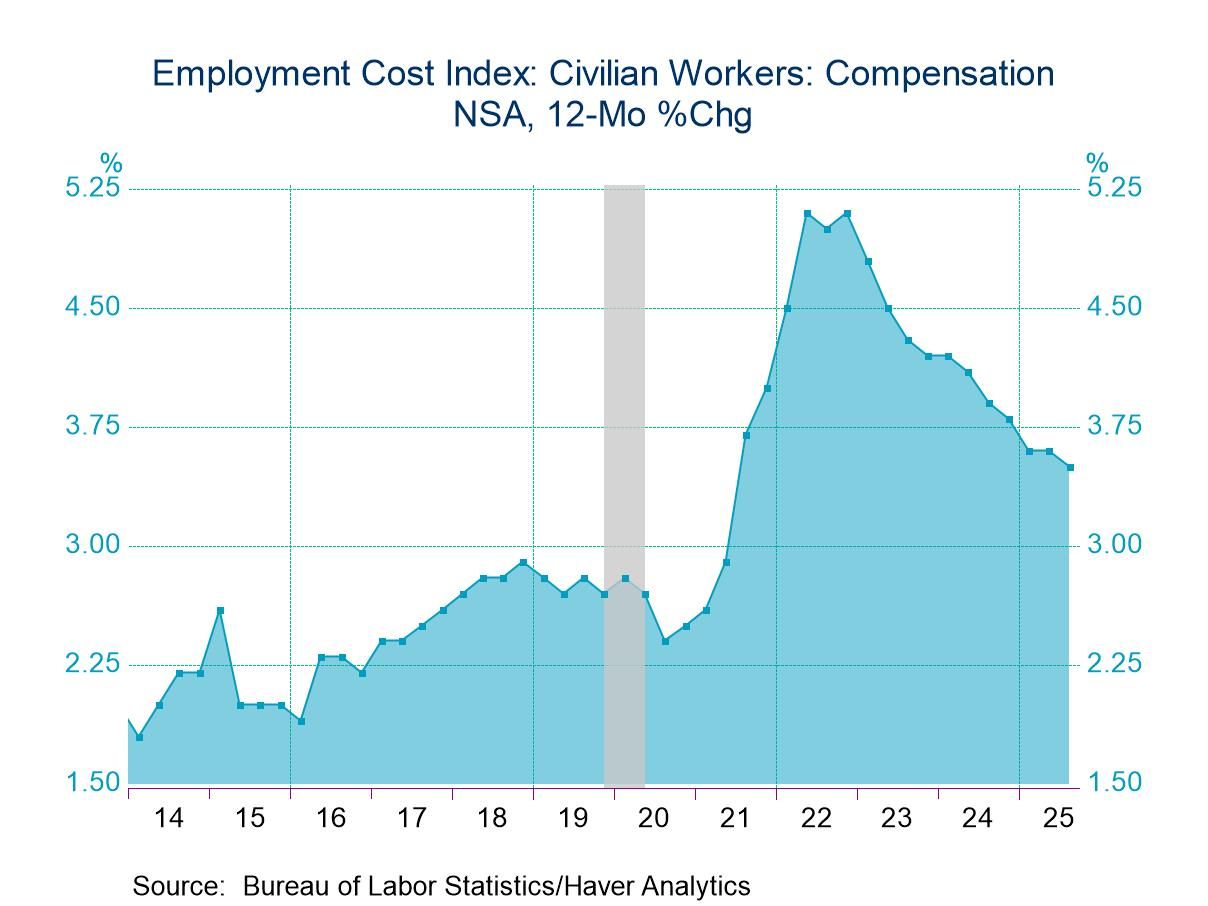

- Compensation continues to decelerate.

- Wage growth eases.

- Benefits increase edges up.

USA| Dec 10 2025

USA| Dec 10 2025U.S. Employment Cost Index Growth Eases in Q3’25

by:Tom Moeller

|in:Economy in Brief

USA| Dec 10 2025

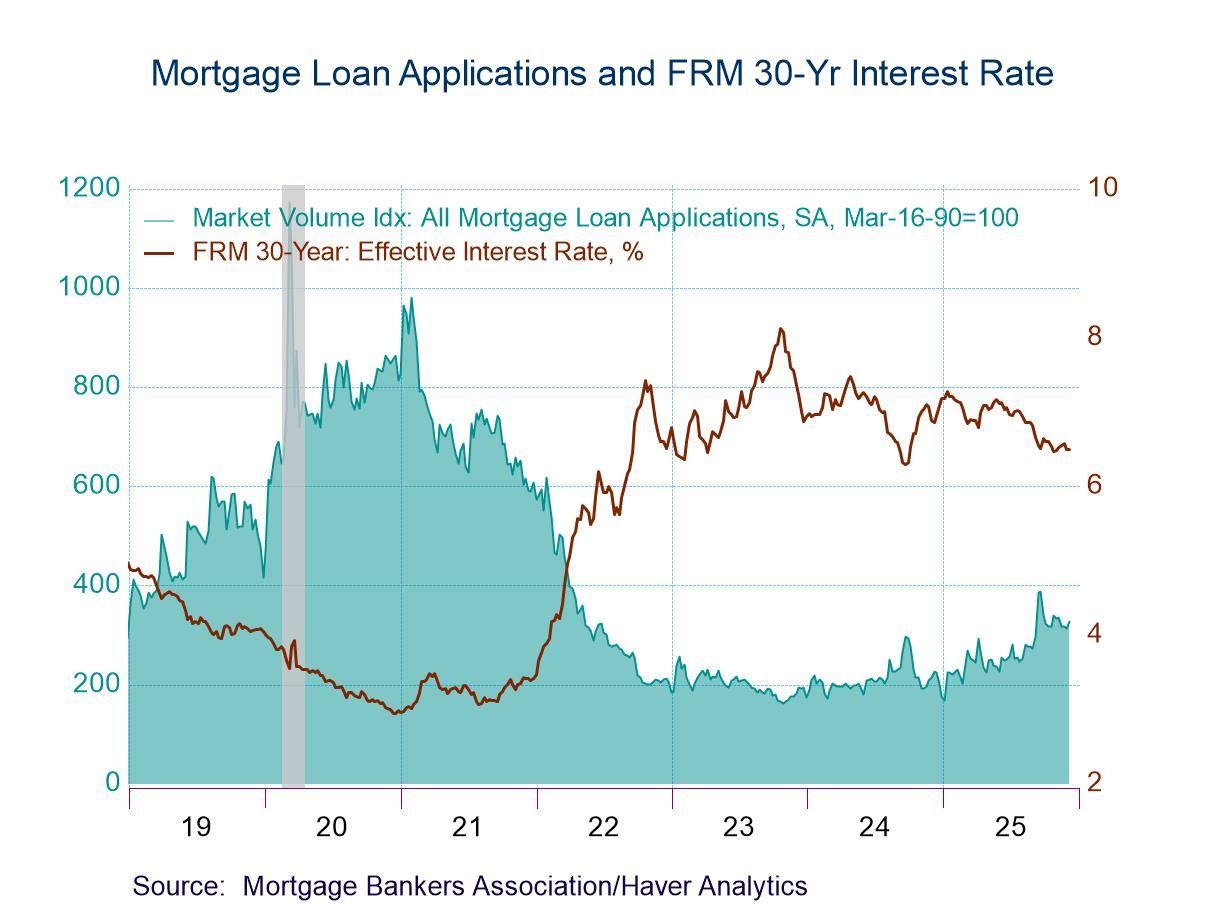

USA| Dec 10 2025U.S. Mortgage Applications Jump in the Week of December 5

- Purchase applications fell 2.4% w/w; refinancing loan applications soared 14.3% w/w.

- Effective interest rate on 30-year fixed loans largely unchanged at 6.50%.

- Average loan size fell moderately.

Sweden| Dec 10 2025

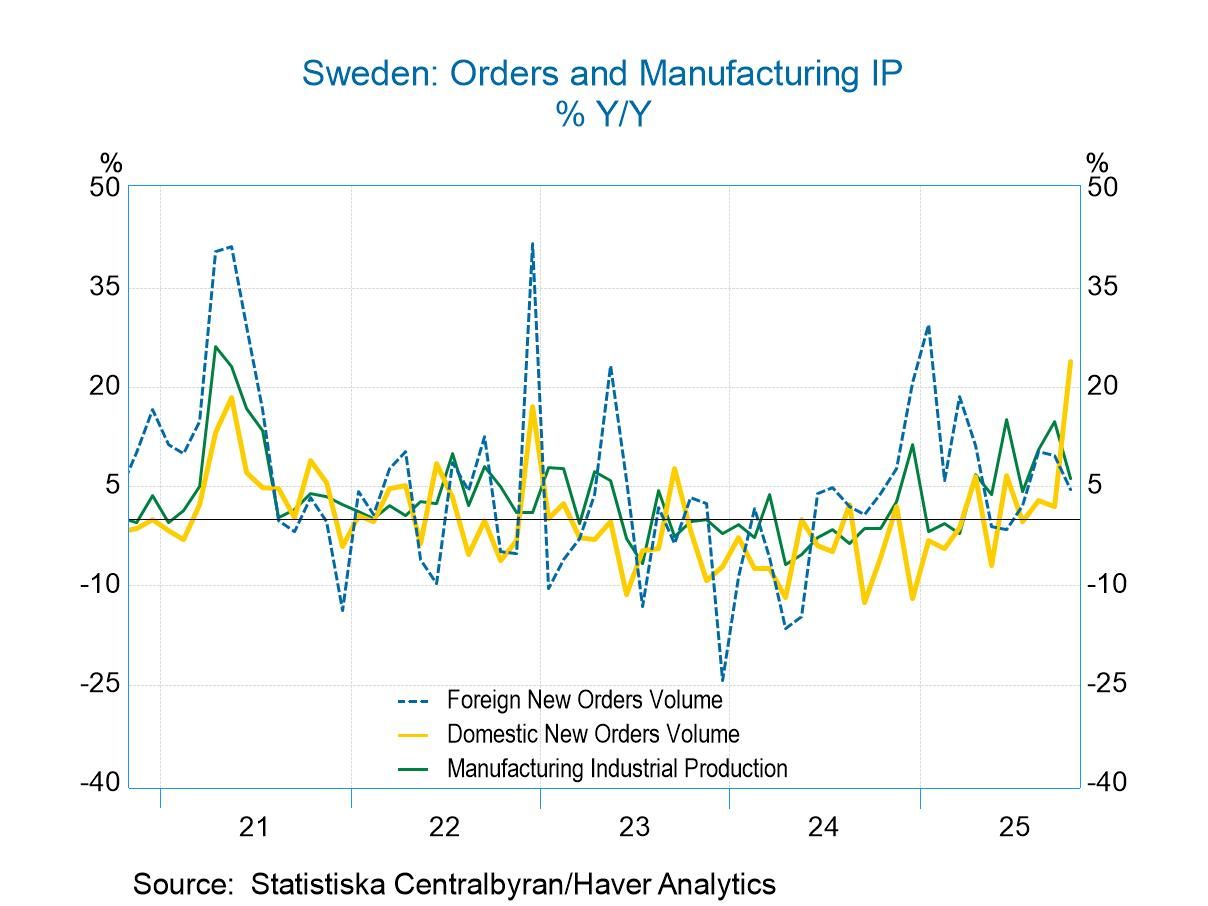

Sweden| Dec 10 2025Sweden’s Industrial Production Falls in October

Swedish IP turns up sour in October: Industrial production in Sweden fell 5.7% in October, a relatively large decline, but it comes in a period when industrial production has been unusually volatile. Going back to July, industrial production fell month-to-month by 7.8%, then rose by 5.6% in August, rose again by 4.3% in September, and now fell by 5.7% in October. These month-to-month figures show a great deal of volatility in this series for industrial production excluding construction. The performance for overall manufacturing production is similarly volatile. The components in the table show that vehicle production, intermediate goods production, investment goods production, and the production of consumer nondurables all demonstrate the same kinds of monthly volatility.

Broader sequential growth rates settle down: Turning to sequential growth rates, conditions appeared to settle down to some extent, as industrial production excluding construction rises 6.6% over 12 months, at a slower of 5% annual rate over six months, then hops up to a 16.6% annual rate over three months. Manufacturing demonstrates the same growth slowdown and spurts over 12 months, six months, and three months. So does motor vehicle production, but with even greater extremes in the swings. The production of intermediate goods, on the other hand, shows steady acceleration. The investment goods sector shows growth over 12 months leading to a six-month slowdown and then a super spurt over three months that brings the growth rate to 50% annualized. Consumer nondurables output, on the other hand, shows a consistent slowdown from a 15.9% increase over 12 months to an 11.7% annual rate of increase over six months, to a decline of 1.7% at an annual rate over three months.

All are off their cycle peaks: All industrial production figures are well off of cycle peaks with motor vehicles the farthest off their cycle peak at just under 80% of their cycle peak, a standing similar for consumer nondurables. Overall industrial production excluding construction is only about 6 percentage points below its actual peak.

Quarter-to-date: The quarter to date industrial production excluding construction and the figure for overall manufacturing both showing annual rate declines between 7 and 10% at an annual rate. Motor vehicle production is making a modest recovery with a low single-digit growth rate. Intermediate goods are so far flat in the new quarter, with the investment goods output rising at a 22.1% annual rate and consumer nondurables output falling at a 37.2% annual rate. Once again, we see a great deal of volatility in these figures.

Current growth rate rankings over 24 years: However, taking an historic context, if we confine ourselves to looking at the year-over-year growth rates for Swedish industrial production, we find that overall production excluding construction has the growth rate with an 85.2 percentile standing. Manufacturing has an 84-percentile standing. Intermediate goods have a 71.5 percentile standing, with consumer nondurables having an 86-percentiles standing; investment goods have only a 63% standing. The production of motor vehicles has a 41.6% standing; it is the only category with a growth rate below its historic median.

Industrial order volumes The picture for order volume is volatility by month; however, on a sequential timeline from 12-months to six-months to three-months, order volume is accelerating. Domestic order volume is accelerating at an extremely rapid rate with orders at 23.8% year-over-year, a six-month growth rate of 43.9%, and a three-month growth rate of 116.4% annualized. Foreign orders also experience ongoing acceleration but to a much less extent, running from 4.5% over 12 months, to a 12.9% annual rate over six months, up to an 18.4% annualized pace over three months.

QTD and % of cycle highlights: Not surprisingly the orders growth rate is at a cycle high for domestic orders; the quarter-to-date total orders and domestic order growth are running at extremely strong rates. Foreign orders growth is at a negative 4.8% annualized for the first month in the new quarter.

Rankings: The ranking of the year-over-year growth rates finds total order volume at a 91.9% standing, domestic orders at a 99.3% standing, and foreign orders at a 62.1% standing, all of them above their historic medians by a wide margin.

Memo: Unemployment For comparison, we include the unemployment rate at the bottom of this table, and we see that Swedish unemployment continues to hover at an exceptionally high level. Ranked on data back to January 2021, the unemployment rate is at its top 2%. In fact, the October unemployment rate is the sixth highest monthly rate on this timeline. Despite what appears to be solid and even strong performance by the industrial sector, Swedish unemployment continues to linger at a level that is historically high for Sweden.

USA| Dec 09 2025

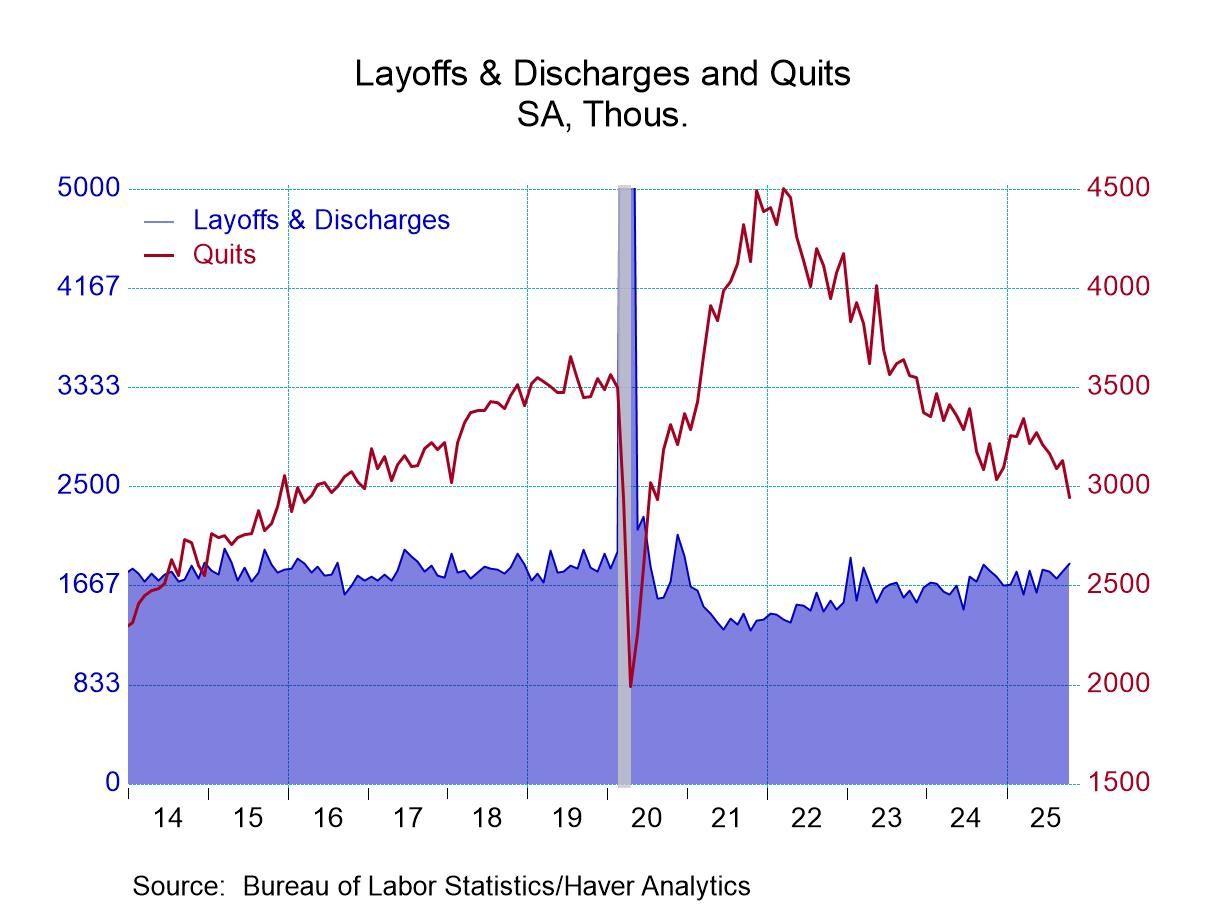

USA| Dec 09 2025U.S. JOLTS—Openings Rise Slightly; Hiring Declines in October

- Minimal rise in job openings follows sharp September increase.

- Sizable hiring decline reverses earlier increase.

- Separations fall sharply as quits plunge and layoffs rise.

by:Tom Moeller

|in:Economy in Brief

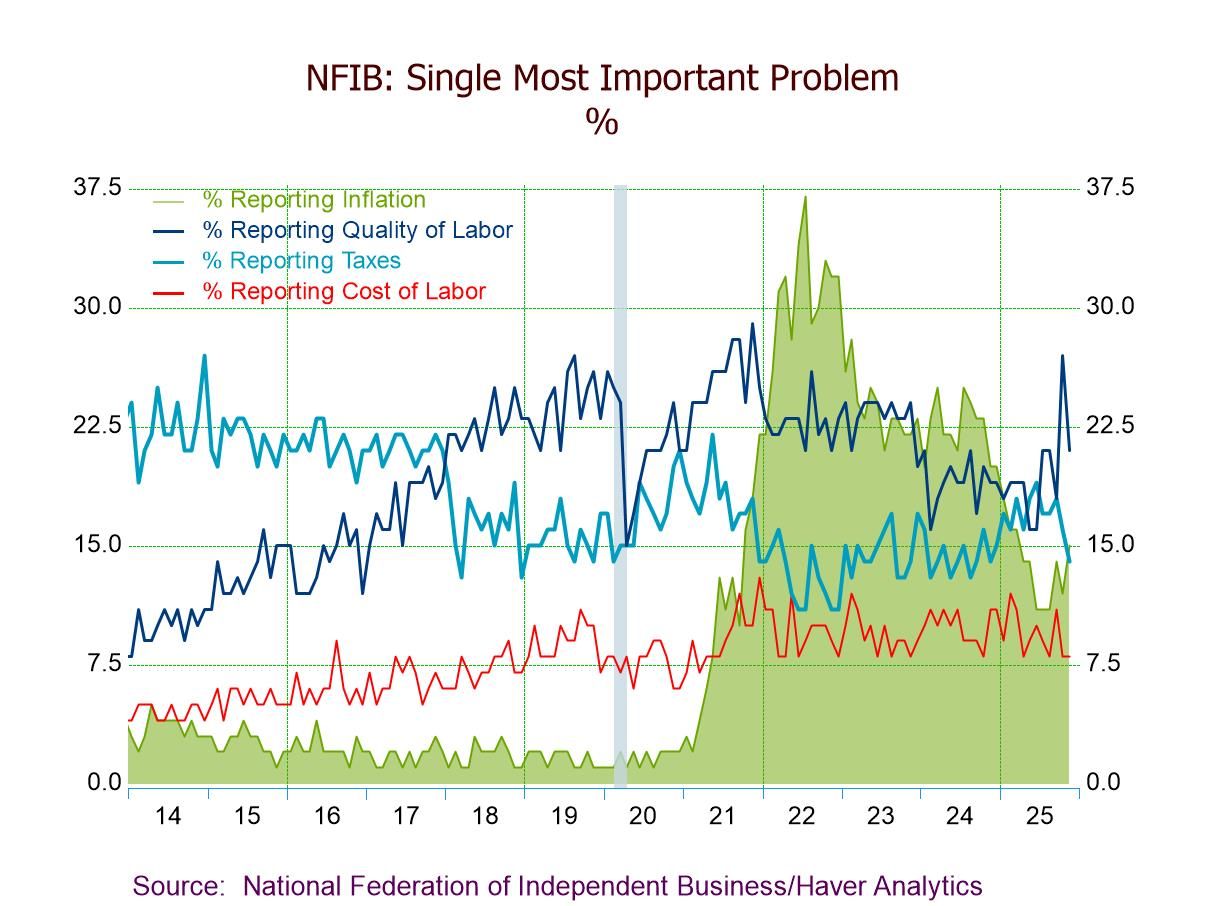

- NFIB Small Business Optimism Idx up 0.8 pts. to 99.0 in Nov., driven by stronger real sales expectations.

- Uncertainty Idx up 3 pts. to 91, reflecting uncertainty about CapEx plans.

- Expectations for economy down 5 pts. to a 7-month-low 15%.

- Expected real sales up 9 pts. to 15%, highest since Jan. ’25.

- Plans to expand business unchanged at 13%.

- Firms raising avg. selling prices up 13 pts. to 34%, highest since March ’23 and largest m/m increase on record.

- Quality of labor (21%), inflation (15%), and taxes (14%) are the top three business concerns.

USA| Dec 09 2025

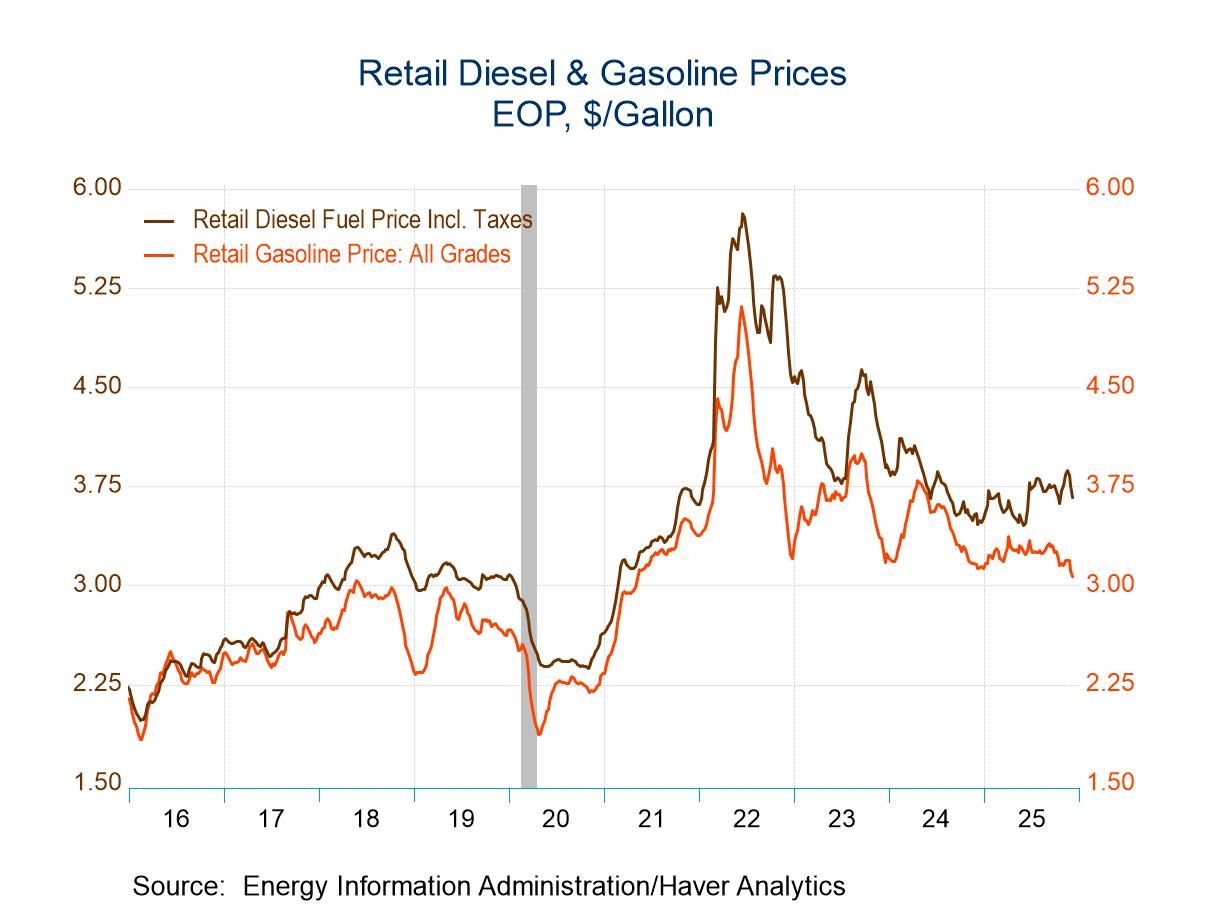

USA| Dec 09 2025U.S. Energy Prices Remain Mixed in Latest Week

- Gasoline prices fall sharply to four-year low.

- Crude oil prices reverse prior week’s decline.

- Natural gas prices move to highest level since February.

- Gasoline demand falls sharply y/y.

by:Tom Moeller

|in:Economy in Brief

Japan| Dec 09 2025

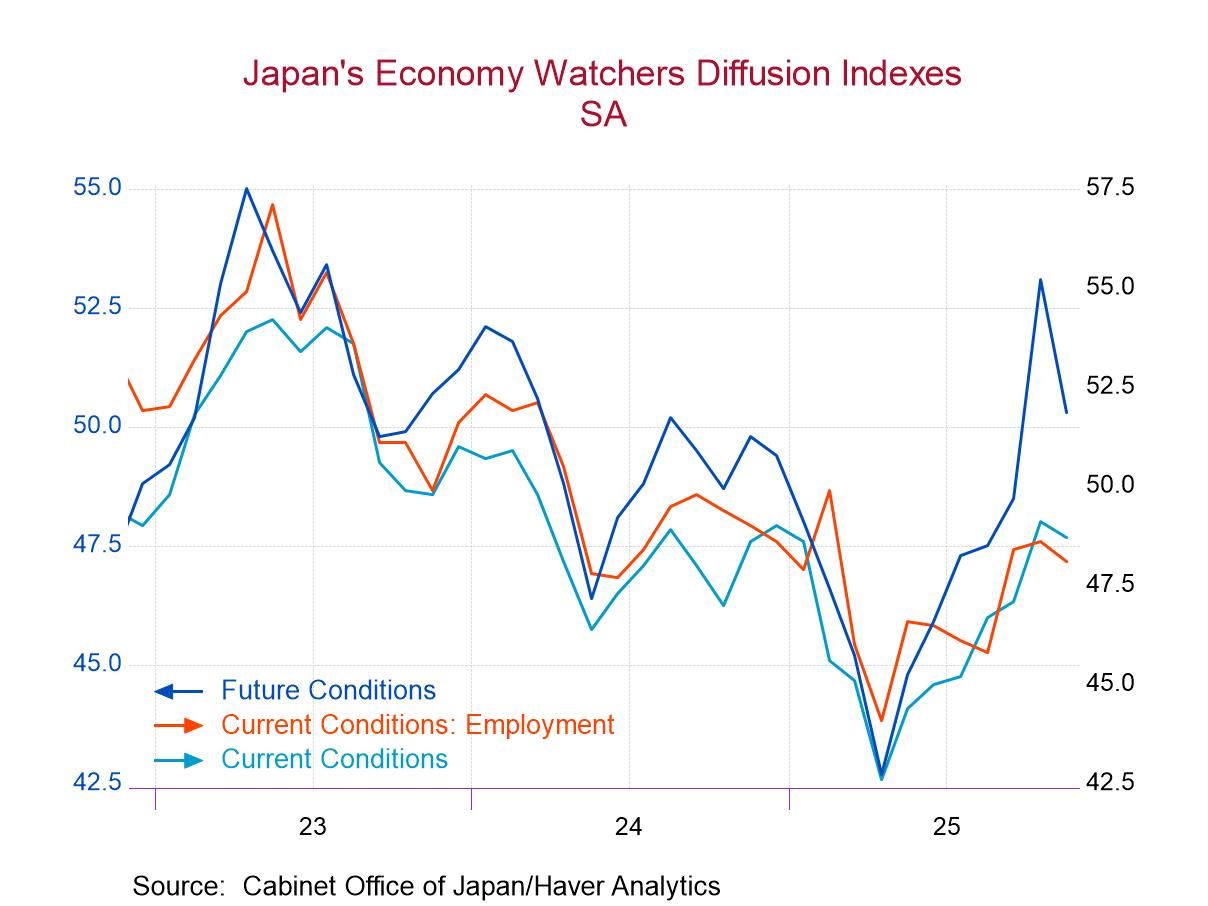

Japan| Dec 09 2025Japan’s Economy Watchers Index Backs Off

Japan's economy watchers index stepped back in November after making some strong strides in October. But the current index and the future index retained stronger values in November than in September even with the backtracking compared to October so that the October improvement actually continues to hold merit. However, there is no follow-through on the October gain.

In November, the current index declined in the headline as well as in six components, with only three components showing improvement month-to-month. The three showing improvement were retailing, services, and nonmanufacturers.

Over three months and point-to-point comparison, the headline improves and seven of nine components improve. Over six months, the headline improves and 8 of 9 components improve. However over 12 months, the headline barely ticks higher and only three components improve compared to 12 months ago.

The queue standing for the current index headline is that 60.9%, leaving it above its historic median. All the components have readings above their 50th percentile except for eating and drinking establishments, housing, manufacturing, and employment. Unfortunately, the employment standing at 26.9% is the weakest of the lot. And despite the breath and other categories, that's concerning.

The future index in November showed month-to-month declines across the board for the headline as well as for all of the components. In October there were increases across the board for the headline and all components while in September there were increases in the headline and all components except two with the lagging components being services and employment. Over three months the future headline increases and all the components increase except for housing. Over six months the future index increases and all the components increase. Over 12 months the future headline increases and all the components improve except for housing, manufacturers, and employment. The standing for the future index in November is at its 68.8 percentile and all the components have standings above their 50th percentile except housing and employment. All the components that have standings above the 50th percentile have standings that are pretty much at the 60th percentile or higher except for manufacturing with a rating of 55.7 percentile.

These findings show that both the current and the future indexes are relatively strong with solid breadth. However, there's even stronger readings and breadth across the future index than for the current index. While the current index and the future index have stepped down relative to October, both show solid and strong momentum over three and six months; however, over 12 months the future index shows better momentum than the current index. This is interesting because Japan has recently installed a new Prime Minister and the Bank of Japan is being looked at more closely; it is beginning to more seriously consider rate hikes as inflation looks to be a more entrenched problem that the central bank is getting ready to turn its attention to.

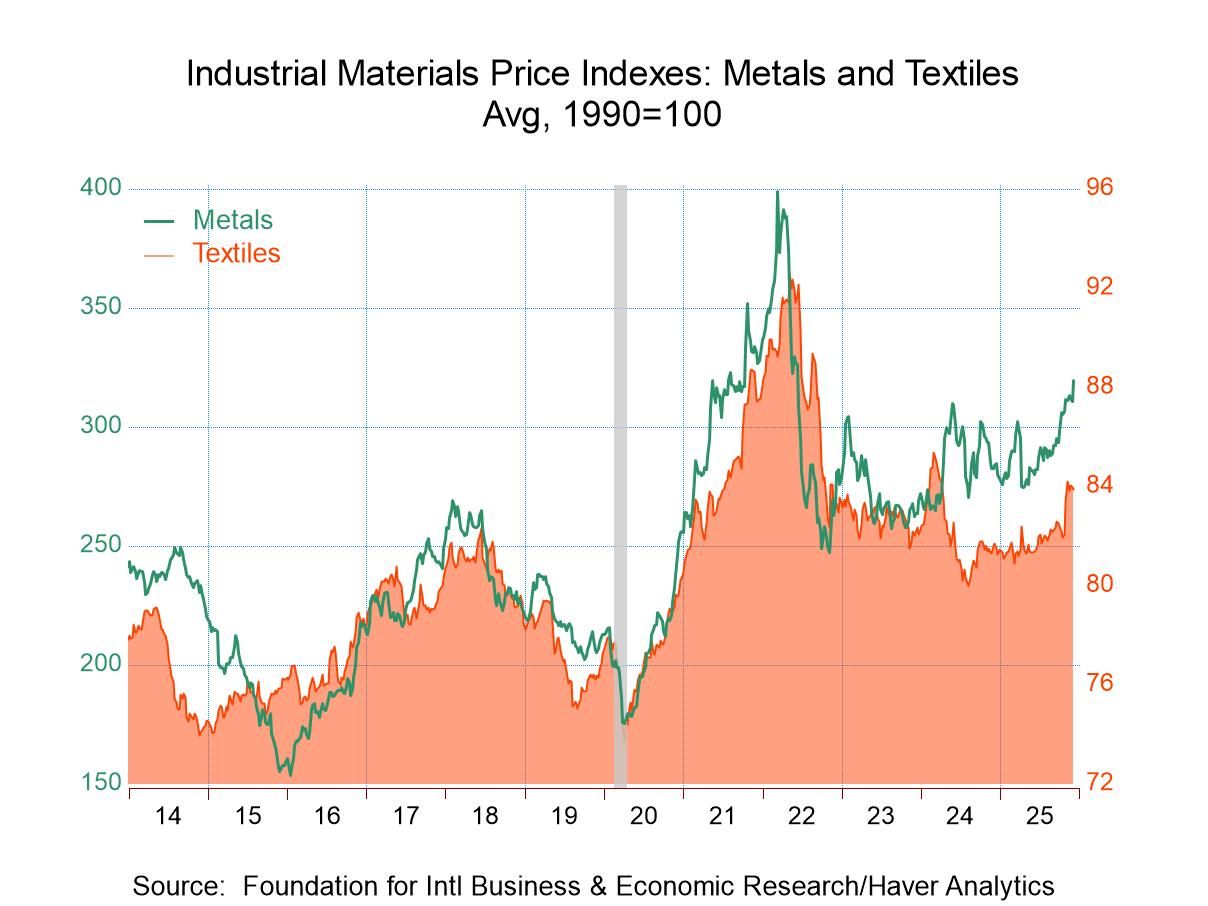

- Higher metals prices lead upturn.

- Crude oil & framing lumber prices also rise.

- Textile prices ease.

by:Tom Moeller

|in:Economy in Brief

- of2726Go to 46 page