- The headline index fell to 44.0, pointing to on-going decline in activity.

- The employment and production subindexes declined 6.0 points.

- Input prices continued to rise at a slow pace.

USA| Feb 29 2024

USA| Feb 29 2024Chicago Business Barometer Falls Again in February

- The index has not been positive since September 2022

- However, the negative reading for February was smaller than in January.

- Shipments and employment picked up, but orders and production were lackluster.

by:Sandy Batten

|in:Economy in Brief

- Initial claims up 13,000; maintain tight range

- Continuing claims also up moderately; 4-week average rises to 26-month high.

- Insured unemployment rate maintains tight 1.2%-1.3% range.

Japan| Feb 29 2024

Japan| Feb 29 2024Japan’s IP Falls Hard in January

Weakness is broad across sectors Japan’s industrial production fell hard in January, dropping 7.4% (month-to-month!) after rising 1.2% in December; the December gain followed a drop of 1.3% in November. Japan's industrial output has been unstable for a number of months: manufacturing production has fallen month-to-month in 11 of the last 16 months. During that span, there was only one episode of industrial production rising month-to-month in consecutive months and one of those two months was an extremely small gain of only 0.1%. The changes in industrial output have been choppy during this span. The last five monthly increases in industrial production averaged a month-to-month rise of 2.6% while the last 11 declines averaged a month-to-month drop of 2.1%. These are extremely volatile numbers, and it makes it very hard to pin down an exact pattern for industrial production except that the preponderance of declines makes it clear that the direction is lower, and the speed is ‘too-fast.’

The table makes it clear that there are declines in industrial production over three months, six months and 12 months for all the categories in the table with one single exception - that is transportation output over 12 months. And the progression is to faster and faster declines with exception of utilities output over the last three months that fell at ‘only’ a 5.6% annual rate while declining at an annual rate of 13.8% of six months.

In the quarter-to-date, industrial production is falling overall in manufacturing and in each category at astonishingly strong paces; even utilities output is falling at a double-digit rate early in the first quarter at a 12% annual rate of decline.

The authorities are giving guidance for some recovery in industrial production ahead although that's not particularly reassuring. After such sharp declines, Japan is really staring in the eye a great deal of weakness.

In addition to that, there's not anything queued up that is boosting industrial production in any obvious way for the road ahead.

- Growth accelerates y/y as domestic final demand growth remains strong.

- Foreign trade & inventory contributions offset one another.

- Halving of Q3 price gain remains in place.

by:Tom Moeller

|in:Economy in Brief

USA| Feb 28 2024

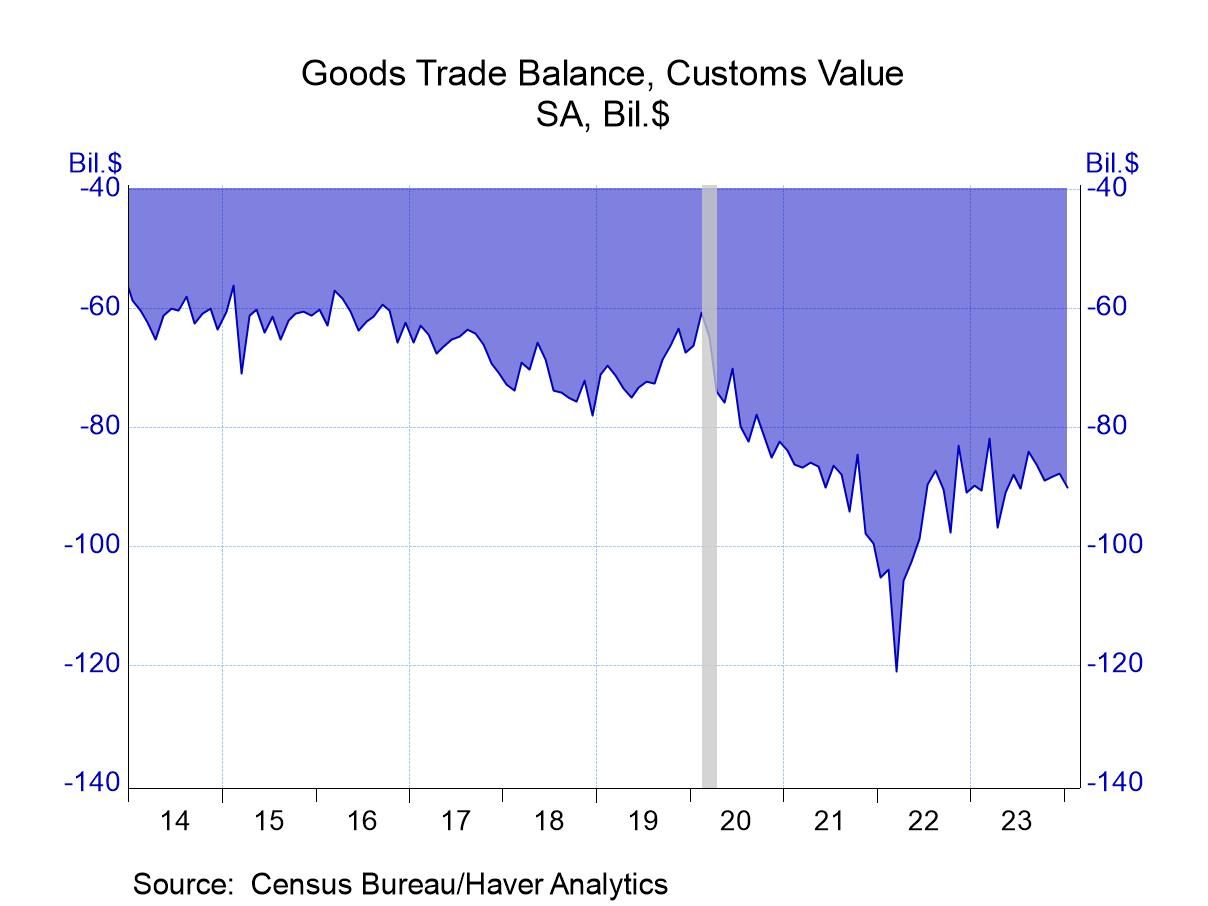

USA| Feb 28 2024U.S. Foreign Goods Trade Deficit Widens Slightly in January

- $90.2 billion deficit modestly wider than expected.

- Exports rise 0.2%, led by shipments of automotive goods.

- Imports increase 1.1%, with autos and associated goods up 5.1%.

USA| Feb 28 2024

USA| Feb 28 2024U.S. Mortgage Applications Fell Again in the Latest Week

- Mortgage loan applications decline for third consecutive week.

- Purchase loan applications decline for fifth consecutive week.

- 30-year fixed-rate mortgage eased only slightly in the last week.

Europe| Feb 28 2024

Europe| Feb 28 2024EU Index Erodes; Germany Lags; Questions Are Raised...

In February, the European Commission economic sentiment index from the monetary union declined to 95.4 from January’s 96.1, a surprise development. This drops the reading below even its December level but above its November level. Declines are logged in three of five sectors with the industrial sector, the retail sector, and the services sector, each weakening month-to-month. The construction assessment was unchanged between January and February while consumer confidence increased to a -15.5 reading in February from -16.1 in January.

- of2727Go to 239 page