Global| Nov 11 2025

Global| Nov 11 2025ZEW Expectations Weaken Mildly

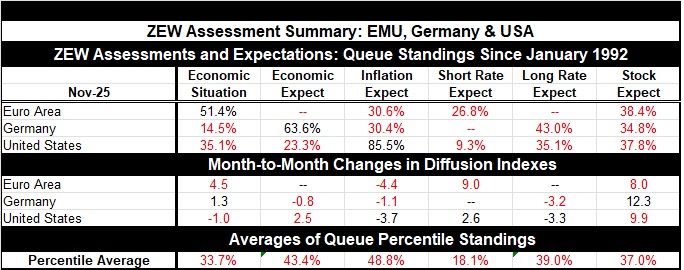

Macroeconomic expectations in the ZEW survey backtracked slightly in Germany while improving slightly in the United States in November. The economic situation improved slightly in the euro area and Germany while backtracking in the United States. That's the assessments of the current economic situation and expectations for Germany or the EMU that are moving in different directions in the U.S. and in Germany or in the U.S. vs. the European Monetary Union in November.

Inflation expectations backed off across the board easing slightly in the euro area, Germany, and also in the United States. While that happened, expectations for short-term interest rates became less focused on rate cuts in the euro area and slightly less tilted toward the expectation for rate cuts in the U.S. as well. Long-term rate expectations receded somewhat in both Germany and in the U.S. in November by small amounts. Stock market expectations picked up in the euro area, Germany, and the U.S., and in most cases, somewhat significantly.

The queue standings The queue standings are ranked standings of these various metrics, and they tell a clear story of how the ZEW experts see current conditions and policy tradeoffs. The euro area has an economic situation where the queue standing is at its 51st percentile, slightly above its historic median (on data since the early 1990s). However, Germany and the U.S. have very weak percentile standings with Germany in its 14.5 percentile and the U.S. in its 35th percentile. Macroeconomic expectations, however, find Germany at a solid 63.6 percentile while the U.S. is at a 23.3 percentile. ZEW experts are far more upbeat on prospects for German recovery right now than in the United States – and that seems odd to me with a lot of fiscal stimulus in train in the U.S. and tons of ‘AI’ investment.

Inflation expectations are high in the U.S. at an 85.5 percentile standing, well above the historic median, and clearly showing threatening conditions. This compares to a 30% queue standing for the euro area and Germany.

Short-term rate expectations are significantly below the median for both the euro area and the U.S. with the euro area at a 26.8 percentile and the U.S. at a 9.3 percentile standing. Long-term rate expectations have Germany at a 43-percentile and the U.S. at a more similar 35-percentile. Stock market expectations are fairly similar across the lot with the euro area at a 38-percentile standing, Germany at a 35-percentile standing and the U.S. at a 38-percentile standing.

Summing up These metrics remind us that ZEW experts see different inflation circumstances in the U.S. compared to Europe as well as very different current economic situations, especially between the U.S. and the euro area and very different macroeconomic expectations between the U.S. and Germany. The U.S. is seen more as a place that's percolating inflation despite the fact that the Federal Reserve continues to say inflation is under control and inflation expectations are well anchored. Apparently, they are not well-anchored among the ZEW financial experts. We might add, nor are they well-anchored among participants in the University of Michigan survey, or for respondents to the NFIB survey that was just released. Maybe it's the Fed that is not very well anchored to reality when it comes to inflation expectations assessments?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief