April CPI: More Energy Pressure; Food and Core Uncomfortable

Summary

- The increase in gasoline prices slowed from the blistering pace in March, but April still brought the third sharpest increase in the past three years.

- Fluctuating food prices left a high-side average change in the past three months.

- The core component was distorted by an anomaly in rents, but the pace was still brisk excluding rents.

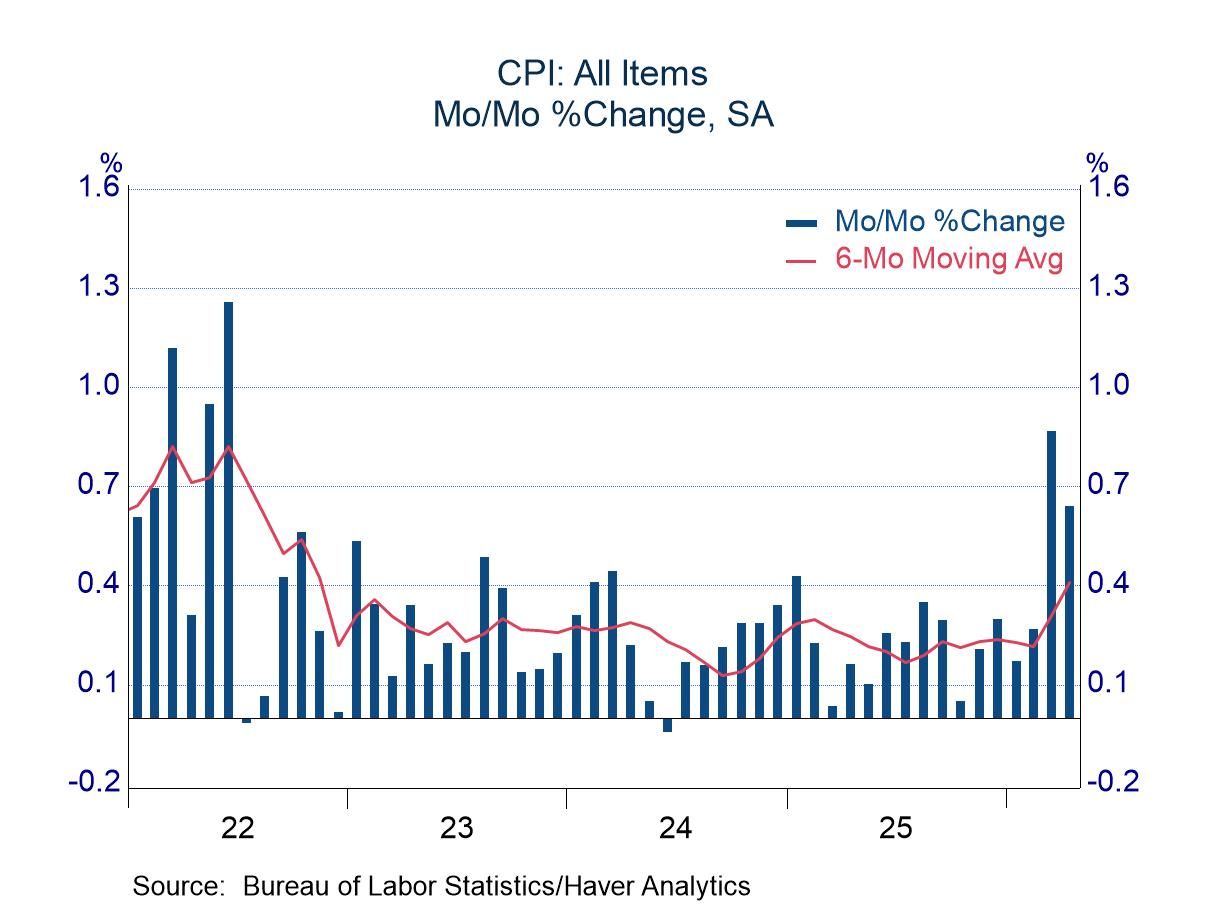

The consumer price index for April matched expectations with an increase of 0.6%. As universally expected, the energy component led the increase, rising 3.8%. The pace in April was notably slower than the jump of 10.9% in March, but it was still brisk by recent standards (third fastest in the past three years and well ahead of the average monthly increase of 0.2% in 2025).

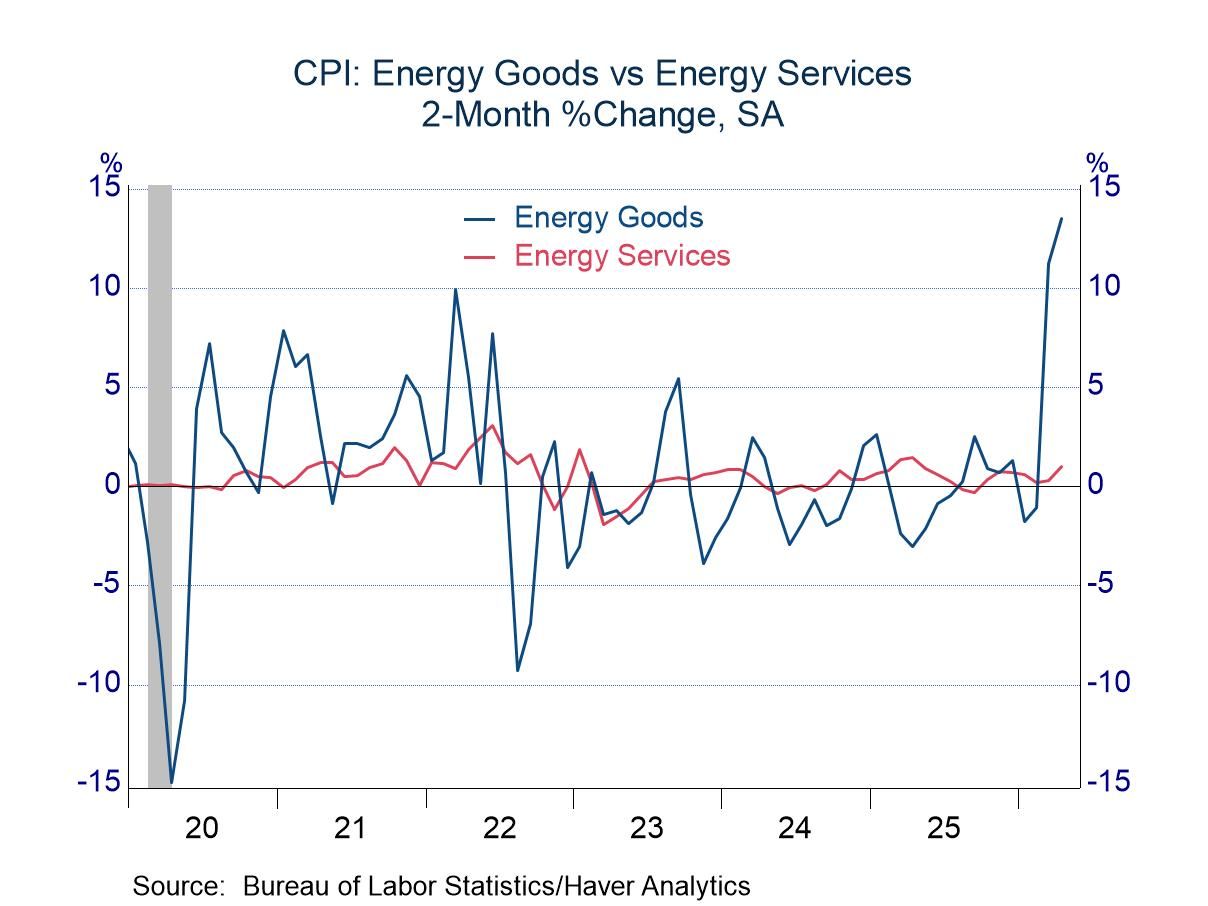

Several media reports have portrayed the current energy episode as the most pronounced disruption in history. Possibly. The average increase in the energy component of the CPI totaled 7.3% in March and April. Only one two-month increase has exceeded this total, and that jump might be viewed as a special factor (driven by hurricanes in August and September 2005 that closed drilling rigs and energy transport in the Gulf of Mexico). Other episodes, although not matching the latest two-month increase, have come close. Energy prices jumped in the aftermath of Russia’s invasion of Ukraine, and other instances of instability in the Middle East have caused problems (oil embargo in 1973, Iranian revolution in 1979, and Iraq’s invasion of Kuwait in 1990). Whether or not the current disruption is the most pronounced in history will depend on what unfolds in the months ahead.

Thus far, the pressure on energy prices has been concentrated in oil-based products (gasoline and fuel oil). Surprisingly, prices of natural gas have not changed meaningfully. Natural gas services for consumers as reported in the CPI dipped in March and April, and Henry Hub prices have eased on balance over this two-month period as well. Futures prices for natural gas also have been tame. The cost of electrical services in the CPI have started to move, increasing 2.1% in April. Prices of natural gas for consumers and electricity are included in the energy services component of the CPI. As shown in the chart below, the pickup in electrical charges has not had much influence on the year-over-year change.

The food component of the CPI rose 0.5% in April. The change might be viewed as benign, as it followed a flat reading in March. However, food prices rose 0.4% in February, leaving an average of 0.3% in the past three months, an uncomfortable pace.

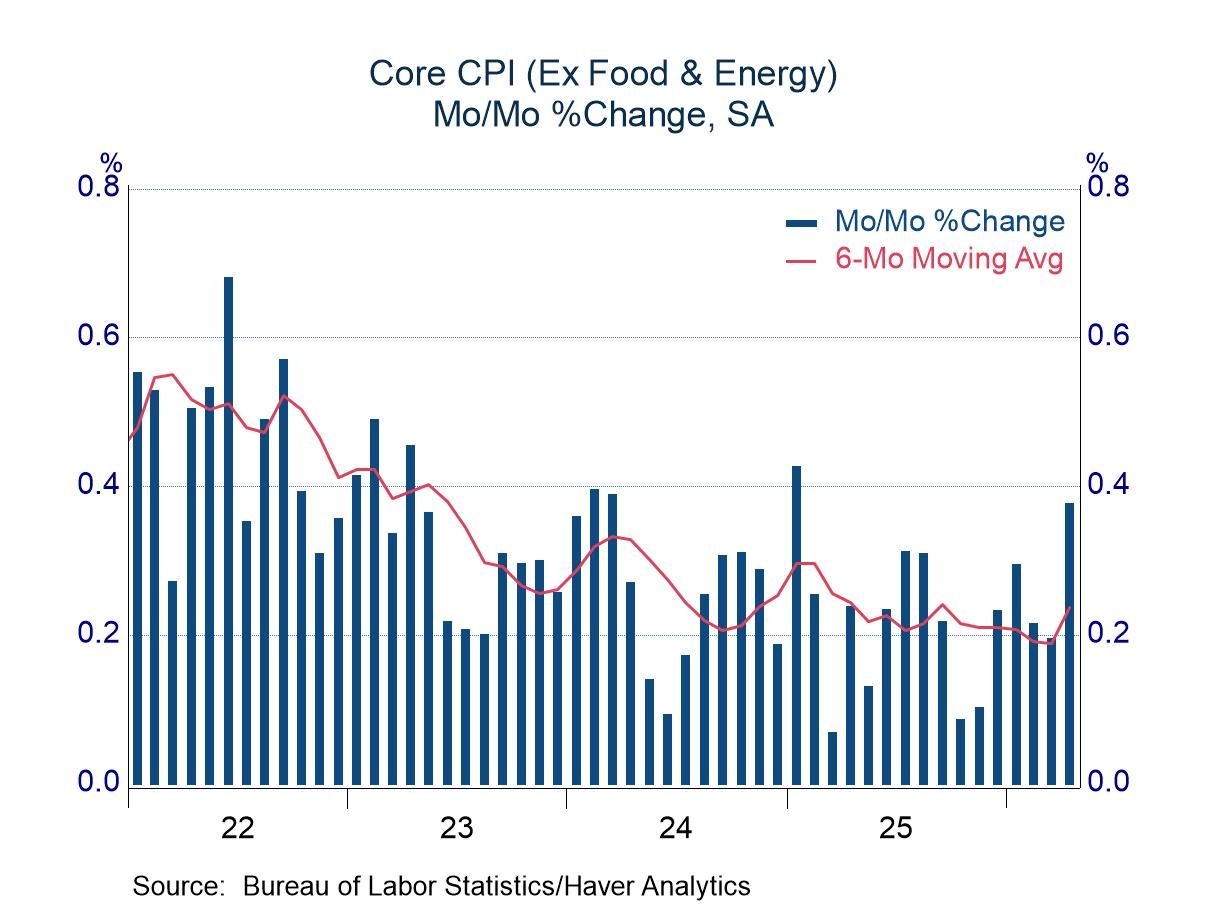

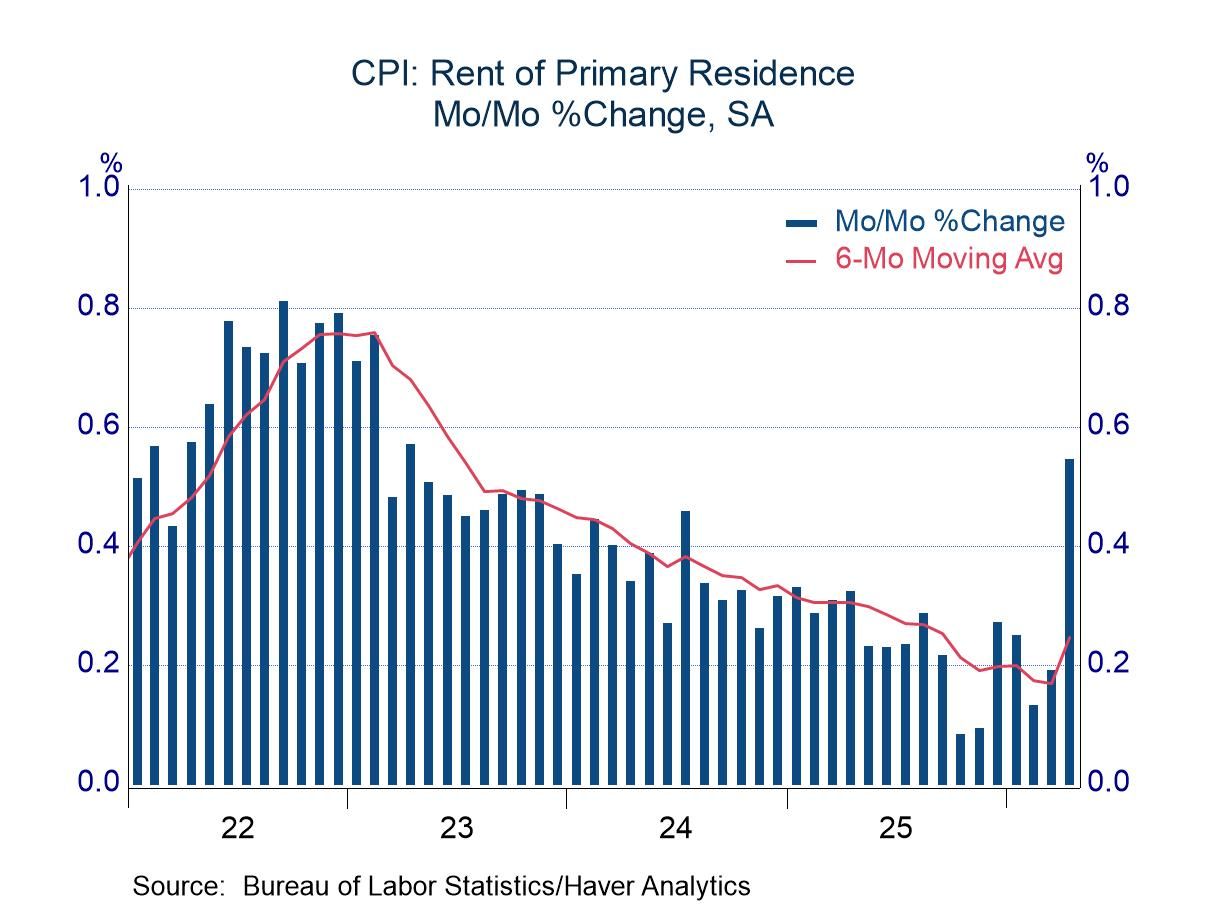

The core CPI rose 0.4% in March, a pace well ahead of that desired by the Federal Reserve. However, a special factor tied to the government shutdown in October led to a sharp increase in rental rates in April (0.5%, versus an average of 0.2% in the prior six months). Rental rates in the CPI are based on six-month averages, and because of the government shutdown, observations for October 2025 were not available. The Bureau of Labor Statistics, in the absence of data, used a value of 0.0% for the increase in rental rates for October. That reading led to understatements of the rental component of the CPI from October of last year through March of this year. The reading of 0.0% dropped out of the April calculation, and thus a jump in the six-month average and the rental component for April. This distortion probably added 0.1 percentage point to the core CPI in the latest month. Without this distortion, the core CPI most likely would have increased 0.3%, a still-firm pace.

The Consumer Price figures can be found in Haver's USECON database. The expectations figure is contained in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global