Global

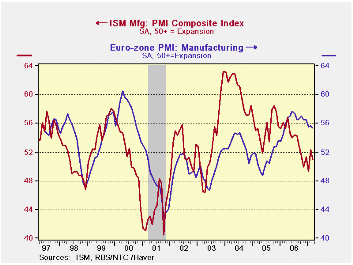

Global As you can tell from the chart on the left the sense of there being separate business cycles in the US and in Europe is a sort of joke. The US and Euro area manufacturing indexes are plotted on top of one another and their sense of co-variation is unmistakable. Also the US is shown to be the male and E-zone is the female; that is to say, if we regard this as a dance, the US leads.

As you can tell from the chart on the left the sense of there being separate business cycles in the US and in Europe is a sort of joke. The US and Euro area manufacturing indexes are plotted on top of one another and their sense of co-variation is unmistakable. Also the US is shown to be the male and E-zone is the female; that is to say, if we regard this as a dance, the US leads. In the recent mini-cycle, Europe has struck out a bit on its own. A US up-cycle from mid-2005 aborted early, turning to decline. Meanwhile, Europe has continued to expand and only recently has hit a plateau with hint of erosion. In the US, the down-cycle is only showing early signs of stabilization.

yes"> We wonder if Europe needs the US more than the US needs Europe?

The table above shows hath the E-zone readings, while off peak, are still very high in the range they have occupied since Mid-1997. The overall index is in the top 30% of its range and stands 6% above its average. Orders are similarly strong. Supplier deliveries are showing the weakest relative performance 10% below their average of the period.

Placing NTC Euro-Zone Readings in their Respective Ranges| Since June'98 | |||||||||

| NTC E-zone | Current | Std Dev | Average | SD% Avg | MAX | MIN | Range | Percentile | % of AVG |

| NTC Index | 55.4 | 3.8 | 52.5 | 7.3 | 60.5 | 42.9 | 17.5 | 71.1 | 106 |

| New Orders | 56.4 | 4.6 | 53.5 | 8.7 | 62.4 | 41.0 | 21.4 | 72.3 | 105 |

| Backlogs | 53.9 | 3.1 | 52.0 | 5.9 | 57.6 | 47.2 | 10.5 | 64.1 | 104 |

| Production | 57.4 | 4.2 | 54.2 | 7.7 | 62.8 | 43.0 | 19.9 | 72.8 | 106 |

| Supplier Deliveries | 42.5 | 4.8 | 47.2 | 10.1 | 56.9 | 34.7 | 22.2 | 35.1 | 90 |

| Inventories | 48.7 | 1.0 | 48.3 | 2.0 | 50.4 | 46.2 | 4.3 | 58.9 | 101 |

| Prices (Pd) | 66.1 | 9.8 | 59.7 | 16.4 | 76.5 | 37.7 | 38.8 | 73.3 | 111 |

| Employment | 52.9 | 2.9 | 49.8 | 5.8 | 56.0 | 44.2 | 11.8 | 73.9 | 106 |

| New Export Orders | 55.3 | 4.3 | 52.8 | 8.1 | 60.0 | 39.4 | 20.6 | 77.5 | 105 |

| Note: From June 1997 to Date; except back logs since Nov '02 | |||||||||

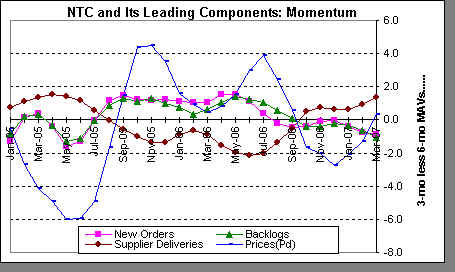

The leading components of the NTC E-zone index are showing mixed trends. We form these trends as the difference between the 3 month and six month indexes. Supplier deliveries and prices-paid are turning up while new orders and order backlog trends are eroding.

The leading components of the NTC E-zone index are showing mixed trends. We form these trends as the difference between the 3 month and six month indexes. Supplier deliveries and prices-paid are turning up while new orders and order backlog trends are eroding.

On balance, we can see the strong US-Europe linkages or commonalities. The history looks as though the US cycle gets transmitted to Europe, but Europe is recently showing some independent strength. However, it is also showing some sign of decay. It hardly seems as though a further rise in the Euro can do any good for Europe. But, so far so good.

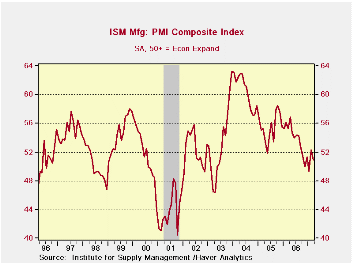

The chart on the left shows the ISM clearly has broken through the up trend from its recession recovery and now is in a well-established downtrend. Its recent up-tick is still in the grip of that down-trending range.

The table below shows the ISM and its components with a number of statistics that describe it/them.

The chart on the left shows the ISM clearly has broken through the up trend from its recession recovery and now is in a well-established downtrend. Its recent up-tick is still in the grip of that down-trending range.

The table below shows the ISM and its components with a number of statistics that describe it/them.

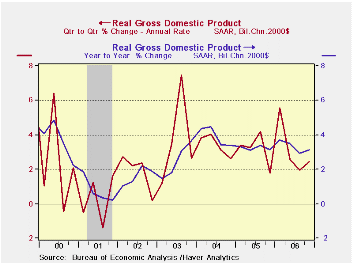

The chart on the left contains the Q/Q as well as the Yr/Yr plot for GDP to show trend and volatility. On it you can seen that GDP growth is still gradually eroding, but amid enough volatility to make the trend less than certain.

The chart on the left contains the Q/Q as well as the Yr/Yr plot for GDP to show trend and volatility. On it you can seen that GDP growth is still gradually eroding, but amid enough volatility to make the trend less than certain.

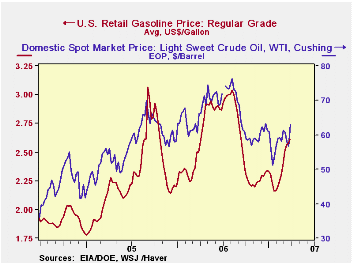

Mid- to late-January had seen a nice break in these markets (at least from consumers' viewpoints), as gasoline was flirting with $2.00/gallon and crude oil fell near $50/barrel. In this period, demand was relatively low and inventories relatively high, as gauged by "days' supply" of gasoline inventory, seen in the second graph. In the days' supply measure, gasoline stocks are compared with the volume of product supplied. This "inventory/sales ratio" is an excellent illustration of the seasonal effect. The graph makes plain that these weeks in mid-winter are always a high point for gasoline availability. In the first week of February, the ratio peaked at 25.0 days, compared with annual averages just above 22 days for each of the last two calendar years. The graph also shows, however, that the whole range of inventory adequacy has declined in recent years; in 2001, that mid-winter peak was 26.3 days and in 1999, it was 29.1 days. Demand appears not to have weakened so much in the winter as it used to.

Mid- to late-January had seen a nice break in these markets (at least from consumers' viewpoints), as gasoline was flirting with $2.00/gallon and crude oil fell near $50/barrel. In this period, demand was relatively low and inventories relatively high, as gauged by "days' supply" of gasoline inventory, seen in the second graph. In the days' supply measure, gasoline stocks are compared with the volume of product supplied. This "inventory/sales ratio" is an excellent illustration of the seasonal effect. The graph makes plain that these weeks in mid-winter are always a high point for gasoline availability. In the first week of February, the ratio peaked at 25.0 days, compared with annual averages just above 22 days for each of the last two calendar years. The graph also shows, however, that the whole range of inventory adequacy has declined in recent years; in 2001, that mid-winter peak was 26.3 days and in 1999, it was 29.1 days. Demand appears not to have weakened so much in the winter as it used to.