It had been a weak housing market recovery anyway, but the National Association of Home Builders reported that their index of housing market activity fell back this month to 14, the lowest level since March 2009. Perhaps this is the [...]

by:Tom Moeller

|in:Economy in Brief

Global| Jul 19 2010

Global| Jul 19 2010EMU Current Account Deficit Widens

The EMU current account deficit widened in May and is fluctuating in a higher deficit zone. Both merchandise exports and imports are accelerating but goods imports are outpacing goods exports in the Zone on all horizons. Services [...]

- Global| Jul 19 2010

New NABE Survey Indicates Pace of Business Recovery Eases But Job Creation Improves

In their latest report, the Nat'l Association for Business Economics indicated that net industry demand increased during 2Q for the fourth consecutive quarter. There was a sign, however, of moderation in the rate of demand's expansion [...]

by:Tom Moeller

|in:Economy in Brief

- Global| Jul 16 2010

U.S. CPI: Broad-Based Declines For Third Straight Month

Broad-based weakness in pricing power continues to accompany moderate U.S. economic growth. The June Consumer Price Index fell 0.1% (+1.1% y/y) for the third consecutive monthly decline. During the first six months of this year prices [...]

by:Tom Moeller

|in:Economy in Brief

- Global| Jul 16 2010

Euro Car Registrations Jump In June But Are Quashed In Quarter

Total car registrations in EU jumped by 9.8% in June. Even so, for the quarter 'sales' are off at a nearly 20% annual rate and the same is true for the three month growth rate. For 2010-Q2 only the UK and Italy have small positive [...]

- Global| Jul 16 2010

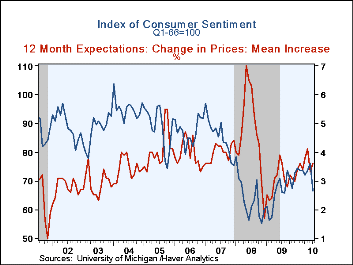

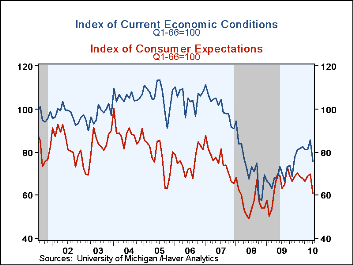

U.S. Consumer Sentiment Falls Sharply

Consumer Sentiment

Consumers aren't upbeat about much these days. As of mid-July,

the University

of Michigan reported that its consumer sentiment measure dropped

sharply from

June to 66.5 which was the lowest reading since last August.

Nevertheless the

index level remained up 20.3% since the low in November 2008. During

the last

ten years there has been an 89% correlation between the level of

sentiment and

the y/y change in real consumer spending.

Consumers aren't upbeat about much these days. As of mid-July,

the University

of Michigan reported that its consumer sentiment measure dropped

sharply from

June to 66.5 which was the lowest reading since last August.

Nevertheless the

index level remained up 20.3% since the low in November 2008. During

the last

ten years there has been an 89% correlation between the level of

sentiment and

the y/y change in real consumer spending.The expectations index dropped sharply m/m but remained up a modest 12.4% from the 2008 low. The readings for expected business conditions during the next year (-5.8% y/y) and expectations for business conditions during the next five years (0.0% y/y) both fell sharply from June. Expectations for personal finances also fell hard from June (-6.4% y/y).

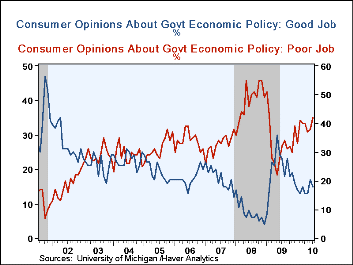

Expected price inflation during the next year ticked higher to 3.6% and remained up from the December 2008 low of 1.7%. Respondents' view of government policy, which may eventually influence economic expectations, retraced the gains of the prior two months and remained down sharply from its high last May. Fifteen percent of respondents thought that a good job was being done by government versus 42% who thought a poor job was being done.

Sentiment about current economic conditions also fell sharply from June to the lowest level since November. The assessment of current personal finances reversed its improvement (7.1% y/y) since February while perceived buying conditions for large household goods, including furniture, refrigerators, stoves & televisions fell hard to the lowest level since November (8.1% y/y).

The Reuters/University of Michigan survey data are not seasonally adjusted. The reading is based on telephone interviews with about 500 households at month-end. The summary indexes are in Haver's USECON database with details in the proprietary UMSCA database.

University of Michigan Mid- July June May June Y/Y 2009 2008 2007 Consumer Sentiment 66.5 76.0 73.6 0.8% 66.3 63.8 85.6 Current Economic Conditions 75.5 85.6 81.0 7.1 69.6 73.7 101.2 Expectations 60.6 69.8 68.8 -4.1 64.1 57.3 75.6 by:Tom Moeller

|in:Economy in Brief

- Global| Jul 16 2010

U.S. CPI: Broad-Based Declines For Third Straight Month

Broad-based weakness in pricing power continues to accompany moderate U.S. economic growth. The June Consumer Price Index fell 0.1% (+1.1% y/y) for the third consecutive monthly decline. During the first six months of this year prices [...]

by:Tom Moeller

|in:Economy in Brief

- Global| Jul 16 2010

U.S. CPI: Broad-Based Declines For Third Straight Month

Broad-based weakness in pricing power continues to accompany moderate U.S. economic growth. The June Consumer Price Index fell 0.1% (+1.1% y/y) for the third consecutive monthly decline. During the first six months of this year prices [...]

by:Tom Moeller

|in:Economy in Brief

- of121Go to 52 page