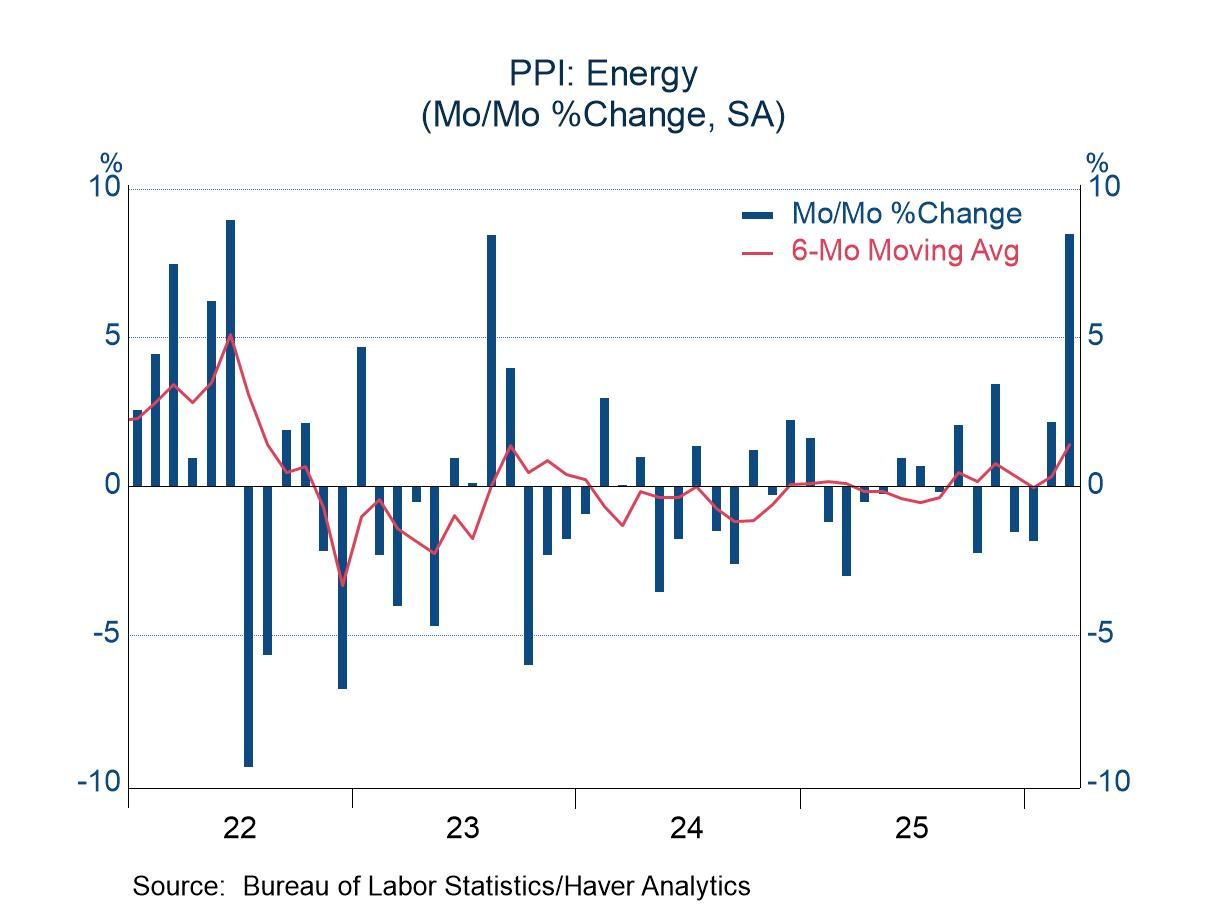

- Energy prices surged in March, but most other items showed modest changes.

- Tame readings were a relief from hints of upward pressure in prior months.

USA| Apr 14 2026

USA| Apr 14 2026March PPI: Tame Excluding Energy

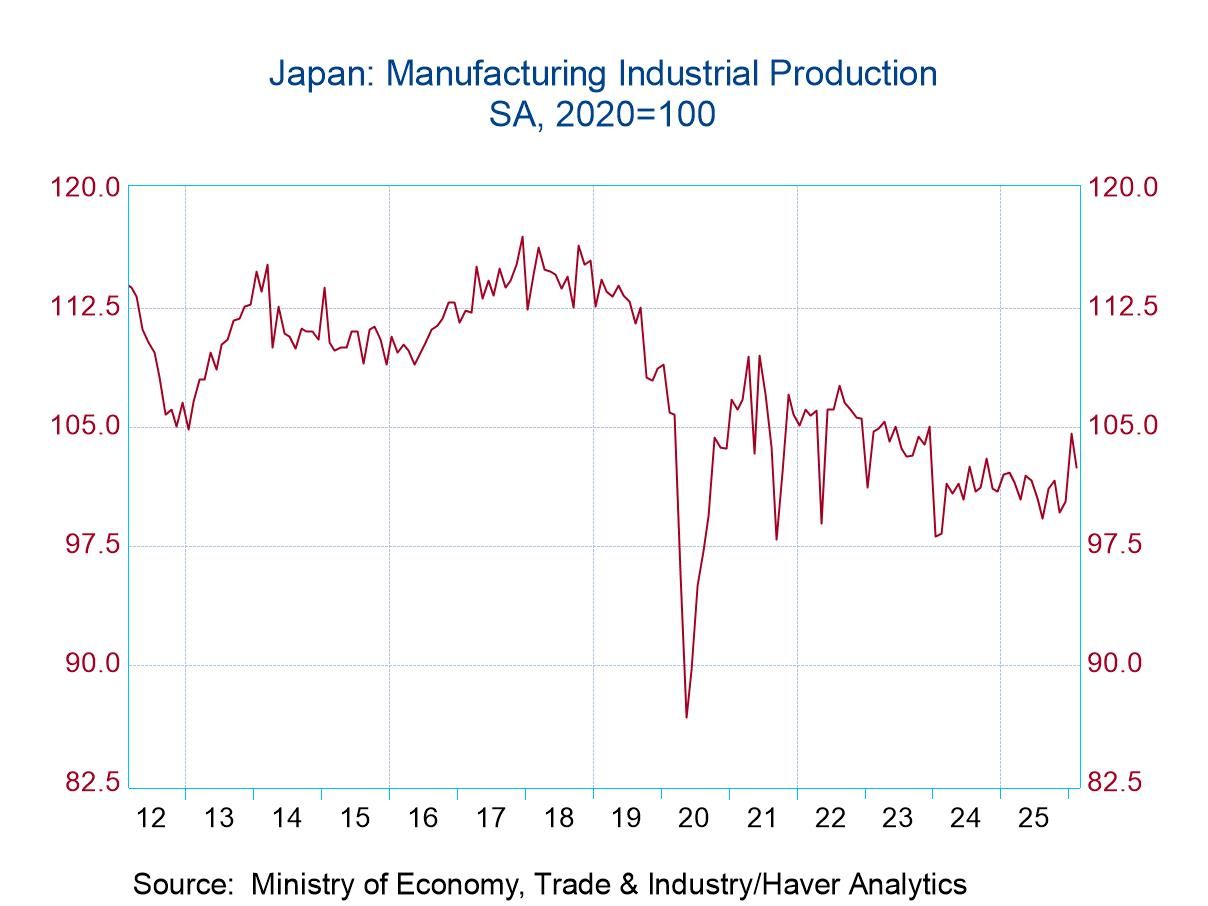

Japan| Apr 14 2026

Japan| Apr 14 2026Japan’s IP: A Step Back in February

Japanese industrial production in February declined by 1.1%, led by a 2.1% drop in manufacturing output. By sector, consumer goods output fell by 0.3%, intermediate goods output fell by 2.1%, while investment goods output dropped by a strong 2.5%, all on a month-to-month basis. Mining sector output fell by 1.5% in February, while utilities output fell by 3.8%.

Sequentially, however, Japanese output had been accelerating, up by 0.1% over 12 months, at a 4.5% annual rate over six months, and at a 7% annual rate over three months.

Manufacturing Manufacturing output is up at 0.3% over 12 months, at a 6.6% annual rate over six months, and by 11.7% annualized over three months.

Within manufacturing, consumer goods output is expanding at a strengthening pace, rising by 0.8% over 12 months, at a 4.8% annual rate over six months, and then at a 10.8% annual rate over three months. Intermediate goods output is flat over 12 months, rising at a 2.9% annual rate over six months, and at a 6.2% annual rate over three months. Investment goods output is up at a 7% annual rate over 12 months, at a 5.2% annual rate over six months, and at a 6% annual rate over three months. However, mining output is down year-over-year; output changes get progressively worse from 12 months to three months. Utilities show a 4.8% decline over 12 months, decline by 3.2% at an annual rate over six months, and then fall at a 4.7% annual rate drop over three months. Mining and utilities sectors are experiencing more in the way of contracting effects.

Quarter-to-date Reported on a quarter-to-date basis (two months into Q1), total industry output is up at a 7.3% annual rate, with manufacturing up at a 15.2% annual rate on the same basis. For sectors, however, the strength is in consumer goods and investment goods where output is increasing at an 11.9% annual rate in the quarter; intermediate goods output is up at a 9.3% annual rate quarter-to-date. Mining output shows a decline at an annual rate in the quarter-to-date, while utilities output posts an increase.

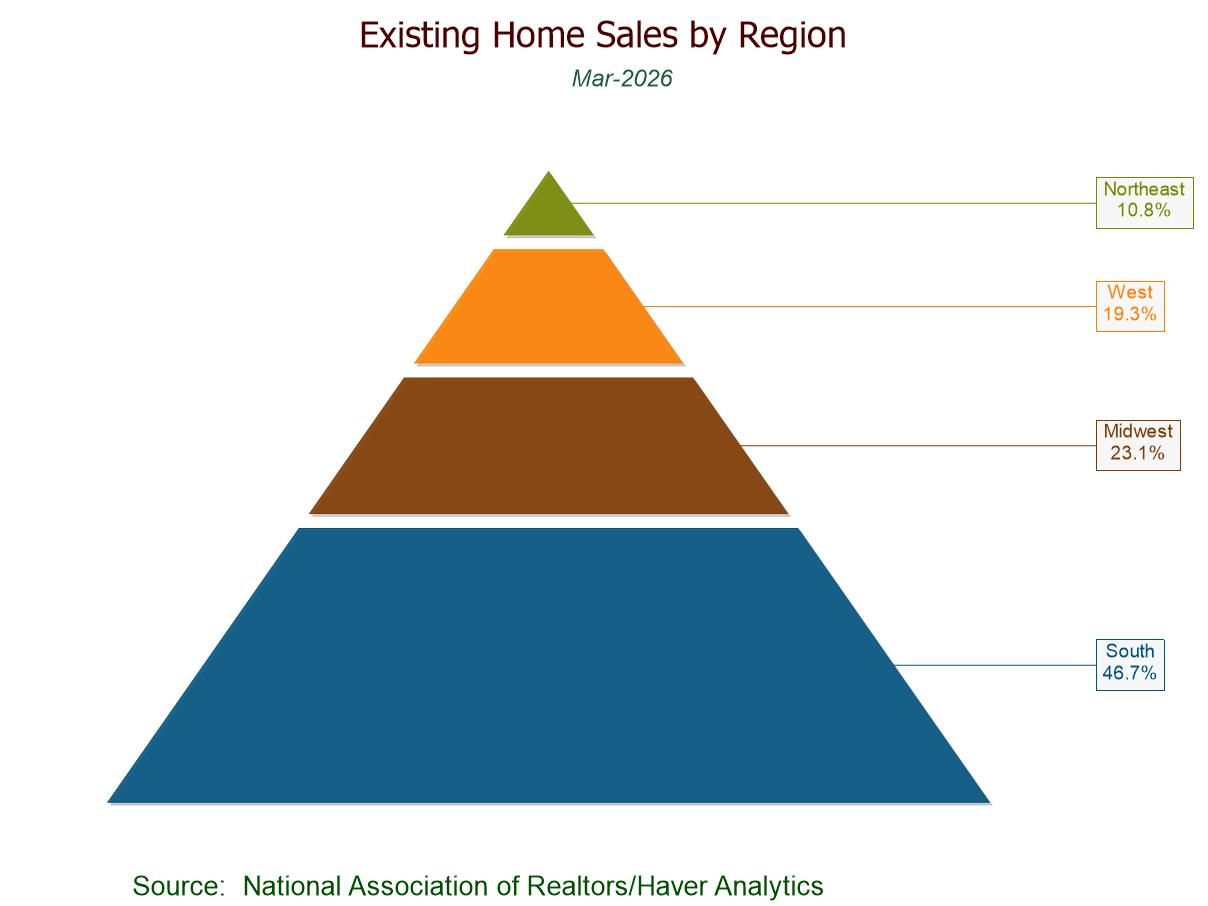

USA| Apr 13 2026

USA| Apr 13 2026U.S. Existing Home Sales Drop in March to a Nine-Month Low

- March sales -3.6% m/m to lower-than-expected 3.98 mil.; -1.0% y/y, fifth straight y/y decrease.

- Broad-based regional m/m declines: Northeast (-8.5%), Midwest (-4.2%), South (-3.1%), West (-1.3%); y/y sales up in the South and West but down in the Northeast and Midwest.

- Median sales price +2.7% (+1.4% y/y) to $408,800, highest since November.

- Unsold inventory +3.0% (+2.3% y/y) to four-month-high 1.36 mil. units; 4.1 months' supply.

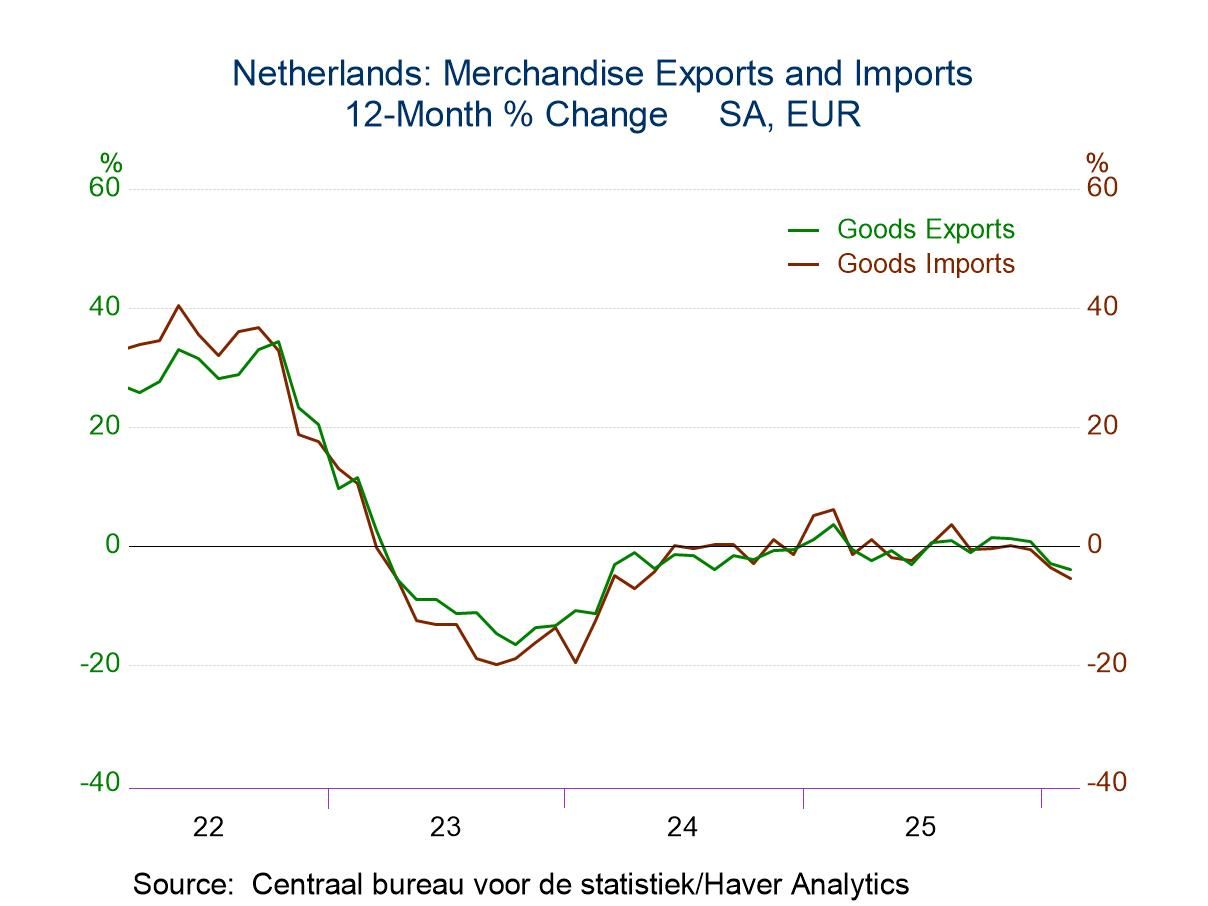

Netherlands| Apr 13 2026

Netherlands| Apr 13 2026Dutch Trade Trends Improve Goods Balance—for Now

As the chart makes clear, Dutch exports and imports are driven by very complementary forces and tend to track one another closely. Both flows boomed when COVID ended, slowed to a contraction in 2023, and then recovered to maintain steady levels (growth rates that hugged a zero-percent growth rate) from mid-2024 to late-2025. Recently, exports and imports have begun to weaken, with both flows showing contraction over 12 months. Goods imports are falling at a 5.5% pace as exports are falling at a 4% pace.

As for intra-year trends, the sequential growth rates show exports have transitioned into a progressively more contractive mode, while imports have declined over 12 months, six months, and three months, but without a clear signal on whether the trend is getting better or worse.

Of course, the trade flow depends on price trends and economic trends; both are under strain and uncertainty.

Asia| Apr 13 2026

Asia| Apr 13 2026Economic Letter from Asia: A Shifting Consensus

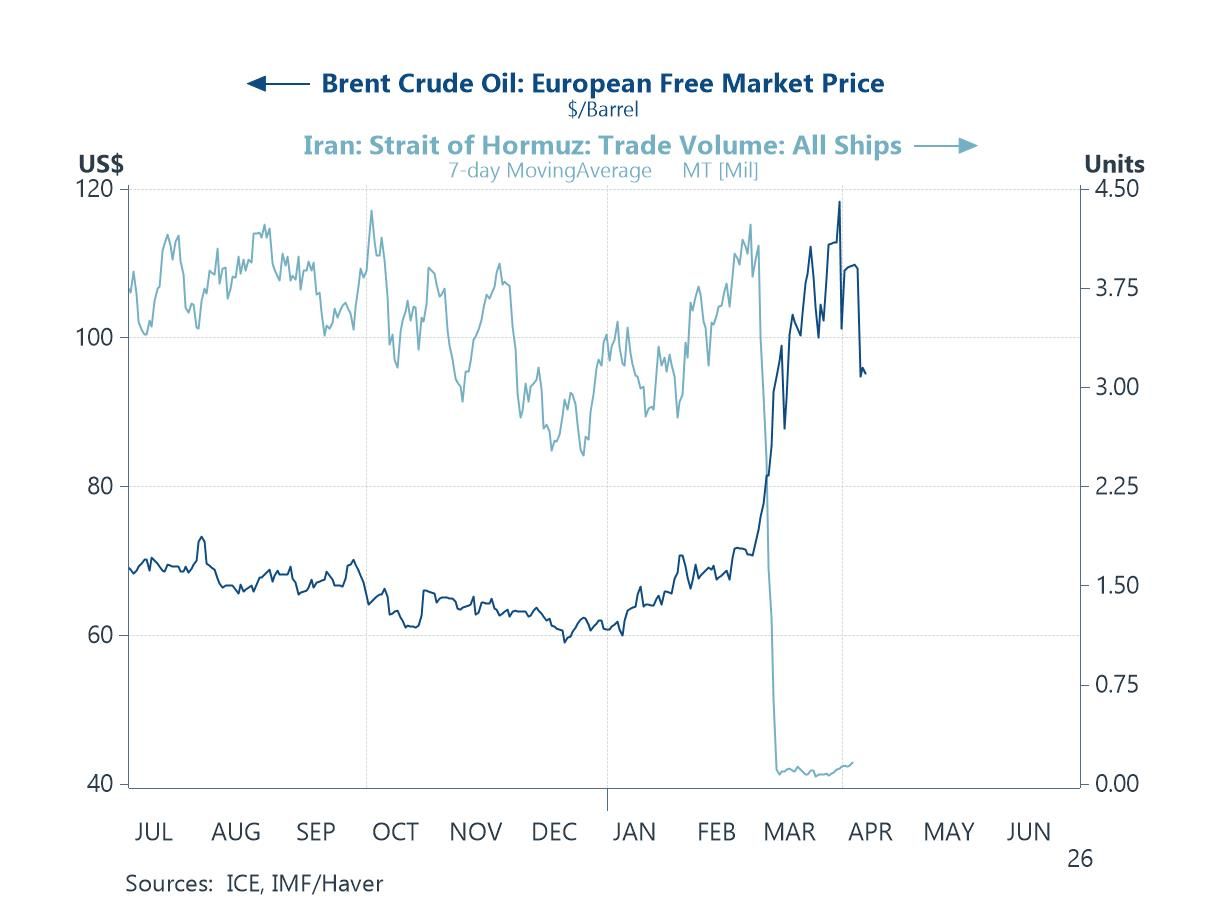

In this week’s Letter, we continue to track developments in the Middle East and their implications for Asia. While the recent US–Iran ceasefire initially provided some relief to markets, subsequent complications have kept uncertainty elevated, with no conclusive resumption of trade flows yet through the Strait of Hormuz (chart 1)—flows that are critical to restoring the global energy system to more normal conditions.

Overall, our Blue Chip Economic Indicators panellists have broadly downgraded growth expectations for Asia this year, with the exceptions of China and Taiwan, while inflation forecasts have been revised higher across the board (chart 2). That said, the growth and inflation impact from the conflict are largely viewed as transitory, with most panellists expecting them to last between six and twelve months (chart 3). Nonetheless, central banks in the region appear increasingly reluctant to ease policy further. This is evident in the latest round of decisions, where India, South Korea, and New Zealand all held policy rates steady (chart 4), citing heightened uncertainty stemming from the ongoing conflict.

While inflationary pressures are beginning to build more broadly across the region, China had already been experiencing a pickup in recent months (chart 5). This has been supported by easing producer price deflation and improving industrial profits, alongside policy efforts to curb excessive price competition among producers. Attention now turns to China’s upcoming Q1 GDP release and the full slate of monthly data due later this week (chart 6).

Middle east conflict developments Crude oil prices fell sharply earlier last week following news of a temporary US–Iran ceasefire. That said, the geopolitical backdrop remains highly fragile, as reflected in continued rhetoric from both sides, alongside the US announcement of a naval blockade over the strait after talks failed to yield an agreement. Compounding this, Iran has indicated that it cannot fully reopen the strait, citing uncertainty over the location of sea mines it had previously laid—further complicating any swift normalization of oil flows. Even prior to these latest developments, IMF-tracked shipping volumes had only begun to show tentative signs of recovery and remain well below pre-escalation levels. As such, while the ceasefire provides a welcome reprieve, meaningful economic relief will hinge on a sustained restoration of oil flows—crucially without additional frictions or costs that could impair global trade. Until then, crude prices are likely to remain elevated, albeit possibly off recent highs, weighing on growth while sustaining inflationary pressures. In Asia, where many economies are heavily reliant on oil imports, the region is likely to bear a disproportionate share of these effects.

USA| Apr 10 2026

USA| Apr 10 2026March CPI: Pressure in the Energy Sector (as Expected); Tame Elsewhere (Surprisingly)

- Gasoline prices drove the energy component higher; electricity prices also contributed.

- Food prices provided a surprise by posting a fractional decline.

- Core prices rose less than expected; both goods and services components were contained.

- Factory orders virtually unchanged (+3.7% y/y) in Feb. for second straight month; still 7.6% above the Jan. ’24 low.

- Durable goods orders (-1.3%), fourth m/m fall in five mths.; nondurable goods orders (+1.5%), largest of three successive m/m gains; shipments (+1.4%), fourth m/m rise in five mths.

- Transportation orders -5.3% m/m, led by a 28.6% plunge in nondefense aircraft orders.

- Unfilled orders +0.1%, smallest of seven straight m/m increases.

- Inventories +0.1%, holding within a narrow 0.1%-0.2% range for four consecutive mths.

Global| Apr 09 2026

Global| Apr 09 2026Charts of the Week: From Oil Shock to Policy Dilemma

Amid further tentative signs of de-escalation—most notably President Trump’s decision on April 7th to step back from further escalation—financial markets have stabilised somewhat, but the macroeconomic implications of the Middle East crisis remain highly uncertain. As our charts show, the global economy entered this shock from a position of relative strength, with positive growth surprises and easing inflation pressures still evident in the data (chart 1). However, that benign backdrop now looks vulnerable. Central banks are already reassessing the outlook, with expectations for policy easing being pared back (chart 2) and a growing consensus that any response to persistent energy-driven inflation will likely involve delaying cuts rather than tightening aggressively—albeit with significant regional divergence (chart 3). Financial markets, for their part, are not yet signalling a loss of inflation control, but the rise in real yields suggests increasing concern around the broader policy mix, particularly fiscal pressures (chart 4). Finally, the adjustment to the shock is unlikely to be uniform. Structural differences in domestic energy capacity are already driving wide divergences in electricity prices, leaving more import-dependent economies exposed to higher costs and sharper trade-offs between growth and inflation (charts 5 and 6). Taken together, the message is clear: even if geopolitical tensions ease, the economic aftershocks are likely to be uneven, persistent and increasingly shaped by structural constraints.

by:Andrew Cates

|in:Economy in Brief

- of2725Go to 17 page