- Initial claims increase 1,000 to 203,000.

- Continued weeks claimed fell again to a new 52-year low.

- Insured unemployment rate remained at record low of 1.0%.

USA| May 12 2022

USA| May 12 2022U.S. Unemployment Claims Edge Upward

USA| May 12 2022

USA| May 12 2022U.S. Producer Price Inflation Moderates in April

- Services prices hold steady.

- Core goods prices remain strong.

- Energy & food prices soar again.

by:Tom Moeller

|in:Economy in Brief

USA| May 12 2022

USA| May 12 2022U.S. Housing Affordability Plunges in March

- Home prices & mortgage rates continue to surge.

- Payment as a percent of income increases almost two percentage points.

by:Tom Moeller

|in:Economy in Brief

USA| May 11 2022

USA| May 11 2022U.S. Consumer Price Increase Slows During April

Pricing power overall at the retail level moderated in April, but the details show evidence of continued pricing strength. The Consumer Price Index rose by 0.3% last month as expected in the Action Economics Forecast Survey, following an unrevised 1.2% March rise. The 8.3% y/y gain was below the 8.5% y/y pace set in March and stood a hair under the previous peak 8.4% y/y set in January 1982.

Prices excluding food & energy rose an expected 0.6% last month, doubling the March rise. It was the strongest increase in three months. The 6.2% y/y gain jumped from a recent low of 1.3% y/y set in February 2021.

A 2.7% decline (+30.3% y/y) in energy prices led the moderation in pricing strength overall during April, following an 11.0% March increase. Gasoline prices fell 6.1% (+43.6% y/y) after reaching a record high in March. Fuel oil prices, however, surged 2.7% (80.5% y/y). Natural gas prices strengthened 3.1% (22.7% y/y) while the cost of electricity rose 0.7% (11.0% y/y).

Food prices remained strong last month, rising 0.9% (9.4% y/y) which was similar to the increases in each of the prior three months. Meat, poultry, fish & egg prices rose 1.4% (14.3% y/y). Cereal & bakery product prices also were strong and gained 1.1% (10.3% y/y). These increases were offset by a 0.3% decline (+7.8% y/y) in fruit & vegetable prices.

Services prices rose 0.7%. The 4.9% y/y gain compared to 1.3% y/y at the start of 2021. The cost of public transportation surged 12.1% (21.8% y/y). Shelter costs increased 0.5% (5.1% y/y). The owners' equivalent rent of primary residences gained 0.5% (4.8% y/y) as rents of primary residences rose 0.6% (4.8% y/y). The cost of medical care services increased 0.5% (3.5% y/y). Recreation services prices gained 0.4% (4.4% y/y) while education prices edged 0.2% higher (1.7% y/y).

Goods prices excluding food & energy rose 0.2% (9.7% y/y) in April after a 0.4% March decline. Price changes within categories were mixed. Used car & truck prices weakened 0.4% (+22.7% y/y), the third straight monthly decline, but new vehicle prices rose 1.1% (13.2% y/y). Education & communication product prices fell 2.6% (-4.0% y/y) as recreation product prices gained 0.5% (4.0% y/y). To the upside, home furnishings prices rose 0.5% (10.6% y/y) but household appliance prices fell 0.5% (+7.8% y/y). Apparel prices declined 0.8% (+5.4% y/y).

The Consumer Price Index data can be found in Haver's USECON database with additional detail in CPIDATA. The Action Economics survey figure is in the AS1REPNA database.

by:Tom Moeller

|in:Economy in Brief

USA| May 11 2022

USA| May 11 2022U.S. Mortgage Applications Rose for Second Week

- Total applications increased 2.0%.

- Loans to purchase a house rose 4.5% while refinance loans fell 2.0%.

