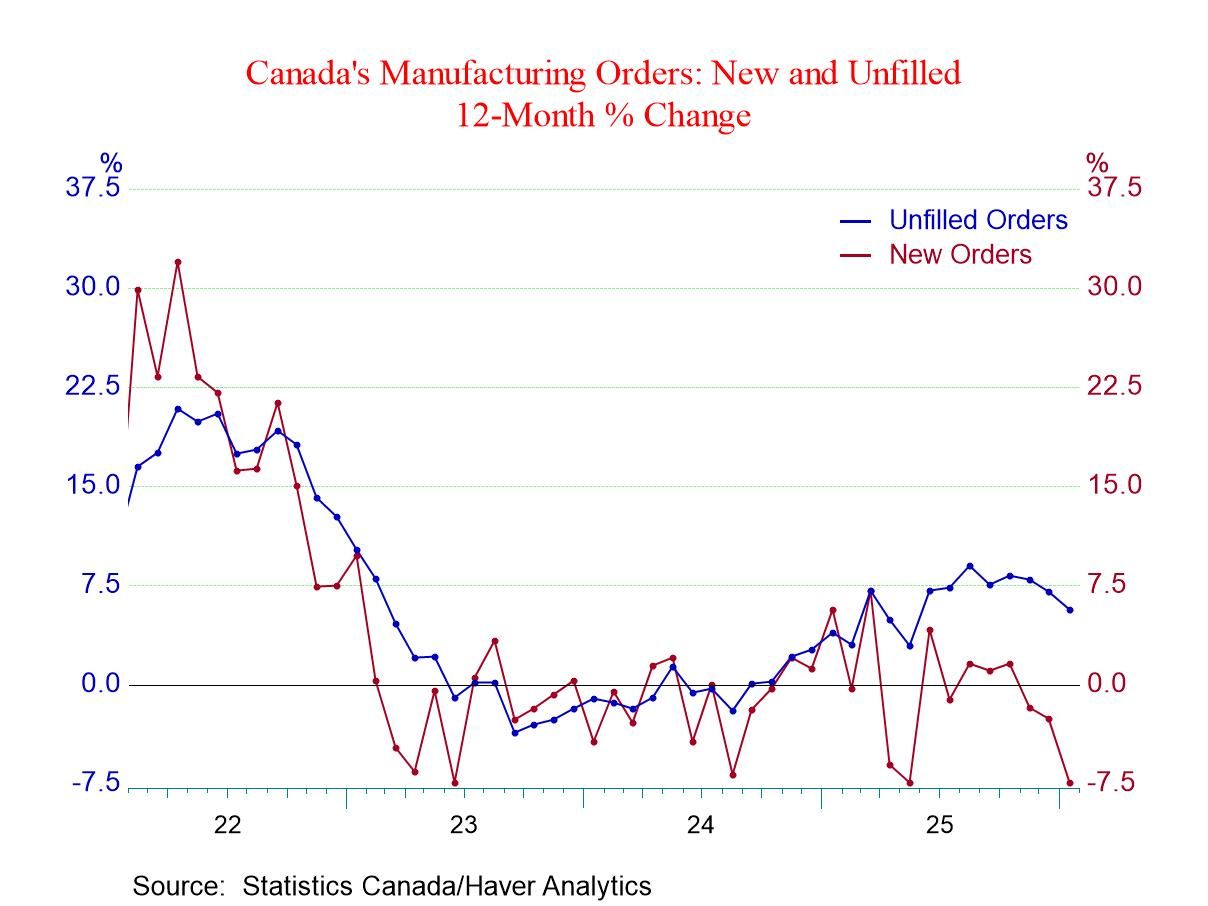

Canada| Mar 16 2026Canada’s Industrial Orders Falter

Canadian orders fell by 3.3% in January after running flat in December and falling by 1.1% in November.

The top-line sequential growth in orders shows contraction over 12 months, six months, and three months, with the pace of contraction having gotten more severe over the most recent three months.

In January, orders declined, while unfilled orders rose but decelerated from their December growth rate. Manufacturing shipments fell, durables shipments fell, durable shipments excluding motor vehicles fell, and motor vehicle shipments fell. In addition, nondurables orders declined in January although at a lesser pace than in December. Among this key batch of industrial statistics, only manufacturing inventories rose in January, increasing by 0.9%.

Progressive growth rates from 12 months to six months to three months show progressively weaker growth in shipments of durable goods, durables excluding motor vehicles, and motor vehicle shipments themselves. Inventories are also shrinking, and at a progressively faster pace over shorter periods. The headline series for orders shows a 16.5% annual rate contraction over three months, compared with a contraction pace of 7.4% over 12 months. There is no sign of stabilization in orders, and this shows up plainly in the data or on the chart.

The column heading marked “standing” shows that the standings of all the items listed in the stub are below 50%, placing each entry below its median based on data back to 1999. Judging from 12 month growth rates, the only exception is unfilled orders, which are right at the 50.4 percentile mark. For the most part, the shortfalls from their respective medians are quite severe, with the low standings for manufacturing shipments and durable goods shipments at 7.4%, out done only by a 1.8 percentile standing for motor vehicle shipments growth. The table also ranks the categories on six month growth rates, providing a slightly shorter term view to see how much conditions improve. On that basis, and viewed in that way, most of the rankings do improve. In fact, all rankings improve compared to the year over year growth rate rankings except for three: unfilled orders, durable goods shipments, and durable goods shipments excluding motor vehicles.

The six-year growth from January 2020 to date shows declines in real terms (inflation-adjusted net changes) for unfilled orders, durable goods shipments, durables shipments excluding motor vehicles, and inventories of manufactured goods. Increasing on balance over six years are orders and total manufacturing shipments, but by very thin margins. Motor vehicle shipments are up by 0.7% in real terms over six years, while nondurables shipments are up by 2.1% on balance over the same period. It has been a very difficult period for industry to cope with the strains from COVID, the war in the Ukraine, and more recently, the imposition of tariffs by the United States.

Asia| Mar 16 2026

Asia| Mar 16 2026Economic Letter from Asia: Strait Squeeze

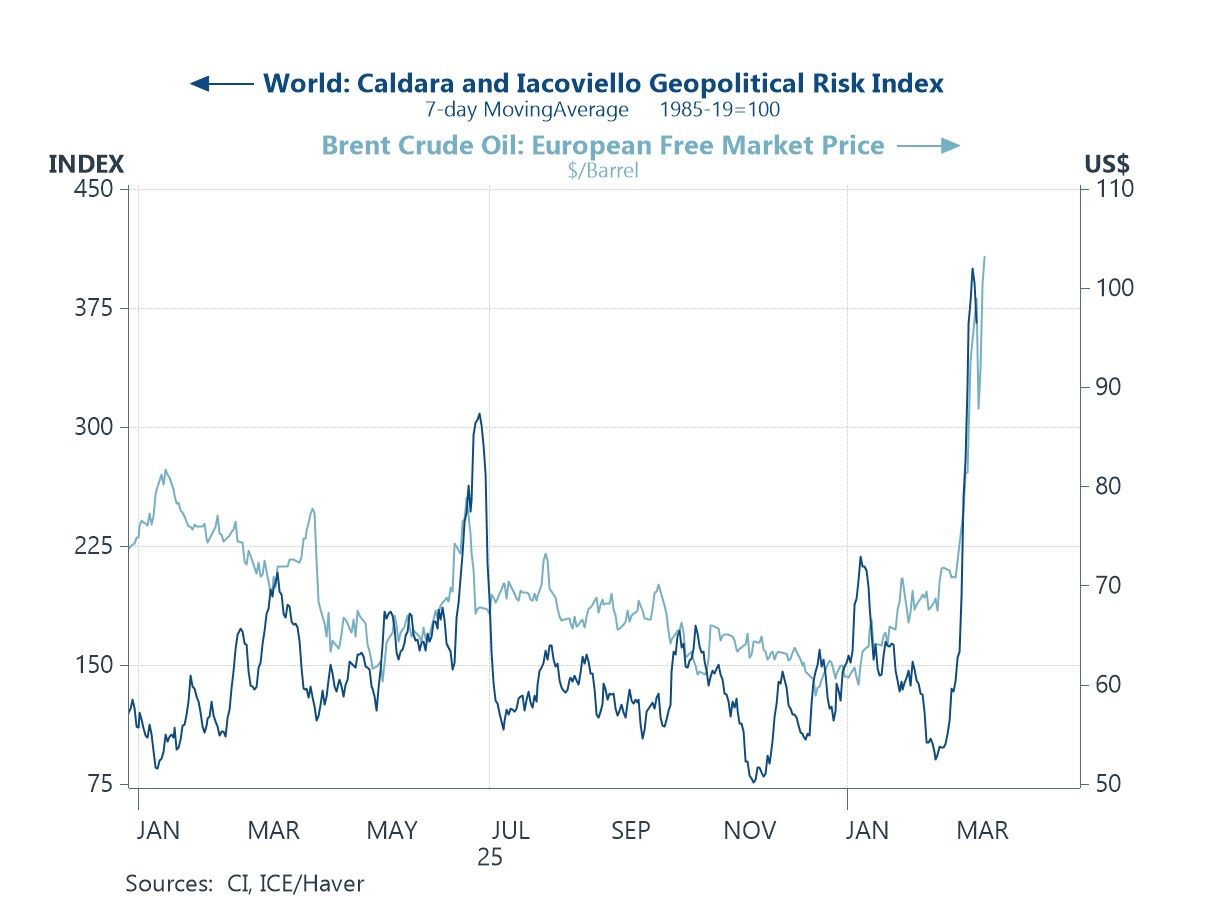

In our Letter this week, we examine the ongoing Iran war through an Asian lens. Geopolitical uncertainty and crude oil prices have remained elevated (chart 1), despite early reports concerning the potential for a brief conflict that tempered investor caution. Attention has now centred on the Strait of Hormuz, through which a significant share of global oil typically flows. With shipments now nearly halted (chart 2), much of the world’s energy flow has effectively stalled. While these developments have broad global implications, their impact on Asian economies is more nuanced. This partly reflects differences in energy mixes across the region (chart 3), as well as the historical relationship between oil prices and energy inflation (chart 4). Further compounding the challenges faced by Asian oil importers are currency effects: a broader risk-off turn in markets has weighed on several Asian currencies (chart 5), raising the local-currency cost of energy imports. Amid these pressures, several regional central banks are also set to decide on policy this week (chart 6), alongside major Western counterparts such as the Federal Reserve. Near-term rate cut expectations have been pushed back in many cases amid renewed inflation concerns, while in some Asian economies markets are even pricing in the possibility of further rate hikes.

The Iran war Two weeks in, the Iran war continues with no clear end in sight. Crude oil prices and geopolitical risk therefore remain elevated, as shown in chart 1, despite earlier news that had briefly tempered investors’ heightened caution. Even reports that the 32 members of the International Energy Agency are set to release around 400 million barrels in emergency reserves have done little to curb the surge in crude prices. Latest reports indicate that reserves for Asia will be released immediately, while supplies for Europe and the Americas will only become available from the end of March. Meanwhile, uncertainty surrounding the Strait of Hormuz continues to underpin elevated prices. The strait—currently blocked by Iran—handles roughly 20% of global oil flows. Iran has recently indicated that it may allow ships from certain countries to transit the waterway, though the situation remains fluid.

USA| Mar 13 2026

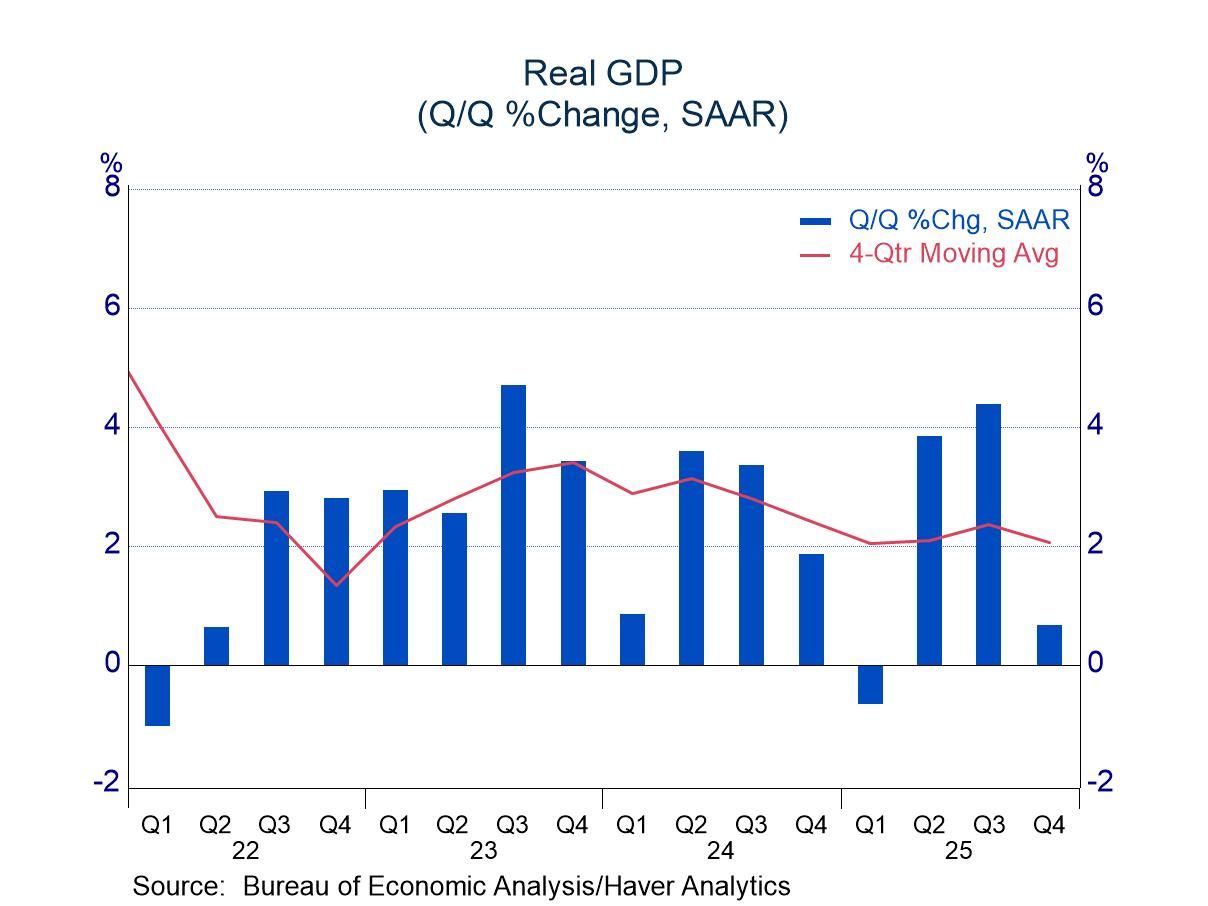

USA| Mar 13 2026Revised Q4 GDP: Downward Adjustment Leaves Modest Growth

- Consumer spending and business investment in structures accounted for most of the adjustment.

- Although growth was slow, the results were not alarming.

- of2725Go to 23 page