April Employment: Signs of Improvement

Summary

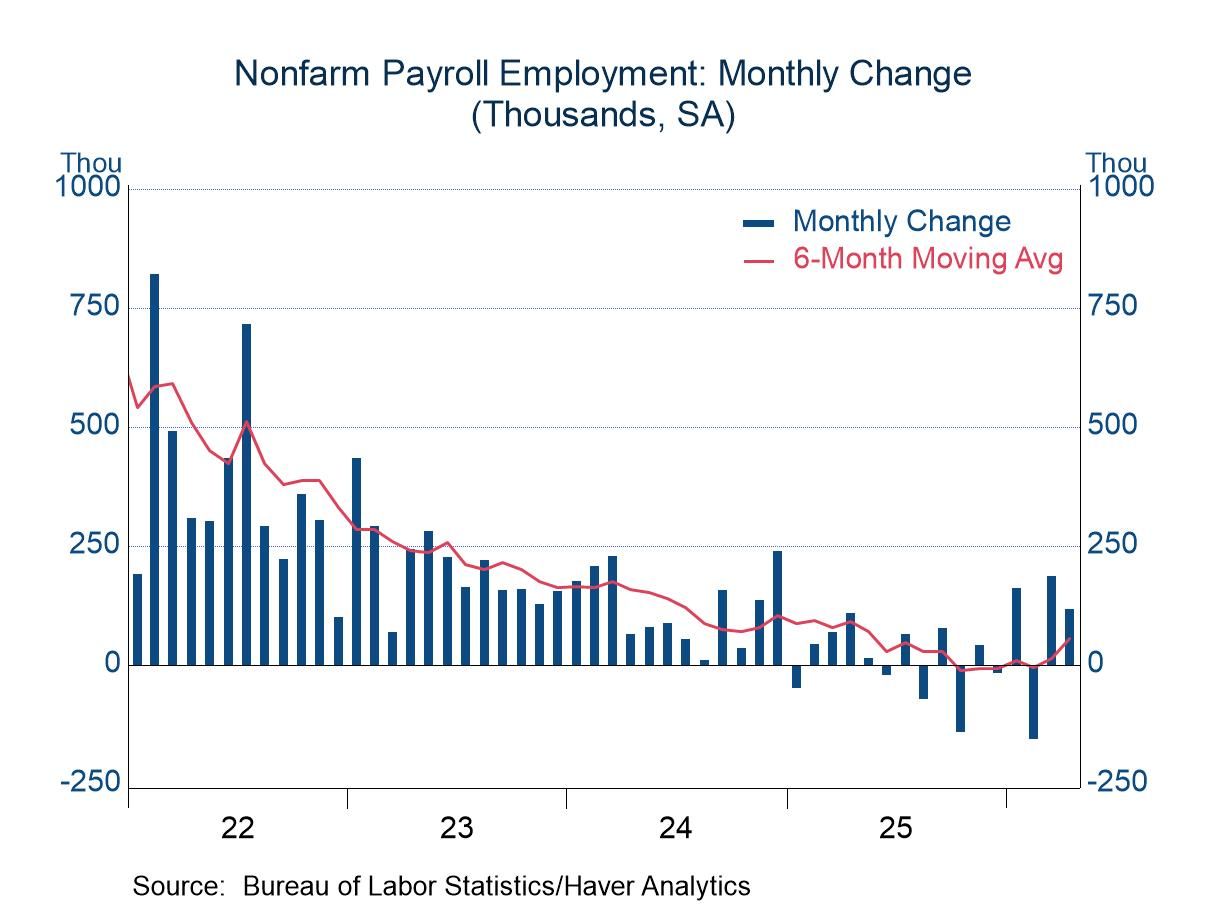

- Nonfarm payrolls advance for the second consecutive month.

- Unemployment rate steady; average hourly earnings tame.

Nonfarm payrolls rose 115k in April, exceeding an expected gain of 70k. The increase represented the second consecutive advance, ending a nine-month string of up and down shifts. The erratic changes in prior months had left average job growth close to zero, but the new results showed a solid six-month average of 55k.