- Mortgage interest rates resumed their uptrend.

by:Sandy Batten

|in:Economy in Brief

USA| May 10 2022

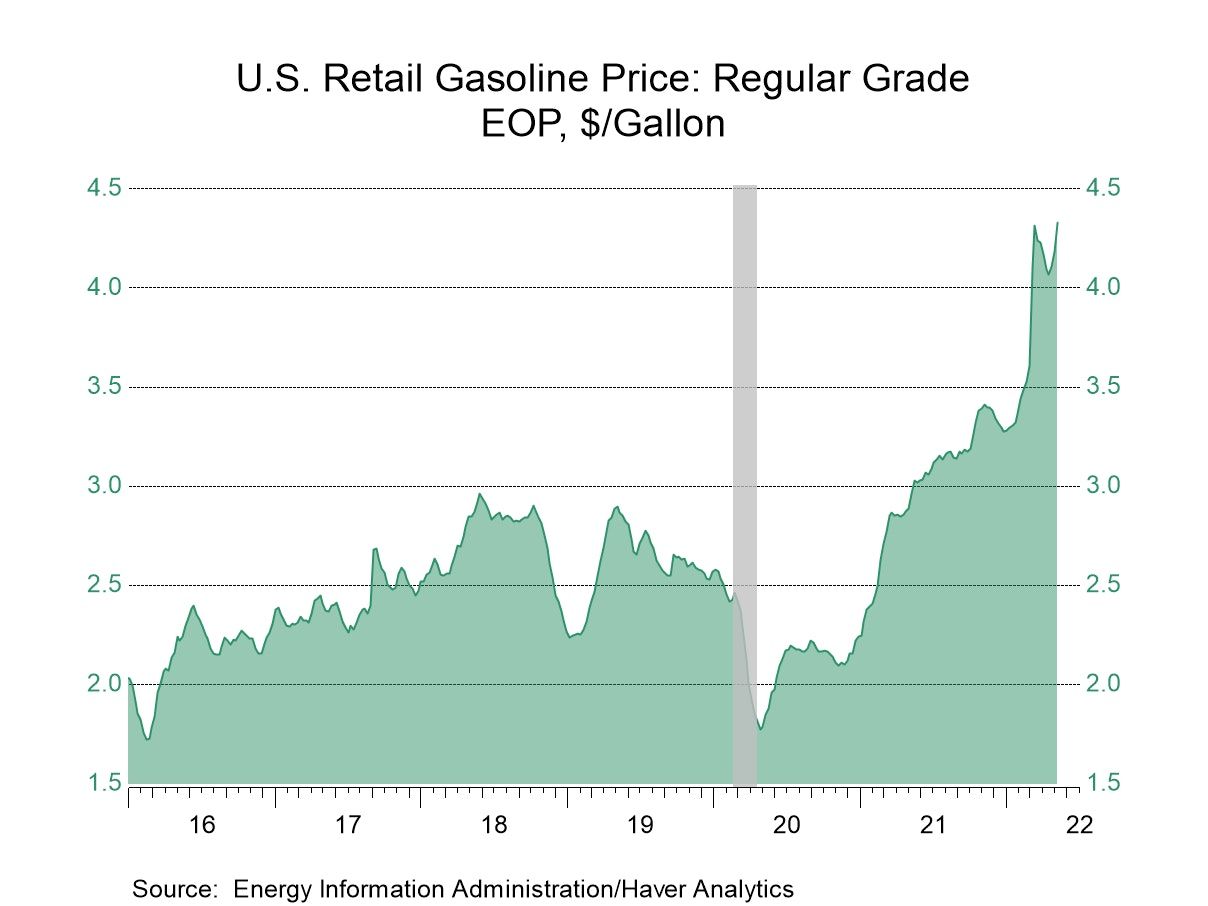

USA| May 10 2022U.S. Energy Prices Strengthen

- Gasoline prices jump to record high.

- Crude oil prices increase sharply.

