Global| Mar 29 2007

Global| Mar 29 2007U.S. Corporate Profits Head Lower Fast…

Summary

Corporate profits with capital consumption adjustment fell by 0.3% in Q4 2006. Profits had risen by 3.9% in Q3 2006. The drop off comes as corporate executives have been warning of a pending earnings slowdown.

Corporate profits with capital consumption adjustment fell by 0.3% in Q4 2006. Profits had risen by 3.9% in Q3 2006. The drop off comes as corporate executives have been warning of a pending earnings slowdown.

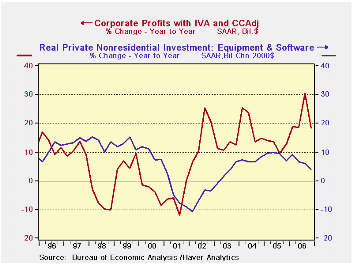

Corporate profits are of course important for stock market investors. They also are important in determining the trend for capital spending. When profits slide corporations generally reduce capital spending. As the chart above shows, the current slowdown in capital spending is coming ahead of profits weakness. This is a worrying result since a number of earnings estimates just released point to a slowdown in the period ahead and capital spending is lower before that effect has hit the corporate balance sheet.

| Q4-06 | Q3-06 | Q2-06 | Q1-06 | Q4-05 | |

| Profits Pre Tax w/IVA & CCA | 18.3% | 30.6% | 18.5% | 18.9% | 12.8% |

| Less Corp Tax | 12.2% | 29.5% | 21.2% | 14.0% | 33.5% |

| Equals Profits after tax w/…… | 21.0% | 31.0% | 17.4% | 21.0% | 5.7% |

| Net Dividends | 11.7% | 11.4% | 11.1% | 11.1% | -7.6% |

| Undistributed Profits w/…… | 36.2% | 68.8% | 26.9% | 36.1% | 38.2% |

| Cash Flow | |||||

| Net Cash Flow w/…… | 12.7% | 12.2% | 11.6% | 14.2% | 14.7% |

| Undistributed profits w/…… | 36.2% | 68.8% | 26.9% | 36.1% | 38.2% |

| Consumption of fixed capital | 2.6% | -6.4% | 4.6% | 4.5% | 6.9% |

| Less IVA | 10.6% | 12.5% | 14.5% | 12.4% | 13.8% |

| Equals Net Cash Flow | 10.6% | 12.5% | 14.5% | 12.4% | 13.8% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief