- Consumer credit strength exceeds expectations.

- Both nonrevolving and revolving credit move notably higher.

USA| Jun 06 2025

USA| Jun 06 2025U.S. Consumer Credit Surges in April

by:Tom Moeller

|in:Economy in Brief

Germany| Jun 06 2025

Germany| Jun 06 2025German IP Slips

German industrial production (headline series including construction) fell by 1.4% month-to-month in April as a recent see-saw pattern of monthly increases vs. declines is in train back to October. Output declines in the month were distributed across consumer goods, capital goods and intermediate goods.

In addition, construction output fell in April, dropping by 1.5% month-to-month after rising in March and declining in February.

Manufacturing output fell by 1.8% month-to-month in April as real sales also fell by 1.5%, and as real orders for manufactured goods rose in the month by 0.6%.

Sequential trends The sequential trends for IP and its various sectors as well as for orders show unclear trends. Capital goods and intermediate goods show improving trends (from 12-months to 6-months, to 3-months) as output transitions from declines over longer periods to increases over the recent shorter periods. Manufacturing joins that sequence as it also shows a transition from a period of declining output to increases in recent periods. But construction trends remain erratic and the trend for real orders is also chaotic, although it is topped up by a very strong gain over three months. Real sales are on board for the transitional move from declines to sales increases over recent periods. While there is some degree of mixed trends in the data, there are also some traces of an ongoing recovery with improvement in progress. It is still nascent, but the improvement is identifiable and easily recognizable.

Surveys Manufacturing surveys from ZEW, the IFO, and the EU Commission are mixed in their message. The ZEW survey shows a sharp improvement month-to-month. The IFO shows weakening for manufacturing and for manufacturing expectations. The EU commission index shows an improvement month-to-month. Compared to February levels, these same four readings show contrary results. Their sequential signals remain mixed, both in terms of their lack of monotonic signaling as well as in terms of the simpler comparison of the 12-month readings to the 3-month readings. There is simply no clear signal on direction here.

Other Europe Portugal and Norway offer two separate Northern- and South-European signals; both show strongly improving sequential trends. Their month’s performance remains chaotic, but their sequential performance is upward and a clear positive signal.

QTD Quarter-to-date signals (QTD) show mixed results for output-based measures and for real orders in Germany. But the survey data show improvement QTD and the two European readings for Portugal and Norway show gains in progress as well.

Queue standing The queue standing data that ranked performance over a longer profile show most readings with rankings below the 50% mark which in all cases leaves the current reading below its median for this period (data back to 2000), the exceptions with above 50-percentile readings are consumer goods in Germany (54.6%), real manufacturing orders in Germany (66.7%), and Norway (99.6%).

Summing up Despite the month’s step back, there is still evidence that growth and improvement is stirring or trying to stir. Economic performance often is not monotonic and various factors including weather and other unique and temporary factors can interrupt even a solid trend. There is reason to be hopeful that German data still show progress and with the mandate to do more to defend themselves in NATO is also a spur to output we should expect over the coming months.

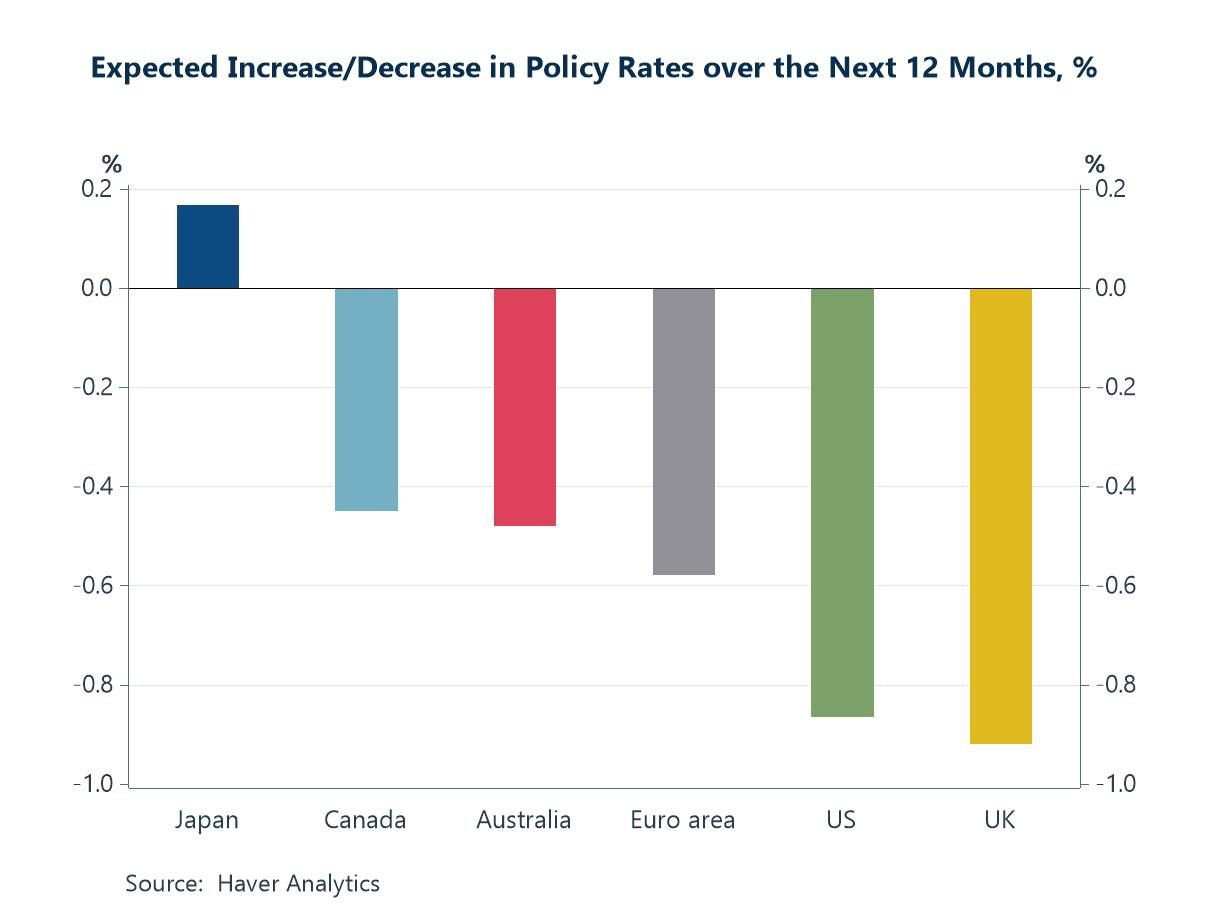

Global| Jun 05 2025

Global| Jun 05 2025Charts of the Week: Fault Lines and Rate Cuts

Recent weeks have seen a complex recalibration in global financial markets, as investors weigh the implications of renewed US tariff actions against accumulating signs of economic softness and growing confidence in the prospect of central bank easing. As part of this recalibration, there has been heightened, if not uniformly sustained, concern about the safe-haven appeal of US assets, with long-dated Treasury yields rising at times on fiscal worries and the US dollar showing episodic vulnerability. Yet despite these concerns, consensus forecasts continue to anticipate meaningful policy rate cuts across most major economies (chart 1). Shorter-dated yields in bond markets have moved in sympathy, with 2-year Treasury yields, for example, have trending lower from mid-May, tracking a deterioration, albeit modest, in the US labour market (chart 2). Lower oil prices and a slew of negative inflation surprises have further softened inflation expectations (chart 3). In the euro area, wage growth and services inflation have also cooled, giving the ECB more latitude to reduce its policy rates again this week (chart 4). The growth backdrop, in the meantime, remains fragile, with global export demand and new manufacturing orders softening, and increasingly exposed to a drag from protectionist US trade policy (chart 5). Finally, China’s entrenched financial imbalances — persistent private sector surpluses, fiscal deficits, and external imbalances — remain a key source of domestic fragility and global distortion (chart 6).

by:Andrew Cates

|in:Economy in Brief

USA| Jun 05 2025

USA| Jun 05 2025U.S. Trade Deficit Narrows Sharply in April as Imports Plummet

- Tariff impositions prompt sharp decline in imports.

- Exports surge led by industrial supplies & materials.

- Petroleum product imports weaken as crude oil prices decline.

by:Tom Moeller

|in:Economy in Brief

USA| Jun 05 2025

USA| Jun 05 2025U.S. Nonfarm Labor Productivity for Q1 Revised Weaker

- Productivity fell 1.5% q/q saar in Q1, down from a 0.8% decline in the advance report.

- The previously reported decline in output in Q1 was little changed while hours worked were revised up.

- Compensation remained elevated, reflected in a marked acceleration in unit labor costs.

by:Sandy Batten

|in:Economy in Brief

- But total beneficiaries decreased over prior week.

- The insured unemployment rate eased back to its recent "favored" rate of 1.2%.

Global| Jun 05 2025

Global| Jun 05 2025Composite PMIs Show Some Life- But Still Near Death

The global PMIs for May continue to show a good deal of stability but at relatively weak levels of performance.

There is, in the May report, some difficulty in assessing performance in what always will be a large sample of countries. Here we're looking at 25 countries and each country reports initially 3 values, one for manufacturing, one for services and then a composite reading (a few do only report a composite). In this table, we're looking only at the combined composite reading which as a weighted reading emphasizes the service sector more than the manufacturing sector. Service sectors have come under pressure and at the same time there's been a lot more concern about manufacturing because of tariff policy and because of international sanctions that have been placed on pariah countries particularly Russia for its attack and its ongoing war against Ukraine. There is concern about manufacturing output and trade which is a factor more for goods than for services.

However, it now appears that this long grinding pressure against the goods sector has spilled over into the service sector and that service sectors are behaving much more erratically and performing at lower levels of activity. However, there's a complicated relationship involving goods sectors because U.S. tariff policy that has threatened global trade patterns and possibly the volume of global trade itself. This has also created a situation that has generated leads and lags that may have stimulated manufacturing sectors over the last few months as manufacturers have tried to pump out goods and shove them into countries ahead of expected there are barriers. Tariffs may have provided stimulus.

The initial draconian tariff barriers indicated by the U.S. were largely put into an abeyance, however the U.S. has a more modest 10% tariff in place and more recently a much larger set of tariffs has been imposed on steel and aluminum. I don’t know what ash changed to make U.S. steel a darling of U.S. industry because when I first studied economics back in the 1960s U.S. steel was then a laughingstock of excesses and competitiveness. It may now be the George Floyd poster-boy of U.S. industry.

The United States and China had a certain tariff detente that seemed to be in place; however, it now appears to be challenged. China has been denying access to rare earth exports not just to the U.S. but to European firms as well. This has generated a backlash from the U.S. and a claim that China has not been fairly administering the detente that had been agreed to. In response, China claims that the U.S. was not adhering to policies and among other things pointed to the recent U.S. policy of canceling Chinese student visas to study in the United States. However, in the last day or so, there has been a telephone call between President Trump and Prime Minister Xi and we'll have to see if that leads to any change in these circumstances. Most recently, Donald Trump, who considers himself a skilled negotiator, has said that Xi is a very difficult person to negotiate with. Trump also has run into difficulties with his negotiations with Vladimir Putin who seems to continue to shine on Mr. Trump and then to do none of the things that he promised Trump he would do. So, reality bites.

The comprehensive PMI data show the unweighted average that is just slightly weaker in May than in April; the median is also slightly weaker in May than in April; however, the G7 GDP-weighted reading is higher in May at 51.5 compared to 49.9 in April and the G6 weighting which excludes the U.S. finds an improvement to 49.2 in May compared to 48.9 in April. On a GDP-weighted basis, there does appear to be some progress that might be occurring, but overall based on the unweighted averages and looking at various groupings of countries there still seem to be severe challenges based on the assessments of the PMI.

In addition, the rankings that are presented show that very few of these 25 reporting countries have current readings that are above their medians of the last 4 1/2 years. Only 6 of 25 countries show current ratings that are above their historic medians; among those, Italy is the only large-economy country that's above its median.

The chart plotted for this presentation shows a great deal of confusion in terms of where these various aggregated sector trends are going. The services and the composite indexes are still clearly trending lower, setting aside their particular movements in the last couple of months. Manufacturing that has weaker readings overall, show some life, but some of this may be generated by the leads-and-lags of the tariff process.

Manufacturing may be turning higher on the need for Europe to provide more of its own defense. This requirement should stimulate the manufacturing sector in Europe in the months and years ahead as the U.S. is going to be relying on Europe to provide more of its own security. However, over the long run, spending more money on military goods doesn't seem to be a good way to improve global welfare. We have benefited in recent years from a long period of political stability and demilitarization, but now it looks like that peace dividend is gone and at least there will be some increase in output from the goods sector as a result. But it's hard to paint that overall as a good development.

- Total index nears one-year low.

- Business activity & new orders weaken. Employment & supplier deliveries improve.

- Price index approaches late-2022 high.

by:Tom Moeller

|in:Economy in Brief

- of10Go to 8 page