Global| Mar 28 2007

Global| Mar 28 2007U.S. Durable Goods Weakness - NO RELIEF!

Summary

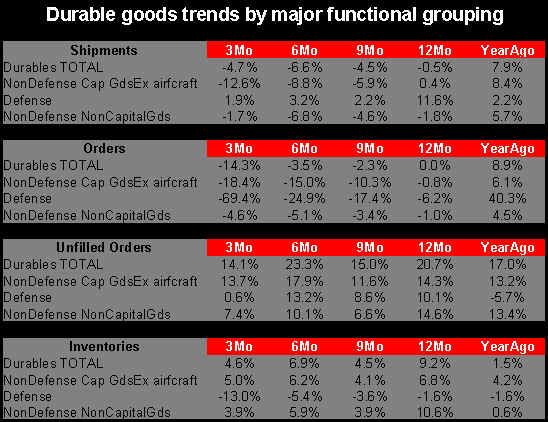

What results from this is still a series of weak sector growth rates. The economy is not faring as badly as orders suggest because shipments are growing better than orders. Defense shipments are positive although have softened their [...]

| · For the month, durable goods orders were made even weaker at -9.3% with a February rebound of just 2.5%- pathetic. The table below re-casts some familiar categories to exclude volatile aircraft orders. |

|---|

|

What results from this is still a series of weak sector growth rates.

In the chart on durable orders you see the point about how weak orders are compared to shipments…The worst apt is not how weak they are but that the weakness shows no sign of abating in terms of the speed of the growth rate.

Expanding order backlogs are one factor that reduces the sense of impending doom from the weak orders. But even the strong order backlog growth is beginning to lose some pace.

Another of my ‘favorite charts’ to diagnose this sector is the sequential growth chart of key durable goods sectors. We carry as a footnote item on diffusion accounting on inventory to sales ratios by noting for which time segments sales are outpacing inventories. You can see that inventories out-pace sales for all industries and all segments excerpt the recent three months where about 30% of the sectors saw sales grow faster than inventories. This sort of progress is essential to make progress on excess inventory levels. So far we have too little of it.

Another of my ‘favorite charts’ to diagnose this sector is the sequential growth chart of key durable goods sectors. We carry as a footnote item on diffusion accounting on inventory to sales ratios by noting for which time segments sales are outpacing inventories. You can see that inventories out-pace sales for all industries and all segments excerpt the recent three months where about 30% of the sectors saw sales grow faster than inventories. This sort of progress is essential to make progress on excess inventory levels. So far we have too little of it.  Fabricated metals and electrical equipment are healthy sectors; together they make up about 17% of shipments. Weakness in capital goods is all the more surprising given the strength in exports.For example turbine and generators weakness is surprising:

Fabricated metals and electrical equipment are healthy sectors; together they make up about 17% of shipments. Weakness in capital goods is all the more surprising given the strength in exports.For example turbine and generators weakness is surprising:  The weakness in construction equipment is more expected given the woes in the residential sector.

The weakness in construction equipment is more expected given the woes in the residential sector. And, interestingly, material handling equipment, which is the stuff that helps to load trucks and trains and to move goods around in warehouses, shows a fading trend.

And, interestingly, material handling equipment, which is the stuff that helps to load trucks and trains and to move goods around in warehouses, shows a fading trend.

Summing up. On balance the weakness in durable goods orders is in the VANGUARD of economic weakness. It does not seem due to events abroad as US capital goods exports remain strong. It is not on the back of weak consumer spending since the consumer has been somewhat irregular in early 2007 but ended 2006 on a strong note. Service sector spending continues quite strong; job growth and income growth are still firm. The rate of unemployment is low and wages have seen a boost recently. CEOs do not tell us they have plans to reduce their pace of investment. Yet they seem to be doing it. They nonetheless have excess funds but they use them for other financial transactions to dress-up their balance sheets. We have seen lowered earnings guidance from a variety of companies. Is this now to become a self-fulfilling prophecy?

German CPI Picks Up, Pushed by Energy and Non-Energy Factorsby Carol Stone March 28, 2007

CPI inflation in Germany increased 0.3 percentage point this month to 1.9% (year/year % change) from 1.6% in February. A year ago this broad measure was 2.1%. In between, as is evident in the first graph, the German CPI held near a 2% rate, then plunged during September and October when energy prices broke. Over the last five months, the total CPI resumed a near-2% pace as both energy and non-energy prices began to accelerate.

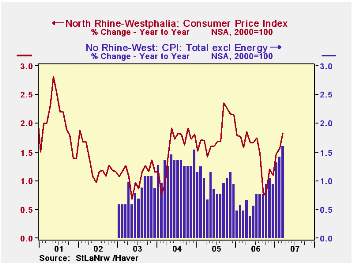

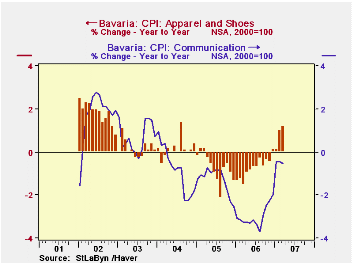

Today, only the total index is available for March for all of Germany. But several individual Länder published their full array of CPI data. Our table below lists the Länder maintained in Haver's GERMANY database and their CPI performances excluding energy. (We've also included the names of their capital cities to aid in identifying the specific territory. These areas constitute 64% of the weight in the Pan-German CPI) In each case, these data show that inflation aside from energy has picked up noticeably. For example, in the largest Länd (by population), North Rhine-Westphalia, the total CPI in the last few months looks to have simply resumed the pace of 1.6-1.8% year-on-year that prevailed before last autumn's energy drop. But more significantly, even as energy prices have picked back up again, prices excluding energy have accelerated substantially. In early 2006, they were increasing at a pace well below 1% in that region, touching as low as 0.4% year-on-year last May, but they rose 1.6% this month. Similarly, in Bavaria, the total index has risen 2.1% in March, hardly different from 2.0% in March 2006. However, the index excluding energy was also up 2.1% this March, compared with just 1.0% in the same month a year ago.

In both of these regions, the distribution of the ex-energy price increases has been broad. Food prices have accelerated, as have lodging and restaurants, recreation and "other" (mostly personal care goods and services). Two other seemingly unrelated categories are seeing noticeable changes: clothing and communication had both been falling sharply but are no longer doing so. Clothing prices have turned upward, not rapidly, but much different from the declines seen earlier. Communications prices are still falling, but again, much less than they were through the middle of last year.

So while overall inflation looks no worse, for either Germany as a whole or for the two Länder we have described here, it is much broader in scope than experienced until a few months ago. And two sources of price weakness, the technology revolution in communications and the shift toward inexpensive production of clothing in Asia, are apparently playing out. These conditions generate good questions about prospects for the course of inflation going forward.

| Germany (NSA, Yr/Yr % Change) | Mar 2007 | Feb 2007 | Jan 2007 | March 2006 | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|---|

| Pan-Germany | 1.9 | 1.6 | 1.6 | 2.1 | 1.7 | 2.0 | 1.7 |

| ex Energy | -- | 1.7 | 1.8 | 0.8 | 1.0 | 1.2 | 1.4 |

| Energy | -- | 2.2 | 1.6 | 11.8 | 8.5 | 10.3 | 4.1 |

| Excluding Energy:Baden-Württemberg (Stuttgart) | 1.8 | 1.8 | 1.8 | 0.9 | 1.1 | 1.0 | 1.7 |

| Bavaria (Munich) | 2.1 | 1.9 | 1.9 | 1.1 | 1.3 | 1.5 | 1.8 |

| Hessen (Frankfurt) | 1.8 | 1.6 | 1.9 | 0.7 (May) | -- | -- | -- |

| N. Rhine-Westphalia (Düsseldorf) | 1.6 | 1.4 | 1.3 | 0.5 | 0.7 | 1.0 | 1.3 |

| Brandenburg (Potsdam) | 1.8 | 1.9 | 1.9 | 1.1 | 1.4 | 1.5 | 1.7 |

| Saxony (Dresden) | 2.2 | 2.2 | 2.4 | 1.1 | 1.5 | 1.3 | 1.4 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief