EMU Large Country Inflation Runs Cold – Over Tepid Cores

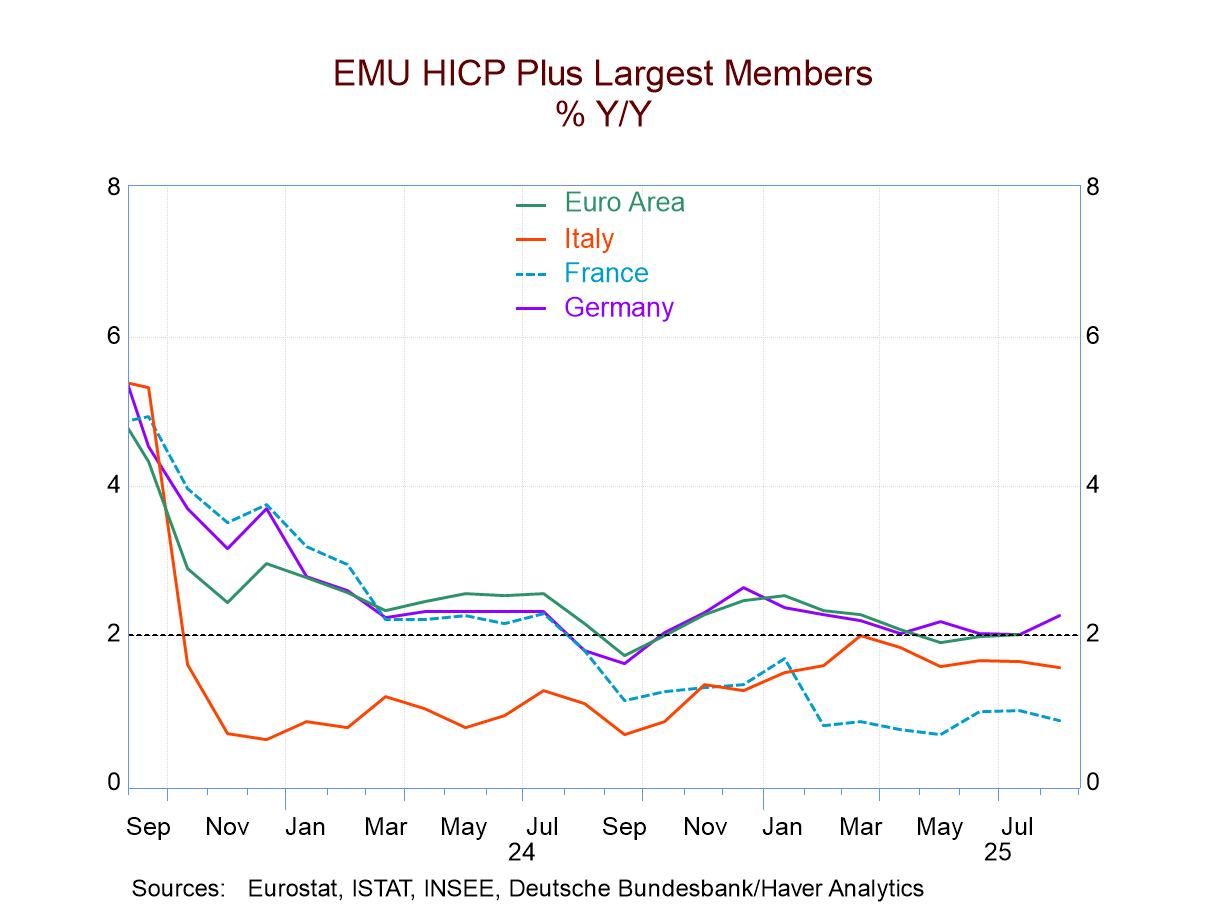

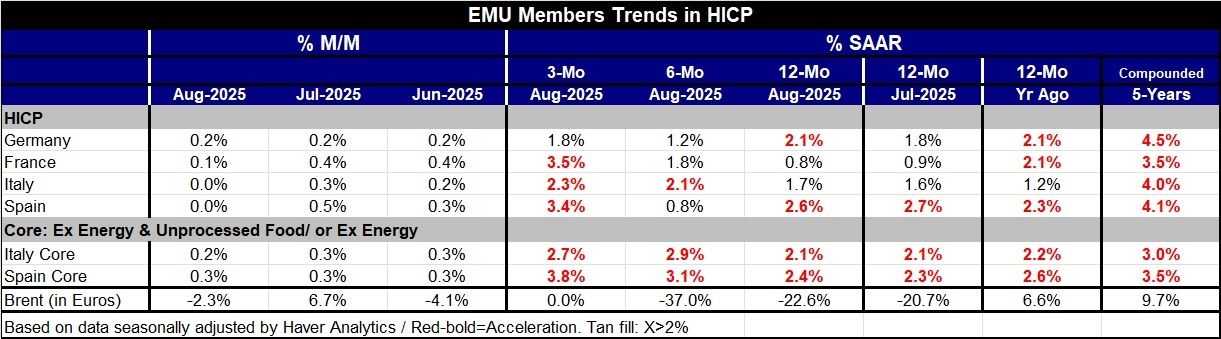

Inflation in the monetary union was tepid across the large, early-reporting, economies in August. The HICP rose by 0.2% on the month in Germany, rose by 0.1% in France, while it was flat in both Italy and Spain. However, these outstanding readings followed several months of stronger inflation; in particular in July German prices rose by 0.2%, in Italy the gauge rose by 0.3%, in France by 0.4%, and in Spain by 0.5%.

As a result, over three months, inflation is running hot on the headline gauge, over 2% in France, Italy, and Spain, and just below it, at a 1.8% annual rate in Germany. Over 12 months, inflation is well behaved, but that headline is up 0.8% in France, rises by 1.7% over 12 months in Italy, by 2.1% in Germany, and at a 2.6% pace in Spain. That is a bit more mixed but still quite solid set of results. The EMU-wide HICP for July – on a one-month lag- rises by 2.1% over 12 months with a core at 2.3%.

Core inflation is not well reported on an early basis. The Italian core rate rose 0.2% in August with Spain at 0.3%; both Italy and Spain logged increases of 0.3% in July and in June and as a result the 3-month inflation rate on the core for Italy and Spain runs at 2.7% in Italy and at 3.8% for Spain. These, of course, are much higher and more disturbing numbers for inflation. The 6-month inflation rate for core Italy and Spain runs at 2.9% and 3.1%, respectively, while over 12 months the Italian core is up by only 2.1% and the Spanish core is up by only 2.4%. The kick up and inflation for the core is a relatively recent phenomenon.

These statistics give the ECB some room and some time to maneuver, since headline inflation is in pretty good shape and the inflation issues are scattered and have emerged more recently from the core and with growth still weak and with rising unemployment in Germany where it just topped 3 million for the first time in a decade. There may not be any impetus to have to raise rates to cool inflation. The European Central Bank, like the Federal Reserve, is likely playing a watch and wait game with the economic statistics, and this month the watch and wait game turned pretty much in its favor with very good headline figures although still having some difficult core figures. It will take a little time before we get the core numbers for the rest of the monetary union members to fill in to understand exactly where those trends sit.

However, based on the early returns, the ECB is probably relatively happy with how inflation is sitting even with the core rates slightly excessive and varied. There doesn't appear to be any burgeoning inflation problem; there's some kind of a modest core inflation issue building in Italy and Spain and we'll have to watch that in the coming months. For now, the ECB should be relatively content.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global