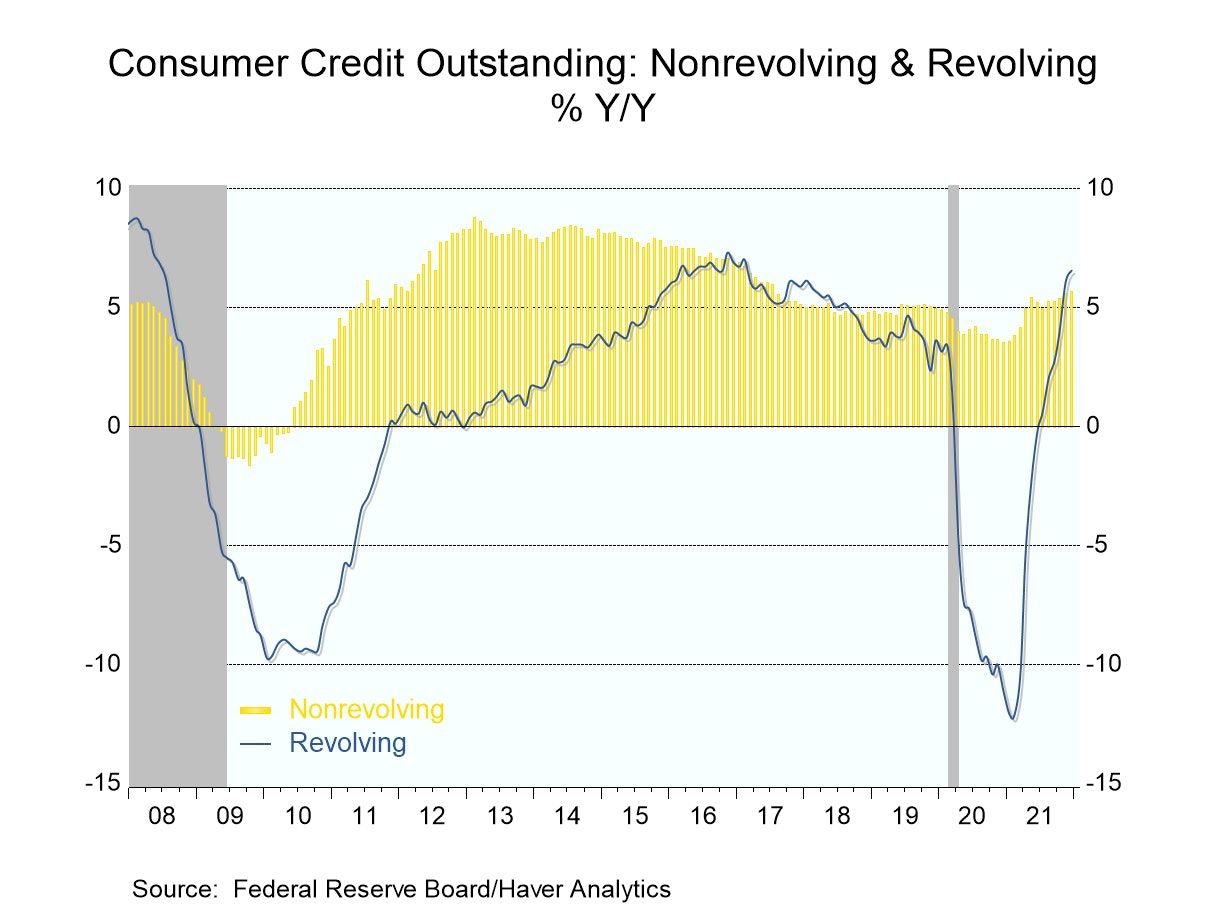

- Nonrevolving credit remains robust.

- Revolving credit growth slows.

USA| Feb 07 2022

USA| Feb 07 2022U.S. Consumer Credit Usage Continues Strong in December

by:Tom Moeller

|in:Economy in Brief

USA| Feb 07 2022

USA| Feb 07 2022FIBER: Industrial Commodity Prices Edge Higher

- Crude oil prices strengthen.

- Metals prices continue to rise.

- Lumber costs decline.

by:Tom Moeller

|in:Economy in Brief

Germany| Feb 07 2022

Germany| Feb 07 2022German IP Sends Mixed Signals at Yearend

German IP slowed at yearend. After rising by a strong 2.3% in October, it gained 0.3% in November and then shed 0.3% in December. While that marks a clear slowing, sequential growth rates of a broader dimension find German IP at a -4.2% falling pace over 12 months, shrinking again by at a smaller -1.6% pace over six months but then rising at a strong 9.7% pace over three months. The three-month gain obviously is driven by that gain in October, not true sustained yearend strength. But such is the way that the numbers fall and the tale they tell. That explains why we look at them from so many angles: to find the true trend, not just the numerical one.

It is often said that the devil is in the details. Here, we find that the sector data show a devilishly convoluted pattern: some clear, some muddled, some contrary. The clear story is from capital goods, there, a 4.4% 12-month drop that gives way to 9.2% pace of growth over six months and a whopping 46.7% annualized gain over three months. German capital goods, the laggard sector since Covid struck (still 11% below its February 2020 level, in fact), is now the leading growth sector for German IP. That begins to look like a restoration of normalcy. But consumer goods and intermediate goods do not go along with that sharp sequential rebound as both show a muddled pattern of expansions and setbacks over this same set of intervals. The construction sector, like capital goods, shows a clear pattern, but it’s the opposite one from capital goods- a pattern of deceleration. Construction output is up by 0.3% over 12 months. The pace slips to the negative over six months then worsens over three months. Construction output ends the year with a 3.9% drop in December. The trend for German IP may be upward on sequential data, but that trend does not get overwhelming support from German sectors. Moreover, it hangs in the balance on one very strong sector.

Manufacturing output also show the same sort of acceleration as overall IP. But real orders for manufactured goods show a convoluted sequence of growth rates from 12-months to six-months to three-months. Real sales in manufacturing, however, show a progressive explosion of growth.

The indicators, like the ZEE current conditions survey, the IFO and the EU Commission industrial index, show mixed results. The ZEW index is convoluted. The IFO current and expectations readings show steadily eroding trends. The EU Commission index also is convoluted. However, in the quarter-to-date, all these metrics are weakening compared to one quarter ago. And all show net gains compared their respective February 2020 levels – unlike IP that is still lower on balance along with all its sectors. Construction also is weaker compared to its pre-Covid readings. The messaging from all this is unclear, but it is not bullish.

France. Portugal, and Norway are also early reporters this month of IP data. Portugal shows a sequence of monthly readings that has clear upward momentum unlike Norway or France. All three, however, show net declines in the quarter-to-date (quarter just completed) compared to a quarter ago. France shows sequential acceleration, Norway shows sequential deceleration and Portugal misses the designation of acceleration on a numerical technicality (14.5<14.8), but it clearly is and has been accelerating (14.5>0.4, by a long shot). And all three countries have readings that are still above their respective levels of February 2020.

USA| Feb 04 2022

USA| Feb 04 2022U.S. Payrolls Show Unexpected Strength in January; Earnings Improve but Jobless Rate Edges Higher

- Annual payroll employment revisions substantially lift recent job gains.

- Earnings growth continues to strengthen.

- Jobless rate edges higher from two-year low.

by:Tom Moeller

|in:Economy in Brief

- Decrease in jobless claims suggests firm labor market conditions.

- Continued claims were up in January 15 week.

- Insured unemployment rate remains in historically low range.

Germany| Feb 04 2022

Germany| Feb 04 2022Domestic German Orders Show Surprising Strength

German domestic orders jumped in December, rising by 11.7% month-to-month (yes, that's month-to-month) and driving the year-on-year gain to 11.0%. This result compares to foreign orders that fell by 3.0% (after a strong 6.5% gain in November and an 11.3% plunge in October) as foreign orders are up over 12 months by just 2.1%.

Foreign orders show sequential deterioration with the annualized growth rates falling from 2.1% over 12 months to -2.4% over six months to -29.6% over three months. Foreign orders in addition to this secular deterioration have become extremely volatile in the last few months.

Domestic orders, in contrast, have no trend and are simply volatile. They are very strong in December, and they impart that strength to the three-month growth rate that surges at a 73% annualized rate. That is up strongly from -5.8% over six months and that was a deceleration from +11% over 12 months. By tenor, domestic orders slow then surge – no trend there. We do not know whether to treat this month as a one off (probably) or as the start of a new, stronger, trend (possibly).

Volatility was up, fell back, but is rising again The data on volatility show that the standard deviations of month-to-month percentage changes in foreign vs. domestic rates of growth have been highly correlated since late-2018. The correlation coefficient over that period (run on overlapping 12-month periods) is 0.972 (R-square of 0.945). Both series show a sharp ramp up in volatility starting around March 2020, peaking around June 2020, and holding at that very high level until March 2021. Volatility fell to a low in July 2021 and since then volatility is up again by about 85% from its recent low. That 'low' was still more than 100% above the sorts of volatility numbers that had been generated (which were very stable for both foreign and domestic orders) prior to Covid striking. Current foreign volatility has crept up higher than domestic volatility (despite this month's 'appearance'). Prior to Covid striking, the volatility of foreign orders was steadily and consistently higher than that for domestic orders by about a factor of 100%. That relationship appears to be in the process of being returned but with both volatility measures at a higher level.

With higher volatility, the signal to noise ratio falls. It will be harder to detect changes in trend and we will have more instances of spikes that are large and that are meaningless as they go away in future months. From April 2021, the percentage gain in foreign orders led the order parade with few exceptions but in December that is switched. Will it stay that way or is this just the result of volatility? In fact, since January 2008, foreign orders (based on year-over-year growth) have been stronger than domestic orders 63% of the time. And foreign order growth year-on-year seems to be weaker than domestic order growth (correlation coefficient 0.61) when overall order growth is negative. So, this inversion of strength between domestic and foreign orders may also be a signal of developing weakness even though orders are still up year-on-year. Remember that foreign orders are trending weak.

These correlations are 'interesting' for several reasons. Germany has the largest economy in the EMU. A large proportion of German exports stay within the EMU block. This month, orders from within the euro area fell by 4.2% with orders from outside the zone falling by 2.3%. While German domestic orders were strong- in an economy that is very export-dependent and sells a lot within the EMU as well - orders from EMU trade partners were weak. This confluence of relationships seems to ensure that domestic and foreign order series are not going to drift to far apart except in the short run, as they have done this month.

As for product type in December, consumer goods orders rose by 5.3%, intermediate goods orders rose by 4.1% and capital goods orders rose by 1.8%.

Real sales data in the bottom panel of the table show manufacturing sales rose by 0.2% on the month and those sales have been expanding at steady and strengthening rates from 12-months to six-months to three-months. In fact, the component sales data all show sequential acceleration except for consumer nondurables goods (and they pass that exception on to total consumer goods) as consumer durable capital good and intermediate goods sales all show sequential acceleration. All the accelerating series show power gains over the recent three months

The industrial sector data from the EU Commission on Germany, France Italy, and Spain – fellow EMU members- shows all of them with accelerating industrial sectors despite the drop in foreign orders and the weakness in the EMU-only orders.

Quarter-to-date (QTD) QTD orders show a strong 8.6% gain as the quarter finishes with foreign orders weaker, falling at a 3.9% pace and domestic orders popping at a 28.8% annual rate. Real sector sales show huge gains in manufacturing led by a very strong rebound in capital goods for the quarter and followed by a double-digit growth rate gain from intermediate goods.

Pre-Covid comparisons Comparing sales and orders to their pre-Covid January 2020 levels finds domestic orders up by 15.4% with foreign orders up by only 0.9%. Real sales are lower by 2.4% in manufacturing with shortfalls all around except for consumer durables and intermediate goods.

EU Commission index The EU Commission indexes show strong queue standings in December in their upper 90th percentiles for the most part for the industrial sectors of Germany, France, Italy, and Spain. All these metrics show double-digit gains from their January 2020 levels. Germany leads the group with a gain of 38.1 points; the rest show gains of from 10 points to 15 points.

- Nonfarm productivity advances at strong 6.6% annual rate in Q4.

- Compensation also strong, yet again.

- Gains in productivity and unit labor costs almost exactly offsetting.

USA| Feb 03 2022

USA| Feb 03 2022U.S. Factory Orders Posted a Modest Decline in December

- New orders for manufacturing goods dropped in December following seven consecutive monthly gains.

- Shipments were up 19 of the last twenty months.

- Both unfilled orders and inventories rose again during December.

- of9Go to 7 page