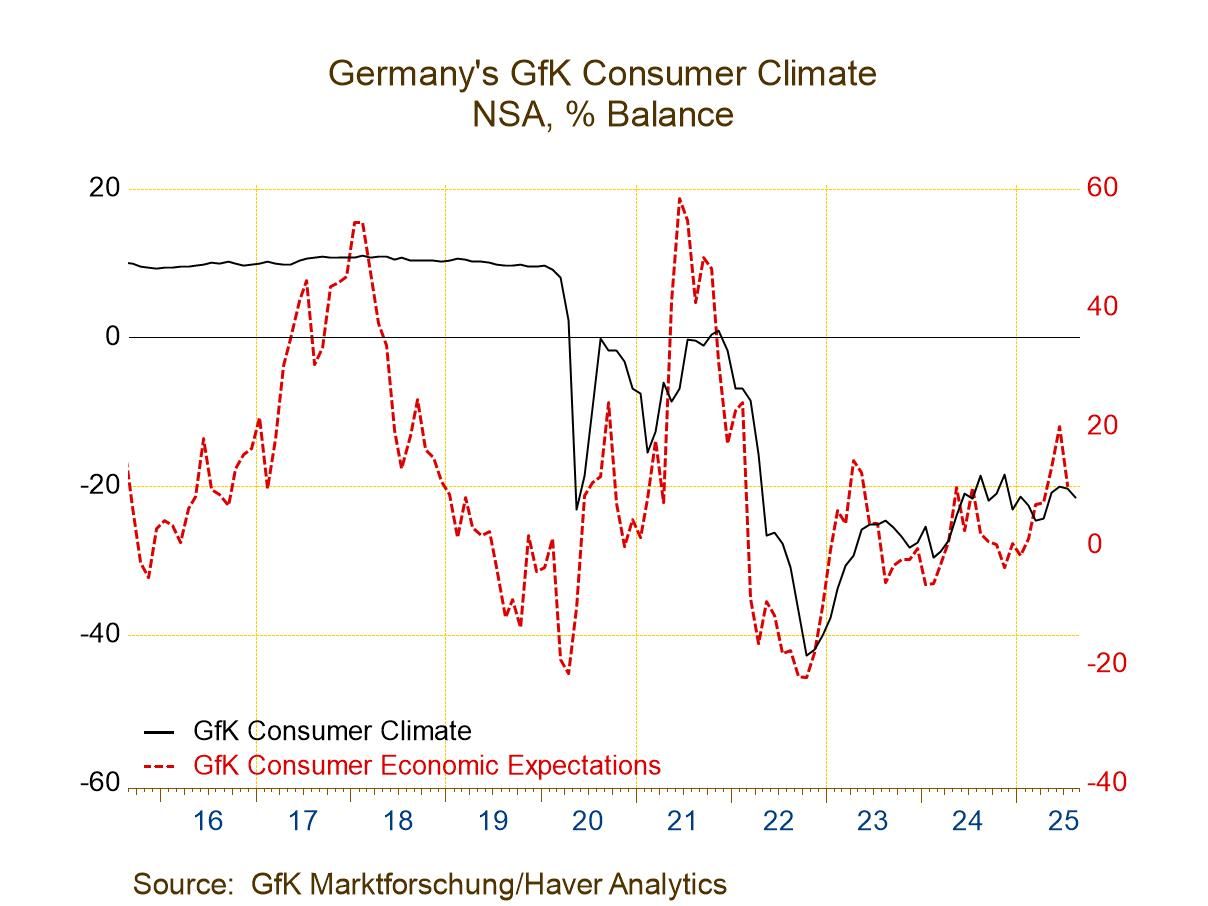

GfK Consumer Climate Steps Back After a Rise and a Pause

German consumer climate fell to -21.5 in August after logging -20.3 in July; July had posted a slight deterioration compared to June which had a -20.0 reading; however, previously in May the reading had improved sharply to -20.8 from -24.3 in April. The month of May had seemed to signal an improvement that took the climate readings from the -24 to -25 range into the -20 range. And while the -20 level held for three months in a row, there's now been a deterioration back to -21.5 in August and some renewed concerns about the economy.

Resilience and questions... So far there has been a good deal of economic resilience in Germany and in Europe; however, the recent deal by NATO members to spend 5% of GDP on defense is channeling a lot of that money to the United States to purchase missiles to help Ukraine in defense against Russia. However, 1 1/2 percentage points of that military spending pledge can actually be infrastructure spending that can be used for domestic purposes to bolster military preparedness and operations. Therefore, that portion of the spending, at least, remains as stimulus for the European economy.

The inflation setting Inflation in the euro area is basically at ‘target’ for the headline and close to it for the core; the year-over-year core rate is about 2.3%. Even so, Europe is looking at a pace that's close to 2%, but still higher than 2% after a long stretch of inflation being over the 2% target. In today's press conference, ECB President Christine Lagarde, speaking on the inflation picture and outlook in the EMU, said that the bank's target was an intermediate target and that the ECB expected inflation to be at its target over the intermediate term. The question I would have for her and for the ECB at this point is whether that means that the inflation target has become “aspirational” and is no longer operational? If the ECB is going to be happy with an inflation rate that stays above 2% as long as it thinks that ‘in the intermediate term’ inflation is going back to 2% has something significant changed? And since all forecasts are notoriously wrong – is this now a credibility issue for the ECB?

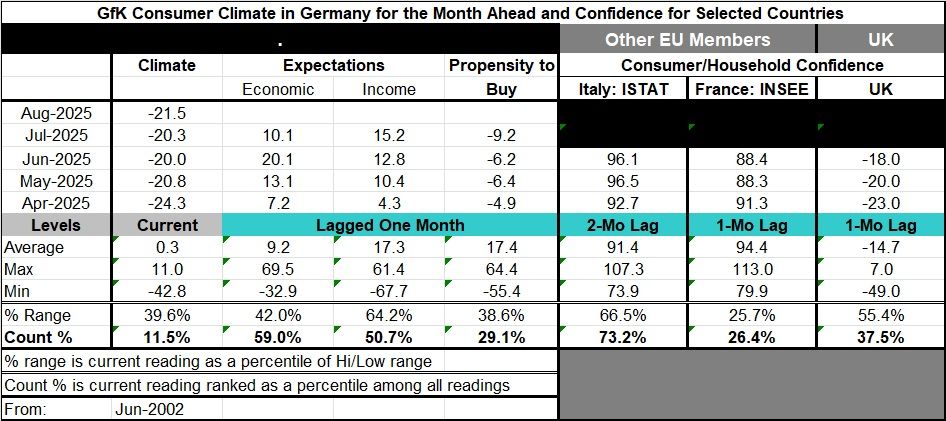

German eco-climate In Germany, the GfK measure is for August; components for the climate measure are up-to-date through July. Economic expectations took a turn lower after posting 20.1 in June; they slipped to 10.1 in July. The most recent observation of record for income expectations, however, advanced from 12.8 in June to 15.2 in July, continuing a string of improvements. The propensity to buy metric worsened and remained negative at -9.2 in July compared to -6.2 in June. The overall climate metric is now at its weakest since April 2025; economic expectations are their lowest since April 2025. Income expectations are trending higher, nonetheless. The propensity to buy metric at -9.2 in July is at its weakest reading since February 2025; but that was a single-isolated low, setting that observation aside, the ‘propensity to buy’ is the weakest it's been since August 2024. The German consumer clearly hasn't recovered in terms of having faith and purchasing power restored even though income expectations have risen more substantially.

Queue standing assessments In terms of the queue percentile standings (ranked data observations), climate has been weaker than this 11.5% of the time, economic expectations have been weaker 59% of the time, income expectations have been weaker 50.7% of the time, while the propensity to buy has been weaker only 29.1% of the time. Economic expectations are above their median - above a ranking value of 50% - while income expectations have only returned to their median estimate, marginally above 50%, at a reading of 50.7%. The propensity to buy languishes at the bottom 1/3 of its historic queue of values. The climate headline remains in disaster territory.

Other Europe: Other EMU and the U.K. These observations for Germany contrast to observations in the rest of Europe where data lag. Consumer confidence metrics for Italy, France, and the U.K. are up-to-date only through June. And through that period, Italy shows the last two observations a little bit stronger, France shows the most recent two observations as, very similar, but weaker than April, while the U.K. shows the progression towards stronger readings from April to May to June. However, the rankings for these countries are quite mixed. For Italy consumers held confidence in June at a 73.2 percentile standing, relatively firm, while in France the standing is at its 26.4 percentile and in the U.K. it is at its 37.5 percentile. The climate in Germany is exceptionally low although the readings for the European countries in the table are somewhat more similar to the readings for the German climate components that are up-to-date through July.

Summing up The GfK report for August continues to send the same message that the German economy is weak; it no longer has a silver lining of any significance, apart from income expectations. The rest of Europe is emitting signals that, for the most part, are weak with the exception of the U.K. The U.K. might be giving us somewhat better consumer confidence readings, but it is still an economy fighting off its own devils of various sorts.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global