Japan’s Ex-Fresh-Food Ex-Energy Inflation Runs Hot

No one will be critical of Japan’s efforts to free itself of its torpor into disinflation and deflation that it suffered for many years. The Bank of Japan struggled long and hard to remove the contraction in prices from its economy since falling prices can have a pernicious effect on growth and investment. Japan still faces challenges: it has a contracting population and faces dealing with tariff demands from the United States as negotiations on that front continue to drag and have become harder to settle than Japan had expected. Despite the current inflation overshoot, on data back to January 2011, Japan’s to-date inflation is only averaging 1%; that is still well below its 2% target and ample reason for the Bank of Japan to continue to move carefully to corral inflation especially if inflation has stopped accelerating – as it seems to have done. Against this background, we look at Japan’s CPI report.

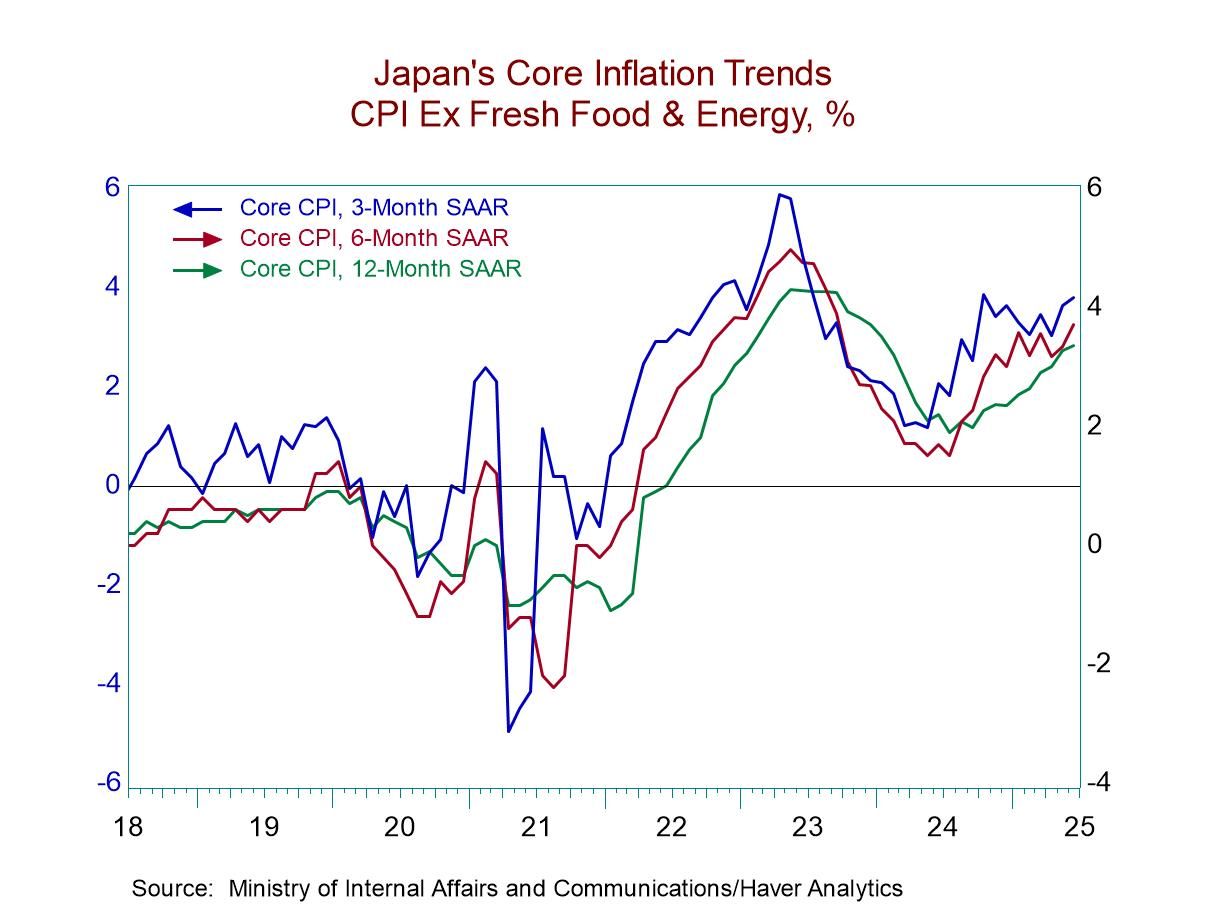

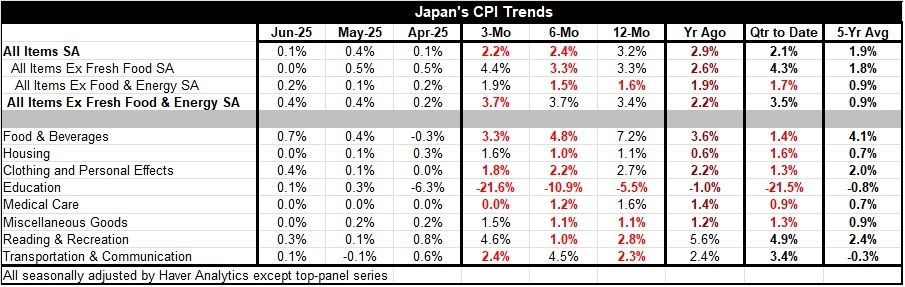

Current inflation: June Japan has dispatched deflation and currently faces an inflation problem. In June, the BOJ’s preferred gauge for the CPI excluding fresh foods & energy rose 0.4% month-to-month for the second month in a row; it rose by 0.2% in April. Japan’s headline inflation rate seems to have fallen into line A traditional ‘core reading’ excluding all food & energy flies under the BOJ’s target pace. But the BOJ’s preferred inflation gauge shows a 3.4% rise over 12 months and then gains at a pace of 3.7% over both six months and three months. All of those numbers are too hot to handle.

Line-items Education costs in Japan are falling sharply and sequentially. Medical care costs are deescalating too. And while food & beverage prices continue to overshoot, 2% by a wide margin, the pace of total food & beverage inflation has been falling. No broad category has steadily accelerating inflation. But the BOJ’s preferred gauge of inflation, a specialized core measure excluding energy & fresh foods, sees inflation ramping up and staying high over three months and six months.

Diffusion/breadth Among the eight major categories, year-on-year inflation has accelerated compared to where it was one-year ago in four of the eight. Inflation is above the 2% benchmark for four of eight categories as well.

Acceleration or not... The chart on sequential inflation for the BOJ’s preferred core gauge shows that this measure has accelerated since August or December of last year and since then has more or less marked time oscillating without any clear trend.

BOJ policy and communication With interest rates having been elevated, this may be the peak for inflation rates in the wake of past interest rate increases- but the BOJ moves to-date have been more about communication and signaling than about actual restraint. These sorts of determinations about the impact of policy are always preliminary and never made clear until time passes and we are able to observe how the trend unfolds. Has inflation really peaked or not?

BOJ actions The BOJ has raised its policy rate in very small and careful steps with an eye to not disrupt markets. Until early 2024, the BOJ has promoted a negative policy rate coupled with policy of yield curve control. However, in early 2024 the BOJ switched the -0.1% target rate to +0.1% and then moved it up to 0.25% just after mid-year 2024, then, early in 2025, it hiked it again to 0.5%. These have been cautious step-wise moves that after three hikes leave the official rate higher by less than one percentage point. But it also reversed an eight-year period of having a negative policy rate and one coupled with yield curve control policy. The BOJ’s careful steps may owe to some learning from the Federal Reserve’s SNAFU when it announced a coming end to its policy of QE for the first time creating a ‘taper tantum.’

The environment While Japan’s economy is growing, it has logged four quarters of negative growth in the past seven quarters (Q/Q). Year-on-year growth is positive for three quarters in a row after two in a row that logged declines. The economy is not strong, but it is growing in Q1; it grew by 1.7% over the past four quarters even though the Q/Q change was -0.2%, annualized.

Summing up The BOJ is taking policy steps slowly with national elections hovering in the background, keeping monetary policy out of the way of election discussions. So far, we would regard the BOJ’s anti-inflation steps as being more about communicating an end to a period of super easy policy than as a frontal-attack on rising inflation. Given that, Japan’s prices declined for many months from August 2020 to March 2020; the BOJ is being careful to try to arrest inflation increases without pummeling prices and restarting deflation. From January 2011 to September 2022, Japan had only 12 (out of 141) months of inflation above 2% on its preferred gauge. It is now on a run of 33 (well 32 out of 33) months in a row with year-on-year inflation at or above 2%. It is understandable that the BOJ is walking on eggshells when it comes to hiking rates. If its inflation requires a monetary brake, the BOJ has more to do. If inflation merely needs to be ‘reminded’ that the period of excess is over, the recent flattening of inflation could be a sign that the message has been heard. A turn lower for inflation may still be achievable without draconian monetary steps.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia