German PPI Continues to Behave

Inflation reports are still very much of market interest largely because inflation remains in the forefront, sufficiently contained, to allow central banks to choose a policy course of easing monetary policy. To stay on that course, they will need for inflation to remain under control.

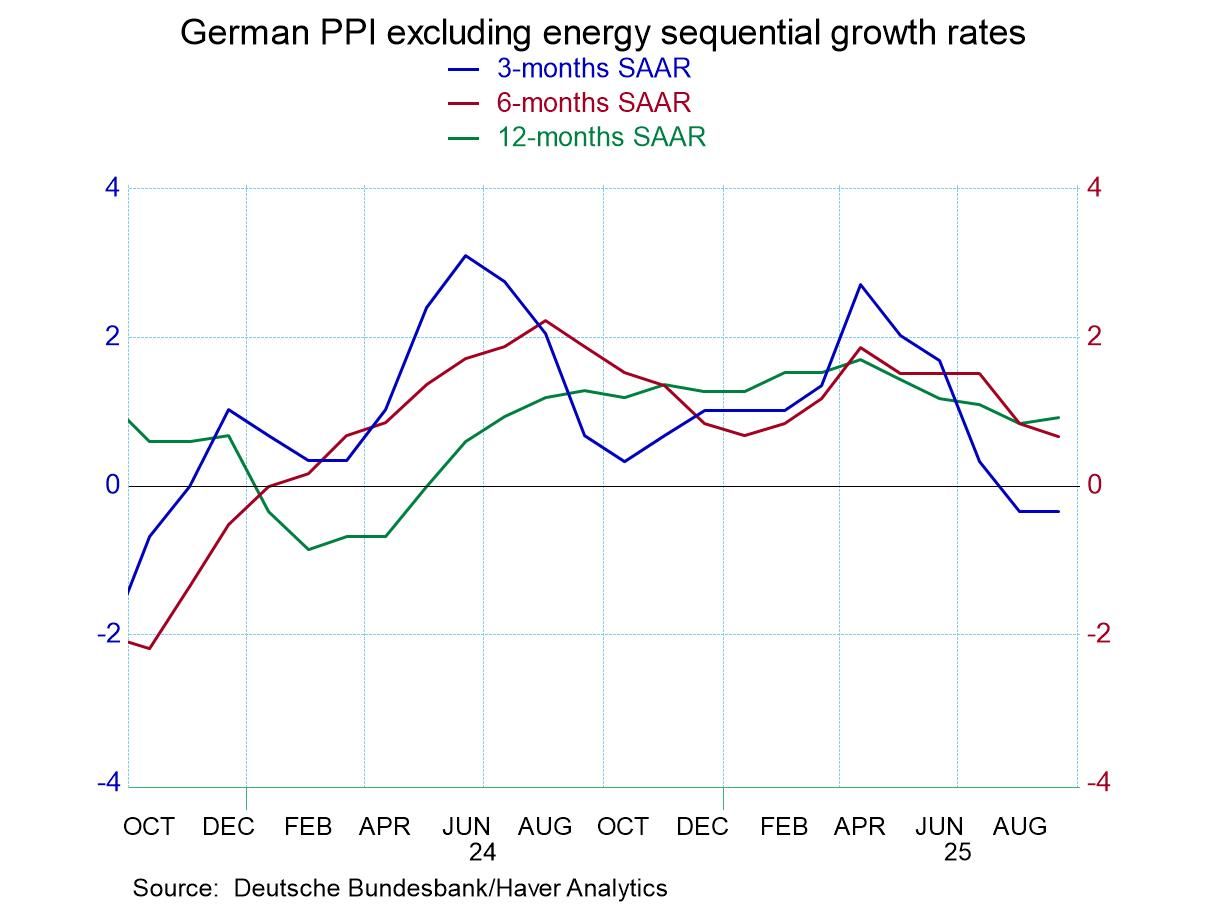

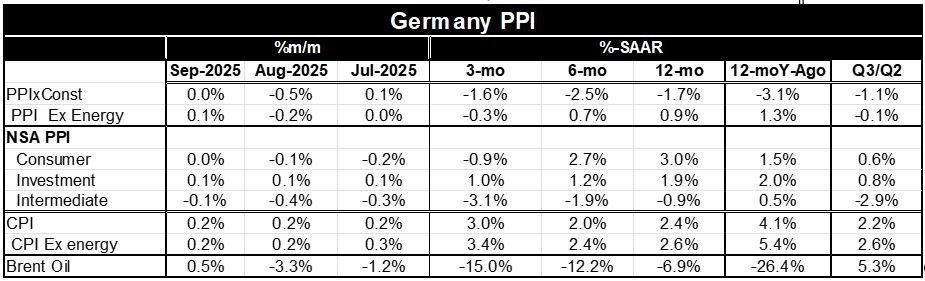

The German PPI in September is flat after falling 0.5 in August and rising only 0.1% in July. The PPI excluding energy has flattened in July, fallen by 0.2% in August and is up by only 0.1% in September. Both of these PPI series generate significant optimism sequentially as well. The PPI headline series falls by 1.7% over 12 months; it falls at a 2.5% annual rate over 6-months, and it falls at a 1.6% annual rate over 3-months; its change is negative on all three horizons. Inflation is quite contained and reinforcing of the theme of cutting interest rates from the standpoint of the monetary authorities.

For the PPI excluding energy inflation is up by 0.9%, Over 12-months it rises at a slower 0.7% annual rate over six-months and the PPI excluding energy falls by 0.3% over 3-months. The contained status of headline inflation is thus translated into the core so that the sequential core pattern shows inflation progressively lower measured over longer to shorter periods. For the German economy, its good news from the standpoint of inflation although part of the cost of this is that the German economy has been exceptionally weak.

The details of the PPI are a little bit less interesting because they're not seasonally adjusted, however, consumer goods, investment goods, and intermediate goods, trends are working lower.

Comparing the PPI to the CPI - and to the CPI excluding energy - we see that the excellent PPI trends do not translate directly into solid CPI inflation. CPI inflation is somewhat erratic but at 2.4% over 12-months and at 3% over three months, and the CPI ex-energy at 2.6% over 12-months and much higher at 3.4% at an annual rate over three-months, the German CPI has more work to do.

Still the underpinning of a solid PPI report is reassuring. With Brent oil prices off by about 7% over 12-months and falling at a 15% annual rate over three-months, the beneficial inflation trend is being driven by weakness in oil prices. And that does help the PPI more and faster than the CPI.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global