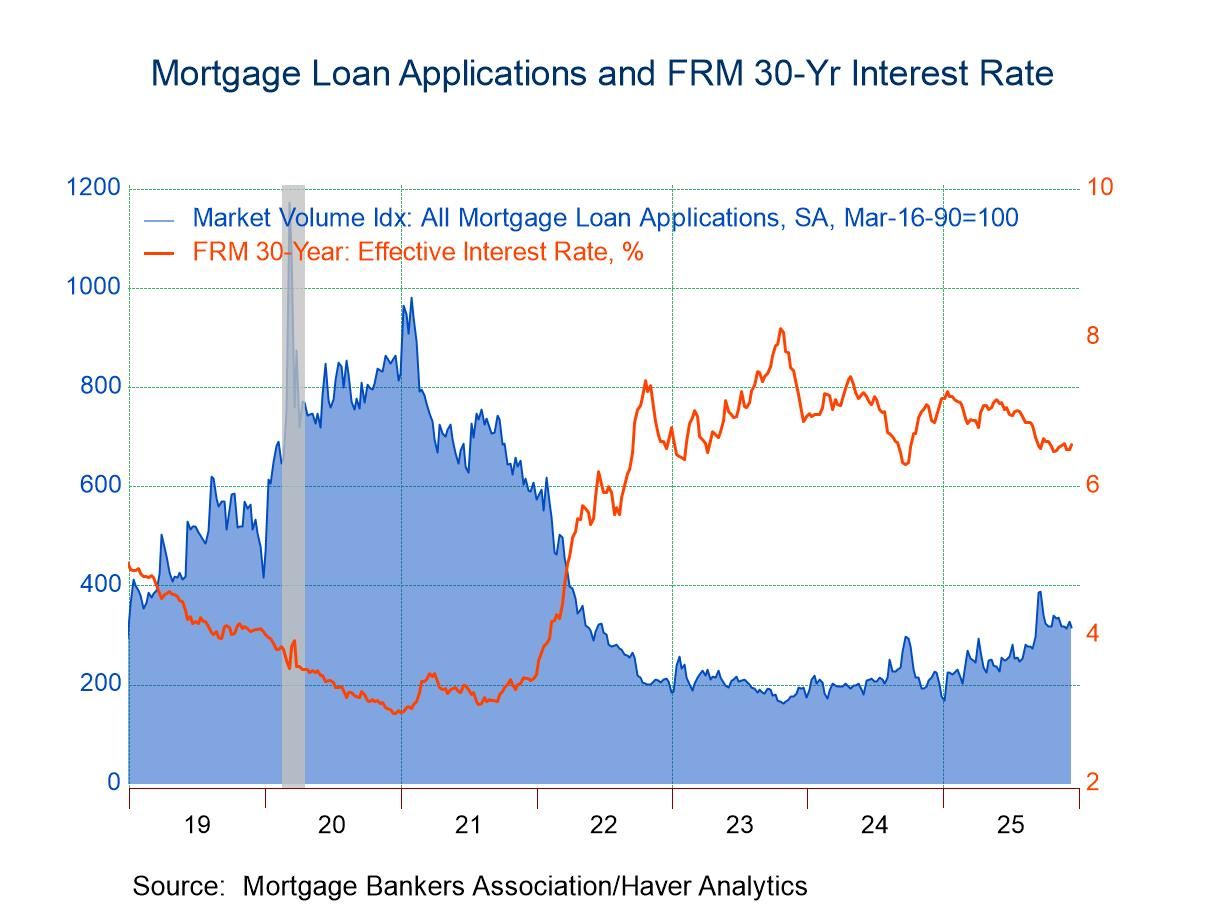

- Purchase applications fell 2.8% w/w; refinancing loan applications fell 3.6% w/w.

- Effective interest rate on 30-year fixed loans rose to 6.56%.

- Average loan size rose moderately.

USA| Dec 17 2025

USA| Dec 17 2025U.S. Mortgage Applications Retreated in the Week of December 12

United Kingdom| Dec 17 2025

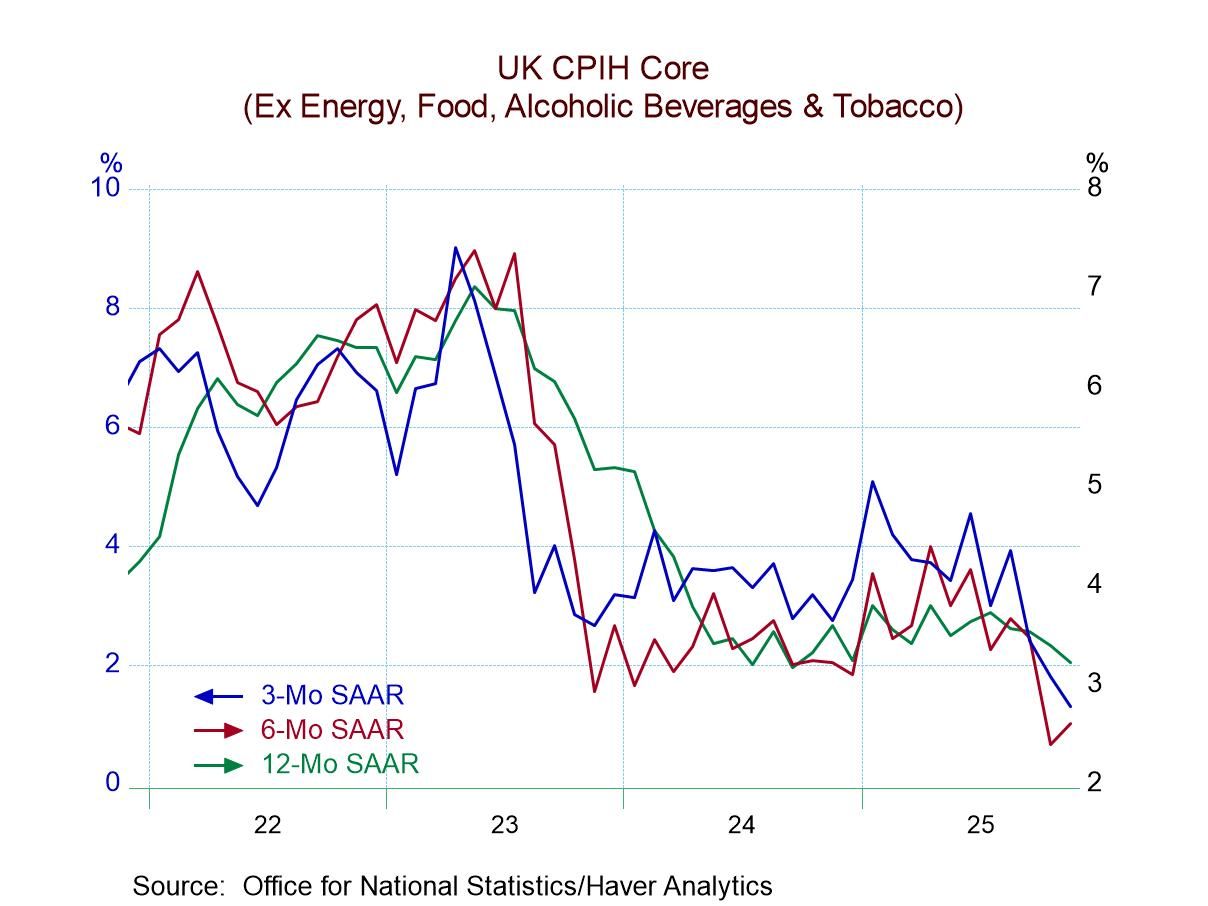

United Kingdom| Dec 17 2025U.K. Inflation Moderates Open Door for BOE Rate Cut

U.K. inflation has moderated in November, posting a 0.1% drop on the HICP, a 0.1% gain in the CPI-H headline measure as well as a 0.1% gain in the CPI-H core (excluding energy, food, alcohol, and tobacco). The sequential trend in core inflation points lower and is eroding but continues to run over the 2% mark set as a target by the Bank of England for overall inflation (over 12 months). The headline is excessive as well but also eroding.

Sequentially the CPI-H gains 3.5% over 12 months, slows to a 2.8% annual rate over six months and then dips to 1.4% annual rate over three months. The CPI-H core rises by 3.6% over 12 months, ticks down to a 3.0% pace over six months, and then runs at a 2.4% annualized pace over three months.

The trend for the CPI core, and for the headline, both are quite good and would be completely consistent with the Bank of England cutting rates, a move that is widely expected – although the 12-month pace for each is excessive.

Not only is inflation showing signs of falling into the Bank of England's target zone, but the economy has been weak although the unemployment rate currently is only hovering around the 4% mark. Still, recent economic data have been weak, and the recent monthly GDP report posted a negative reading, further unsettling the outlook. The October monthly GDP change was estimated at -0.1% while the year-over-year increase in GDP in October produced a gain of just 1.1%. These metrics have put the U.K. economy on recession watch at a time when there has been a sharp revision in the budget process that will be much more constrictive. A sharp pullback in the manufacturing of motor vehicles is blamed for the sudden weakness in GDP in October. The three-month drop in GDP is the first such drop since December 2023.

Meanwhile, the headline and the core inflation statistics are progressing. The table calculates breadth statistics on how widespread inflation acceleration has been and we see that it has not been prevalent (over 50%) in September or November, although breadth did touch the 58% mark in October. Sequentially, inflation acceleration has been tamed: over 12 months (when it is neutral), six months, and three months. Over 12 months, inflation accelerated in only 50% of the categories. And inflation according to the CPI headline and in the core over six months continues to show deceleration to accompany narrowing breadth - only 8.3%. That reading indicates that there was more inflation deceleration than acceleration by a wide margin over six months. At 50%, inflation acceleration and deceleration forces are balanced. Readings below 50% indicate relatively more deceleration, and that is now the more common condition. Inflation acceleration is extremely rare across categories over six months and three months.

USA| Dec 16 2025

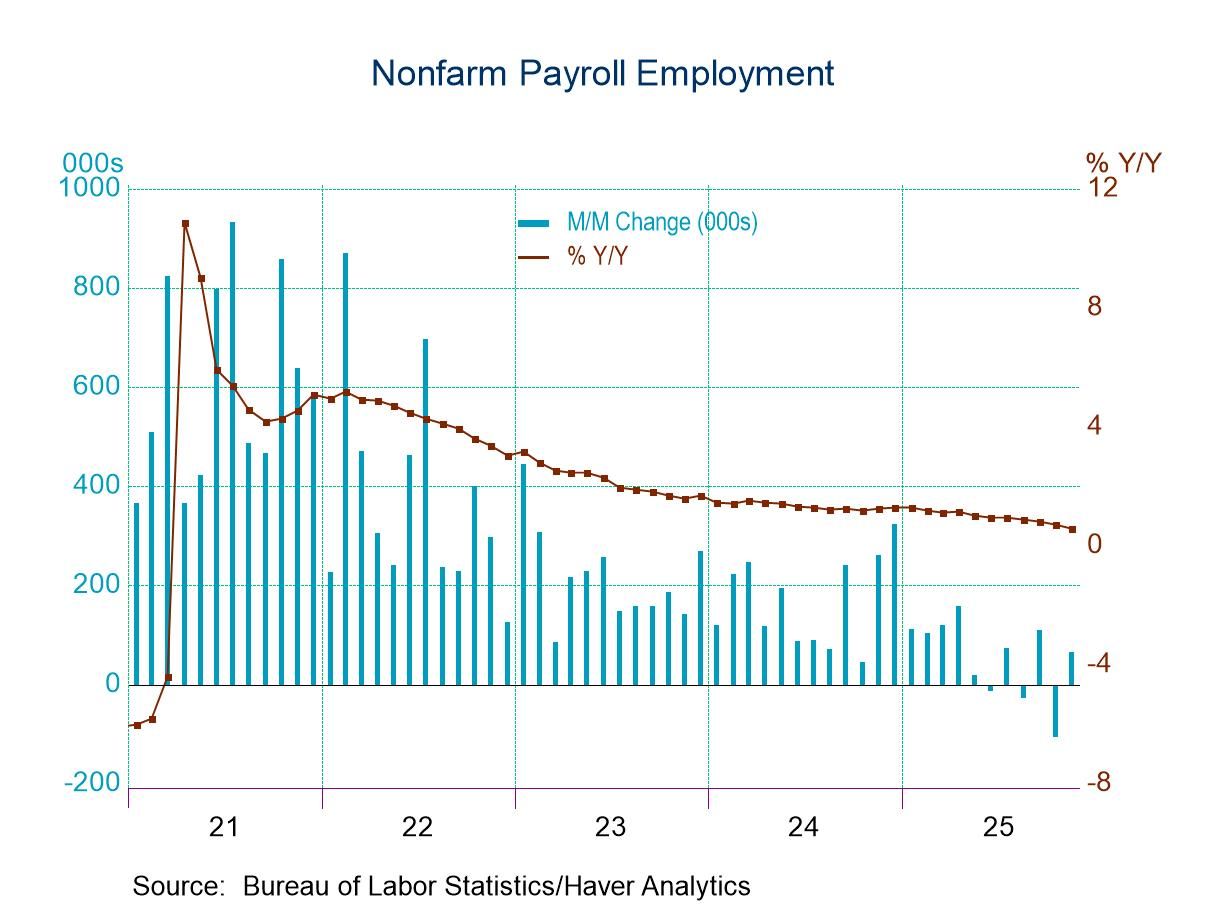

USA| Dec 16 2025U.S. Employment and the Unemployment Rate Rose in November

- Total payrolls rose 64k in November but fell 105k in October

- The October decline was more than accounted for by a 157k decline in government employment

- The unemployment rate jumped to 4.6% in November from 4.4% in September.

- There were no household survey data collected for October.

by:Sandy Batten

|in:Economy in Brief

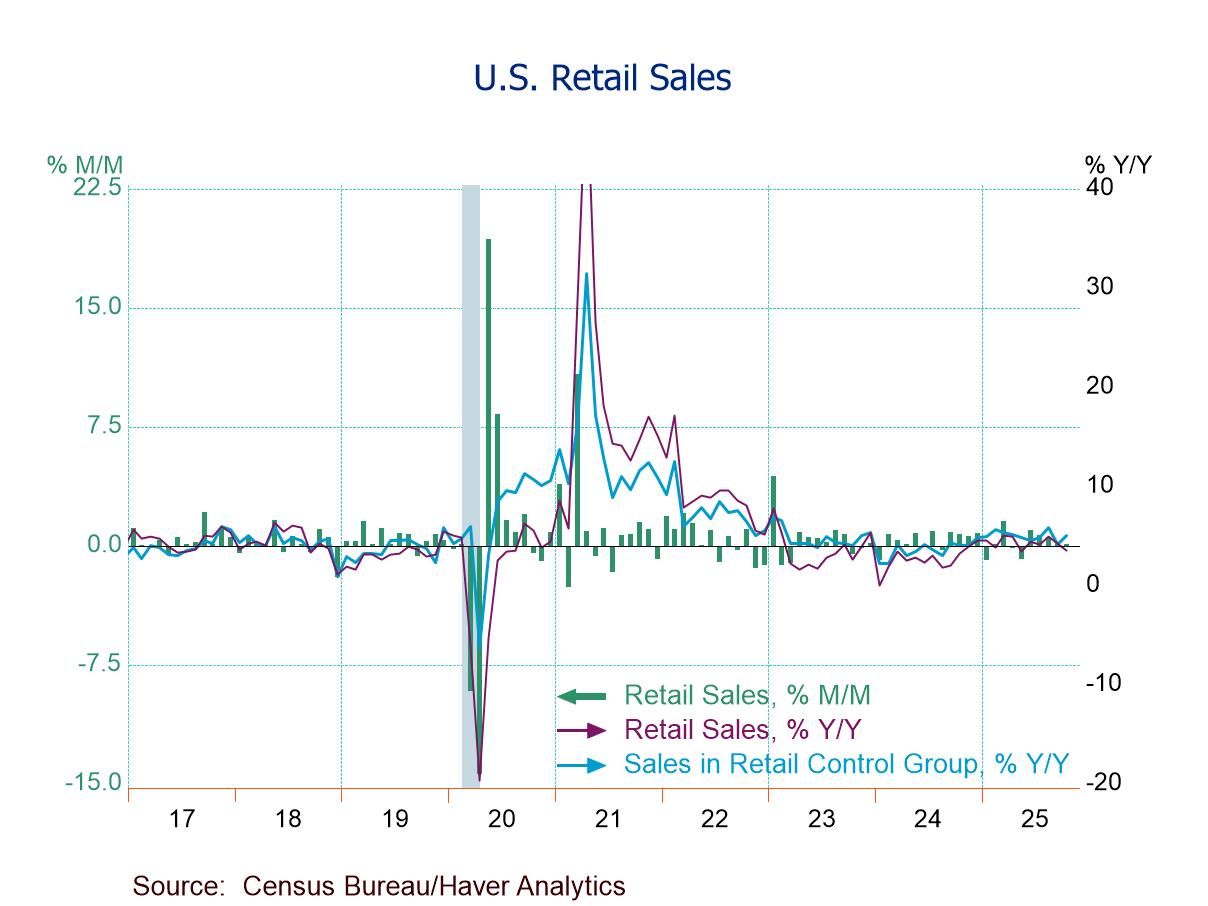

- October total retail sales +0.03% (+3.5% y/y), w/ mixed results across categories.

- Ex-auto sales +0.4% (+4.0% y/y); auto sales -1.6% (+1.2% y/y).

- Sales rebound m/m in department stores (+4.9%) and furniture stores (+2.3%).

- Sales drop m/m in bldg. materials & garden equipt. stores (-0.9%) and gasoline stations (-0.8%).

Europe| Dec 16 2025

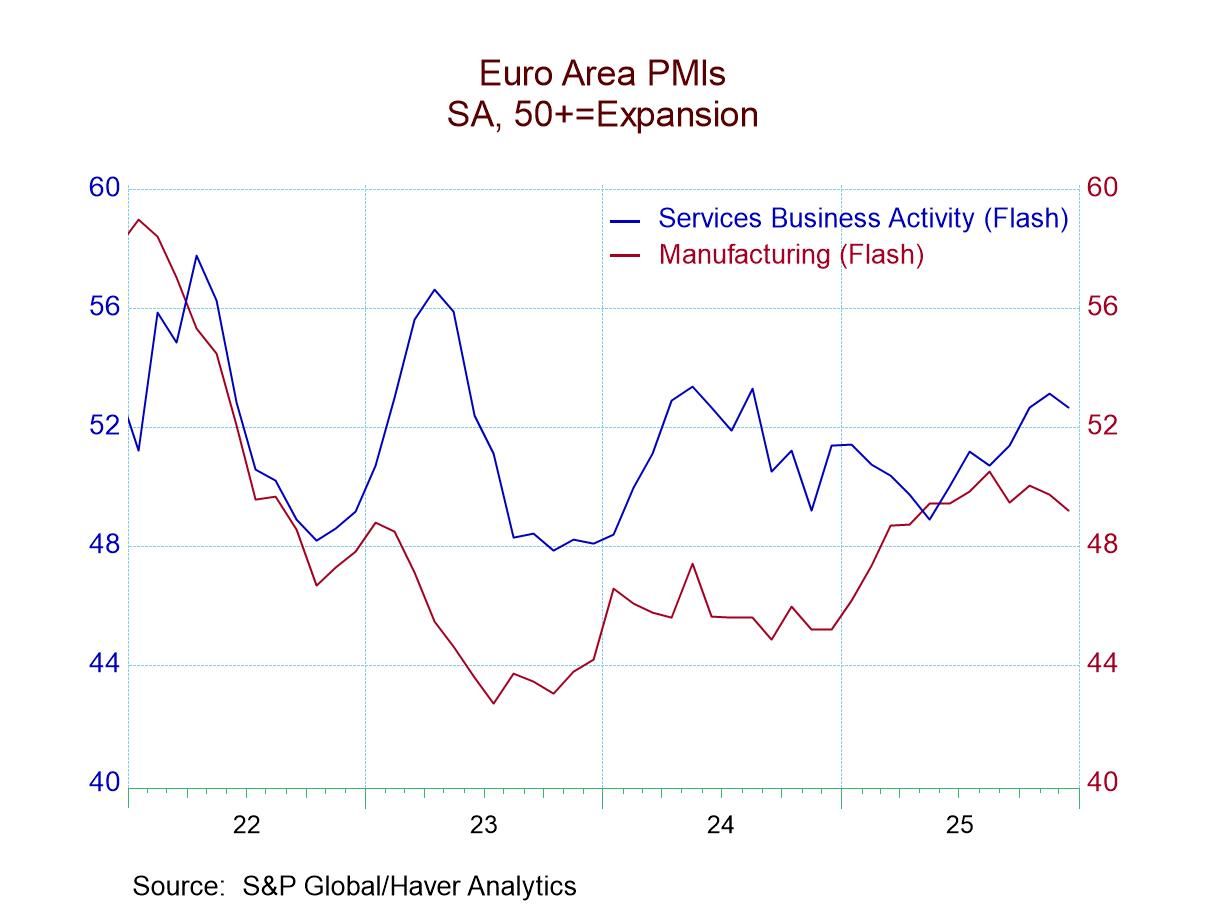

Europe| Dec 16 2025S&P Flash PMIs Weaken in December

The Standard & Poor’s PMI data seem to have taken a fork in the road in December as the previous strong trend toward improving has been reversed in December. Out of 24 sector changes across eight different countries (or economic regions), there are only 6 sectors that show improvement month-to-month in December. This is a sharp contrast to November when 10 sectors showed improvement and to October when 20 of 24 sectors showed improvement. The worm has turned, but is it a lasting turn or not?

The sequential data look at changes in the hard data (that's data through November) over three months, six months, and 12 months. They show a strongly weighted preponderance of sectors that are better, getting stronger, rather than getting weaker. Over three months, 9 of 24 sector readings get weaker compared to six-months. Over six months, every single sector gets stronger compared to 12-months. Over 12 months, 19 sectors get stronger compared to 12-months ago. Monthly data show that this impressive string of improving sectors shows that progress began to slow down in November and kicked into reverse in December.

As of December, the United Kingdom, which is a struggling economy, is the only reporting unit to show a stronger composite, stronger manufacturing, and stronger services. Apart from the U.K.’s strength, there's stronger manufacturing month-to-month reported in France, Japan, and Australia. And that's the end of month-to-month improvements in December. In November, there is a triple improvement in Japan with manufacturing, services, and the composite strengthening month-to-month. There are isolated sector improvements in manufacturing in Australia and in the U.K. There were also improvements for services in India as well as in services and in the composite index for France and in the European monetary union. Still, these are only 10 of 24 sectors in November.

The previous strong trend movement higher has left most of the readings as of December above their medians on data back to January 2021. Among the 24 headline and sector calculations, only six of them show standings below their 50th percentile since January 2021, which puts them below their historic median for that period. The service sector is below the 50% mark in the United Kingdom, Japan, and the United States, while the overall composite is below the 50% mark in the U.S. and in India, with India showing a below median manufacturing rating as well and the U.S. showing below 50% in services. The weaker U.S. data is a new and interesting feature with U.S. job data for November just reported and looking a bit stronger, despite a rise in the unemployment rate. The December S&P survey data, on the other hand, hint that such an improving trend may not last.

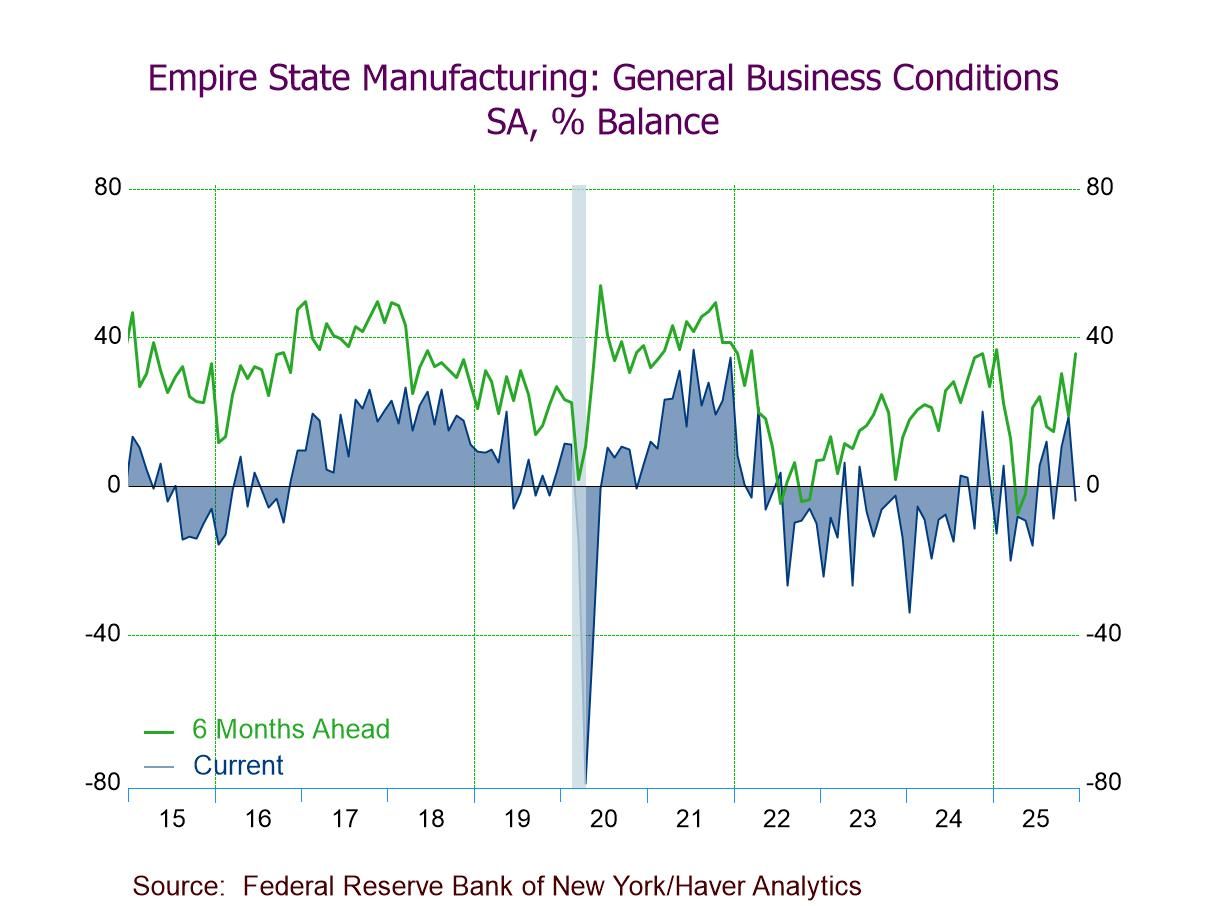

- December General Business Conditions Index down 22.6 pts. to -3.9.

- Unfilled orders (-14.9) and shipments (-5.7) negative; employment (7.3, highest since July) and inventories (4.0) positive; new orders flat (0.0).

- Prices paid at an 11-month-low 37.6 and prices received at a 10-month-low 19.8, still elevated.

- Firms optimistic: Future Business Conditions Index at an 11-month-high 35.7 and future prices paid at an 11-month-low 55.4.

Japan| Dec 15 2025

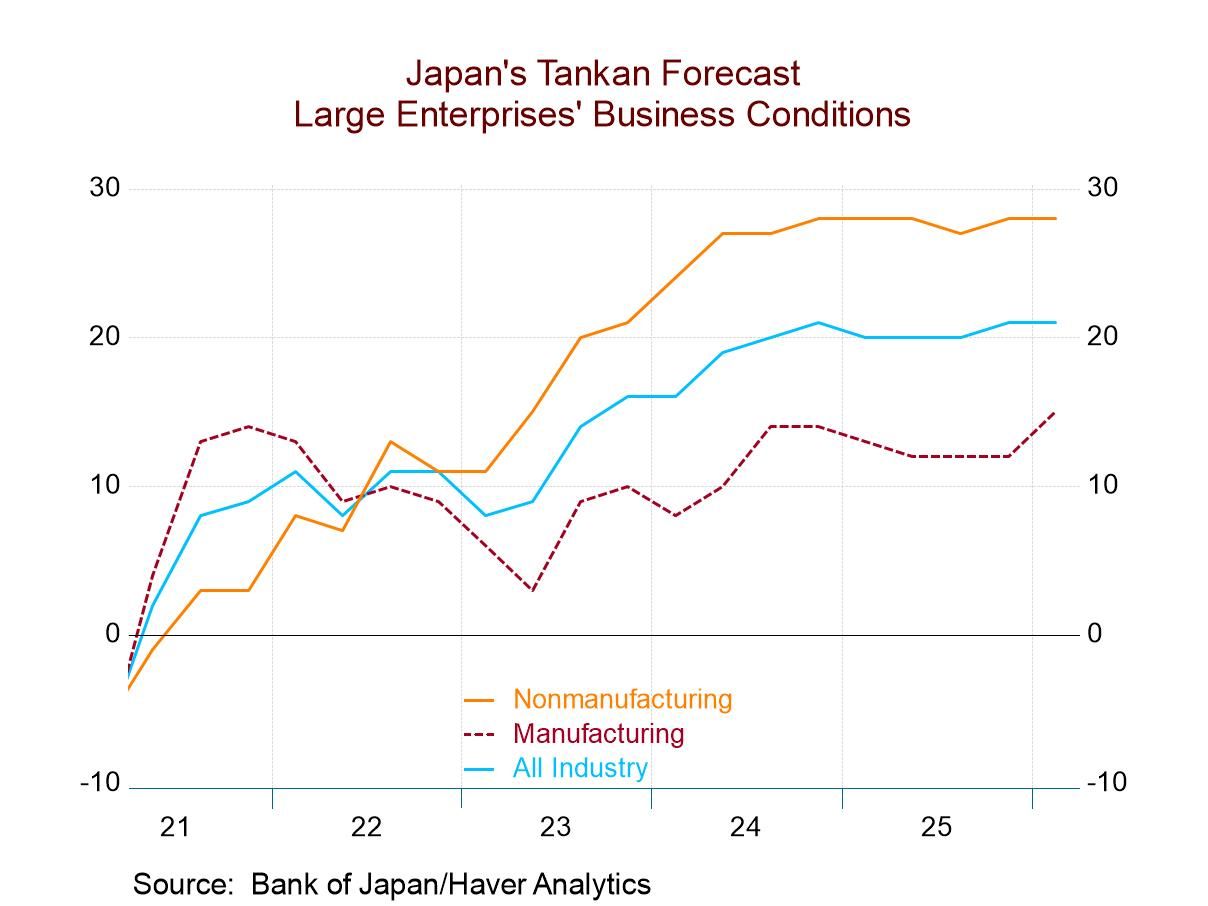

Japan| Dec 15 2025Japan’s Tankan Ticks Higher for Large Manufacturers

Tankan overview: Japan's Tankan report is an important quarterly assessment and outlook of the Japanese economy. Historically, the performance of manufacturers is considered to be the bellwether in this survey for performance of the economy. In the fourth quarter of 2025, the manufacturing index moved up to 15 from 14 in the third quarter. This compares to a value of 12 in the first quarter and a four-quarter average of 13.5. Since late-2006, the manufacturing index has averaged 5.3, marking the performance in 2025 as a substantial improvement from the long period where Japan struggled with deflation. On dated back to 2003, the manufacturing index has a standing in the queue of data in its 70.8 percentile, a reasonably firm reading.

Nonmanufacturers: The index for nonmanufacturers logged a reading of 34 in the fourth quarter compared to 34 in the third quarter and a reading of 35 in the first quarter of 2025; the one-year average for nonmanufacturers is 34.3, marking that sector as little changed over the course of the year. Nonmanufacturing in the fourth quarter has an index standing at its 97.8 percentile, marking it as an extremely high standing on data back to late-2003.

Nonmanufacturing details: Readings across the nonmanufacturing sector are above their respective one-year averages for all subsectors except transportation where the fourth quarter index backs down to 27 from an average of 30.5 and for restaurants & hotels that back down to a reading of 25 from an average of 39.3. The queue percentile standings for the subsectors show a good deal of strength with construction at a 98.9 percentile standing, services for businesses also at a 98.9 percentile standing, transportation - despite the back off from the average - is at a 94.4 percentile standing, and real estate and wholesaling are at 93.3 percentile standings on data back to 2003.

The Tankan outlook- The survey also produces an outlook. For large manufacturers for the first quarter of 2026, the outlook metric moves up to 15 from what had been 12 for the fourth quarter of 2025. The outlook for nonmanufacturers is flat month-to-month at 28, the same as in the fourth quarter. The outlook for manufacturing has a queue standing in its 78.7 percentile on data back to 2003, while nonmanufacturing has a standing for the outlook reading at its 98.9 percentile marking these outlooks as quite good.

The BOJ is watching- This is a survey the Bank of Japan will be looking at and assessing what policy should do and how strong the economy appears to be. On these data, the economy would appear to be firm, the outlook would appear to be solid, and if the Bank of Japan were to decide to pay more attention to inflation, the economy would seem to be in a position to absorb a rate hike without much difficulty.

Other-sized enterprises- Manufacturing: The survey also produces results for medium-sized and small-sized firms, as well as outlooks for medium-sized and small-sized firms (that are not presented in the table). The fourth quarter assessments of performance, however, show improvements for manufacturing in both medium- and small-sized enterprises; they also show rankings of medium-sized firms in manufacturing in their 85th percentile, the same as for small sized enterprises.

Nonmanufacturing: Nonmanufacturing for medium- and small-sized enterprises show improvements in the fourth quarter results and also demonstrates high rankings of those readings for those respective sectors.

Summing up: On balance, it's a solid Tankan report for Japan's economy and should provide reassurance to the Bank of Japan and to the current government that the economy is on solid footing as each looks at the situation and tries to assess the best policy options.

Asia| Dec 15 2025

Asia| Dec 15 2025Economic Letter from Asia: Balancing Risks

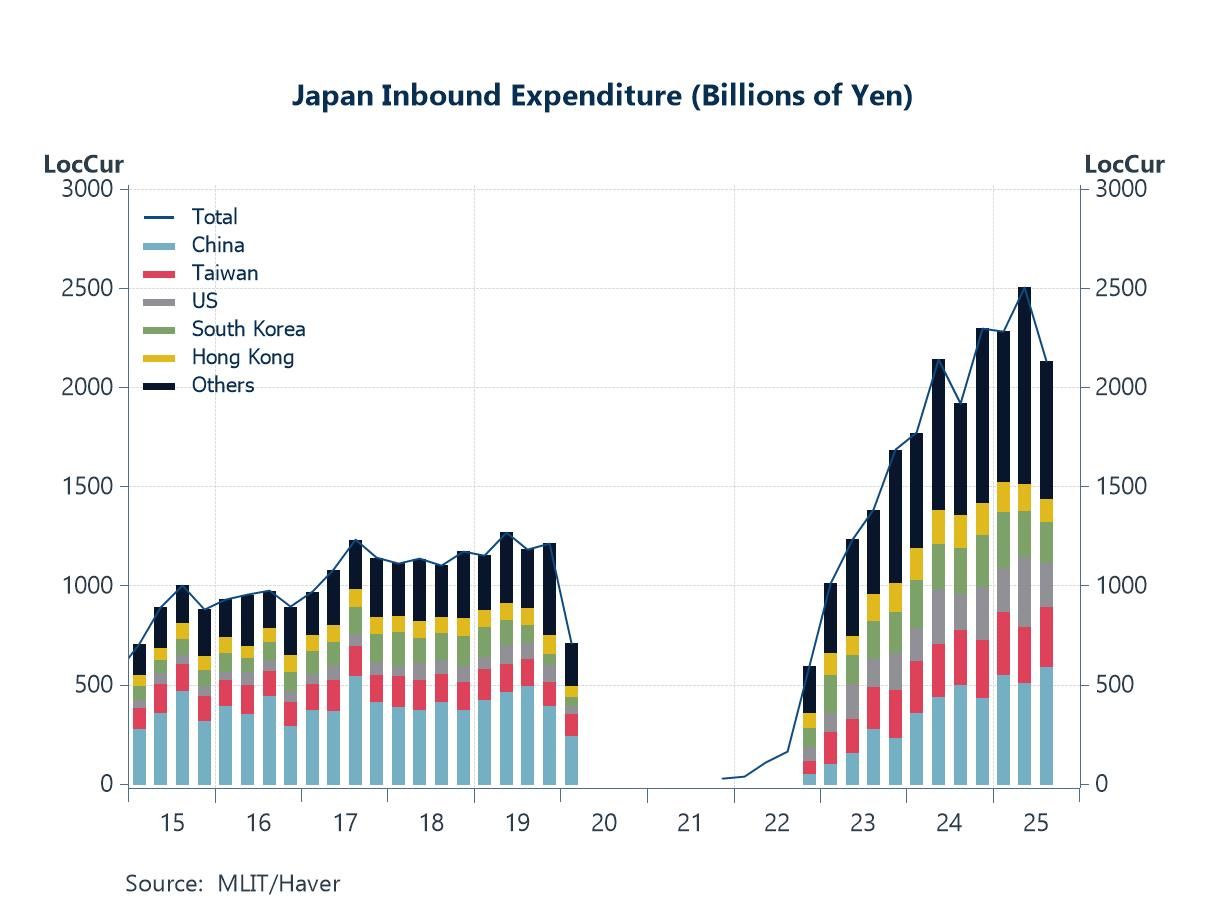

This week, we assess Asia through a risk lens, given the recent flare-ups across the region. Japan–China tensions, following Japanese Prime Minister Takaichi’s recent remarks on Taiwan, have prompted some retaliatory measures from China, including travel advisories against visiting Japan. This raises the risk of a dent to Japan’s tourism income this year, given the significance of aggregate Chinese tourism expenditure (chart 1), although any such impact would come at a time when Japan is already grappling with the effects of overtourism. Beyond Japan–China relations, investors are also bracing for the Bank of Japan’s (BoJ) final scheduled policy decision of the year, where a rate hike is expected despite Takaichi’s pro-growth fiscal stance. This expectation reflects ongoing yen weakness (chart 2), alongside encouraging results from Japan’s Q3 Tankan survey, among other factors. While the anticipated hike is not, in itself, a risk, the associated increase in financing costs—coupled with the likelihood of higher government bond issuance to support growth objectives—adds to investor concerns.

Risks are also evident in China, particularly after the November data docket showed a continued deterioration in growth across multiple sectors (chart 3). While China’s 5% growth target for the year remains within reach, achieving it appears to hinge on a narrow set of growth drivers, notably trade. On this front, China has defied earlier investor concerns to record a substantial widening of its trade surplus this year, despite a worsening bilateral trade balance with the US (chart 4). However, while supportive of growth, this development risks drawing increased pushback from non-US trading partners that have been absorbing China’s excess capacity.

Elevated risks are also present elsewhere in Asia, particularly in Southeast Asia, where renewed military clashes between Thailand and Cambodia have once again pushed bilateral tensions to the fore (chart 5). Thailand additionally faces political uncertainty ahead of early elections, following Prime Minister Anutin’s dissolution of parliament last week. Lastly, we turn to semiconductor- and AI-related risks, which are especially pertinent to Asia given the dominance—and reliance—of Taiwan and South Korea in the sector. A key risk lies in the current extent of market optimism surrounding future AI-related earnings (chart 6), suggesting greater scope for disappointment than for further upside surprises.

Japan-China tensions Geopolitics will likely remain front and centre in Asia heading into the new year, with several flashpoints carrying the risk of broader regional spillovers. One such case is the recent flare-up in tensions between China and Japan, following new Japanese Prime Minister Takaichi’s parliamentary remarks on Taiwan. Since then, Chinese authorities have rolled out a series of measures — urging Chinese citizens to avoid travelling to or studying in Japan, reinstating an import ban on Japanese seafood, among others. While none of these steps are particularly substantial on their own, they underscore a rapidly deteriorating bilateral dynamic. The economic implications are not trivial. As shown in chart 1, spending by Chinese tourists has historically made up a significant share of Japan’s total inbound tourism receipts — roughly a quarter in recent quarters — with especially strong concentrations in certain regions such as Osaka. Although the absence of Mainland Chinese tourists has been keenly felt since tensions escalated, early indications suggest that increased arrivals from other countries have helped offset some of the shortfall. More recently, a series of close military encounters between China and Japan has further heightened concerns. The risk of miscalculation has grown, raising the possibility of an inadvertent escalation at a time when geopolitical sensitivities in the region are already elevated.

- of2725Go to 44 page