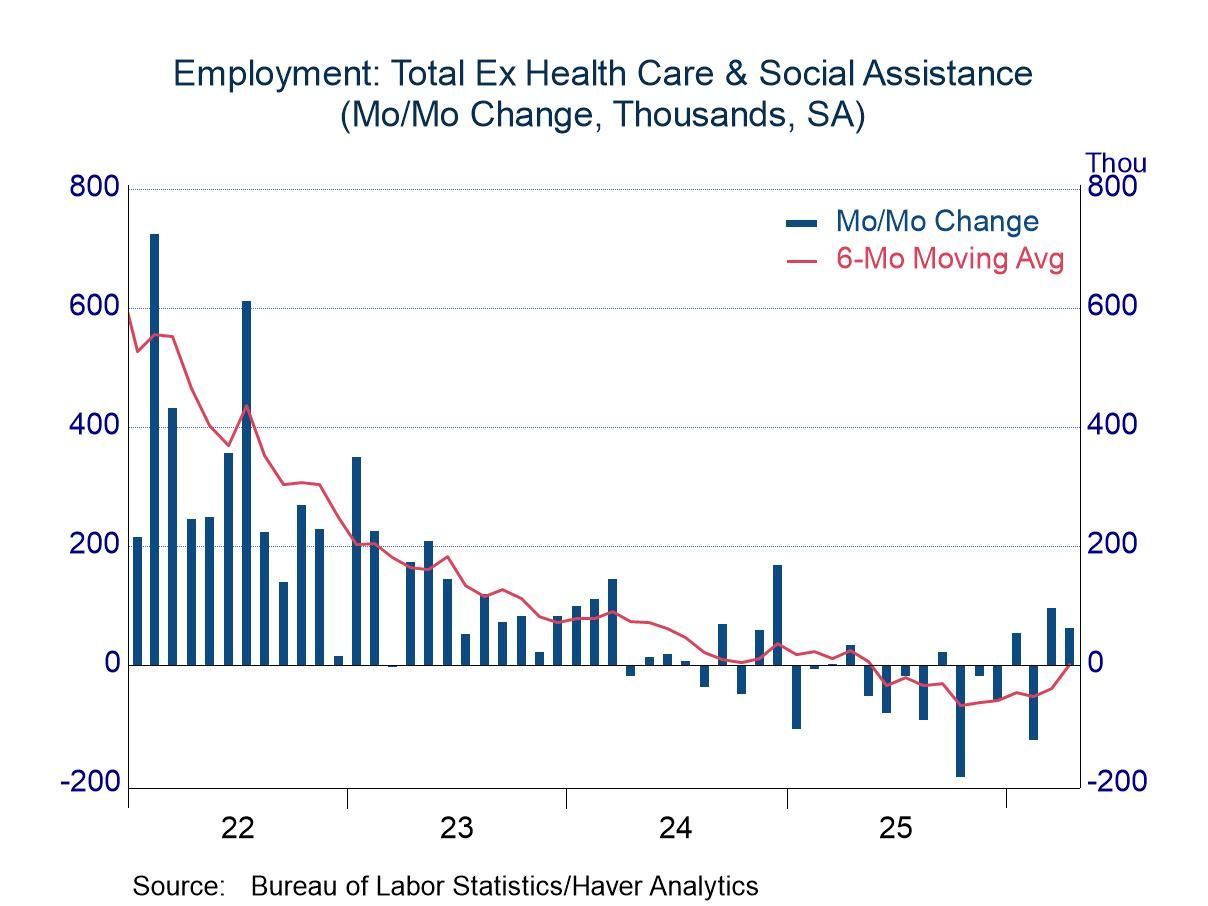

The soft results in prior months reflected respectable gains in the health-care sector that were largely offset by declines in other areas. However, job growth excluding health care also rose for the second consecutive month, and the six-month average moved into positive territory (although barely so, 1K). The construction industry has done well recently, and employment in wholesale and retail trade has improved as well. Employment in the business-services sector has inched up recently. Employment remained weak in financial services and information (motion pictures, publishing, internet-based services).

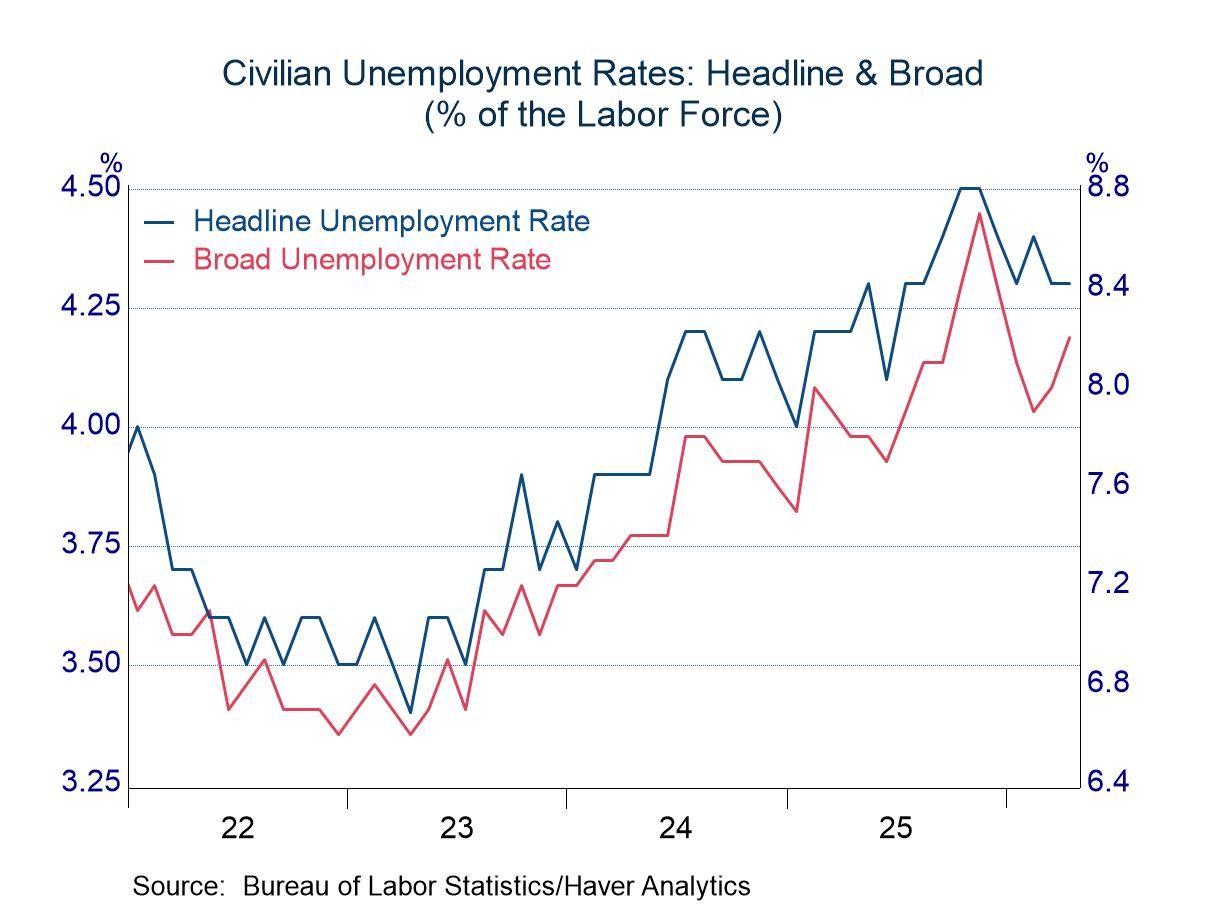

The unemployment rate was unchanged at 4.3 percent, but when calculated with more precision it showed an increase of almost 0.1 percentage point (4.337% versus 4.258% in March). The steady reading was soft in that both the labor force and employment as measured by the household survey declined, with the drop in employment exceeding the shift in the size of the labor force (-226K and -92k, respectively). The broad unemployment rate rose 0.2 percentage point to 8.2%, but it remained below the recent high of 8.7% in November of last year. A jump in the number of individuals working part time for economic reasons dominated a drop in the number of individuals marginally attached to the labor force (those that would like a job but are not actively searching).

