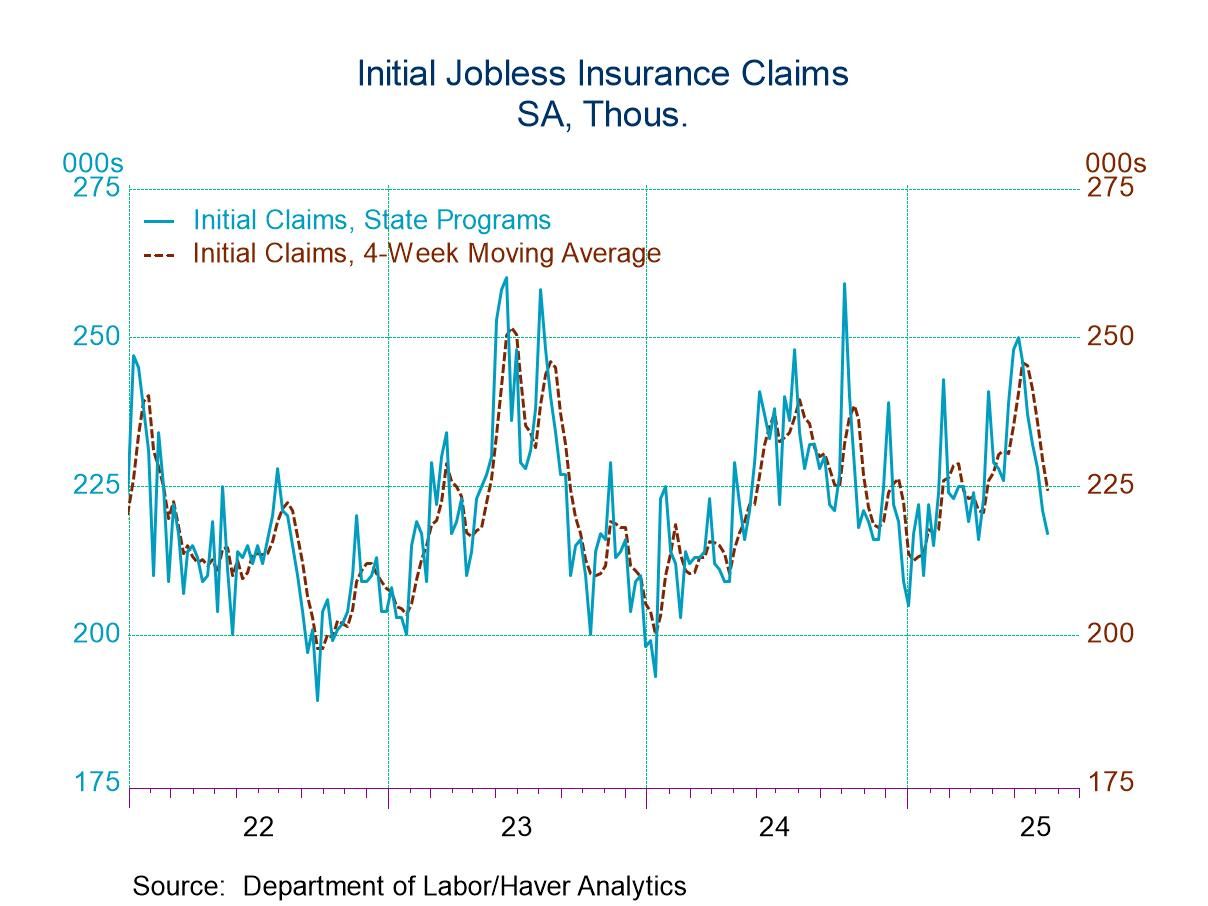

- Initial claims have declined for six consecutive weeks in the July 19 week.

- Continuing claims rose slightly in the July 12 week.

- Insured unemployment rate was unchanged for the seventh consecutive week.

Germany| Jul 24 2025

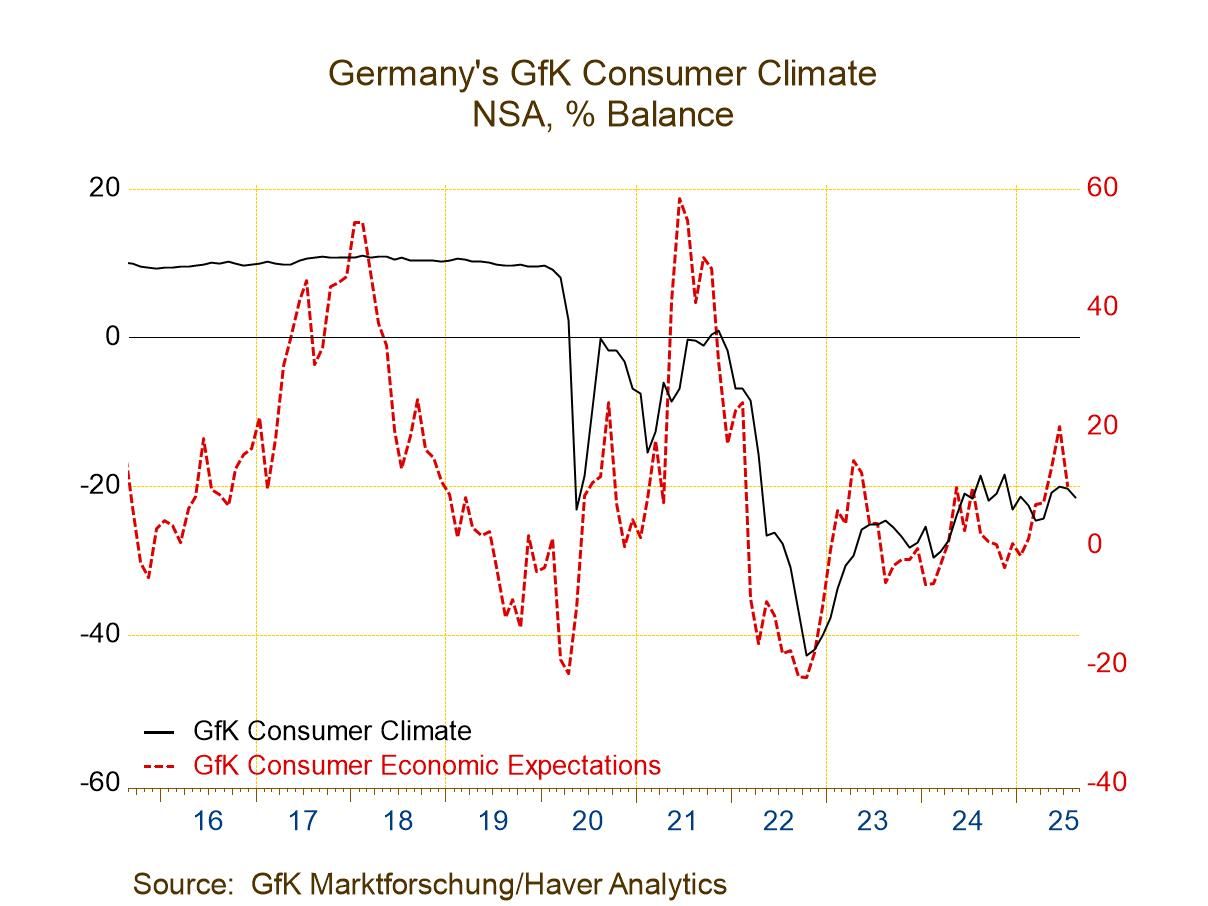

Germany| Jul 24 2025GfK Consumer Climate Steps Back After a Rise and a Pause

German consumer climate fell to -21.5 in August after logging -20.3 in July; July had posted a slight deterioration compared to June which had a -20.0 reading; however, previously in May the reading had improved sharply to -20.8 from -24.3 in April. The month of May had seemed to signal an improvement that took the climate readings from the -24 to -25 range into the -20 range. And while the -20 level held for three months in a row, there's now been a deterioration back to -21.5 in August and some renewed concerns about the economy.

Resilience and questions... So far there has been a good deal of economic resilience in Germany and in Europe; however, the recent deal by NATO members to spend 5% of GDP on defense is channeling a lot of that money to the United States to purchase missiles to help Ukraine in defense against Russia. However, 1 1/2 percentage points of that military spending pledge can actually be infrastructure spending that can be used for domestic purposes to bolster military preparedness and operations. Therefore, that portion of the spending, at least, remains as stimulus for the European economy.

The inflation setting Inflation in the euro area is basically at ‘target’ for the headline and close to it for the core; the year-over-year core rate is about 2.3%. Even so, Europe is looking at a pace that's close to 2%, but still higher than 2% after a long stretch of inflation being over the 2% target. In today's press conference, ECB President Christine Lagarde, speaking on the inflation picture and outlook in the EMU, said that the bank's target was an intermediate target and that the ECB expected inflation to be at its target over the intermediate term. The question I would have for her and for the ECB at this point is whether that means that the inflation target has become “aspirational” and is no longer operational? If the ECB is going to be happy with an inflation rate that stays above 2% as long as it thinks that ‘in the intermediate term’ inflation is going back to 2% has something significant changed? And since all forecasts are notoriously wrong – is this now a credibility issue for the ECB?

German eco-climate In Germany, the GfK measure is for August; components for the climate measure are up-to-date through July. Economic expectations took a turn lower after posting 20.1 in June; they slipped to 10.1 in July. The most recent observation of record for income expectations, however, advanced from 12.8 in June to 15.2 in July, continuing a string of improvements. The propensity to buy metric worsened and remained negative at -9.2 in July compared to -6.2 in June. The overall climate metric is now at its weakest since April 2025; economic expectations are their lowest since April 2025. Income expectations are trending higher, nonetheless. The propensity to buy metric at -9.2 in July is at its weakest reading since February 2025; but that was a single-isolated low, setting that observation aside, the ‘propensity to buy’ is the weakest it's been since August 2024. The German consumer clearly hasn't recovered in terms of having faith and purchasing power restored even though income expectations have risen more substantially.

Queue standing assessments In terms of the queue percentile standings (ranked data observations), climate has been weaker than this 11.5% of the time, economic expectations have been weaker 59% of the time, income expectations have been weaker 50.7% of the time, while the propensity to buy has been weaker only 29.1% of the time. Economic expectations are above their median - above a ranking value of 50% - while income expectations have only returned to their median estimate, marginally above 50%, at a reading of 50.7%. The propensity to buy languishes at the bottom 1/3 of its historic queue of values. The climate headline remains in disaster territory.

Other Europe: Other EMU and the U.K. These observations for Germany contrast to observations in the rest of Europe where data lag. Consumer confidence metrics for Italy, France, and the U.K. are up-to-date only through June. And through that period, Italy shows the last two observations a little bit stronger, France shows the most recent two observations as, very similar, but weaker than April, while the U.K. shows the progression towards stronger readings from April to May to June. However, the rankings for these countries are quite mixed. For Italy consumers held confidence in June at a 73.2 percentile standing, relatively firm, while in France the standing is at its 26.4 percentile and in the U.K. it is at its 37.5 percentile. The climate in Germany is exceptionally low although the readings for the European countries in the table are somewhat more similar to the readings for the German climate components that are up-to-date through July.

USA| Jul 23 2025

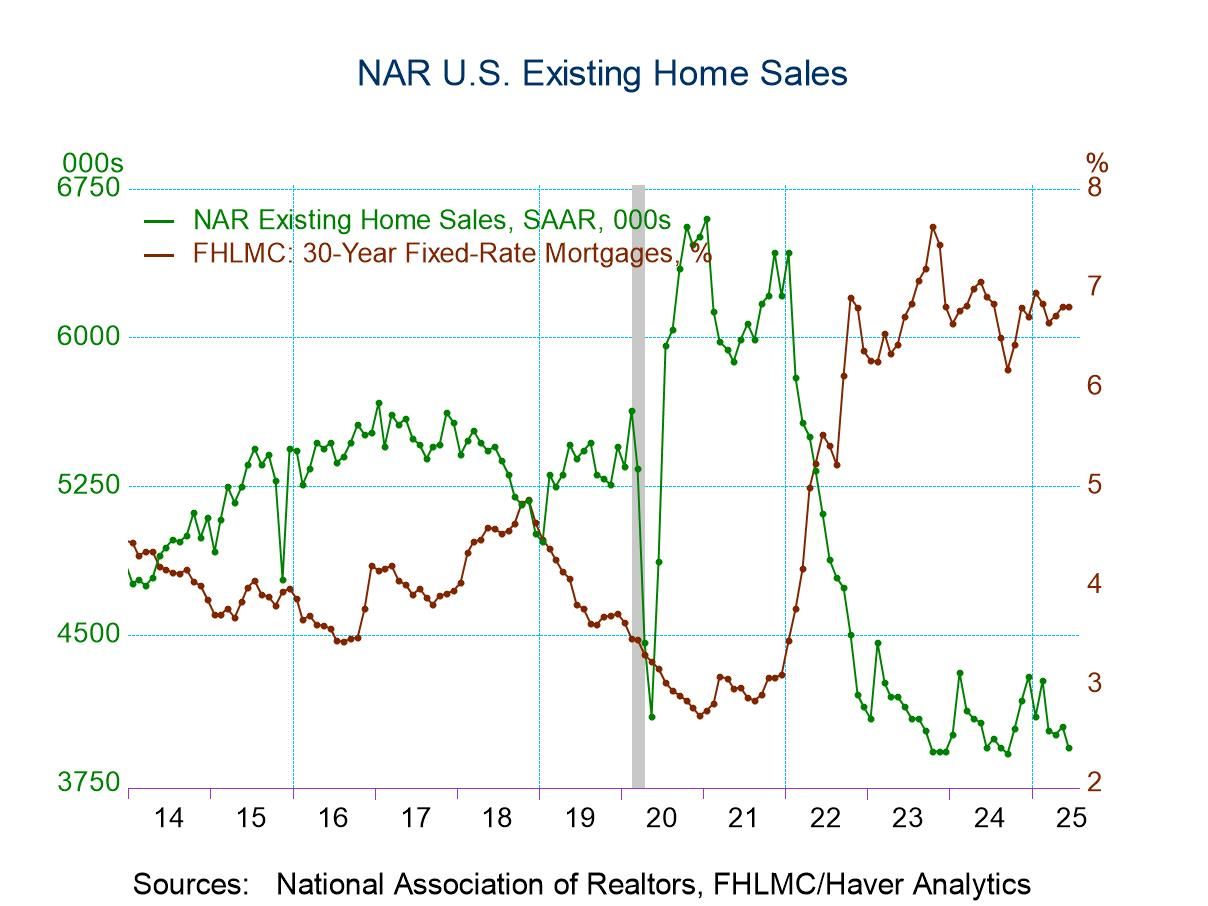

USA| Jul 23 2025U.S. Existing Home Sales Decline in June; Home Prices Set Record

- Sales are lowest in nine months.

- Decline spreads throughout country except in West.

- Median sales price strengthens to record high.

by:Tom Moeller

|in:Economy in Brief

USA| Jul 23 2025

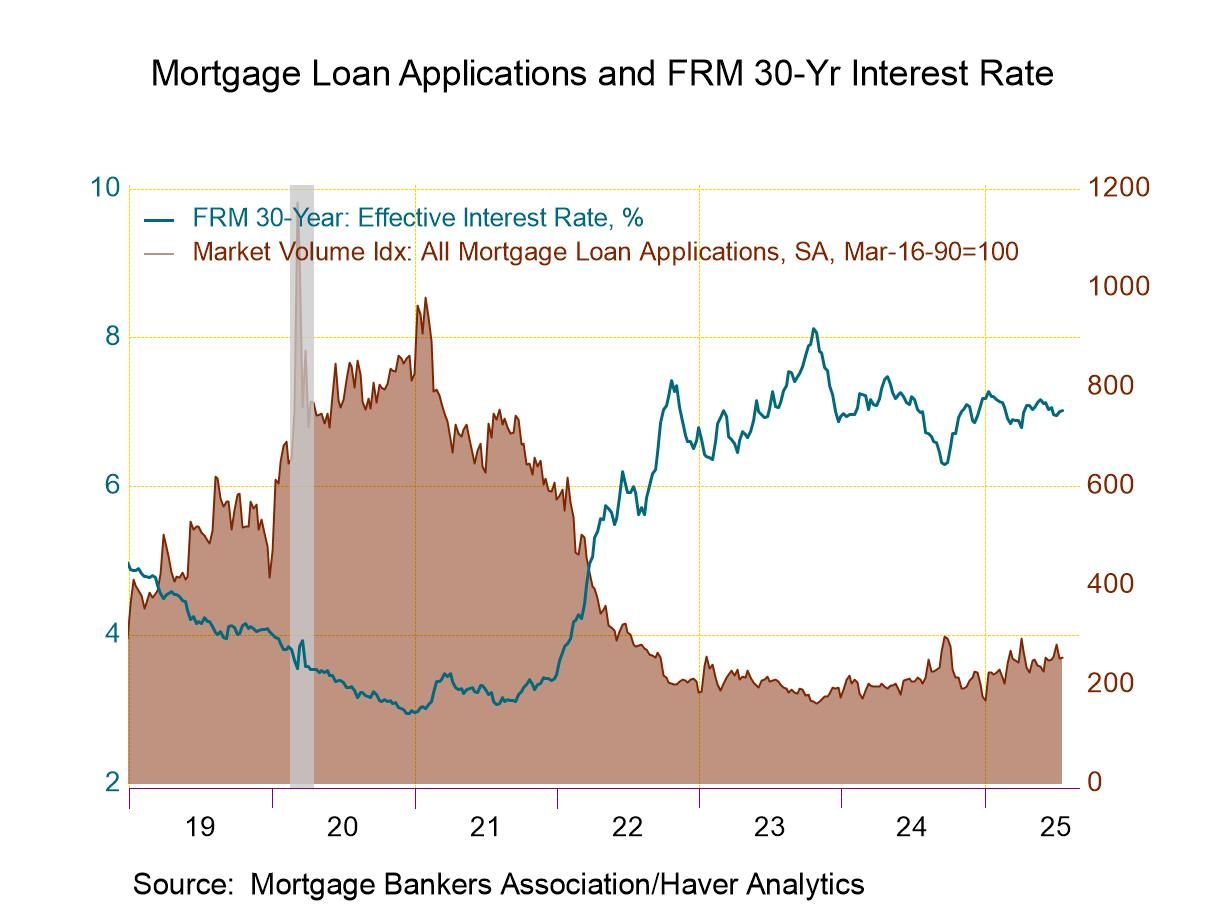

USA| Jul 23 2025U.S. Mortgage Applications Edge Higher Last Week

- Purchase applications increase sharply while loan refinancing falls.

- Effective interest rate on 30-year fixed-rate loan increases minimally.

- Average loan size declines for fifth week in last six.

by:Tom Moeller

|in:Economy in Brief

USA| Jul 22 2025

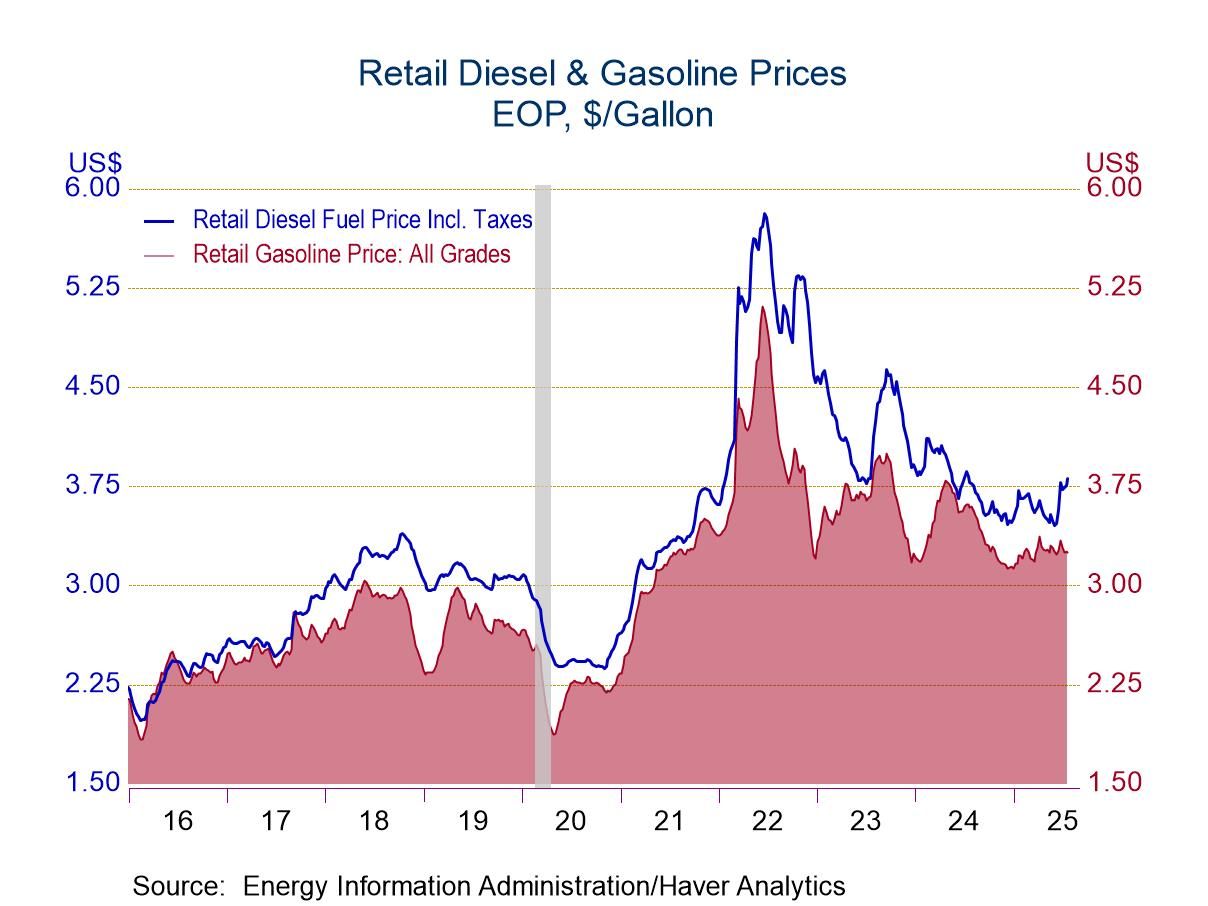

USA| Jul 22 2025U.S. Energy Prices Are Mixed in Latest Week

- Gasoline prices hold steady.

- Crude oil prices decline.

- Natural gas prices strengthen.

by:Tom Moeller

|in:Economy in Brief

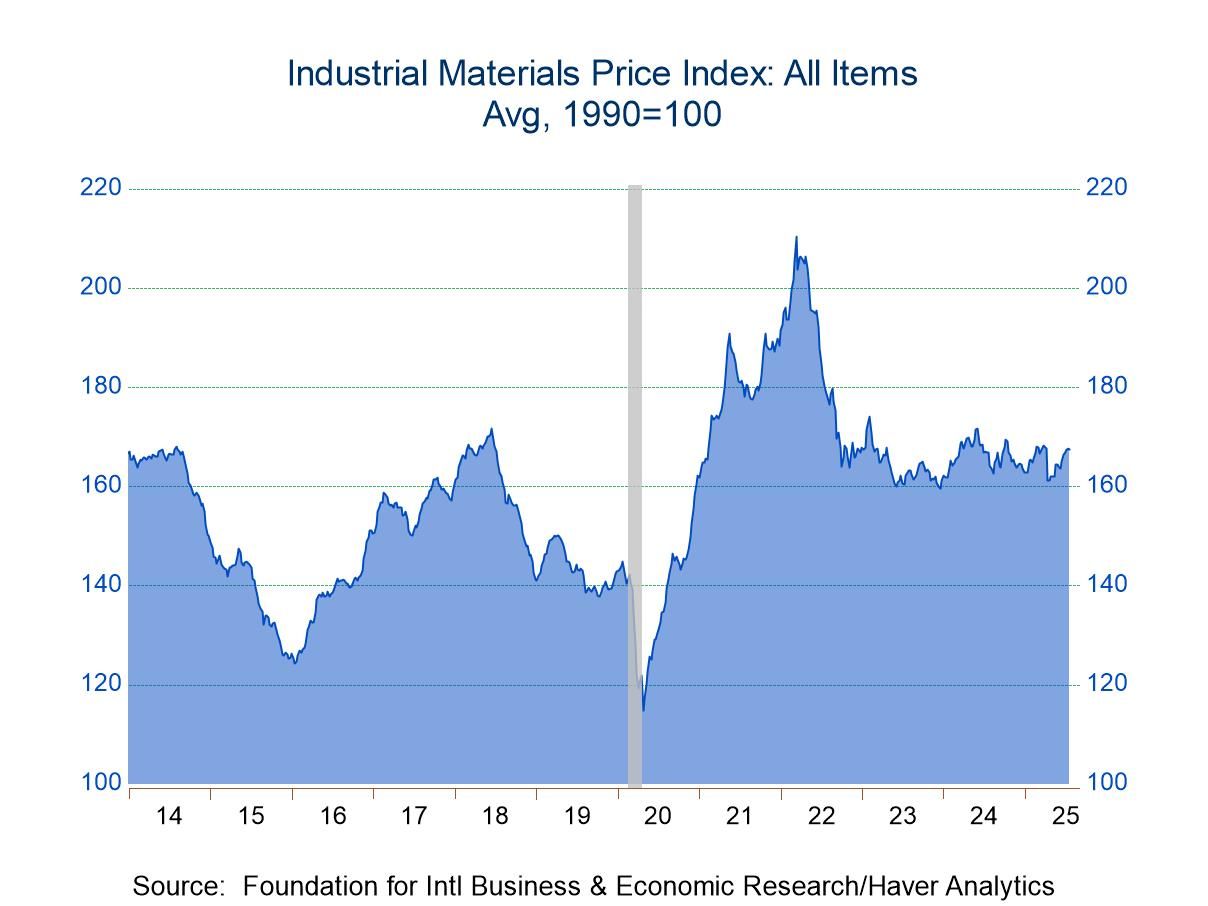

- Prices movement by category is mixed.

- Lumber & metals prices strengthen.

- Crude oil prices decline.

by:Tom Moeller

|in:Economy in Brief

USA| Jul 18 2025

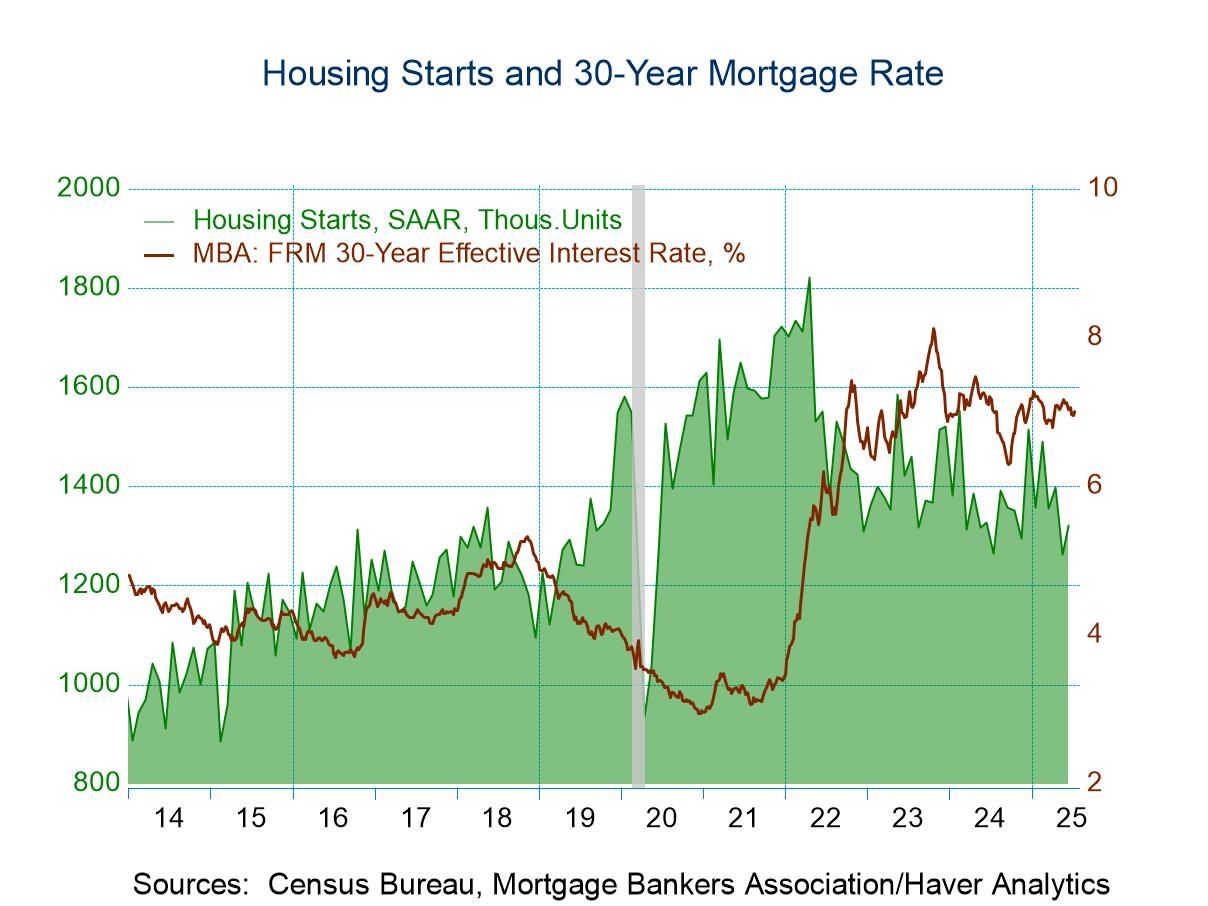

USA| Jul 18 2025U.S. Housing Starts Rebound in June

- Increase recovers half of prior month’s drop.

- Multi-family starts surge but single-family starts fall.

- Building permits rise negligibly after two months of decline.

by:Tom Moeller

|in:Economy in Brief

Japan| Jul 18 2025

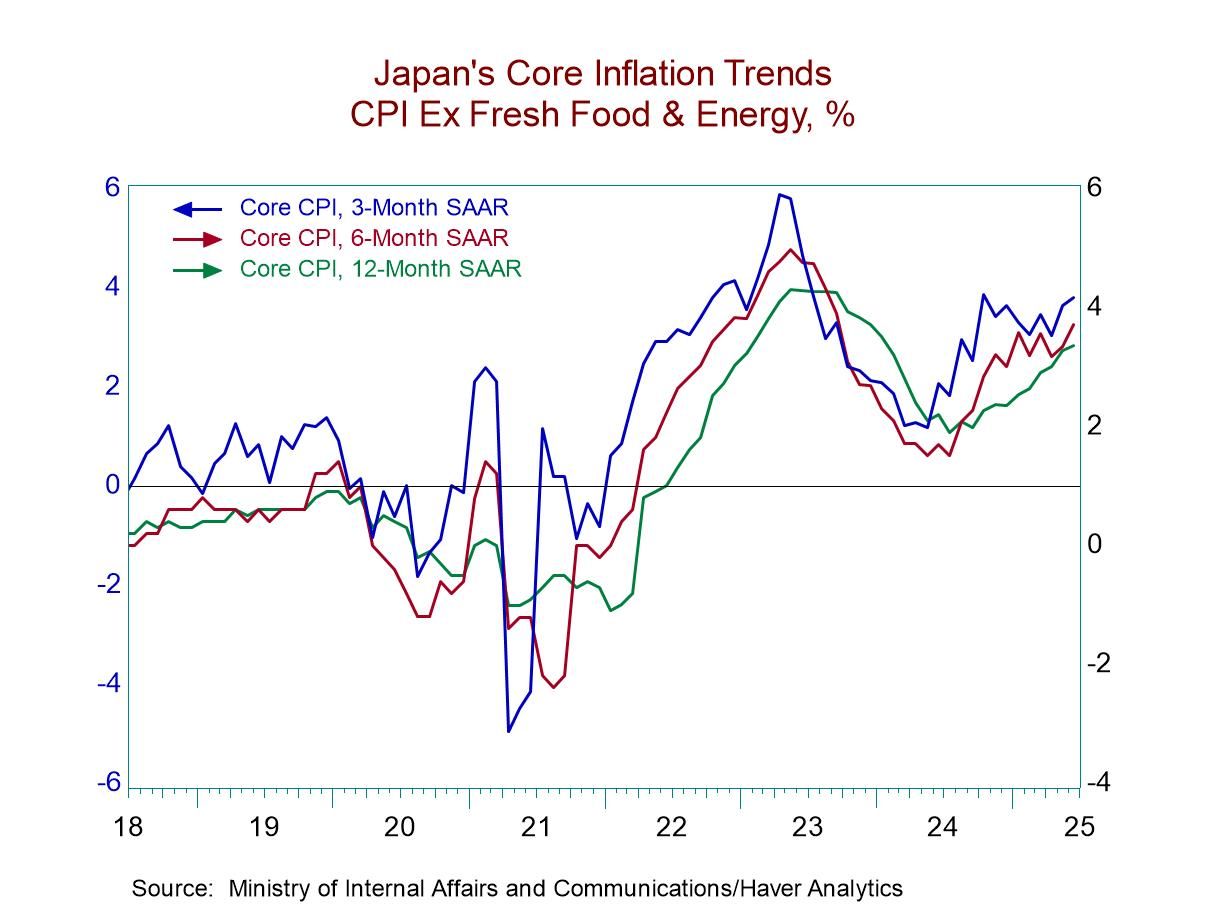

Japan| Jul 18 2025Japan’s Ex-Fresh-Food Ex-Energy Inflation Runs Hot

No one will be critical of Japan’s efforts to free itself of its torpor into disinflation and deflation that it suffered for many years. The Bank of Japan struggled long and hard to remove the contraction in prices from its economy since falling prices can have a pernicious effect on growth and investment. Japan still faces challenges: it has a contracting population and faces dealing with tariff demands from the United States as negotiations on that front continue to drag and have become harder to settle than Japan had expected. Despite the current inflation overshoot, on data back to January 2011, Japan’s to-date inflation is only averaging 1%; that is still well below its 2% target and ample reason for the Bank of Japan to continue to move carefully to corral inflation especially if inflation has stopped accelerating – as it seems to have done. Against this background, we look at Japan’s CPI report.

Current inflation: June Japan has dispatched deflation and currently faces an inflation problem. In June, the BOJ’s preferred gauge for the CPI excluding fresh foods & energy rose 0.4% month-to-month for the second month in a row; it rose by 0.2% in April. Japan’s headline inflation rate seems to have fallen into line A traditional ‘core reading’ excluding all food & energy flies under the BOJ’s target pace. But the BOJ’s preferred inflation gauge shows a 3.4% rise over 12 months and then gains at a pace of 3.7% over both six months and three months. All of those numbers are too hot to handle.

Line-items Education costs in Japan are falling sharply and sequentially. Medical care costs are deescalating too. And while food & beverage prices continue to overshoot, 2% by a wide margin, the pace of total food & beverage inflation has been falling. No broad category has steadily accelerating inflation. But the BOJ’s preferred gauge of inflation, a specialized core measure excluding energy & fresh foods, sees inflation ramping up and staying high over three months and six months.

Diffusion/breadth Among the eight major categories, year-on-year inflation has accelerated compared to where it was one-year ago in four of the eight. Inflation is above the 2% benchmark for four of eight categories as well.

Acceleration or not... The chart on sequential inflation for the BOJ’s preferred core gauge shows that this measure has accelerated since August or December of last year and since then has more or less marked time oscillating without any clear trend.

- of10Go to 4 page