New Zealand Trade Shoots to Surplus on Export/Import Twist

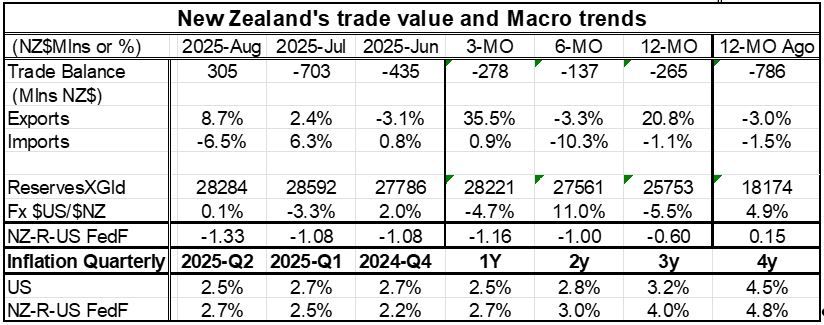

New Zealand exports surged in August as imports plunged causing a twist in the in the month-to-month trade balance that was thrust into a modestly positive surplus from a deeply negative position in July on these trends. New Zealand trade moved into a surplus of $NZ305 million, compared to a deficit of $NZ703 million in July The progression of deficits shows A 12-month monthly average monthly deficit of $NZ265 mln, a six-month monthly average deficit of $NZ137 mln and then an expanded monthly average deficit of NZ$278 mln over three-months.

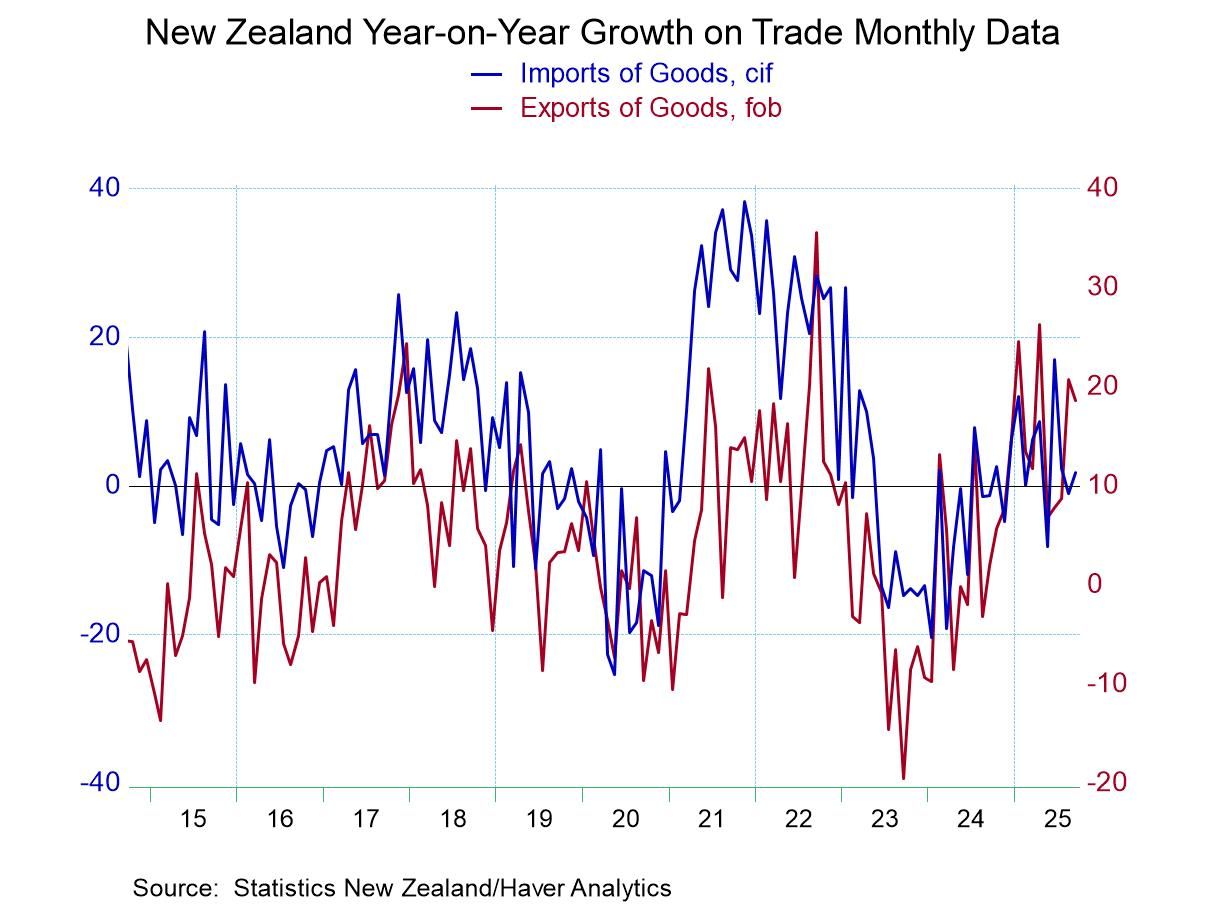

Exports rose by 20.8% over 12-months; export performance then cools over six-months followed by an exports surge of 35.5% over 3-months. This is in sharp contrast to imports, where imports fall by 1.1% over 12-months then fall at a 10.3% annual rate over six-months before recovering to rise at a meager 0.9% annual rate over 3-months.

New Zealand's international reserves excluding gold have continued to creep up sequentially. Inflation has hovered around the 2.5% to 2.7% since March of this year ending a period during which New Zealand inflation consistently overshot inflation in the US.

New Zealand's exports are and have been showing life better than imports for some time. Ten-year NZ government bond yields have been stuck in the 4% to 4 1/2% range. New Zealand's GDP growth has been locked in an extremely low range with negative GDP growth logged in the last three quarters of last year. It is displaying erratic and continued weak performance in 2025. The import restraint recorded in the trade accounts reflects weak domestic demand that stems from weak GDP growth.

The NZ CPI that has stabilized but also shows the potential to have ceased falling and may be mounting a period of some minor acceleration starting at rates around or below 2.5%. However, core inflation remains restrained and still in a declining mode – a strong counterpoint to the potential for acceleration. Meanwhile, the unemployment rate has been pressured higher. In the second quarter it shot back up to 5.2%, which is the peak that it experienced during Covid in 2020. New Zealand's current account deficit as of the second quarter continues to shrink, Economic weakness should keep interest rates headed lower and keep inflation contained for at least the balance of the year.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global