U.S. JOLTS: Openings Rose and Hires Fell in April

by:Sandy Batten

|in:Economy in Brief

Summary

- Openings increased to their highest level since May 2024.

- However, hiring slumped, reversing most of the March increase.

- Separations fell with declines in quits, layoffs and other separations.

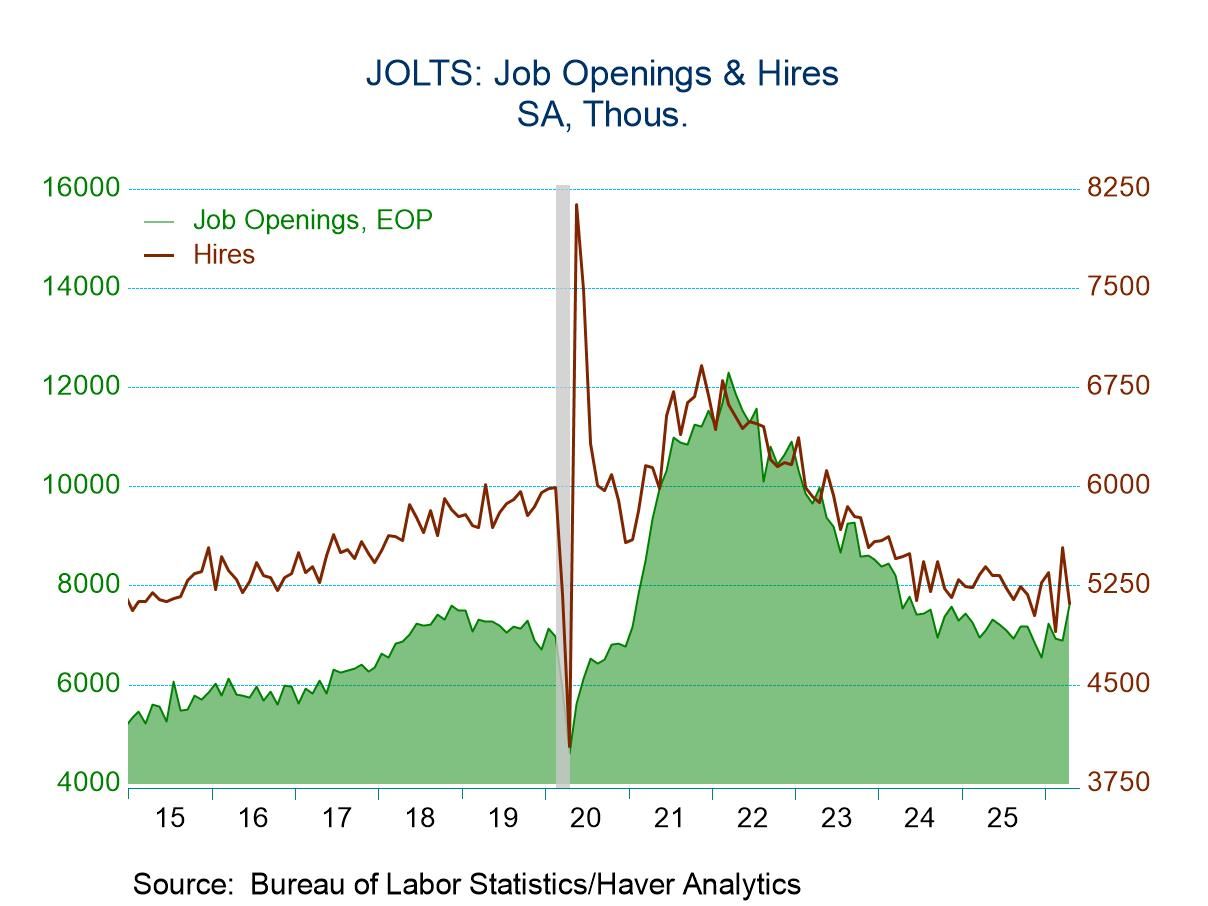

Total job openings jumped 10.6% m/m (7.3% y/y) to 7.618 million in April, the highest level since May 2024, from a slightly upwardly revised 6.887 million in March (previously 6.866 million), according to the Job Openings and Labor Turnover Survey. Accordingly, the job openings rate (the ratio of openings to nonfarm employment plus openings) rose to 4.6% in April, its highest reading since November 2024, from an upwardly revised 4.2% in March (previously 4.1%). In April, while both the number of job openings and the number of unemployed both rose, the number of openings rose much more, leaving the number of openings above the number of unemployed for the first time in ten months, another sign that previously observed softening of labor market conditions may be stabilizing.

An 11.1% m/m jump (8.9% y/y) in private sector openings to 6.841 million, the highest level since March 2024, led the overall rise. The private sector openings rate to 4.8% in April from 4.4% in March. Gains in openings were widespread across major industries with only accommodation and food services (-74k, their third consecutive monthly decline) experiencing a monthly decline in April. Leading the rise was a 668k jump in professional and business openings, by far the largest monthly gain in the series history, more than offsetting an outsized 256k decline in March. Construction and manufacturing openings rose for the second consecutive month. Total government openings increased 47K to 777k in April, their fourth monthly increase in the past five months, with a 30k increase in state and local government openings.

In contrast to the surge in openings, total hiring fell 7.6% m/m (-419k) to 5.116 million in April from a slightly downwardly revised 5.535 million in March (previously 5.554 million). The hiring rate slumped to 3.2% in April from 3.5% in March. Private sector hiring declined 423k to 4.794 million with the private sector hiring rate falling to 3.5% from 3.9% in March. Declines were widespread across major industries with only construction (+17k) and arts and entertainment (+25k, the first monthly gain in five months) posting increases. Government hiring increased 5k following a 15k decline in March.

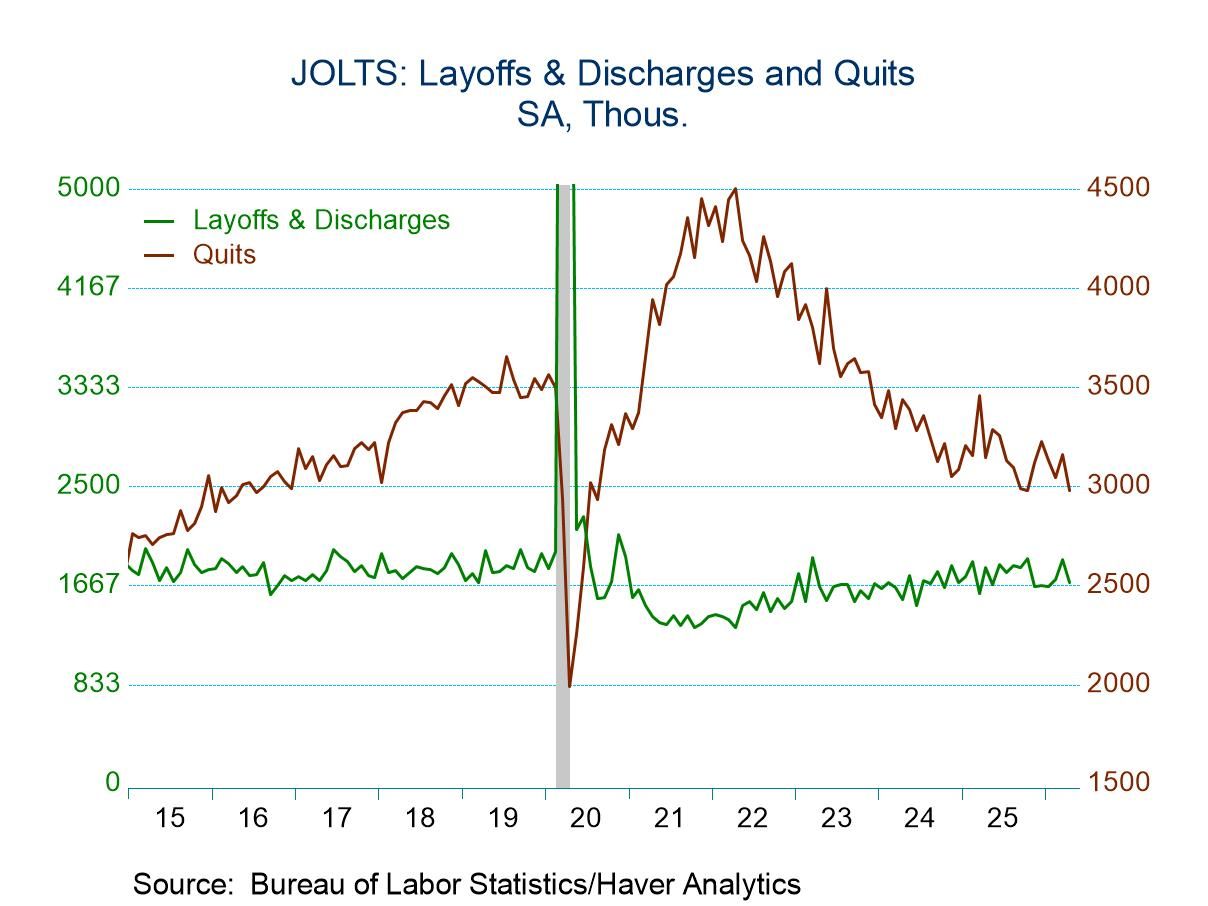

Total separations fell 7.4% m/m (-399k) to 4.978 million in April, the lowest level since August 2020, with declines in quits (-183k), layoffs (-192k) and other separations (-23k). The separation rate fell to 3.1%, the lowest since March 2013, from 3.4% in March. Private separations plunged 413k in April, the largest monthly decline since January 2021, reflecting a 204k drop in private quits and a 194k decline in private layoffs. The decline in layoffs was concentrated in retail trade (-88k, the first monthly decline in three months) and in professional and business services (-112k). The April decline in private quits was rather widely spread across major industries, led by an 83k decrease in trade, transportation and utilities with only construction (+6k) posting a monthly increase. One implication of the widespread decline in quits is that workers do not feel comfortable with their employment prospects and hence are choosing to remain in their current job.

On the whole, employers remain cautious in hiring. Furthermore, workers are sufficiently unsure of their alternative employment prospects that they are refraining from leaving their current position. Amid all this caution on the part of both employers and workers, openings have gradually risen since the end of last year.

The Job Openings and Labor Turnover Survey (JOLTS) data are available in Haver’s USECON database.

Sandy Batten

AuthorMore in Author Profile »Sandy Batten has more than 30 years of experience analyzing industrial economies and financial markets and a wide range of experience across the financial services sector, government, and academia. Before joining Haver Analytics, Sandy was a Vice President and Senior Economist at Citibank; Senior Credit Market Analyst at CDC Investment Management, Managing Director at Bear Stearns, and Executive Director at JPMorgan. In 2008, Sandy was named the most accurate US forecaster by the National Association for Business Economics. He is a member of the New York Forecasters Club, NABE, and the American Economic Association. Prior to his time in the financial services sector, Sandy was a Research Officer at the Federal Reserve Bank of St. Louis, Senior Staff Economist on the President’s Council of Economic Advisors, Deputy Assistant Secretary for Economic Policy at the US Treasury, and Economist at the International Monetary Fund. Sandy has taught economics at St. Louis University, Denison University, and Muskingun College. He has published numerous peer-reviewed articles in a wide range of academic publications. He has a B.A. in economics from the University of Richmond and a M.A. and Ph.D. in economics from The Ohio State University.

More Economy in Brief

Global

Global