- Inventories made even larger contribution than in first two estimates.

- Domestic demand growth revised down. Corporate profit growth slowed.

- Price inflation unrevised at 40-year high.

USA| Mar 30 2022

USA| Mar 30 2022U.S. Q4 GDP Growth Revised Down Slightly in Third Estimate

by:Sandy Batten

|in:Economy in Brief

USA| Mar 29 2022

USA| Mar 29 2022U.S. FHFA House Price Index Strengthens in January

- Monthly increases are mixed regionally.

- Mountain states lead price gains y/y.

by:Tom Moeller

|in:Economy in Brief

USA| Mar 29 2022

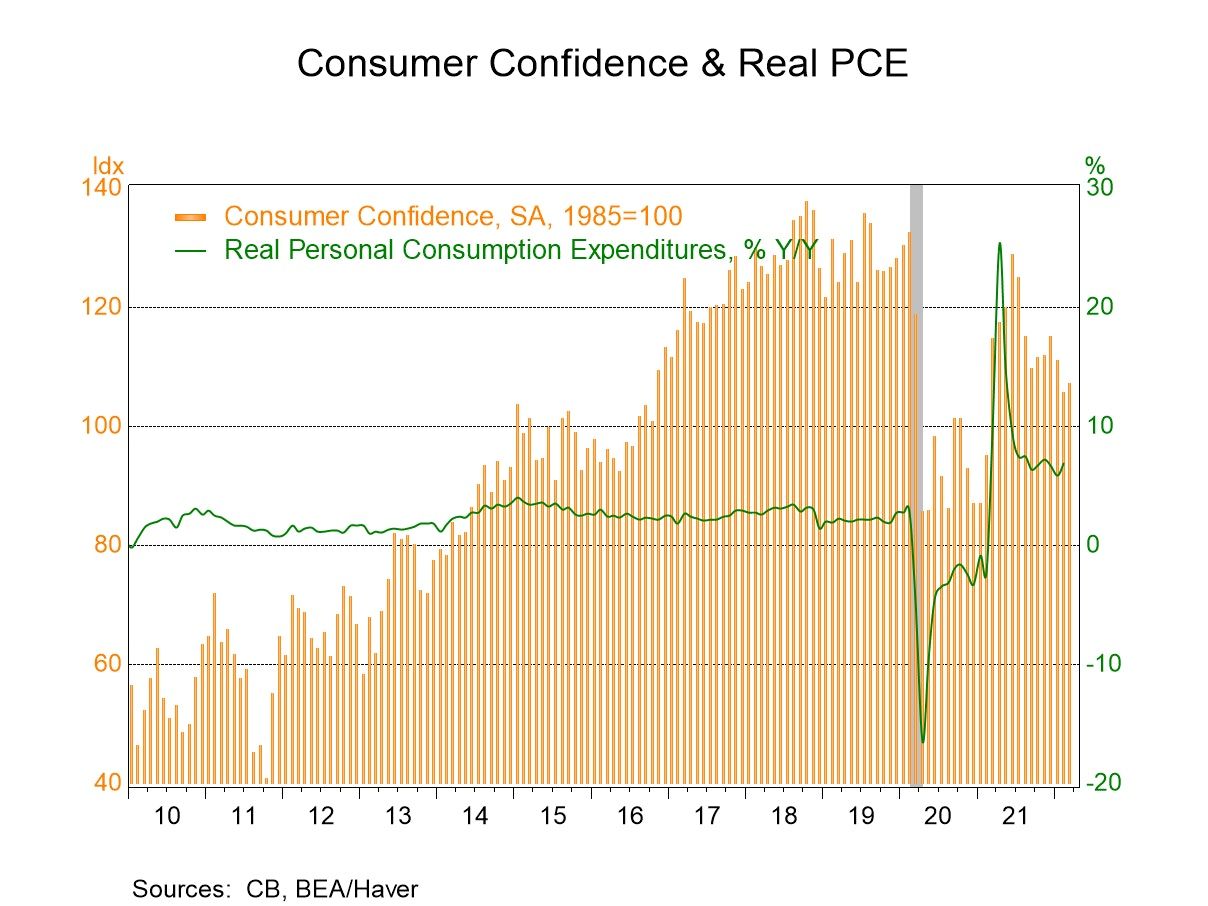

USA| Mar 29 2022U.S. Consumer Confidence Improves in March

- Present situation index strengthens; expectations falter.

- Jobs are easier to find.

- Expectations for inflation surge.

by:Tom Moeller

|in:Economy in Brief

USA| Mar 29 2022

USA| Mar 29 2022U.S. Energy Prices Remain Strong

- Gasoline prices edge downward.

- Crude oil prices move higher.

- Natural gas prices exhibit renewed strength.

by:Tom Moeller

|in:Economy in Brief

USA| Mar 29 2022

USA| Mar 29 2022U.S. JOLTS: Job Openings Nearly Steady in February

- Job openings rate unchanged at 7.0%.

- Hirings increase enough that rate rose.

- Quits rose while layoffs & discharged eased.

USA| Mar 28 2022

USA| Mar 28 2022U.S. Goods Trade Deficit Narrows in February

- Exports rebound after sharp decline.

- Imports edge higher following strong increase.

by:Tom Moeller

|in:Economy in Brief

Germany| Mar 28 2022

Germany| Mar 28 2022German IFO: Man Overboard!

The current IFO gauge in March fell sharply from a value of 15.5 in February to -6.3 in March. The manufacturing sector fell from a reading of 23.1 to -3.3. Construction fell from a reading of 8 to a reading of -12.2. Wholesaling fell from 14.3 to -6 6. Retailing fell from a February mark of -3.4 to -19.0 in March. The service sector reading of 13.6 in February diminished to 0.7 in March. It's the only positive net reading for climate in the IFO in March. As a whole, the business situation in the current environment erodes from 24.8 in February to 21.1 in March while expectations plummet from 6.3 in February to -21.7 in March. These are dramatic declines in the assessment of climate and expectations in the March IFO report.

Rankings We further evaluate the climate assessments by looking at the rankings of these sectors: the all-sector index has a ranking since 1991 in its 35th percentile, meaning it's been weaker only 35% of the time. Manufacturing is in its 27.7 percentile, wholesaling is in its 45th percentile, and retailing is in its 32nd percentile. Services, despite being the only positive net reading, is at the lowest standing of the bunch at a 9.5 percentile reading. Construction, despite its climate reading of -12.2, has a 60.1 percentile standing. That means based on all the construction metrics back to 1991 construction is lower 60% of the time and higher 40% of the time; it is the only sector above its historic median on this timeline.

Ranking of one-month changes The ranking of month-to month changes back to 1996 shows the largest one-month change and decline in manufacturing on record. Construction, wholesaling, and services have weakened by more month-to-month less than 1% of the time on that timeline. Retailing has weakened by more only 1.2% of the time. These are draconian changes month-to-month. It is stunning that markets have not reacted by more than they have with these kinds of erosions in the fundamentals.

Current conditions vs. expectations show stark difference There's a stark difference between the readings for current conditions and expectations this month. It noted above that the all-sector current index fell to 21.1 in March from 24.8 in February, while expectations in March plunged to -21.7 from 6.3. In February current conditions have not been that adversely affected at this point by the war in Ukraine, the sanctions, the recirculating virus, and other generalized economic circumstances in the German economy. However, expectations have been vastly downgraded. We see this by looking at standings of the two metrics: for current conditions, a 36.2% standing prevails which leaves the reading weak, in the lower one-third of its range; however, expectations have a 4.8-percentile standing. The components of expectations are even weaker than the 5% overall expectations standing. Each of the components of expectations in the IFO framework has a rank standing below the 4.8-percentile mark. The weakest being construction at 0.3%, the second weakest is wholesaling, followed by retailing at 2.3%, and then manufacturing at 2.4%. Looking at the individual standings for current conditions, services clearly is driving down the overall rank for the sector. Services has a 22.1 percentile standing. All the other industries: wholesaling, retailing, and manufacturing boast respective standings that are well above their 50th percentile mark (60th, 70th and 80th percentiles, in fact) indicating that they're above their medians for the period (reminder: median occurs at a ranking of 50%). Yet, the sector median stands in the 36th percentile dragged down exclusively by services weakness.

Position since before Covid struck is broadly weaker The far-right column chronicles change in the various line items compared to their levels in January 2020, before the virus struck. All the climate readings show declines compared to that date. Under current conditions, only manufacturing and wholesaling show increases. Among expectations all sectors are weaker and all of them are weaker in double digits.

USA| Mar 28 2022

USA| Mar 28 2022Texas Manufacturing Activity & Outlook Weaken in March

- Production & shipments growth falls sharply.

- New orders growth and employment improve.

- Prices received & wages strengthen.

by:Tom Moeller

|in:Economy in Brief

- of102Go to 79 page