Global| Mar 29 2007

Global| Mar 29 2007U.S. GDP: The Upward Revisions That Seem Like a Downer

| GDP GROWTH | 2006 Q1 | 2006 Q2 | 2006 Q3 | 2006 Q4 | 2006 Q4 | 2006 Q4 | |

|---|---|---|---|---|---|---|---|

| Actual/A,P,F | Actual | Actual | Actual | Advance | Prelim | Final | Yr/Yr |

| Real GDP | 5.6% | 2.6% | 2.0% | 3.5% | 2.2% | 2.5% | 3.1% |

| PCE | 4.8% | 2.6% | 2.8% | 4.4% | 4.2% | 4.2% | 3.6% |

| Durables | 19.8% | -0.1% | 6.4% | 6.0% | 4.4% | 4.4% | 7.4% |

| Nondurables | 5.9% | 1.4% | 1.5% | 6.9% | 6.0% | 5.9% | 3.7% |

| Services | 1.6% | 3.7% | 2.8% | 2.9% | 3.3% | 3.4% | 2.9% |

| Business Invst. | 13.7% | 4.4% | 10.0% | -0.4% | -2.4% | -3.1% | 6.0% |

| Structures | 8.8% | 20.3% | 15.7% | 2.7% | -0.8% | 0.9% | 11.2% |

| Equipment | 15.6% | -1.4% | 7.7% | -1.8% | -3.1% | -4.8% | 4.0% |

| Housing | -0.3% | -11.1% | -18.6% | -19.2% | -19.1% | -19.8% | -12.8% |

| Inventories($B)* | $41.2 | $53.7 | $55.4 | $35.3 | $17.3 | $22.4 | $35.4 |

| Farm | $4.3 | $1.9 | $2.5 | $2.1 | $2.4 | $2.4 | $1.5 |

| Nonfarm | $36.8 | $52.2 | $53.3 | $33.4 | $14.6 | $20.0 | ($24.8) |

| Net Exports($B)** | ($636.6) | ($624.2) | ($628.8) | ($581.4) | ($585.1) | ($582.6) | $54.0 |

| Exports | 14.0% | 6.2% | 6.8% | 10.0% | 10.5% | 10.6% | 9.4% |

| Imports | 9.1% | 1.4% | 5.6% | -3.2% | -2.2% | -2.6% | 3.3% |

| Government | 4.9% | 0.8% | 1.7% | 3.7% | 3.3% | 3.4% | 2.7% |

| Real Final Sales | 5.6% | 2.1% | 1.9% | 4.2% | 3.6% | 3.7% | 3.3% |

| For Yr/Yr: * average, ** Change from Yr ago Qtr | |||||||

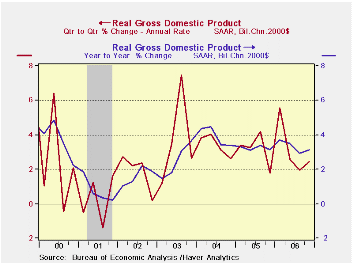

GDP and its main components are displayed in the table above. The most recent four quarters appear in the table as well as the three passes at estimating GDP in the current quarter and the current Yr/Yr value. GDP is still growing by more than 3% Yr/Yr.Q4 GDP’s estimate has fluctuated starting out at 3.5% dipping to 2.2% and now finalizing at 2.5% - that is we call this the final estimate for GDP. It is until benchmark revisions are done. In some sense GDP is never really finalized, but we call this the final estimate. The final estimate was made stronger mainly due to stronger inventory growth and weaker imports. Since imports subtract from GDP, weaker imports boost GDP. But imports are a function of the strength of domestic demand. So, weaker imports also are an indication of weaker domestic demand conditions. The slippage in capital spending in the final estimate on equipment and software is another example of fundamental weakness that is obscured by the upward revision to GDP in 2006-Q4. On balance, after revision, GDP is stronger but its trend looks weaker.

The chart on the left contains the Q/Q as well as the Yr/Yr plot for GDP to show trend and volatility. On it you can seen that GDP growth is still gradually eroding, but amid enough volatility to make the trend less than certain.

The chart on the left contains the Q/Q as well as the Yr/Yr plot for GDP to show trend and volatility. On it you can seen that GDP growth is still gradually eroding, but amid enough volatility to make the trend less than certain.

The GDP report highlights the recent statement made by the Fed Chairman about how the outlook has become more uncertain. While this report shows strong consumer spending, the consumer has been sluggish early in 2007, business investment is much weaker than expected, too. Inventories are in an irregular downtrend. A contracting (real) trade deficit, made up of firm exports and withering imports, has added strength to an otherwise lackluster economy. As we look ahead, it is clear that the economy needs a pick-up from some sector. Certainly the consumer must do better. But with housing askew the economy can ill afford for the business sector to be a drag on growth. Yet that is precisely what appears to be in train for the first quarter.

U.S. Corporate Profits Head Lower Fast…by Robert Brusca March 29, 2007

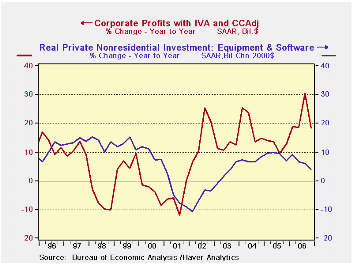

Corporate profits with capital consumption adjustment fell by 0.3% in Q4 2006. Profits had risen by 3.9% in Q3 2006. The drop off comes as corporate executives have been warning of a pending earnings slowdown.

Corporate profits are of course important for stock market investors. They also are important in determining the trend for capital spending. When profits slide corporations generally reduce capital spending. As the chart above shows, the current slowdown in capital spending is coming ahead of profits weakness. This is a worrying result since a number of earnings estimates just released point to a slowdown in the period ahead and capital spending is lower before that effect has hit the corporate balance sheet.

| Q4-06 | Q3-06 | Q2-06 | Q1-06 | Q4-05 | |

| Profits Pre Tax w/IVA & CCA | 18.3% | 30.6% | 18.5% | 18.9% | 12.8% |

| Less Corp Tax | 12.2% | 29.5% | 21.2% | 14.0% | 33.5% |

| Equals Profits after tax w/…… | 21.0% | 31.0% | 17.4% | 21.0% | 5.7% |

| Net Dividends | 11.7% | 11.4% | 11.1% | 11.1% | -7.6% |

| Undistributed Profits w/…… | 36.2% | 68.8% | 26.9% | 36.1% | 38.2% |

| Cash Flow | |||||

| Net Cash Flow w/…… | 12.7% | 12.2% | 11.6% | 14.2% | 14.7% |

| Undistributed profits w/…… | 36.2% | 68.8% | 26.9% | 36.1% | 38.2% |

| Consumption of fixed capital | 2.6% | -6.4% | 4.6% | 4.5% | 6.9% |

| Less IVA | 10.6% | 12.5% | 14.5% | 12.4% | 13.8% |

| Equals Net Cash Flow | 10.6% | 12.5% | 14.5% | 12.4% | 13.8% |

by Carol Stone March 29, 2007

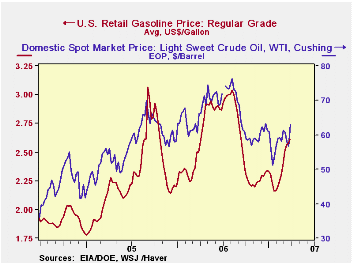

Gasoline prices have started to rise again in earnest. In the week ended last Monday, March 26, regular gasoline was $2.61 a gallon, up 3.7 cents on the week and 22.7 cents from four weeks ago. From the same week a year ago, the price is up 4.8%. Some of the gain is seasonal, some may also be related to international political pressures on oil markets, and some purely supply-and-demand.

On Tuesday, according to the BLS, the price of crude oil was $62.94 per barrel, up $6.20 from a low the week before and $1.47 from four weeks ago. Press reports this morning wonder if some recent firmness in oil relates to increasing tensions, particularly relative to Iran.

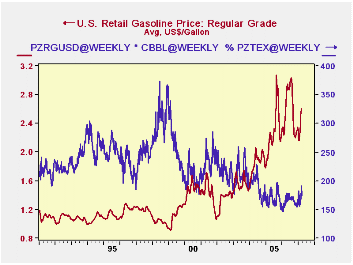

Mid- to late-January had seen a nice break in these markets (at least from consumers' viewpoints), as gasoline was flirting with $2.00/gallon and crude oil fell near $50/barrel. In this period, demand was relatively low and inventories relatively high, as gauged by "days' supply" of gasoline inventory, seen in the second graph. In the days' supply measure, gasoline stocks are compared with the volume of product supplied. This "inventory/sales ratio" is an excellent illustration of the seasonal effect. The graph makes plain that these weeks in mid-winter are always a high point for gasoline availability. In the first week of February, the ratio peaked at 25.0 days, compared with annual averages just above 22 days for each of the last two calendar years. The graph also shows, however, that the whole range of inventory adequacy has declined in recent years; in 2001, that mid-winter peak was 26.3 days and in 1999, it was 29.1 days. Demand appears not to have weakened so much in the winter as it used to.

Mid- to late-January had seen a nice break in these markets (at least from consumers' viewpoints), as gasoline was flirting with $2.00/gallon and crude oil fell near $50/barrel. In this period, demand was relatively low and inventories relatively high, as gauged by "days' supply" of gasoline inventory, seen in the second graph. In the days' supply measure, gasoline stocks are compared with the volume of product supplied. This "inventory/sales ratio" is an excellent illustration of the seasonal effect. The graph makes plain that these weeks in mid-winter are always a high point for gasoline availability. In the first week of February, the ratio peaked at 25.0 days, compared with annual averages just above 22 days for each of the last two calendar years. The graph also shows, however, that the whole range of inventory adequacy has declined in recent years; in 2001, that mid-winter peak was 26.3 days and in 1999, it was 29.1 days. Demand appears not to have weakened so much in the winter as it used to.

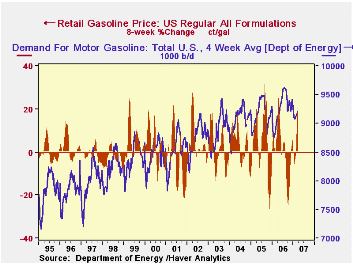

This pattern is well reflected in the behavior of prices. We examined the change in retail gasoline prices over 8-week periods in the spring each year beginning in 1995. Through 2001, the wintertime weakness in prices tended to continue through March; in a couple of those early years, strength in March was followed by a pause in April and May. But beginning in 2002, the spring price surge was well in train already in March; this year, the 8-week span ending March 23 saw a gain of 20.6%, the second largest in the comparable periods of all of the past 13 years.

| GASOLINE PRICES & DEMAND | 3/26/07 | 3/19/07 | 2/26/07 | 1/23/07 | 3/27/06 | Annual Averages||

|---|---|---|---|---|---|---|---|

| 2006 | 2005 | ||||||

| Retail Price, Regular Gasoline, $/gal | 2.610 | 2.577 | 2.383 | 2.165 | 2.498 | 2.572 | 2.270 |

| Spot Price, West Texas Intermediate, $/bbl | 62.94 | 56.74 | 61.47 | 53.90 | 66.08 | 66.10 | 56.47 |

| Gasoline Demand (000 b/d, 4-wk Avg) |

9,210 | 9,178 | 9,129 | 9,090 | 9,066 | 9,259 | 9,146 |

| Inventory: Days' Supply | 22.8 | 22.9 | 24.1 | 24.7 | 23.8 | 22.4 | 22.0 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief