Global| Aug 28 2025

Global| Aug 28 2025Charts of the Week: Riskbusters

by:Andrew Cates

|in:Economy in Brief

Summary

Global markets have continued to rally into late summer, buoyed by AI optimism, dovish signals from central bankers at Jackson Hole, and expectations of easier policy ahead. Yet beneath the surface, risks to the world economy are accumulating. In the US, labour market indicators point to softening conditions (chart 1), while tariff-driven pressures are beginning to push goods prices higher (chart 2). Global trade flows are being reshaped by US policy, with China’s excess capacity increasingly diverted toward Europe, most visibly through surging exports of electric vehicles (EVs) (charts 3 and 4). At the same time, wage growth remains stubbornly elevated in the UK, complicating disinflation (chart 5), while concerns are mounting over the country’s external vulnerabilities as net FDI and portfolio positions weaken against the backdrop of jittery debt markets (chart 6). Together, these dynamics highlight the tension between buoyant market performance and a global economy still grappling with structural fragilities.

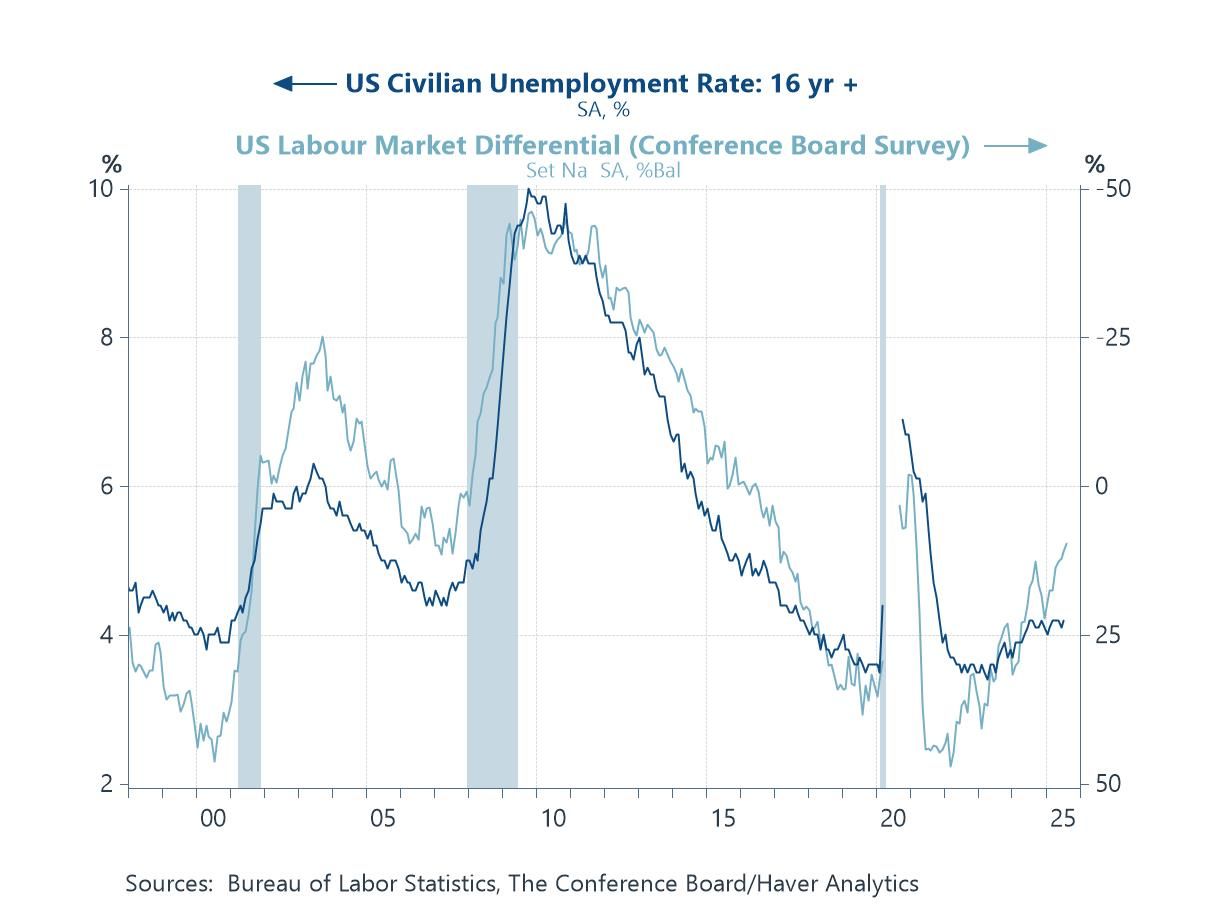

The US labour market The latest data highlight a growing sense of fragility in the US labour market. The unemployment rate, while still relatively low by historical standards, has been edging higher through the course of this year. More telling, however, is the signal from this week’s consumer confidence survey from Conference Board and specifically the labour market differential — the gap between the share of consumers saying jobs are plentiful versus those saying jobs are hard to get. That balance has narrowed sharply, moving back toward levels historically associated with softer labour demand and rising unemployment.

Chart 1: US unemployment versus the Conference Board’s labour market differential gauge

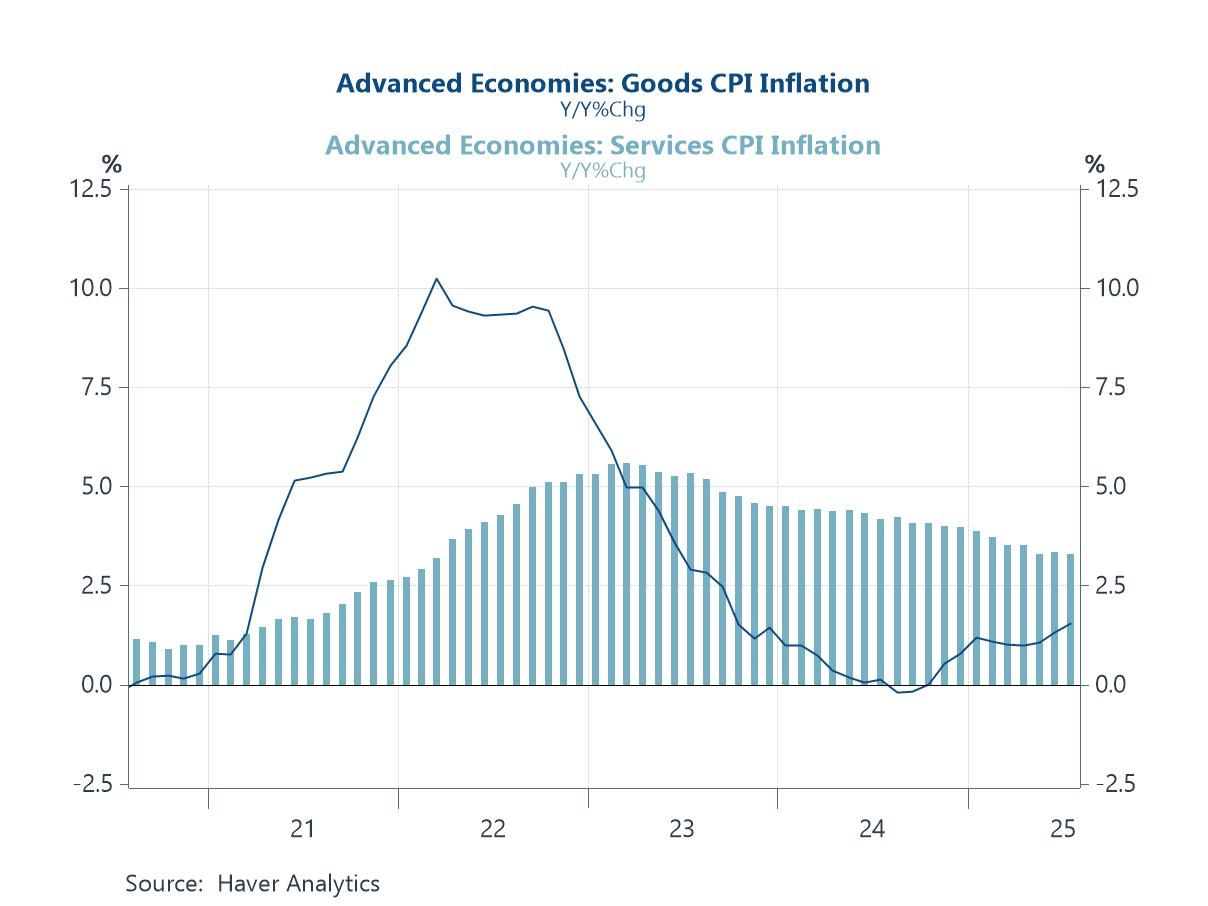

Goods and services inflation Haver’s breakdown of goods and services CPI inflation in the advanced economies highlights where fresh risks are emerging. Goods inflation, which had been receding sharply after the pandemic supply shocks, has recently shown signs of firming again. Some of this probably reflects the impact of US tariff policies, which are raising import costs and putting renewed upward pressure on traded goods prices. While services inflation remains the more stubborn component in most advanced economies, the risk is that tariffs could reintroduce stickiness into goods prices, slowing the overall disinflation process.

Chart 2: Goods and services CPI inflation in advanced economies

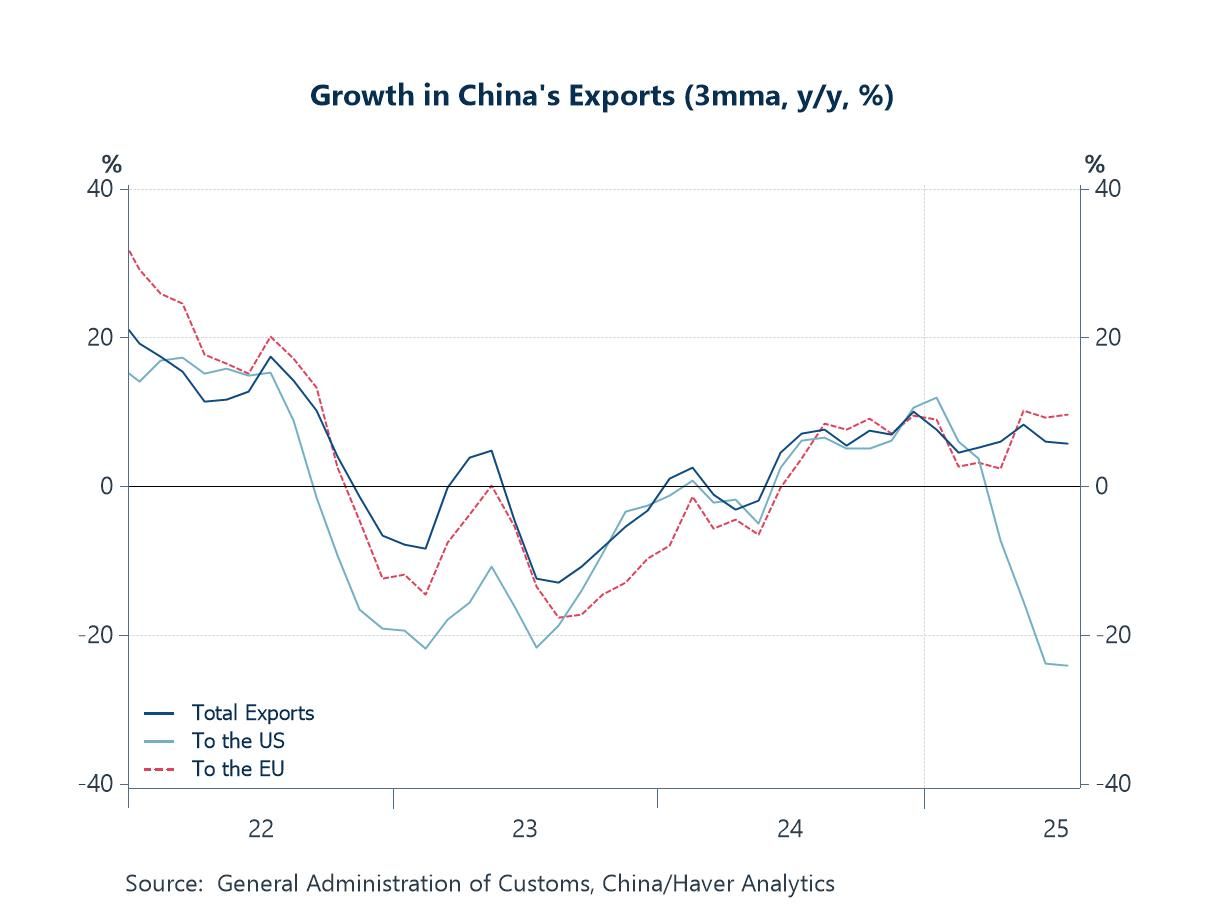

China, Europe and US trade policy A consequence of US tariff policies has been a sharp contraction in Chinese exports to the US market, with much of the surplus redirected elsewhere. Europe in particular has recorded near double-digit import growth in recent months, raising concerns that Beijing is deflecting its industrial overcapacity problem rather than resolving it, effectively transferring the pressure onto trading partners. China’s authorities, however, have begun to push back, introducing measures to curb excess supply and rein in so-called “involution,” including clampdowns on price wars across several industries.

Chart 3: China’s exports to the US and Europe

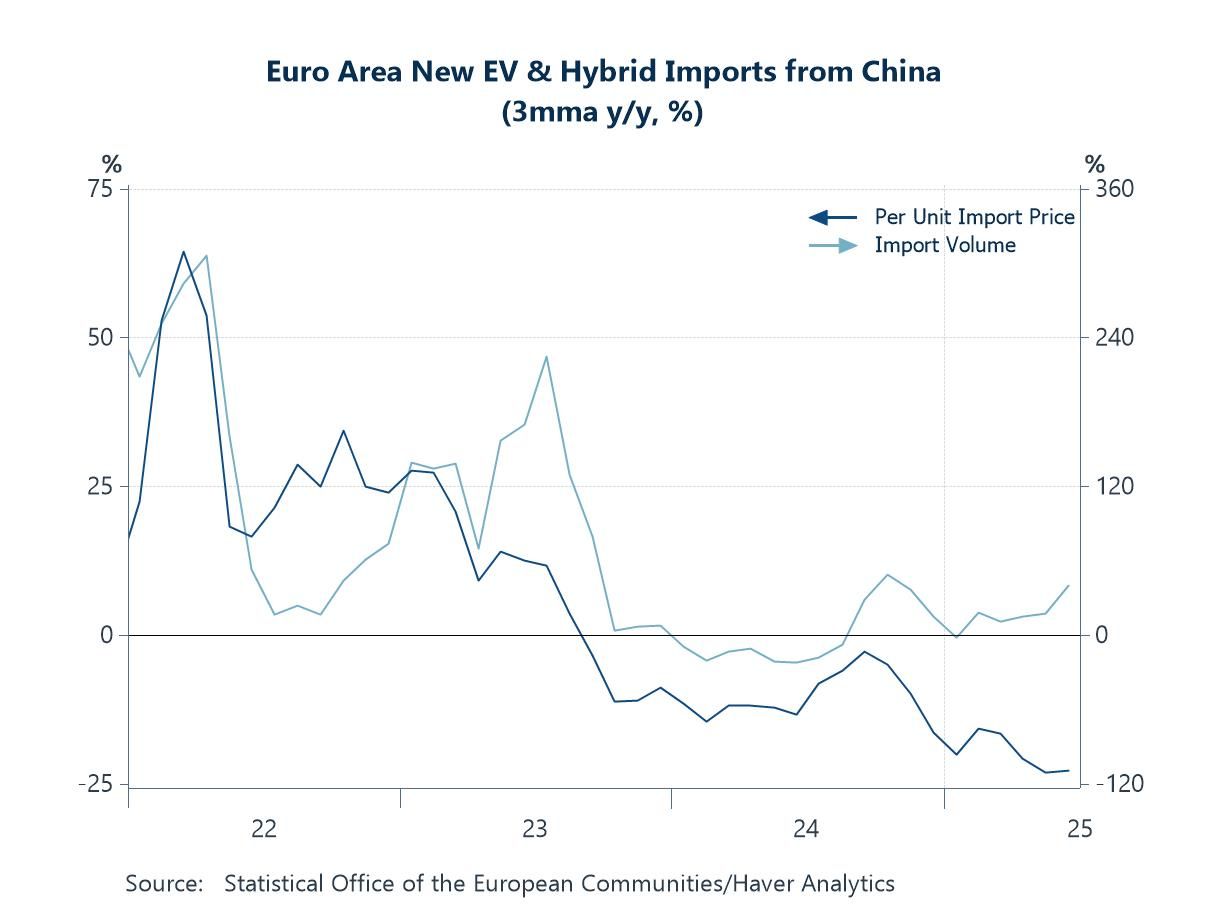

China’s excess capacity and Europe A closer look at Europe–China trade shows that electric vehicles remain a key flashpoint. Import volumes from China have continued to rise even as per-unit prices fall sharply from a year ago —evidence suggesting that industrial overcapacity persists, with low-cost Chinese EVs increasingly challenging European automakers. The surge has carried on despite EU tariffs of up to 45% on battery EVs, as Chinese producers have adapted by pushing plug-in hybrids and expanding onshore production in Europe to bypass duties and defend market share.

Chart 4: The euro area’s EV and Hybrid Car Imports from China

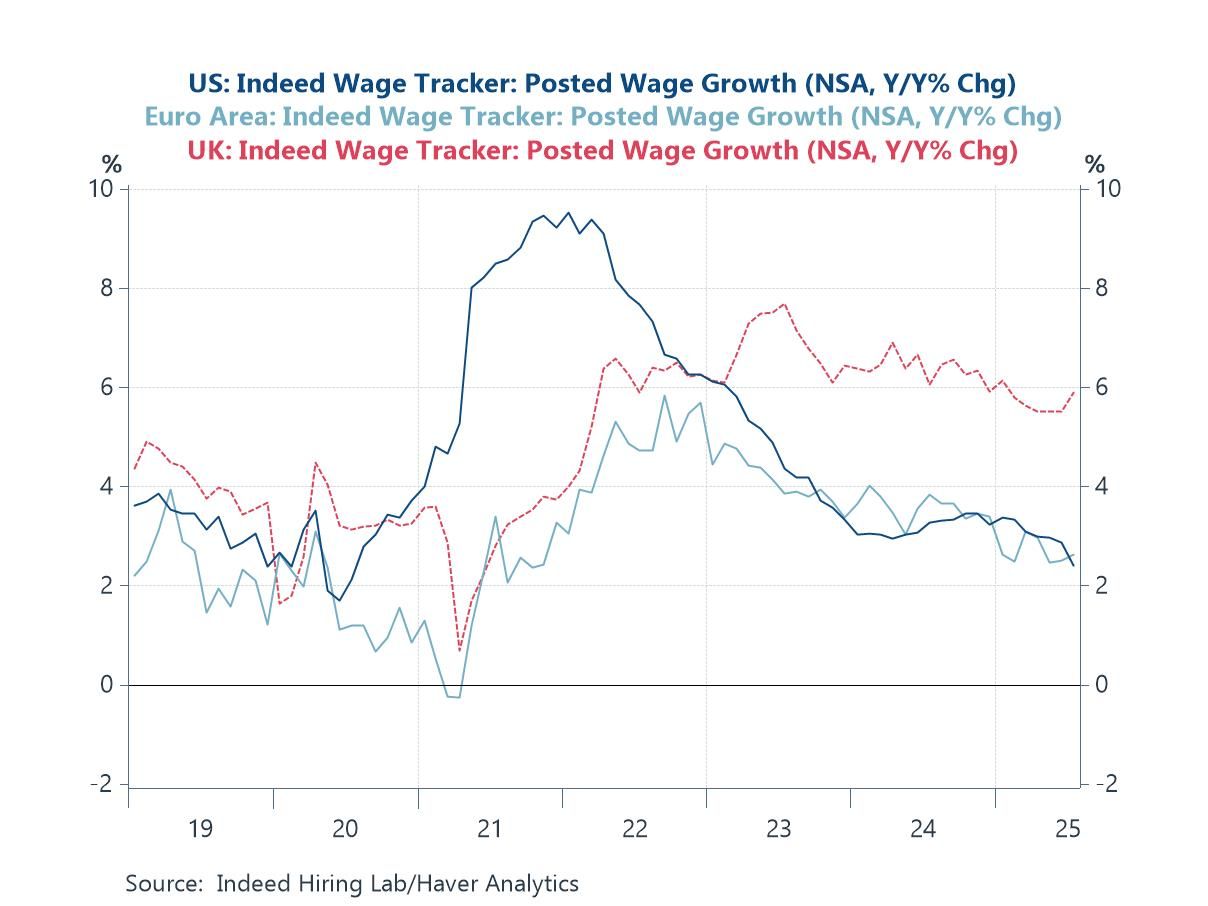

Wage growth in the US and Europe Turning back to inflation dynamics, the UK stands out for its persistent wage pressures. While posted wage growth has cooled across the US and euro area, the UK measure has remained elevated at around 6% year-on-year, well above pre-pandemic norms. This stickiness reflects a still-tight labour market in key service sectors, even as broader activity has slowed and unemployment has edged higher. For the Bank of England, it underscores the dilemma: headline inflation is easing, but underlying pay growth risks keeping services inflation uncomfortably high, complicating the timing and scale of policy easing.

Chart 5: The Indeed Wage Tracker for the US, euro area and UK

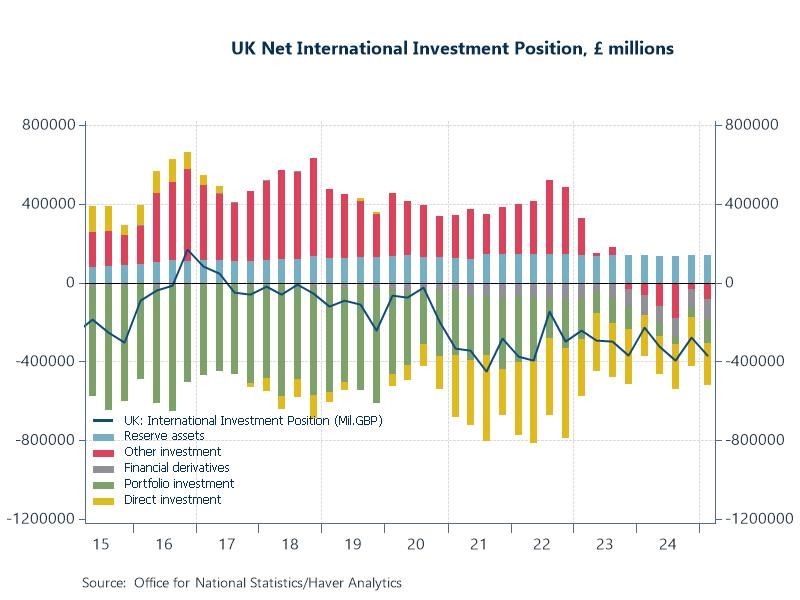

The UK economy The UK’s net international investment position has deteriorated noticeably in recent years, with both direct investment and portfolio flows showing persistent weakness. The latest data underline how net FDI has turned increasingly negative, while the portfolio investment balance has also eroded, leaving the UK more reliant on volatile short-term funding sources. This deterioration comes against a backdrop of heightened investor unease about the riskiness of UK debt markets, where elevated gilt yields and rising debt-servicing costs have amplified concerns over fiscal sustainability. Taken together, these trends underscore the vulnerability of the UK’s external position at a time when global capital is arguably proving more selective and risk sensitive.

Chart 6: The UK net international investment position

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

More Economy in Brief