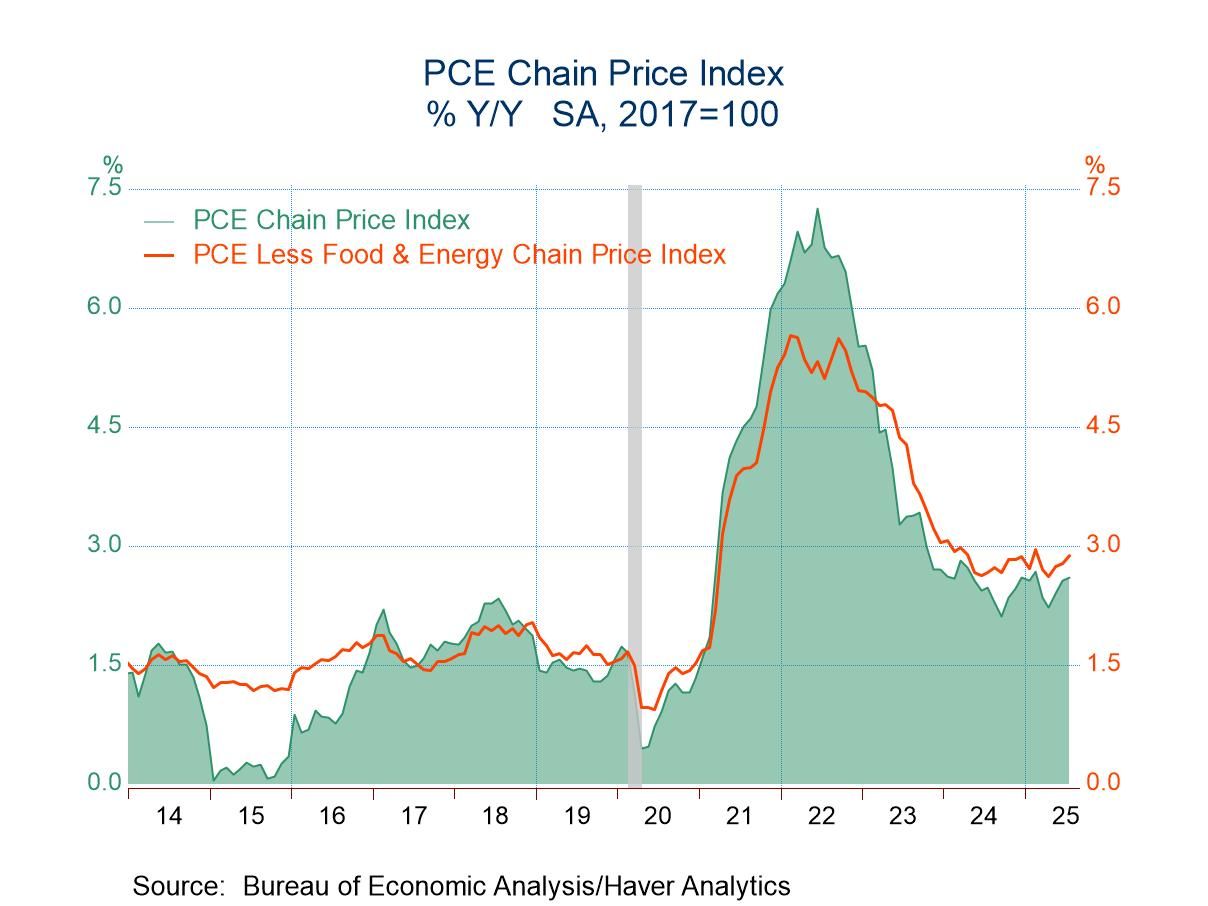

- Core price increase y/y matches highest since February.

- Real spending moderation centers on services.

- Real disposable income improves; personal savings rate steadies.

by:Tom Moeller

|in:Economy in Brief

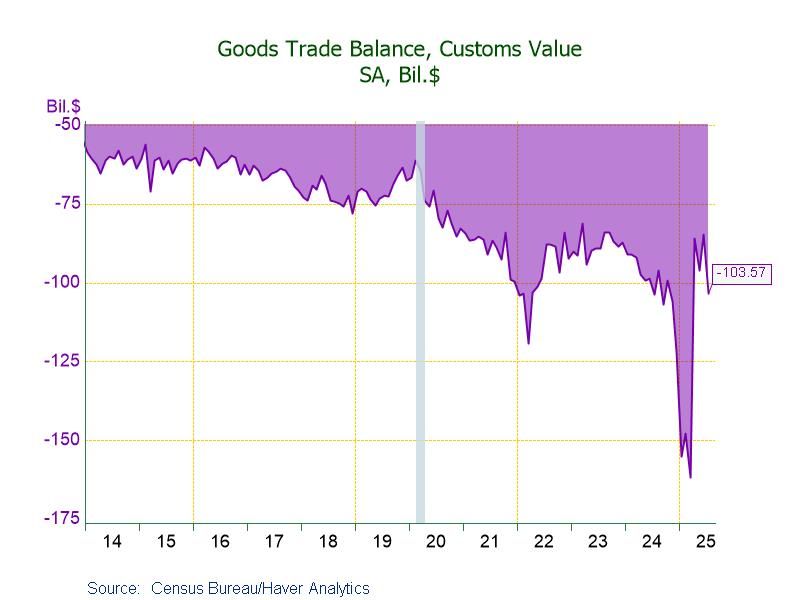

- Deficit: $103.57 bil. in July, jumping 22.1% from June’s $84.85 bil.

- Exports -0.1%, down for the third straight month, led by a 2.4% decline in exports of other goods.

- Imports +7.1%, up for the first time since March, led by a 25.4% surge in imports of industrial supplies & materials.

Europe| Aug 29 2025

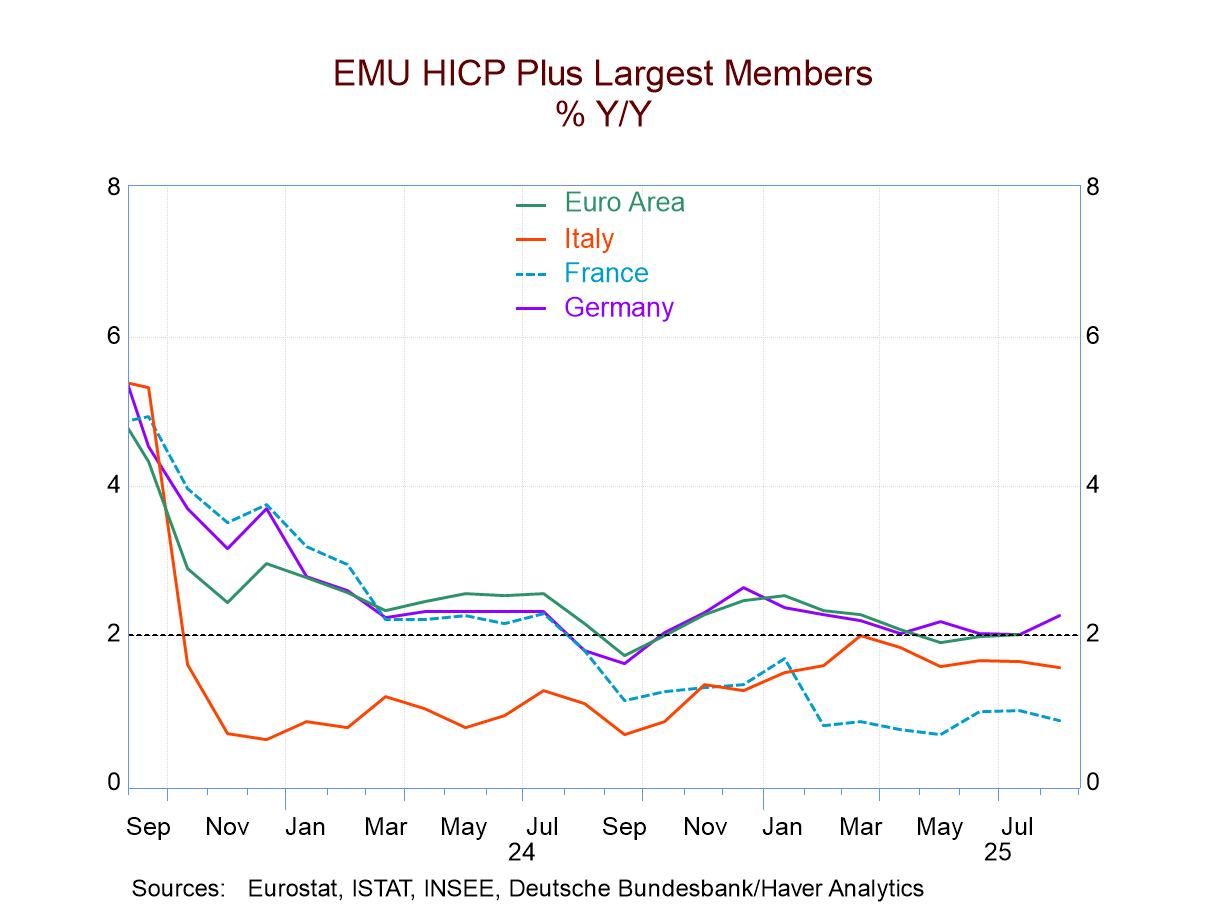

Europe| Aug 29 2025EMU Large Country Inflation Runs Cold – Over Tepid Cores

Inflation in the monetary union was tepid across the large, early-reporting, economies in August. The HICP rose by 0.2% on the month in Germany, rose by 0.1% in France, while it was flat in both Italy and Spain. However, these outstanding readings followed several months of stronger inflation; in particular in July German prices rose by 0.2%, in Italy the gauge rose by 0.3%, in France by 0.4%, and in Spain by 0.5%.

As a result, over three months, inflation is running hot on the headline gauge, over 2% in France, Italy, and Spain, and just below it, at a 1.8% annual rate in Germany. Over 12 months, inflation is well behaved, but that headline is up 0.8% in France, rises by 1.7% over 12 months in Italy, by 2.1% in Germany, and at a 2.6% pace in Spain. That is a bit more mixed but still quite solid set of results. The EMU-wide HICP for July – on a one-month lag- rises by 2.1% over 12 months with a core at 2.3%.

Core inflation is not well reported on an early basis. The Italian core rate rose 0.2% in August with Spain at 0.3%; both Italy and Spain logged increases of 0.3% in July and in June and as a result the 3-month inflation rate on the core for Italy and Spain runs at 2.7% in Italy and at 3.8% for Spain. These, of course, are much higher and more disturbing numbers for inflation. The 6-month inflation rate for core Italy and Spain runs at 2.9% and 3.1%, respectively, while over 12 months the Italian core is up by only 2.1% and the Spanish core is up by only 2.4%. The kick up and inflation for the core is a relatively recent phenomenon.

Global| Aug 28 2025

Global| Aug 28 2025Charts of the Week: Riskbusters

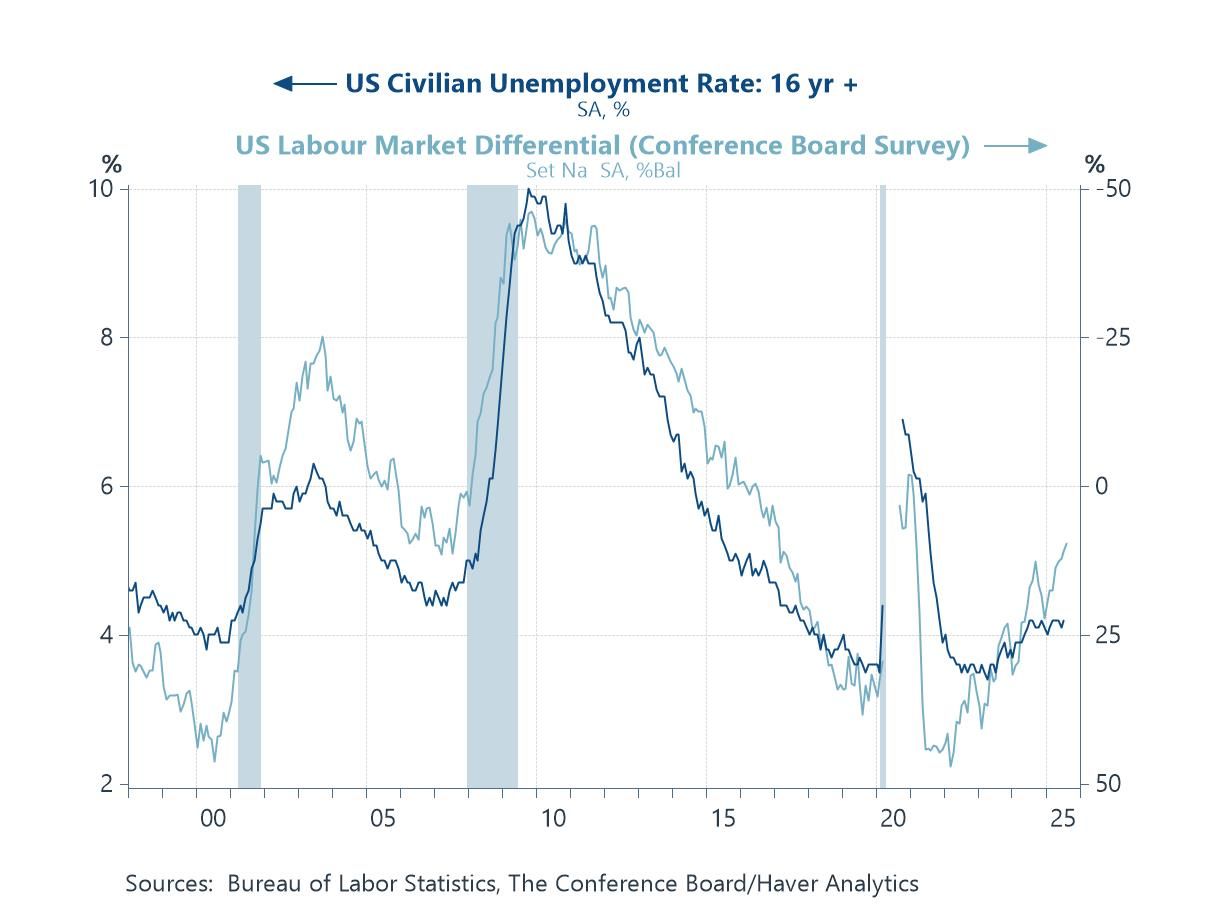

Global markets have continued to rally into late summer, buoyed by AI optimism, dovish signals from central bankers at Jackson Hole, and expectations of easier policy ahead. Yet beneath the surface, risks to the world economy are accumulating. In the US, labour market indicators point to softening conditions (chart 1), while tariff-driven pressures are beginning to push goods prices higher (chart 2). Global trade flows are being reshaped by US policy, with China’s excess capacity increasingly diverted toward Europe, most visibly through surging exports of electric vehicles (EVs) (charts 3 and 4). At the same time, wage growth remains stubbornly elevated in the UK, complicating disinflation (chart 5), while concerns are mounting over the country’s external vulnerabilities as net FDI and portfolio positions weaken against the backdrop of jittery debt markets (chart 6). Together, these dynamics highlight the tension between buoyant market performance and a global economy still grappling with structural fragilities.

by:Andrew Cates

|in:Economy in Brief

USA| Aug 28 2025

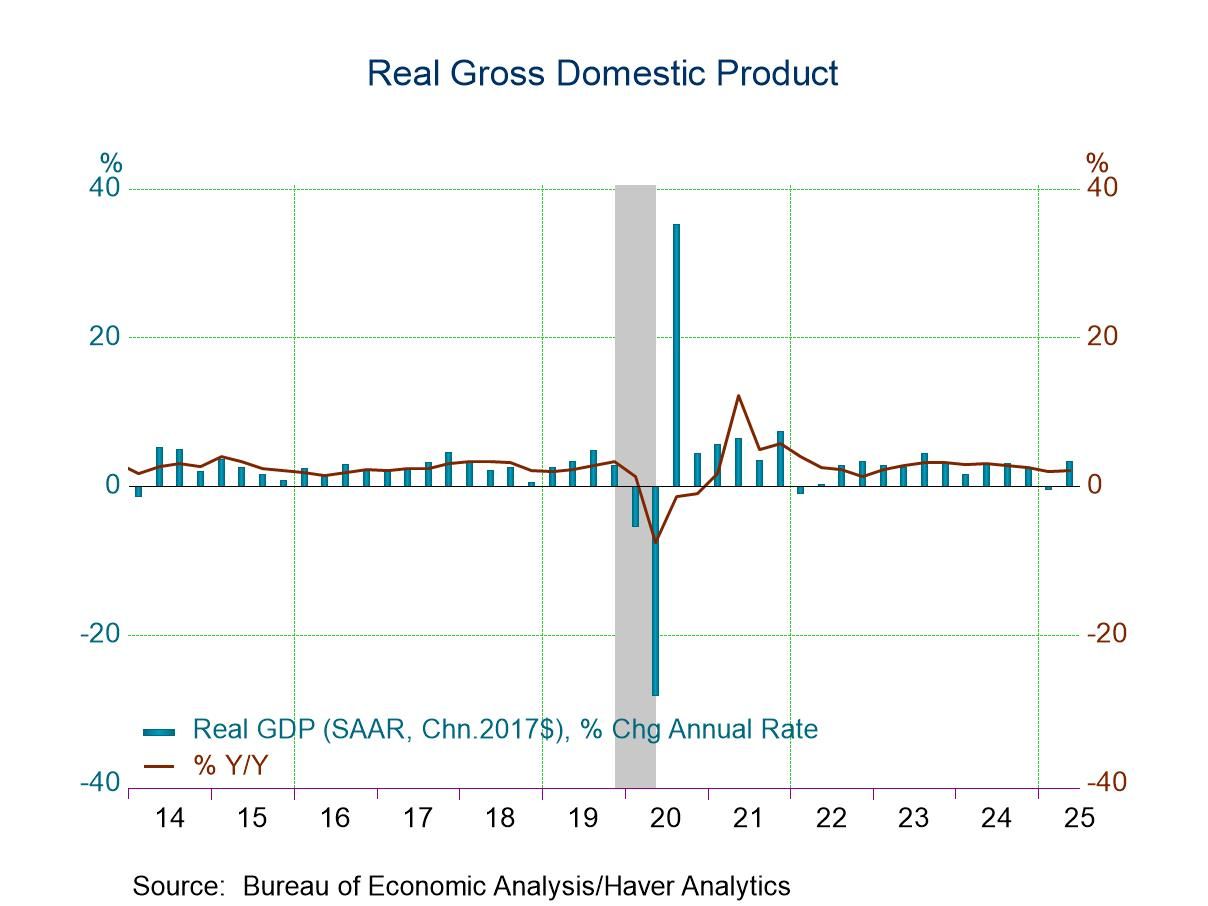

USA| Aug 28 2025U.S. GDP Q2’25 Growth Revised Up; Profits Improve

- Business investment strengthens & consumer spending firms.

- U.S. business earnings reverse Q1 decline.

- Increase in price index is unrevised, remaining roughly half of Q1’s gain.

by:Tom Moeller

|in:Economy in Brief

USA| Aug 28 2025

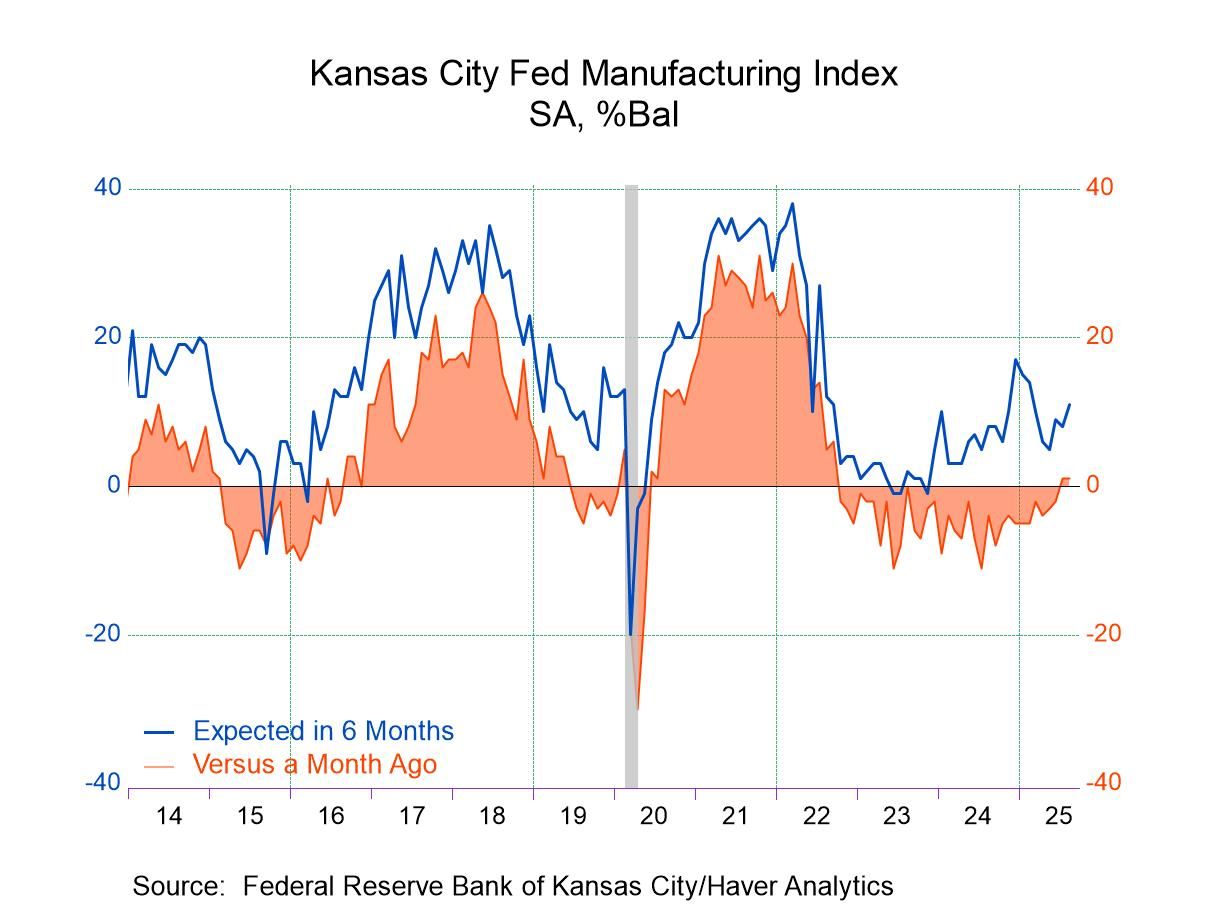

USA| Aug 28 2025FRB Kansas City Manufacturing Index Unchanged in August

- Index remained (though barely) in positive territory for the second consecutive month, indicating that manufacturing activity was inching up.

- Prior to last month, the index had been negative for 22 consecutive months.

- Positive readings across most key components.

by:Sandy Batten

|in:Economy in Brief

USA| Aug 28 2025

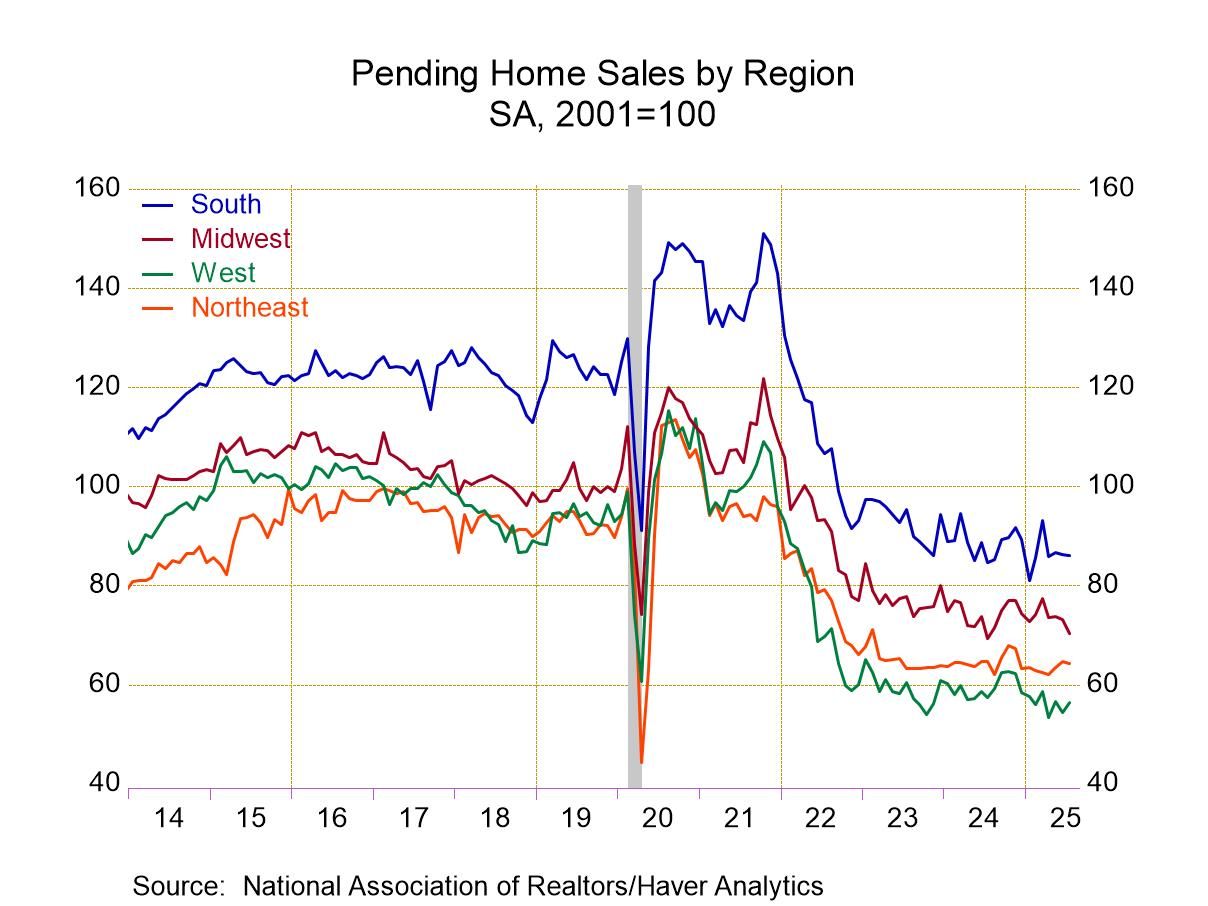

USA| Aug 28 2025U.S. Pending Home Sales Decline in July

- Decline adds to June weakness.

- Regional changes are mixed.

by:Tom Moeller

|in:Economy in Brief

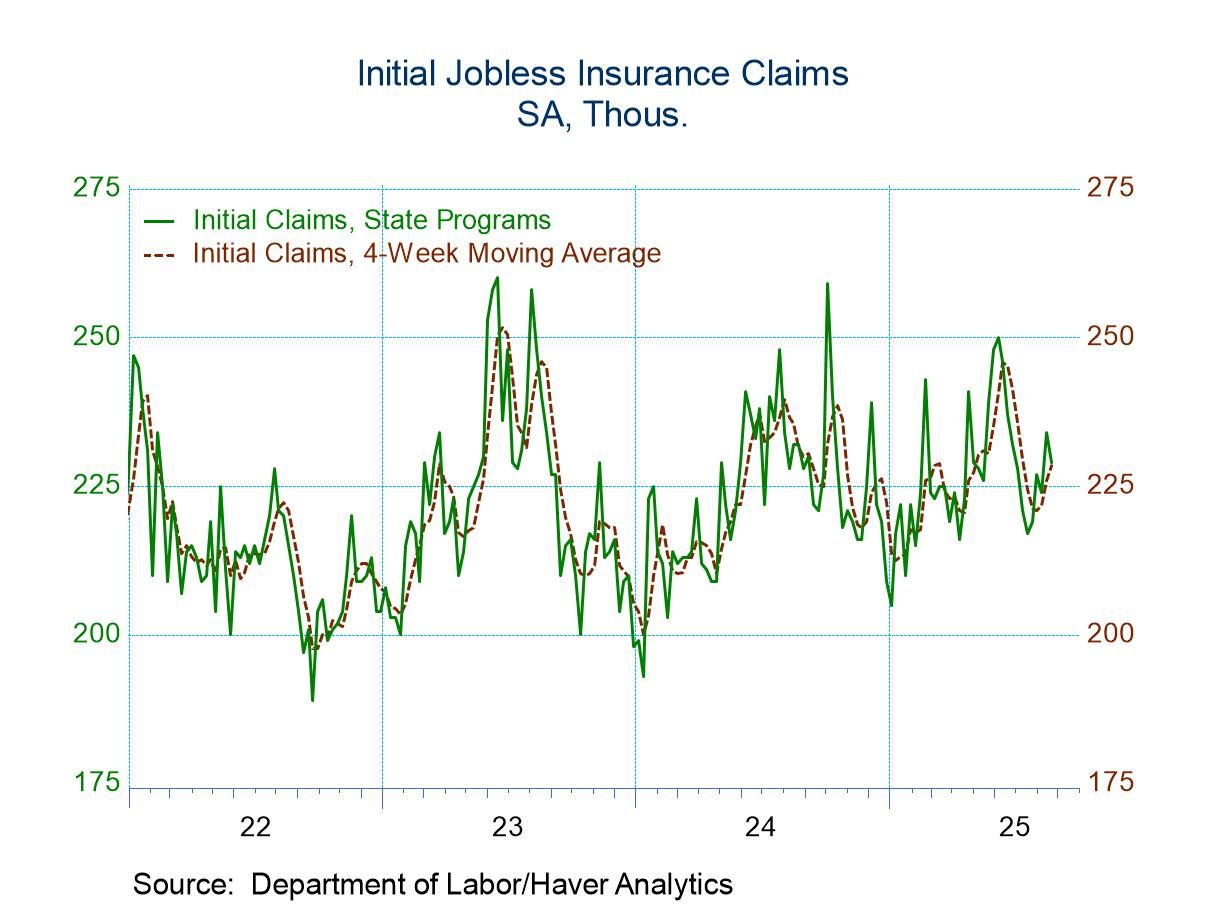

- Initial claims declined in latest week after a surge in the prior week.

- Continuing claims declined.

- Insured unemployment rate holds steady.

- of9Go to 1 page