Global| Dec 01 2025

Global| Dec 01 2025S&P MFG PMIs Remain Mixed

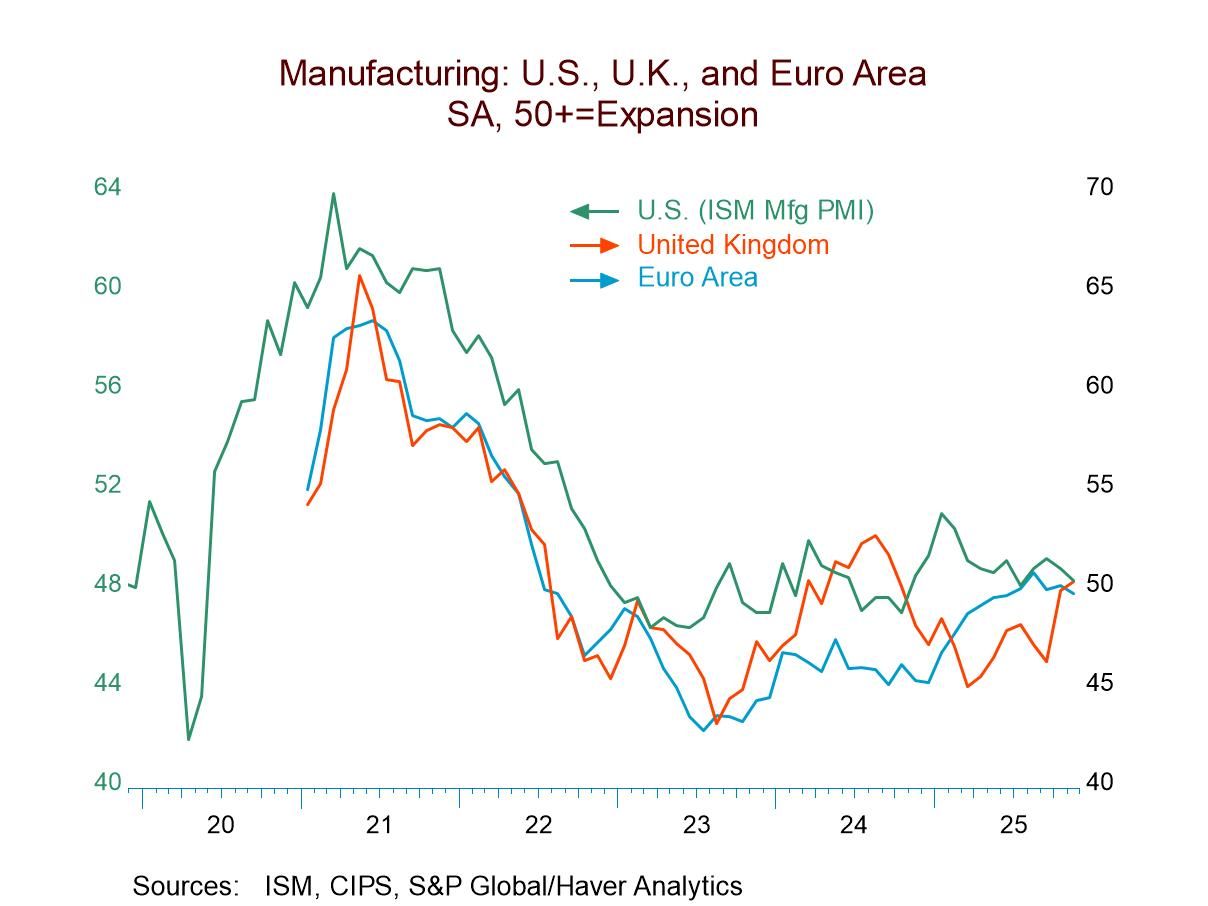

The S&P manufacturing PMIs for November show split results with 9 reporters showing improvement and 9 reporters showing deterioration. The median value among reporters in November is 49.0, exactly the same as its the three-month average, but it's a downtick from 49.5 in October. The split in terms of improving or deteriorating is 50/50 in November and that compares to 61.1% improving versus about 39% deteriorating in October. Both of these diffusion readings are a tremendous step up from September when only 11% of the reporters improved month-to-month.

Sequentially, there's hardly any change at all and none worth speaking about. All of the values for three-months, six-months, and 12-months are either 49.0 or 49.1. Now compared to 12 months ago shows a diffusion of 55.6, indicating relatively more improvement than deterioration. For six-months versus 12-months, diffusion is at 66.7, indicating about 2/3 are improving and only one-third deteriorating. However, over three-months compared to six-months, the split on diffusion is at 50%, a wholly neutral value.

The queue standings that rank the November observations on data back to January 2021 show above 50% readings for eight of the 18 reporters in the table. Above their 50% mark (which means above their medians) are the euro area, Germany, the United States, the United Kingdom, India, Indonesia, Malaysia, and Vietnam. The global manufacturing results from the JP Morgan index which employs weighting is much higher at 68.4 percentile and compares to an unweighted Asian average of 54.7%, and the total average at 45.8%. Neither of the two average statistics employ weighting.

Assessing the change in manufacturing from January 2021 across the 18 reporters, only four have manufacturing indexes that are higher than they were at that time; those reporters are Mexico, Indonesia, Malaysia, and Vietnam.

On balance, there is some improvement. The JP Morgan indexes provide us with some of the most upbeat results but even the JP Morgan responses, the three-month, six-month, and 12-months PMI weighted averages show diffusion values between 50 and 51. The last three months are without much trend and with reading also between 50 and 51.

The bottom line is really that the manufacturing sector continues to move more or less sideways with manufacturing relatively stagnant oscillating between slightly growing and slightly contracting. There's no strong sense of momentum in either direction and even the breath statistics tend to run hot and then cold, obscuring any true underlying signal. The manufacturing sector globally continues to essentially stumble in the dark.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief