Global| Mar 29 2007

Global| Mar 29 2007U.S. GDP: The Upward Revisions That Seem Like a Downer

| GDP GROWTH | 2006 Q1 | 2006 Q2 | 2006 Q3 | 2006 Q4 | 2006 Q4 | 2006 Q4 | |

|---|---|---|---|---|---|---|---|

| Actual/A,P,F | Actual | Actual | Actual | Advance | Prelim | Final | Yr/Yr |

| Real GDP | 5.6% | 2.6% | 2.0% | 3.5% | 2.2% | 2.5% | 3.1% |

| PCE | 4.8% | 2.6% | 2.8% | 4.4% | 4.2% | 4.2% | 3.6% |

| Durables | 19.8% | -0.1% | 6.4% | 6.0% | 4.4% | 4.4% | 7.4% |

| Nondurables | 5.9% | 1.4% | 1.5% | 6.9% | 6.0% | 5.9% | 3.7% |

| Services | 1.6% | 3.7% | 2.8% | 2.9% | 3.3% | 3.4% | 2.9% |

| Business Invst. | 13.7% | 4.4% | 10.0% | -0.4% | -2.4% | -3.1% | 6.0% |

| Structures | 8.8% | 20.3% | 15.7% | 2.7% | -0.8% | 0.9% | 11.2% |

| Equipment | 15.6% | -1.4% | 7.7% | -1.8% | -3.1% | -4.8% | 4.0% |

| Housing | -0.3% | -11.1% | -18.6% | -19.2% | -19.1% | -19.8% | -12.8% |

| Inventories($B)* | $41.2 | $53.7 | $55.4 | $35.3 | $17.3 | $22.4 | $35.4 |

| Farm | $4.3 | $1.9 | $2.5 | $2.1 | $2.4 | $2.4 | $1.5 |

| Nonfarm | $36.8 | $52.2 | $53.3 | $33.4 | $14.6 | $20.0 | ($24.8) |

| Net Exports($B)** | ($636.6) | ($624.2) | ($628.8) | ($581.4) | ($585.1) | ($582.6) | $54.0 |

| Exports | 14.0% | 6.2% | 6.8% | 10.0% | 10.5% | 10.6% | 9.4% |

| Imports | 9.1% | 1.4% | 5.6% | -3.2% | -2.2% | -2.6% | 3.3% |

| Government | 4.9% | 0.8% | 1.7% | 3.7% | 3.3% | 3.4% | 2.7% |

| Real Final Sales | 5.6% | 2.1% | 1.9% | 4.2% | 3.6% | 3.7% | 3.3% |

| For Yr/Yr: * average, ** Change from Yr ago Qtr | |||||||

GDP and its main components are displayed in the table above. The most recent four quarters appear in the table as well as the three passes at estimating GDP in the current quarter and the current Yr/Yr value. GDP is still growing by more than 3% Yr/Yr. Q4 GDP’s estimate has fluctuated starting out at 3.5% dipping to 2.2% and now finalizing at 2.5% - that is we call this the final estimate for GDP. It is until benchmark revisions are done. In some sense GDP is never really finalized, but we call this the final estimate. The final estimate was made stronger mainly due to stronger inventory growth and weaker imports. Since imports subtract from GDP, weaker imports boost GDP. But imports are a function of the strength of domestic demand. So, weaker imports also are an indication of weaker domestic demand conditions. The slippage in capital spending in the final estimate on equipment and software is another example of fundamental weakness that is obscured by the upward revision to GDP in 2006-Q4. On balance, after revision, GDP is stronger but its trend looks weaker.

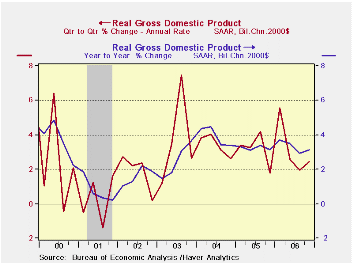

The chart on the left contains the Q/Q as well as the Yr/Yr plot for GDP to show trend and volatility. On it you can seen that GDP growth is still gradually eroding, but amid enough volatility to make the trend less than certain.

The chart on the left contains the Q/Q as well as the Yr/Yr plot for GDP to show trend and volatility. On it you can seen that GDP growth is still gradually eroding, but amid enough volatility to make the trend less than certain.

The GDP report highlights the recent statement made by the Fed Chairman about how the outlook has become more uncertain. While this report shows strong consumer spending, the consumer has been sluggish early in 2007, business investment is much weaker than expected, too. Inventories are in an irregular downtrend. A contracting (real) trade deficit, made up of firm exports and withering imports, has added strength to an otherwise lackluster economy. As we look ahead, it is clear that the economy needs a pick-up from some sector. Certainly the consumer must do better. But with housing askew the economy can ill afford for the business sector to be a drag on growth. Yet that is precisely what appears to be in train for the first quarter.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief