Industrial output in Norway fell by 1% in May after rising by 0.6 in April and falling by 1.1% in March. The seesaw act for output continues. Over broader horizons, however, output is falling. It falls by 0.1% over 12 months, falls at a 1.1% annual rate over six months, and falls at a 6.2% annual rate over three months, giving us a clear sequential trend toward falling and decelerating output. Utilities output has chaotic trends, as do mining and quarrying; however, manufacturing shows a clear trend toward output acceleration, with a 2.1% output increase over 12 months, a 2.6% annual rate rise over six months, and a 9% annual rate increase over three months.

Manufacturing sectors show consumer goods output increasing in May, also showing secular acceleration from 12 months to six months to three months. Durable goods, however, are the fly in the ointment, with output up 2.2% over 12 months, accelerating over six months, and then dropping at a 20.4% annual rate over three months. However, consumer nondurables show growth and acceleration, with a 12-month gain of 1.8%, rising to a 3.6% annual rate increase over six months and a 10.9% annual rate increase over three months. Intermediate goods output trends return to more difficult times and show declines over 12 months, six months, and three months, but not a clear path of deceleration. Capital goods output is up 5.4% over 12 months and at an 8.5% annual rate over three months, but there is an intervening soft spot with output up at only a 3.4% annual rate over six months.

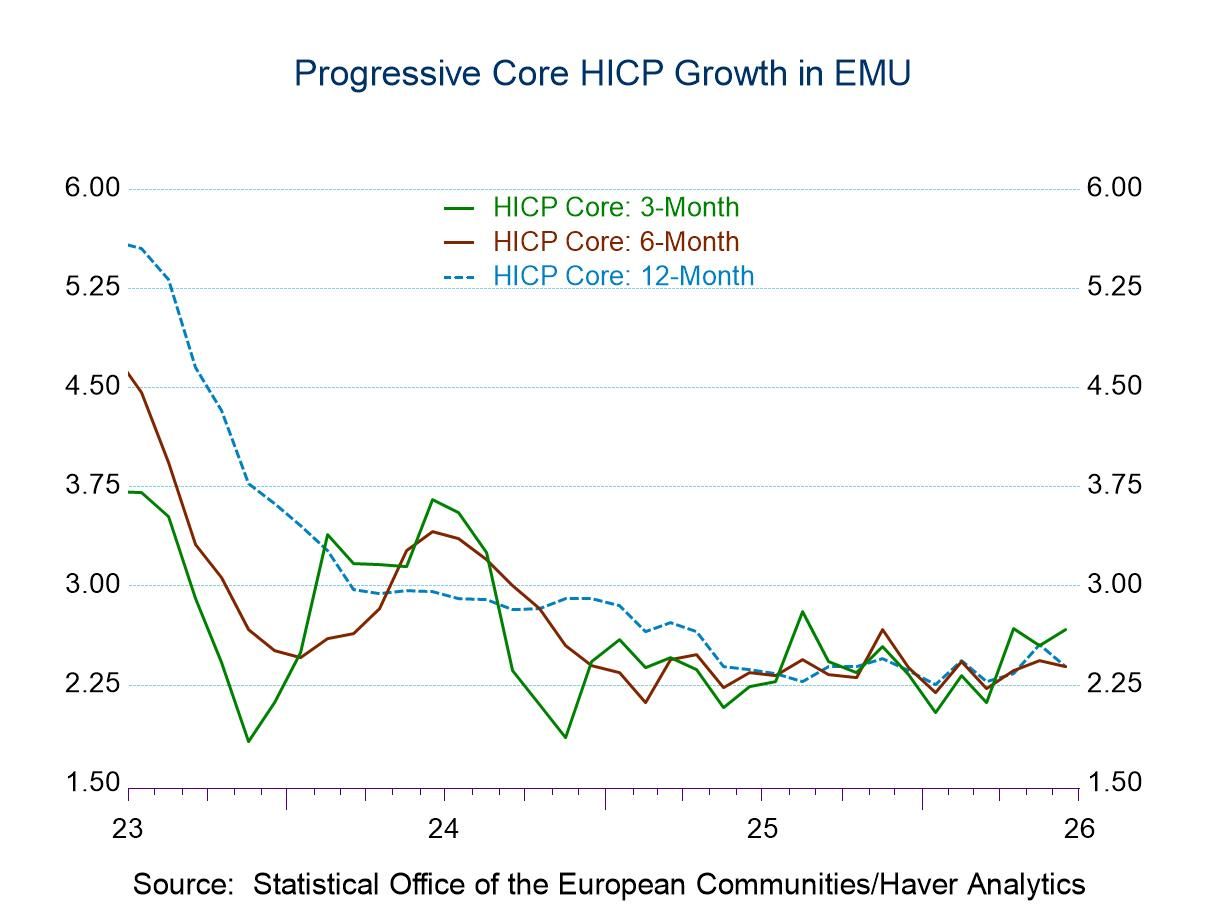

Against this background, inflation in Norway showed solid increases in May, rising by 0.2% overall and by 0.3% for the core HICP. However, sequentially inflation gains 3% over 12 months, rises at a 3.8% annual rate over six months, and then backs down to a 1.2% annual rate over three months. The core HICP is steadier, with a 3.4% gain over 12 months, rising to a 3.8% annual rate over six months, and then backing down to 3.2% at an annual rate over three months. That's a set of growth rates that are more stable than either accelerating or decelerating.

In the quarter-to-date (QTD) basis, industrial production is falling 4.6%; this is two months into the second quarter. On the other hand, manufacturing output is rising QTD at a 4.9% annual rate, with consumer nondurables showing strong positive growth along with intermediate goods output. There is a solid gain of 3.1% at an annual rate from capital goods. The QTD inflation trends remain somewhat mixed, with a weak headline showing a 1.6% annual rate, against a core HICP at a 3.4% annual rate rise, the latter gain being well in step with its sequential results.

The far right-hand column compares industrial production over the broad period from just before COVID (in January 2020) looking at the ratio of the level of output in May 2026 to its index value in January 2020. Remember that IP data are inflation-adjusted, so these are real data. Over this span, industrial production excluding construction is up by approximately 10%, with utilities output up at about 21%, mining and quarrying up about 5%, and manufacturing up a little more than 7%. This is a 5½-year period. Consumer goods output is up by 2.7%, led by consumer nondurables which rise 4.1% on the period and against durable goods output where there is a decline of about 13% on that timeline. Intermediate goods output drops slightly on the timeline by less than half a percentage point, while capital goods output is up at a solid and strong 23% gain. Looking at prices over the same period, the headline HICP is higher by 27% while the core is higher by 24%.

The weakened output shows the stresses and strains of the period, with weak gains in place over the last 5½ years and with the consumer showing considerable wear and tear, leaving consumer goods output lower on balance over this 5½-year span. It hasn't been such a bad time for capital goods, where output rose by 23% over the period. Inflation got out-of-the-box and grew quite strongly. The headline HICP grew by 27% since January 2020, a duration of time during which, sticking to its target, would have implied a gain in the price level of only 11.5%.

Ongoing overshooting

Even now central banks are trying to decide how to come to grips with the inflation pressures from that. Pressures continue to linger and threaten the economies. Of course, there are some new factors in place, but that's the nature of inflation: if it's not one thing, it's something else. And failing to respond to the one thing means that you're going to get hit even worse when it becomes something else. This is the lesson the central banks haven't learned during this period.

Have central banks learned their lesson?

Noting that inflation is over target and then forecasting that it's going to come back down to target over some period ahead puts the inflation performance at risk to whatever happens between now and the end of that period ‘ahead.’ If that forecast isn't perfectly right and if there's something else that disturbs the path of prices, what will happen is that an inflation that is already over the top of the target will push even farther over the top of the target and the dilemma faced by the central bank will become even worse. This is why kicking the can down the road generally is not a very good strategy, but it's one that virtually all the central banks pursued in the wake of COVID. So, will central bankers come to see inflation that is here and now as a here-and-now problem to be addressed here and now, or as a candidate for tomorrow land? The ECB seems to be changing, and the Fed has formed task forces. What about Norway and the rest of the world? Norway did push its target rate up as the ECB hiked. But what is its plan?

Global

Global