- Index recovers January’s decline.

- Three-month average surges.

- Half of components rise.

USA| Mar 24 2025

USA| Mar 24 2025Chicago Fed National Activity Index Rebounds in February

by:Tom Moeller

|in:Economy in Brief

Global| Mar 24 2025

Global| Mar 24 2025S&P Flash PMIs-Services Worse, Manufacturing Better

S&P flash PMI statistics for March show very little change in the composite which has been plugging along at 51.4 in January, 51.4 in February and now 51.5 in March. These are readings from unweighted averages from the eight reporting countries and the European Monetary Union. The manufacturing composite is crawling its way higher from 49.1 in January to 49.5 in February to 49.9 in March, putting manufacturing nearly to a breakeven reading after a long period of showing sector contraction. Service sector readings monthly log 52.0 in January, 51.9 in February and 51.6 in March, a steady but very minor trend to erosion.

The sequential growth rates on the quarterly average readings that exclude March are performed only on hard data. They show that the composite reading has also been very stable at 51.6 for the 12-month average, 51.3 over 6 months and 51.3 over the most recent hard 3 months’ worth of data. Manufacturing has also been stagnant with a reading of 48.4 for the 12-month average, 48.4 for the six-month average and 48.6 for the three-month average for the period ended in February. Services show the same minor slippage we see in the monthly data from 52.5 over 12 months to 52.2 over 6 months, to 52.0 over the most recent three-months of hard data. These trends show minor improvement in manufacturing and minor deterioration in services. Manufacturing continues to show minor contraction as services continue to show minor expansion. Neither sector performs particularly well and neither sector has any particularly notable trend to it. The diffusion data across countries show a great deal of variation.

Asia| Mar 24 2025

Asia| Mar 24 2025Economic Letter from Asia: Reciprocity

This week, we explore the growing impact of recent US policy moves—particularly President Trump’s “reciprocal” tariffs scheduled for April 2—with a spotlight on their implications for Asia. The effects of China’s retaliation to the US’s first round of 10% tariffs are already visible in the data (Chart 1). Similarly, in South Korea, the Biden administration’s tightening of chip export restrictions has likely contributed to a slump in the economy’s recent semiconductor exports to China (Chart 2). Despite these challenges, investor concerns about Trump’s upcoming "reciprocal" tariffs have been eased by reports suggesting they may not be a blanket measure, with certain economies potentially exempt. While the potential impact of these tariffs on Asia may initially seem significant, the effects are likely to be concentrated in a few economies, particularly India. This is mainly because, India still maintains one of the highest average tariff rates in the world (charts 3 and 4), despite progress in reducing tariffs over the years (Chart 5). In contrast, South Korea, though it has a relatively high average tariff rate, benefits from a very low effective tariff rate on US imports (Chart 6), thanks to its bilateral trade agreement with the US.

Tariff effects on China Earlier, China responded to the US’s first round of 10% tariffs on Chinese imports by placing tariffs on certain energy products and large-engine cars from the US. The effects of these tariffs are already evident in the data, as shown in chart 1. Specifically, China’s imports of US cars have continued to decline sharply, and its imports of certain energy-related products have also decreased through the year so far. However, China’s overall imports from the US have increased on a year-over-year basis. Looking ahead, investors are likely focused on the impact of China’s second round of retaliatory tariffs, which mainly target US agricultural goods.

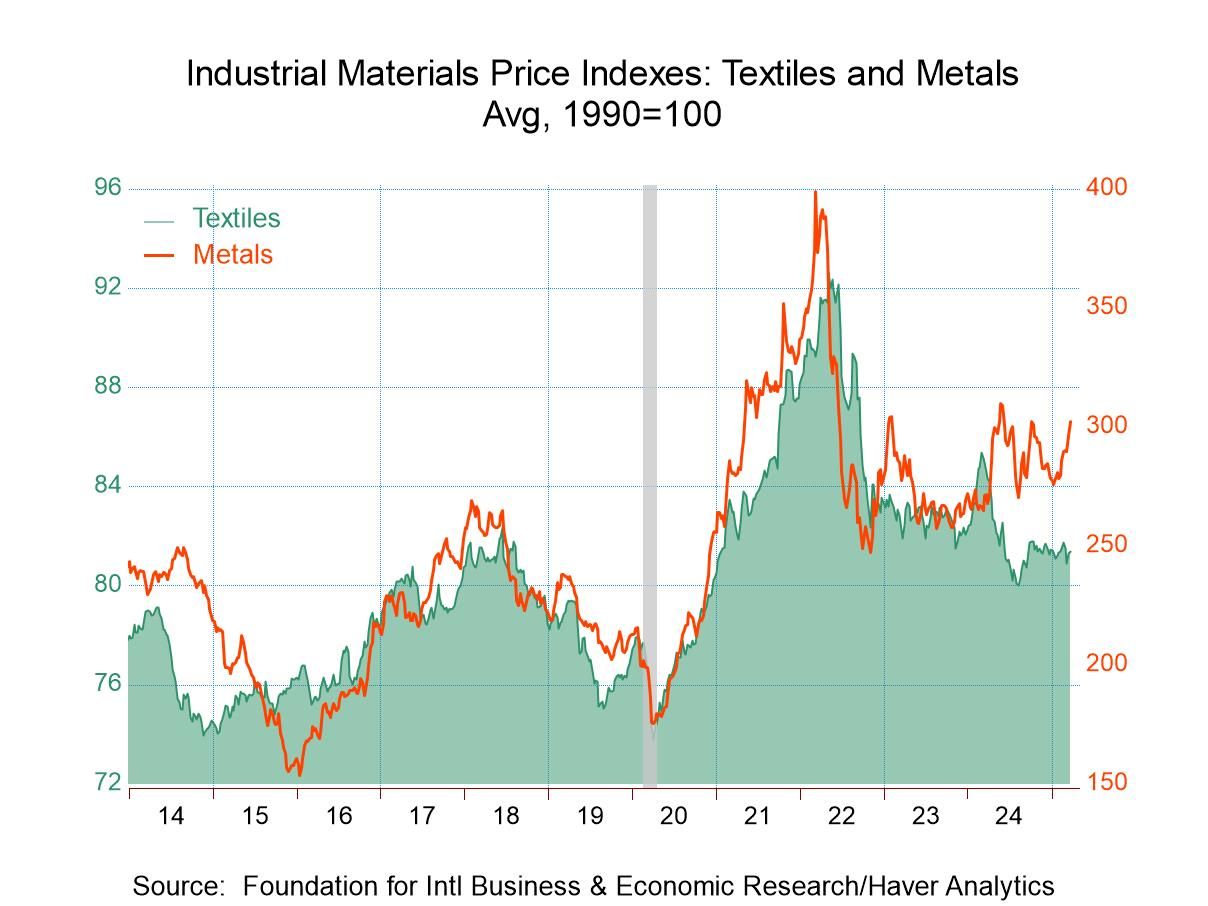

- Metals prices surge.

- Lumber prices strengthen.

- Crude oil costs decline.

by:Tom Moeller

|in:Economy in Brief

France| Mar 21 2025

France| Mar 21 2025INSEE Manufacturing and Services Steady-to-Weaker

The INSEE industry climate index settled lower in March at 95.9, down from 97.0 in February. The index is lower than its year-ago value of 102.1 and since 2001 it has been this low or lower only 7.5% of the time. Despite the sense of some stability in manufacturing in the tabular data for the last year, the chart (of data since 2014) and the table’s own presentation of the queue standing reveals manufacturing to be at a relative weak standing in March.

Manufacturing production expectations have a 34.4 percentile standing but did improve slightly from the February reading of -14.8. The recent trend of production weakens on the month to a lower quartile standing at its 23.7 percentile. The personal likely trend, which is the reading for each respondent gives to the prospects for his own industry, ticked higher in March to a 40.5 percentile standing. That is better than the percentile for industry over all but still below the level that marks the historic median – a standing at the 50th percentile.

Orders and demand as well as foreign orders and demand each weakened. They each have standing at or below their respective 20th percentile around the lower one-fifth of all historic readings. In addition, the March reading for orders and demand are substantially weaker than they were a year ago and the slippage has been worse for foreign orders.

In contrast, inventory level show few changes and are similar to their year-ago readings and close to their historic median.

Prices have moved to lower readings in recent months. However, price trends and level readings are higher than they were a year ago. In terms of rankings, the own likely price trend is at a 61.5 percentile standing, above its historic median while the manufacturing price level has a relatively weak 36.1 percentile standing.

Global| Mar 20 2025

Global| Mar 20 2025Charts of the Week: Reversal of Fortunes

US equity markets have underperformed relative to global peers in recent weeks, as investor sentiment has deteriorated in response to weaker-than-expected growth data and growing concerns about the Trump administration’s economic policies (chart 1). The administration’s renewed push for tariffs, alongside fiscal expansion and tighter immigration policies, has fuelled stagflation fears, compounding the uncertainty surrounding the Fed’s next steps. This week, the Fed opted to keep its policy rate on hold but acknowledged rising downside risks by revising its GDP growth forecast lower, signalling caution about the economic outlook despite lingering inflation concerns. Foreign capital flows into US assets and their impact on the strong dollar are also showing signs of softening, as trade tensions and policy unpredictability raise questions about long-term US economic stability (chart 2). Meanwhile, global imbalances remain entrenched—China and Germany continue to run high savings rates, while the US remains structurally dependent on external capital to finance its deficits (chart 3). Trump’s efforts to rebalance trade through protectionist measures may struggle to overcome these deeper economic realities, particularly as demographic trends reinforce the service-oriented nature of the US economy and constrain China’s transition to a consumption-driven model (chart 4). Other central banks are also caught in this evolving landscape—wage growth is slowing in Europe, but lingering inflation risks suggest that rate-cutting cycles could remain uneven (chart 5). For China, where the property market downturn has been a major drag on growth, recent policy measures have offered signs of stabilization, but the road to recovery also remains uncertain (chart 6). With the US economy at risk of slowing more sharply than anticipated, central bank policies finely balanced, and China’s long-term growth trajectory still in question, the coming months could prove pivotal in determining whether global financial markets find their footing or remain mired in volatility.

by:Andrew Cates

|in:Economy in Brief

USA| Mar 20 2025

USA| Mar 20 2025U.S. Existing Home Sales Rebound in February

- Sales remain up from September low.

- Sales patterns vary from state-to-state.

- Median sales price recovers m/m.

by:Tom Moeller

|in:Economy in Brief

USA| Mar 20 2025

USA| Mar 20 2025U.S. Current Account Deficit Narrows in Q4 2024

- Goods deficit widens to nearly largest in three years. Services surplus increases to largest in five years.

- Balance on primary income returns to positive territory.

- Secondary income balance turns slightly less negative.

by:Tom Moeller

|in:Economy in Brief

- of2725Go to 120 page