- Initial claims in tight range still just above pre-pandemic amounts.

- Continuing weeks claimed edge slightly lower in latest week.

- Insured unemployment rate steady at 1.3%.

Europe| Apr 27 2023

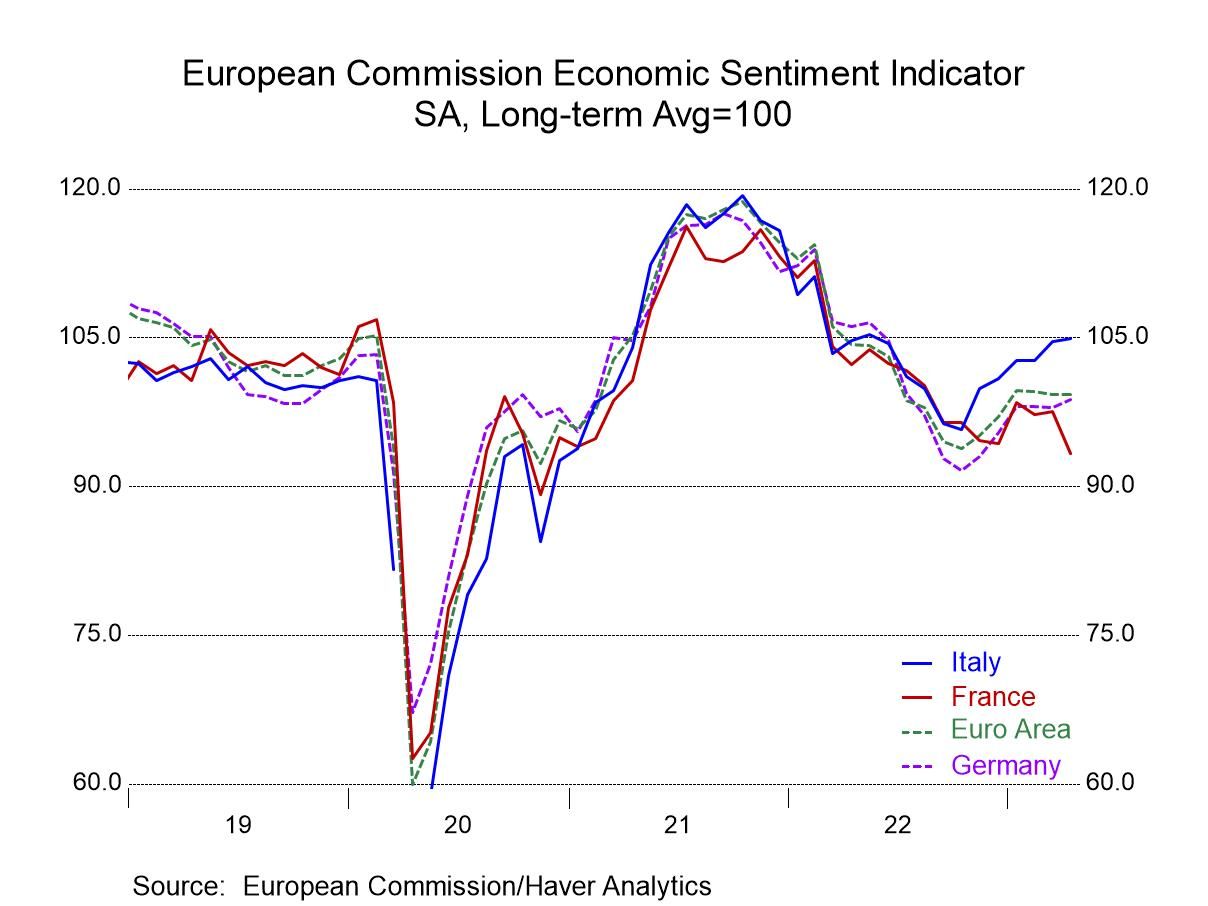

Europe| Apr 27 2023EU Commission Indexes for EMU Show Minimal Uptick

The EU Commission indexes that evaluate the European Monetary Union, its members, and sector results for April, show the smallest possible uptick for the overall index to 99.3 from 99.2 in March. This calls for popping the cork on a champaign bottle and then drinking none of it- a sort of dry celebration. The April value of the index has a 46.9 percentile standing, leaving it still below its historic median. The median on these ranked data occurs at a ranking of the 50th percentile. So, a technical ‘improvement here’ but really nothing to celebrate- a waste of the bubbly.

Monthly changes The overview of sector results shows a setback in April for the industrial sector that fell to a net reading of -3 from -1 in March. The construction sector was unchanged at a rating of plus-one in both March and April. The retailing sector improved to -1 in April from -2 in March; the services sector improved to +11 from +10; and consumer confidence improved to -17.5 from -19.1.

Standings are firm across sectors for the most part…but NOT overall These monthly changes leave the assessments of sector performance quite mixed. Consumer confidence has the weakest ranking at a 15.4 percentile standing, which is quite weak. The industrial sector has a 57.2 percentile standing, above its median, but not impressive. Services do better with the 65.9 percentile standing, retailing has a quite-firm 78.3 percentile standing, while construction continues to score a relatively strong standing at its 85.4 percentile. But as you can see from the rankings, the sector rankings really scatter quite widely and the extreme depressed state of consumer confidence has a large impact on the overall Monetary Union index since only consumer confidence is below its historic median and that's enough to drag the entire overall index below its historic median for April.

Countries month-to-month 18 of 19 member countries report in April and of these, eight show month-to-month deterioration while ten show approvement. However, the data are quite mixed on the month as the declining reporters generally show quite severe declines with five of eight declining entries showing monthly drops of 1.6% or worse. Among the countries reporting improvements in the month, 6 show increases of better than 1% and four show increases of 1.6% or better month-to-month. April becomes a month of some considerable divide among the reporting countries with a number of quite good responses and also significant number of quite bad responses. The number of respondents showing month-to-month deterioration has been relatively stable in recent months with seven countries reporting declines in March and eight reporting declines in February; the number in February being the same as the number in April.

Country standings The percentile standing data for the countries is significantly less upbeat than the percentile standing statistics by sector. Among the five sectors (as we saw above) four of them have standings above their medians with two sectors posting firm to strong queue standings. On a country-by-country overall index basis there was only one strong country entry and that's from Malta with a 94-percentile standing with Greece and Italy having standings we would consider to be on the firm side, above the 70th percentile, but still below the 80th percentile. All-in-all there are only five countries with percentile standings above their medians and 13 countries with standings below their medians. The European Monetary Union evaluates as much stronger when we assess it by looking at sectors rather than looking at country rankings. It's not particularly clear why this is true, because it's not as though the countries assessed positively are the largest economies. The two largest EMU economies have standings well below their historic medians while the 3rd and 4th ranked largest economies have standings above their historic medians and among the remaining 14 countries only three have standings above their historic medians and they aren't particularly large countries.

USA| Apr 26 2023

USA| Apr 26 2023U.S. Advance Goods Trade Deficit Narrows in March

- Deficit is smallest in four months.

- Exports rise but imports decline.

- Quarterly deficit is shallower than Q4’22.

by:Tom Moeller

|in:Economy in Brief

- Increase in total orders is first in three months.

- Orders improve modestly in most categories.

- Shipments and order backlogs rise, but inventories decline.

by:Tom Moeller

|in:Economy in Brief

USA| Apr 26 2023

USA| Apr 26 2023U.S. Mortgage Applications Rose in the Latest Week

- Mortgage applications rose in the week ended April 21.

- The effective rates on all loans rose in the latest week.

- The average loan size dropped in the latest week.

United Kingdom| Apr 26 2023

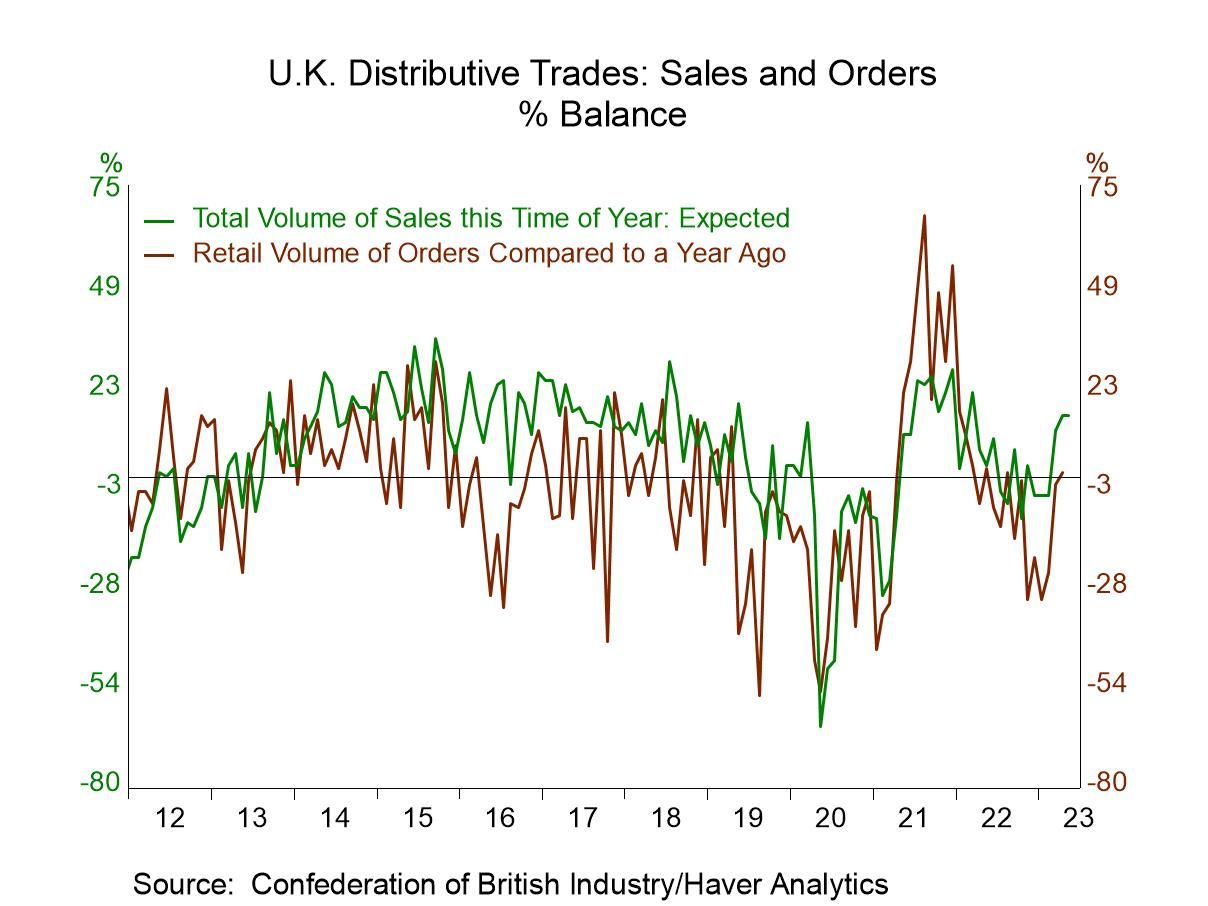

United Kingdom| Apr 26 2023U.K. Distributed Trades - Upswing in Effect and Expected to Persist

The U.K. distributive trades survey provides sector surveys for retailing and wholesaling in the United Kingdom in April as well as look-ahead observations or expectations for May.

Retail sales and orders currently: In April, retail sales, compared to a year ago, picked up to +5 compared to + 1 in March and +2 in February. Orders compared to a year ago were also stronger at a reading of +1 compared to -2 in March and a much weaker -25 in February. Sales for the time of year are quite upbeat with the survey value of 21 compared to 12 in March and 6 in February. The stock-to-sales ratio fell in April compared to March.

Wholesale sales and orders currently: For wholesaling, sales compared to a year ago were slightly weaker, falling back to a +13 reading from +18 in March, but still are much better than the -28 logged in February. Orders compared to a year ago were slightly improved month-to-month at -2 compared to -3 in March, and much better than the -23 logged in February. Sales for the time of year were down sharply at +15 but from an extremely elevated +35 in March; moreover, they compare favorably to zero in February and rank solidly in April. The stock-to-sales ratio has risen steadily from February to March to April.

Current sales and orders queue rankings: The queue ranking data reported sales in retailing and distributive trades show sales for the time of year extremely strong at a 93-percentile standing for retailing and at a firm 52-percentile standing for wholesaling. In retailing sales compared to a year ago have a 40-percentile standing and orders compared to a year ago have a 46.5 percentile standing; each of those metrics is below its respective historic median- on percentile ranked data the median lives at the 50-percentile ranking. The stock-to-sales rank in retailing is low at a 3.5 percentile standing. For distributive trades sales compared to a year ago, sales log a 46-percentile standing and orders compared to a year ago have a roughly 40-percentile standing; these are not too different from the standings for retail sales. The big difference is in the stock-to-sales ratio which is above its historic median for wholesaling at a 64-percentile standing compared to a very weak standing in retailing.

Expectations Expected retail sales and orders: Expected retail sales for the month ahead project a decline in sales compared to a year ago on a -7 reading in May compared to +9 in April. Orders compared to a year ago are also expected to weaken to a -8 reading compared to zero for orders relative to a year ago as assessed last month. However, both these metrics are stronger in May than their March and February values. Moreover, sales, adjusted for the time of year, are expected to rise to +16 in May from +13 in April. This also compared to +11 in March and -2 in February. Expected retail sales for the time of year are strong. The stock-to-sales ratio is expected to be slightly lower.

Expected wholesale sales and orders: Expected wholesale sales year-over-year are stronger at +9 in May compared to +2 in April and compared to values of -22 in March and February. Wholesale orders expected compared to a year ago are improved to -1 compared to -13 in April and compared to much weaker values in March in February. Expected wholesale sales for the time of year are expected to step back to a +14 reading from +17 in April, leaving them even with March’s +14 but stronger than a -8 reading in February. The stock-to-sales ratio is expected to step up in March and to continue with a step-up trend.

Expected retail and wholesale sales and orders queue rankings: The rank standings for expectations are somewhat similar as retailing has an 89-percentile standing for sales for the time of year while wholesaling logs an above median 60th percentile standing- not as strong- but a reading also well above its median. Retailing expectations for sales and orders compared to a year ago are weaker than in wholesaling; the retailing rank for sales compared to a year ago has a 17.5 percentile standing and expected orders compared to a year ago have a 28th percentile standing. For wholesaling expectations, the rankings are 43.2% for sales and 40.7% for orders. Retailing also has a low ranking for the stock-to-sales ratio on expected data while wholesaling has a 75.4 percentile standing; that is firm.

USA| Apr 25 2023

USA| Apr 25 2023U.S. Consumer Confidence Weakens in April

- Expectations decline to nine-month.

- Present situation index improves slightly.

- Inflation expectations slip.

by:Tom Moeller

|in:Economy in Brief

- March sales +9.6% m/m to 683,000 units SAAR; Feb. downwardly revised to a drop from a rise.

- Month-on-month sales gain in three of four major regions with only decline in the South.

- Median sales price, up for the third time in four months, rises to a three-month-high $449,800.

- of10Go to 2 page