Japan’s Manufacturing IP Accelerates

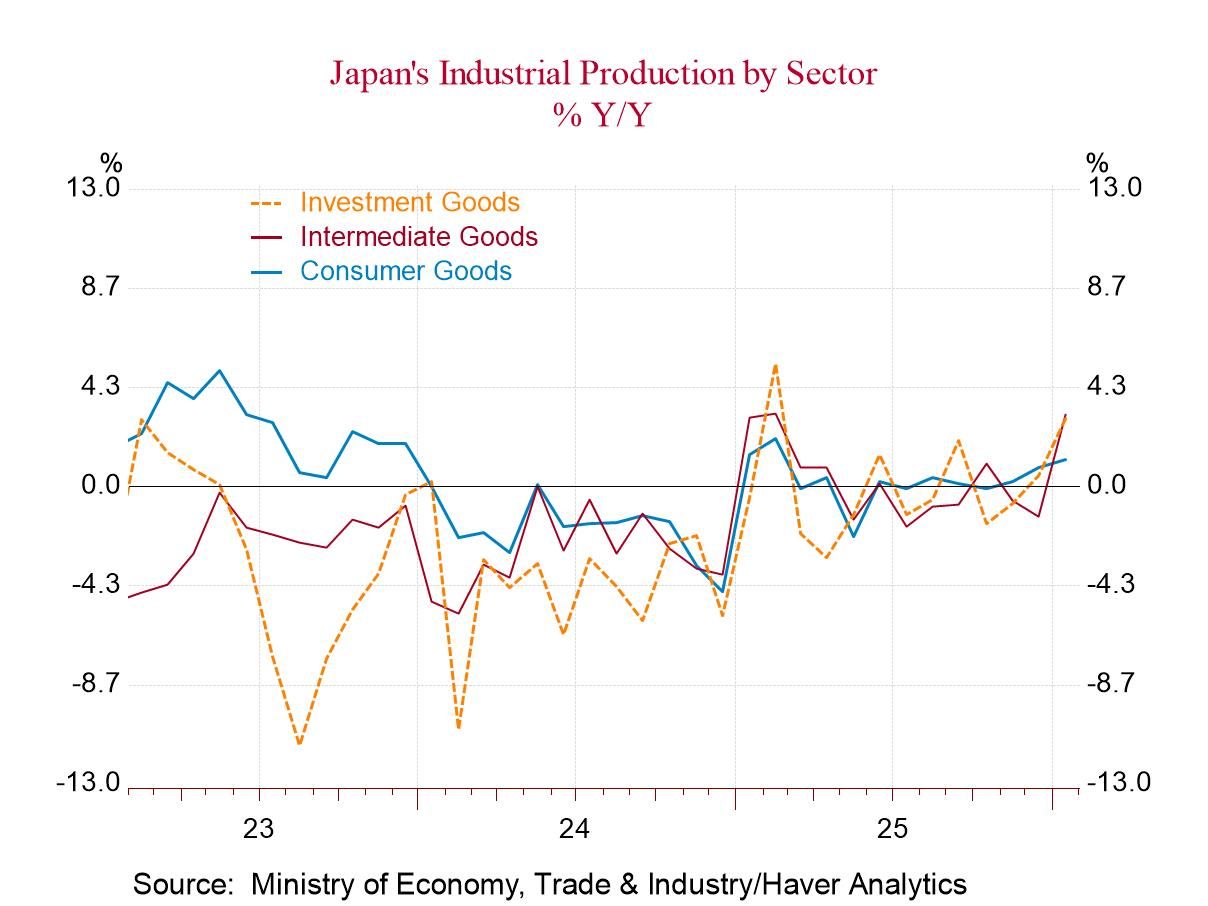

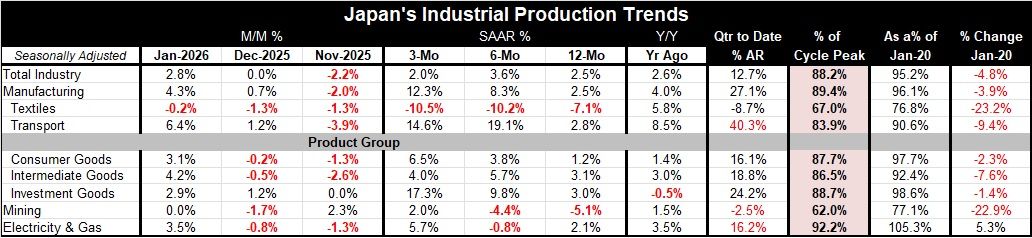

Manufacturing output in Japan rose by 4.3% in January after rising by 0.7% in December. Total industrial production rose by 2.8% in January after a flat performance in December. By major sector, consumer goods output, intermediate goods output, and investment goods output all increased in January; each had a strong pace in January after two of three sectors experienced output declines in December and November. However, the output recovery in January is strong and solid, putting the trend for industrial output and manufacturing back on solid footing.

Sequential growth rates in Japan show overall manufacturing is growing over 12 months, six months and three months, without any particular increase or decrease in the underlying trend. The 12-month growth rate is 2.5%, the six month pace is at a 3.6% annual rate, and the three month pace has eased back to 2%.

Sequential growth rates for manufacturing are much more upbeat, with manufacturing up by 2.5% over 12 months, running at an 8.3% annualized pace over six months, and accelerating further to 12.3% at an annual rate over three months.

The main manufacturing sectors also are very upbeat, with consumer goods output rising 1.2% over 12 months, accelerating to a 3.8% pace over six months, and accelerating further to a 6.5% annual rate over three months. Intermediate goods output shows a tendency for acceleration that later calms down over three months. The 12-month pace is 3.1%, the six-month pace rises to 5.7%, and over three months the pace is back down to 4%, which is cooling from the six-month pace, but still an increase from the 12-month rate.

For investment goods, the 12-month growth rate is 3%; it rises to a 9.8% annual rate over six months and accelerates further to a 17.3% annual rate over three months. Investment goods profile is reassuring and even eye-popping, showing significant strength at a time that yen weakness is helping to make production in Japan much more profitable.

Japan is experiencing this improved performance after a long period of underperformance going back to the pre-COVID period. Industry output is 88.2% of its January 2020 level; manufacturing output is 89.4% of what it was in January 2020. By sector, consumer goods output is 87.7% of its January 2020 level, intermediate goods output is 86.5%, and investment goods production is 88.7% of what it was in January 2020.

The quarter-to-date, which is a very nascent figure since this reflects only January data, shows total industry output rising at a 12.7% annual rate, with manufacturing growing at a 27.1% annual rate, supported by double-digit increases in the growth rates of consumer goods, intermediate goods, and investment goods output.

Although there are concerns about what lies ahead because of the sharp increase in oil prices and the ongoing war in Iran, as of January—before the war broke out—economic data in Japan were solid and strong, with competitiveness underpinned by a weak yen in the face of tariffs imposed by the U.S. as well as pressure by the U.S. for Japan to be somewhat less successful in exporting to the United States.

However, the U.S. and Japan are continuing to form a closer alliance, with new Prime Minister Takaichi gaining newfound support after the snap elections, which gave her a huge boost. The war in Iran is a clear game changer and will be grounds for us to continue to watch with increasing skepticism what the data show in the months ahead. For the moment, Japan looks mighty good.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global