- Spending on goods declines; service outlays increase.

- Real disposable income improves.

- Core price inflation weakens further.

USA| May 26 2023

USA| May 26 2023U.S. Consumer Spending Is Surprisingly Strong in April

by:Tom Moeller

|in:Economy in Brief

USA| May 26 2023

USA| May 26 2023U.S. Manufacturers’ Durable Goods Orders Still Firm in April, but Some Industries Saw Declines

- Transportation orders excluding aircraft & vehicles advanced in April.

- Computers, electrical equipment & metals orders all decreased.

- Shipments of all manufacturers were down, while inventories reversed March decline.

USA| May 26 2023

USA| May 26 2023U.S. Goods Trade Deficit Widens in April; Largest Since October

- $96.77 billion deficit in April, larger than expected.

- Exports decline 5.5%, the deepest m/m fall since April ’20, reflecting drops in most end-use categories.

- Imports rebound 1.8%, the first m/m increase since January.

United Kingdom| May 26 2023

United Kingdom| May 26 2023UK Retail Sales Volume Rebound in April

UK retail sales grew a little more than expected in April. The broader trend also suggests a slightly brighter picture for consumer spending, notwithstanding still-intense cost of living pressures from high inflation.

The main points from this report were as follows –

• Retail sales volumes rose by 0.5% m/m in April 2023, partly reversing the sharp contraction of 1.2% chalked up in March. The consensus forecast was centred on a rise of 0.3% on the month.

• The headline increase in retail sales volume was predominantly driven by a rise in the volume of goods purchased from non-food stores (e.g. clothing and household goods). They increased by 1.0% in April after a decline of 1.8% in March, when poor weather conditions throughout the month affected sales.

• Food stores sales volumes increased by 0.7% following a monthly decline of 0.8% in March.

• Looking through the month-to-month volatility the trend in UK retail sales appears to have improved. Sales volume rose by 0.3% in the three months to April, from -1.0% in the previous three months.

Overall, the pick-up in today’s retail sales volumes is encouraging and will offer some encouragement to the idea that the UK can avoid a near-term recession.

by:Kritika Jain

|in:Economy in Brief

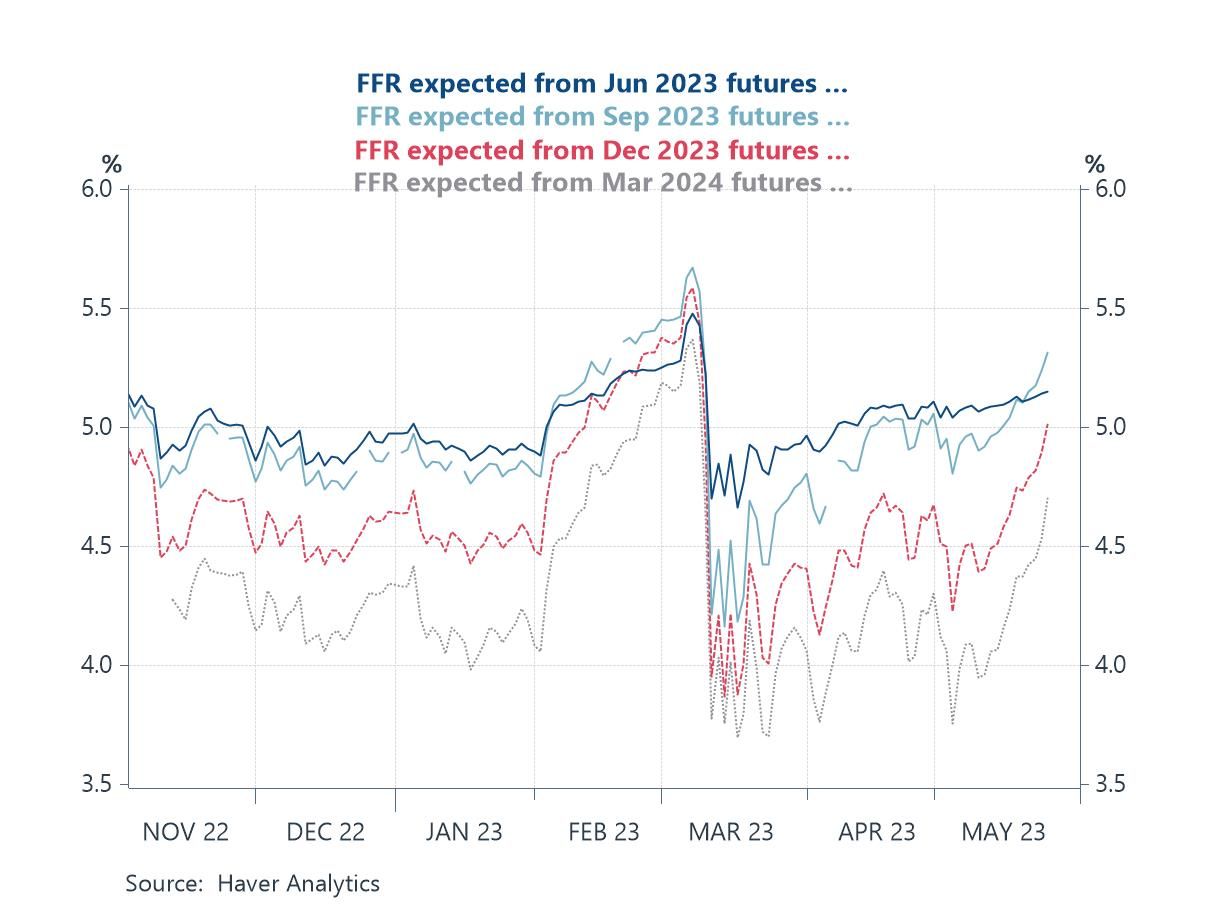

Global| May 26 2023

Global| May 26 2023Charts of the Week (May 26, 2023)

Lingering concerns about US debt ceiling negotiations have left financial markets on the back foot over the past few days. But incoming economic data this week have not helped. May’s flash PMIs, for example, disappointed to the downside in Europe with the details revealing stubbornly high price pressures in the service sector. Those details found an echo in a much stronger-than-expected UK inflation print for April as well. Against this backdrop our charts this week firstly home in on market expectations for Fed policy (in chart 1). We then contrast these with the more downbeat messages for global growth that are being signalled by falling copper prices and negative global growth surprises (in chart 2). We turn next to the sobering messages from the stalling pace of GDP growth in Asia’s more developed economies (in chart 3) and one reason for this (in chart 4), namely soggier world trade growth and rising inventories. Our last two charts then return to inflation issues and examine the relatively high level of energy price inflation in the UK compared with the US and to a lesser extent the euro area (in chart 5). This is then contrasted with the firming trend for core inflation in the UK and the ebbing trend in the US and euro area (in chart 6).

by:Andrew Cates

|in:Economy in Brief

USA| May 25 2023

USA| May 25 2023U.S. GDP Growth Revised Up in Q1’23; Profits Decline

- Inventories continue to subtract substantially from growth.

- Consumer spending stays strong as auto buying surges; business investment slows.

- Price index is unrevised & firm.

- After-tax profitability declines again.

by:Tom Moeller

|in:Economy in Brief

USA| May 25 2023

USA| May 25 2023Kansas City Fed Manufacturing Index Rebounds in May

- Composite Index improves to -1 in May, reflecting rises in production to -2, new orders to -14, and employment to a positive 7.

- Price indexes fall, w/ prices paid for raw materials having cooled significantly (lowest since July ’20) and prices received for finished goods having eased somewhat.

- Expectations for future activity remain flat in positive territory.

USA| May 25 2023

USA| May 25 2023U.S. Pending Home Sales Hold Steady in April

- Sales fall sharply y/y.

- Monthly changes are mixed amongst regions.

by:Tom Moeller

|in:Economy in Brief

- of11Go to 2 page