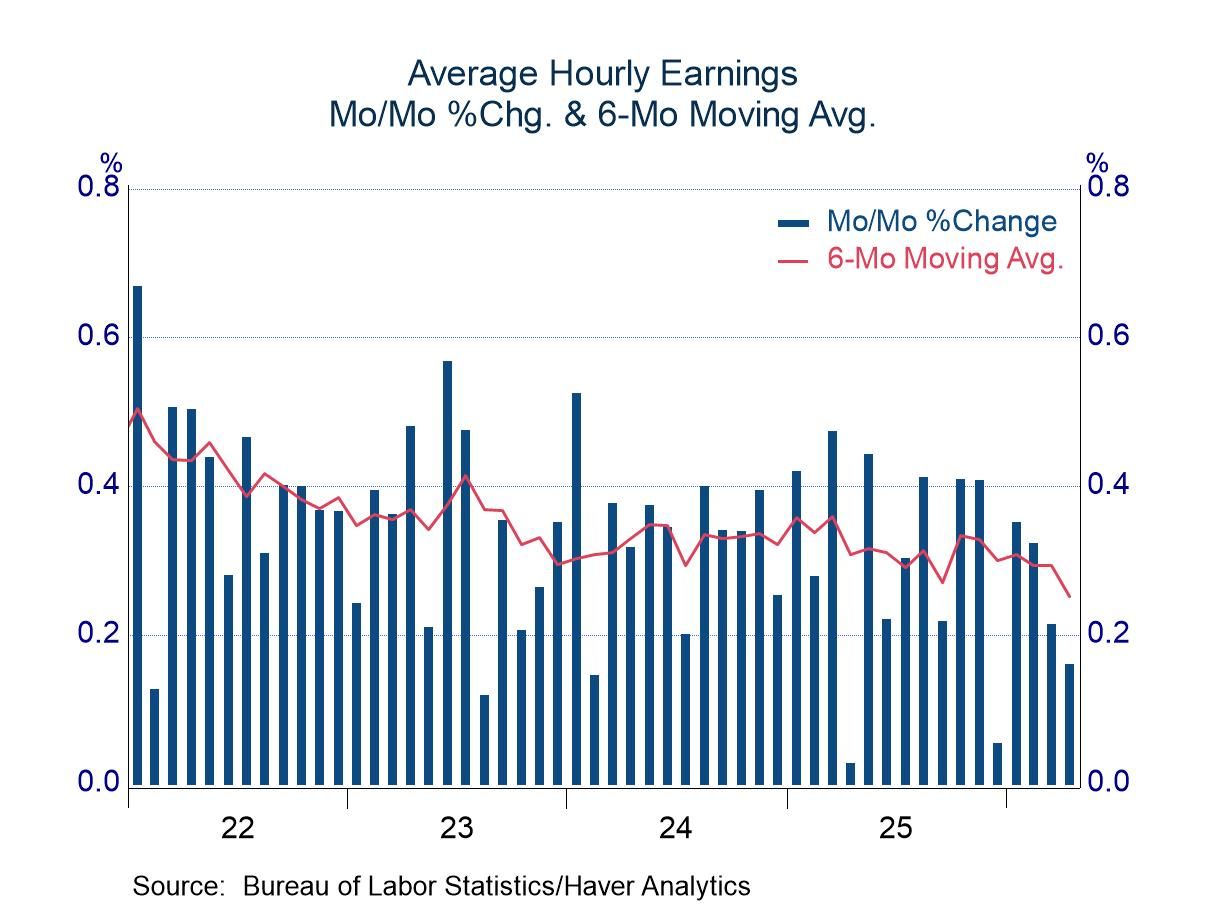

The Bureau of Labor Statistics published an increase of 0.2% in average hourly earnings, but the change almost rounded down to 0.1% (0.161%). Most monthly changes in the past year have been in a range of 0.2% to 0.4%, with a slight downward drift developing recently. The year-over-year change in April totaled 3.6% versus readings close to 4.0% in most of 2025.

The employment and earnings data are collected from surveys taken each month during the week containing the 12th day of the month. The labor market data are contained in Haver's USECON database. Detailed figures are in the EMPL and LABOR databases. The expectations figures are in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Asia

Asia