- Natural gas prices rise to highest level since February 2021.

by:Tom Moeller

|in:Economy in Brief

Germany| May 10 2022

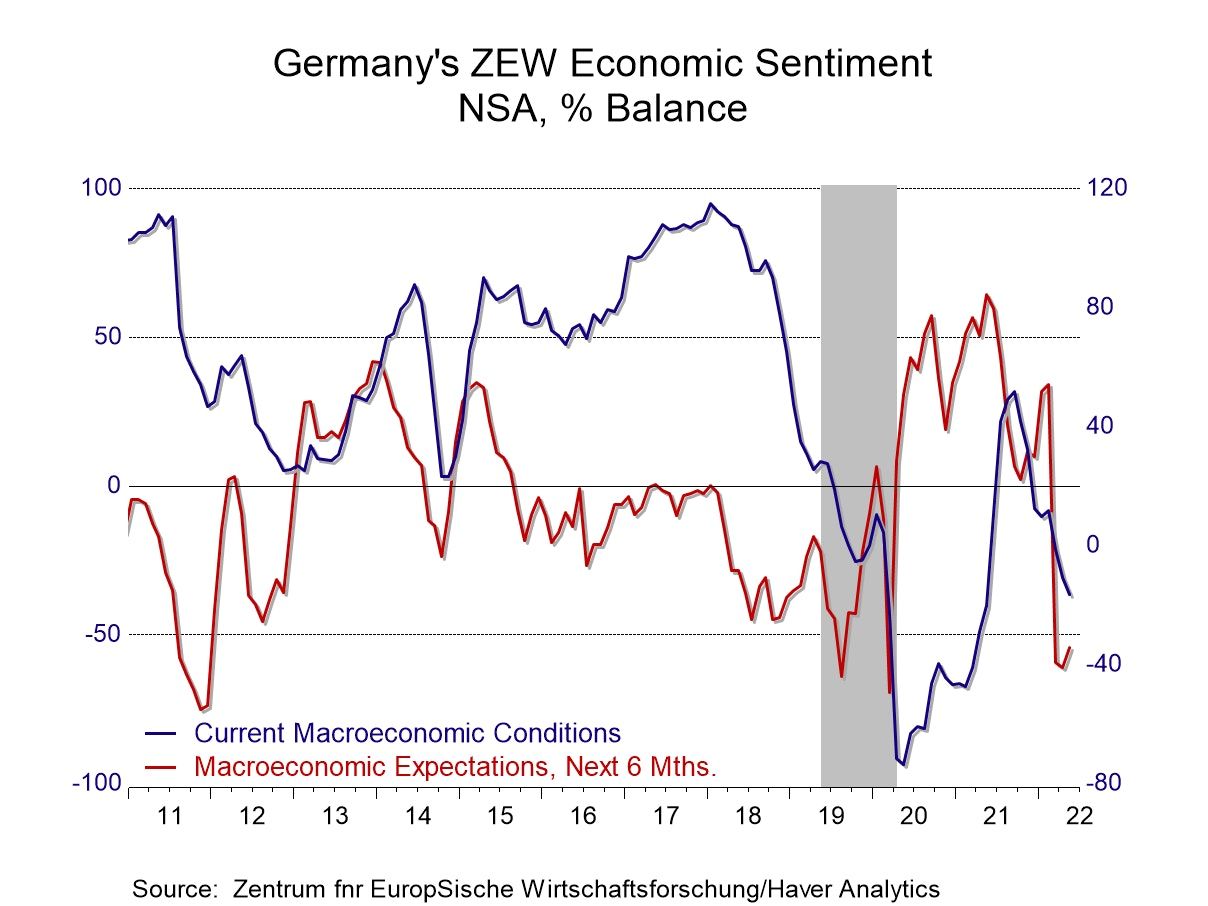

Germany| May 10 2022ZEW Survey: The Death of Optimism

The ZEW Economic situation index for May fell to -35 for the euro area from -28.5 in April. The reading for Germany fell to -36.5 in May from -30.8 in April. The reading for the United States fell to 24.3 in May from 27.9 in April (these are raw diffusion scores; the table below presents percentile standings for these values). These observations are substantially lower over three months. They already had weakened over six months and their readings over 12 months already were poor. The simple summary is that very bad conditions meet poor expectations and slipping momentum for both.

Macroeconomic expectations for Germany and the U.S. continue to give deep negative readings. For Germany, the diffusion reading (not in the table) improves slightly on the month to -34.3 in May from -41.0 in April. The U.S. diffusion reading slips month-to-month to -28.8 from -24.7. However, conditions in Germany measured on a relative yardstick are not better than they are in the United States. The queue standing of the diffusion readings show the German standing in the bottom 8.5% when ranked among all German readings back to late-1991. U.S. indexes stands in the 13.1 percentile of its own data queue, slightly better, but still a very weak reading, on that same timeline. There is nothing to cheer about.

Reality check! There's nothing in this report that is reassuring or good news causing me to put the headline on this report as ‘The death of Optimism.’ It's not that anything so dramatically bad has happened this month; it's that what has been happening in this report has continued to happen and it's important to acknowledge that as well as the prospect for it to continue. The economic and geopolitical conditions that have caused these readings to come about continue in play and in fact the super support mechanisms that countries have used ranging from fiscal policy to monetary policy have been leaned on so long that these crutches have been bent to configurations that put them beyond usefulness. Fiscal measures to support economic activity have been cut or are being cut. Monetary policy assistance is being reduced and policies of restrictiveness are either in play or in train.

The lingering malaise of virus At the same time, the virus that was responsible for creating the recession and the lockdowns and the panics… continues to circulate albeit in a less fearsome form. Countries continue to make their own peace with the virus. Some, like China, continue to have severe episodic lockdowns; others all but ignore it while health officials keep a wary eye on it. The supply chains that were so disrupted during the pandemic are still disrupted; they're in the process of being fixed, but this process is a long one. Maybe this will be viewed as ‘transitory’ by historians, but not to a real-time policymaker.

Disruptions continue Global trade has been severely disrupted. There continues to be long lines at ports although there is also evidence that this situation is being gradually rectified. Many firms simply went out of business and will never return. Others have undergone severe damage and they are shadows of their former selves. Yet, others are still in business and are trying to adopt new ways of operating given the new realities of a world with a pandemic and people who are concerned- perhaps overly concerned- about the potential for its to return.

The current crisis has its own special sauce At the same time, there is a new ingredient that threatens global prosperity and that is Russia's attack on Ukraine. This attack is not only devastating for the people of Ukraine whose lives have been terminated, whose country is being destroyed, whose cities are being decimated, but there's also an adverse impact to the world from economic activity disrupting the normal flow of commerce that would come out of that region to the world. In addition, there are sanctions on Russia for starting this conflict. Some important trade flows have been lost. Ukrainian wheat shipments to the world have been impeded and halted. Russia is stealing Ukraine’s grain and stealing Ukraine's farm equipment. Russian fertilizer exports to the world have stopped and because of this global agricultural is worse off. Farmers no longer have the fertilizer that they have used in the past to enhance crop yields. The potential for a global food crisis and for much higher food prices is on the table. Yes, the crisis may be on the table, food may not be.

The summary table offers little good news A look at the summary table shows that German and the U.S. economic situations have rankings below their historic medians (below rankings of 50). Economic expectations are below their historic medians and extremely weak, to boot. We see that inflation expectations also have low standings, but that's mostly because inflation is so high forecasters are not expecting inflation to accelerate but rather to decelerate although whether inflation will decelerate to a level that is within central bank target areas anytime soon is simply a matter for speculation. To underscore that, short-term interest rate expectations in the euro area and in the U.S. are in their 90th percentiles, extremely high. Long rate expectations are high, in their 88th percentile for Germany and moderately high, in their 66th percentile for the U.S. For some reason, forecasters living with a reality of extremely high inflation and expecting short rates to move up very strongly do not have much of a long-term rate expectation for the U.S. That's a curious situation and it's not clear what theory or belief it's grounded in. Against this background, stock market expectations are well below their medians at the 2.8 percentile for the euro area, at the 1.9-percentiel mark for Germany and in the bottom 22nd percentile for the United States.

USA| May 10 2022

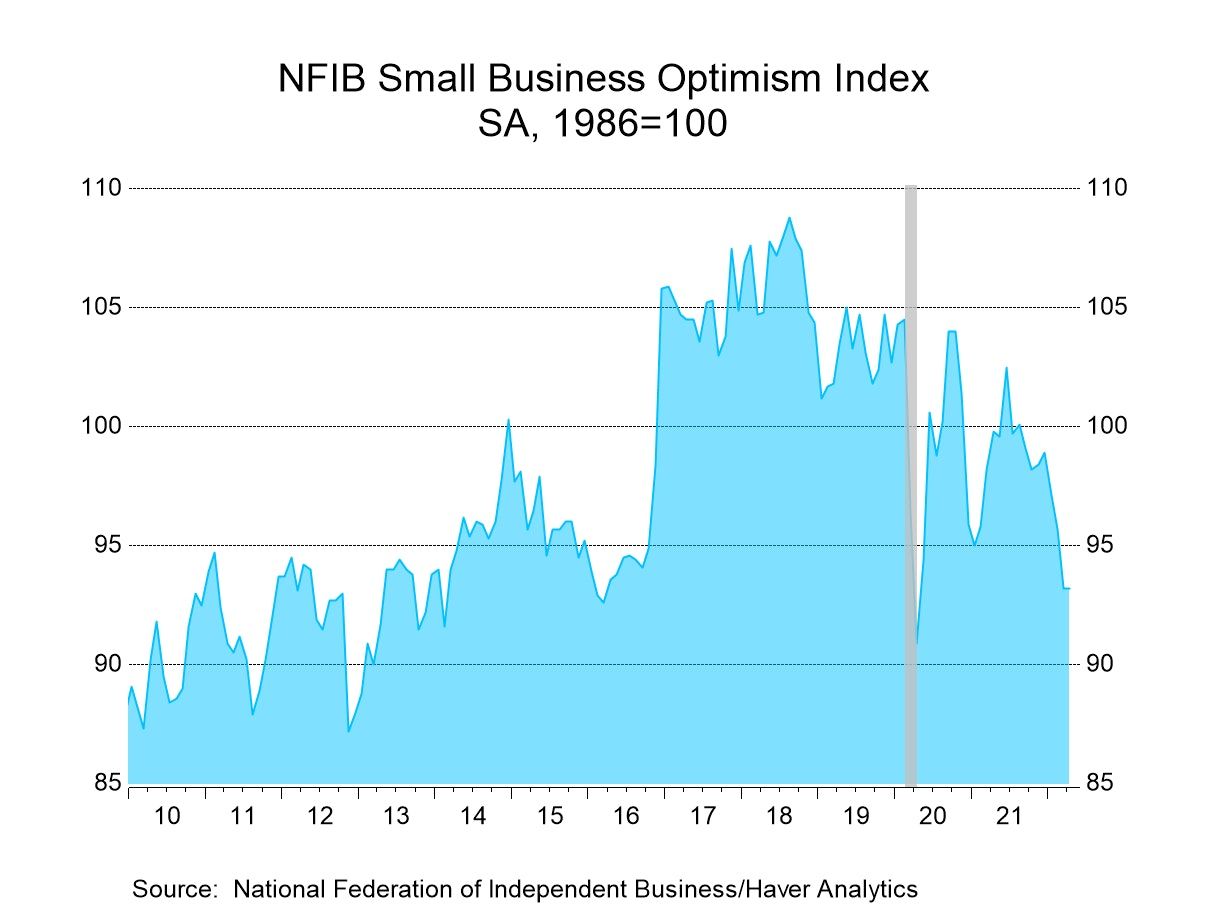

USA| May 10 2022U.S. Small Business Optimism Remains Weak

- Optimism holds at lowest level since April 2020.

- Expectations of better business conditions in next six months fall to another all-time low.

- Pricing power nears record high.

by:Tom Moeller

|in:Economy in Brief

- of102Go to 67 page