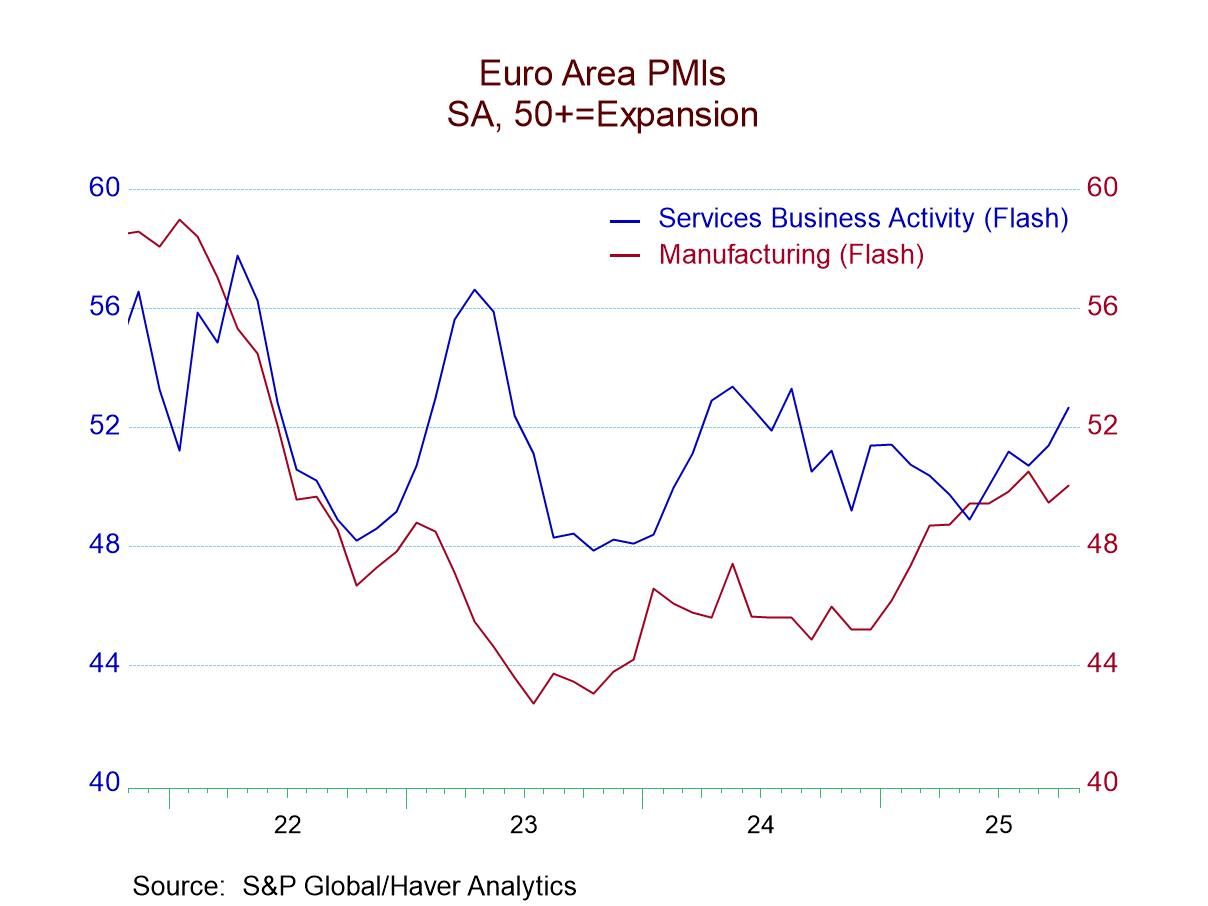

Composite PMIs Mostly Improve in October

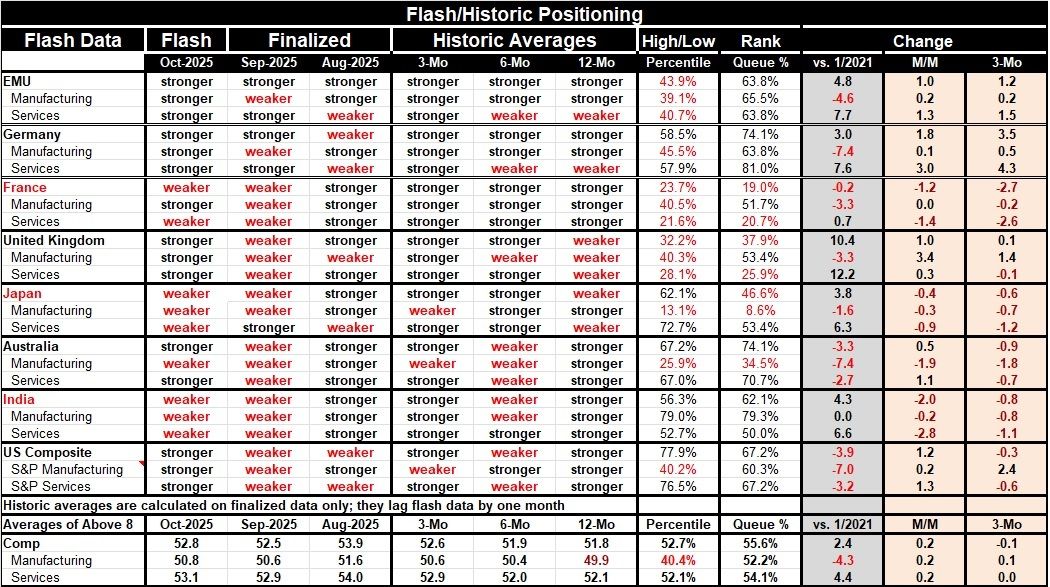

An upswing appears to be underway with both manufacturing and services readings improving. The S&P PMI data for October covered eight different reporters, five of which improved in October compared to September. September had been an extremely weak set of readings; out of the 24 different categories (eight countries with three readings each), there were only five that improved in September compared to August. August had been a strong month. The survey clearly is showing some volatility over these past few months; however, in October we're seeing a fairly broad-based increase, with only nine of the 24 detailed categories that assess the composite, manufacturing, and services showing weaker performance compared to September. And of those comparisons across eight countries, 19 sectors and composite indexes had been weaker month-to-month in September compared to August.

Over three months the averaged composites are stronger compared to six-month average. Among all the reporters, only three of the 24 sectors and composite readings show weakness in three-months compared to six-months. Each of those weakening readings is for manufacturing. They involve weaker manufacturing in Japan, in Australia, and in the United States. Ten of 24 sectors and composite readings weaken over six months compared to 12-months. Only 7 detailed readings out of 24 weaken over 12 months compared to 12-months before based on comparing averages.

Queue percentile standings take the October values and rank them in a queue of data back to January 2021 expressing the standing in October as a percentile in that queue of readings. The average percentile standing for the composite indexes in October is at 55.6%. The average manufacturing sector’s queue standing at 52.2% while the average services rating is at 54.1%. In October, all of the readings averaged across the 8 reporters are above their medians for the period back to January 2021 compared across monthly data. That's not an exceptionally strong performance, but it's a solid performance. Among the reporting countries, only Japan, the United Kingdom, and France have composite standings that are below their medians (that is, they have ranked standings for their respective composites below their 50th percentile).

The average standing across the 8 reporters in October generally shows an improvement from September; September was weaker than August. With that, October values, while higher month-to-month, were lower than they were in August. For example, the overall composite in October moved up to 52.8 from 52.5 in September, but September had fallen from 53.9. Values in October are still below values in August. The same thing is true of services and manufacturing.

The average sequential data for 3-months, 6-months and 12-months, however, show steady improvement with composite readings rising from 51.8 for 12-months to 51.9 over six months and to 52.6 over three months. These calculations are performed only on hard data and are up to date through September. The October monthly reading for the composite, for manufacturing and for services are stronger for each of these readings in October compared to three-month averaged values ended in September paving the way for continued improvement ahead.

Overall, the sense of improvement here is slow. Compared to January 2021, the October readings are stronger for composite and for services but weaker for manufacturing; that sector is taking longer to recover. Still, recovery seems to be in gear; if that remains the case, central banks may have to rethink their programs of ongoing interest rate cuts.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global