Asia| May 11 2026

Asia| May 11 2026Economic Letter from Asia: Of Bits and Barrels

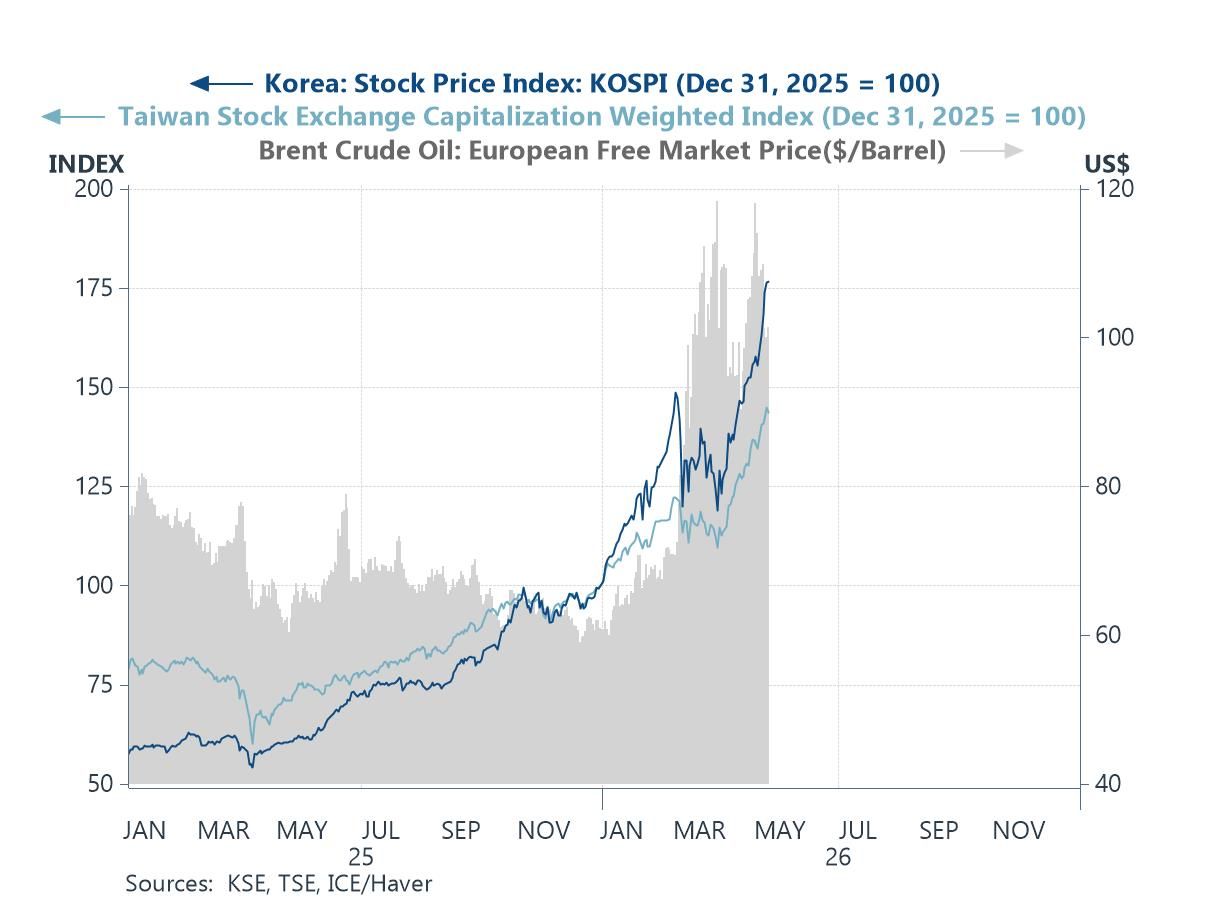

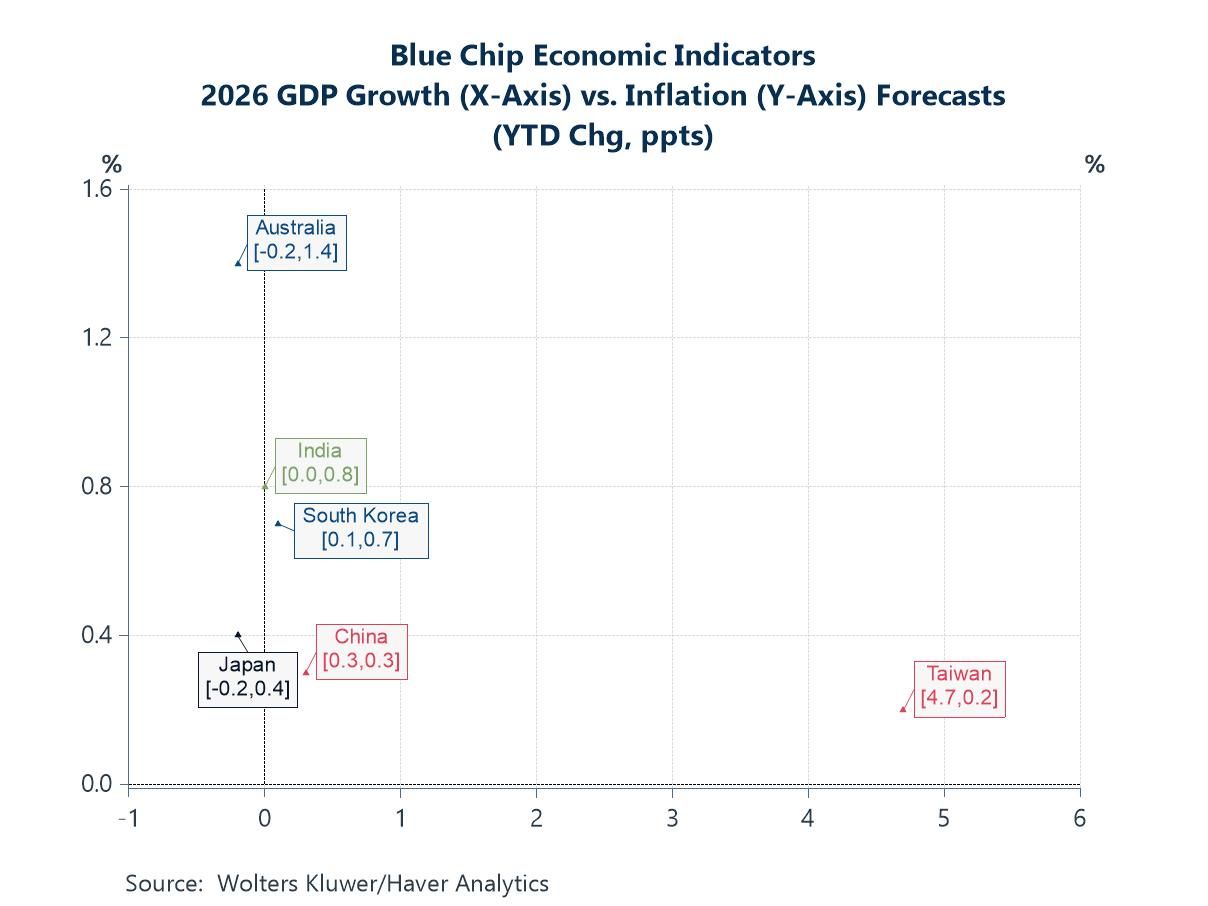

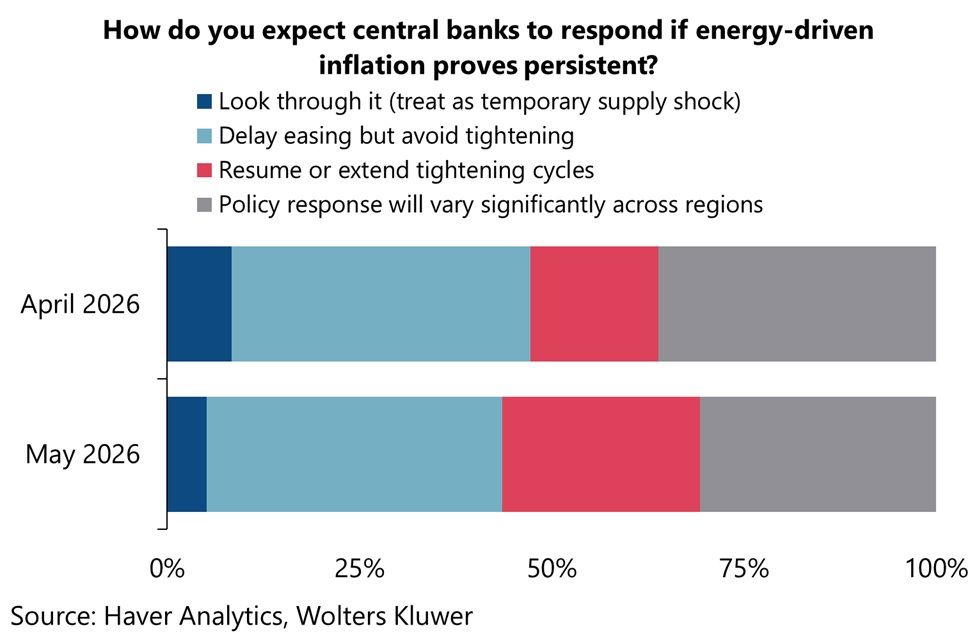

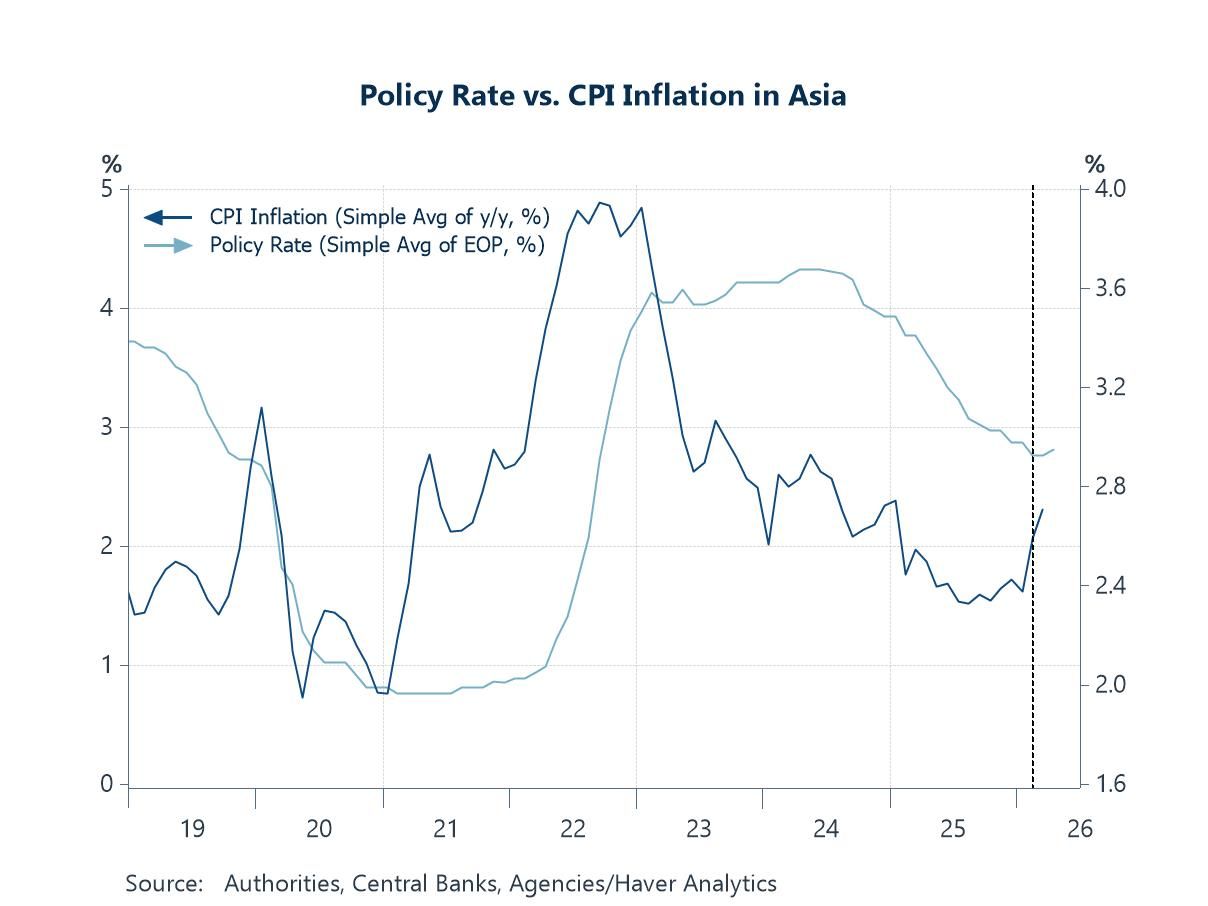

In this week’s Letter, we track the dual drivers of AI optimism and the ongoing Middle East conflict, and how they continue to shape market prices and investor expectations. AI-related enthusiasm has remained a key support for equity markets, particularly in highly exposed indexes in Taiwan and South Korea, while continued oil supply bottlenecks stemming from the closure of the Strait of Hormuz have kept crude prices elevated (chart 1). These dual forces are also evident in the latest Blue Chip Economic Indicators survey. Year to date, all Asian economies have seen upward revisions to inflation forecasts, while the most AI-exposed advanced Asian economy, Taiwan, has recorded a particularly large upgrade to real GDP growth expectations (chart 2). Looking more closely at the monetary policy implications of higher oil prices, this month’s survey shows an increasing share of panellists expecting central banks to resume or extend tightening cycles, marking a modest shift from last month’s results (chart 3). This shift is already partially reflected in recent data, with average inflation across Asia edging higher and several central banks already opting to tighten policy in response (chart 4).

Looking ahead, attention will likely centre on the Trump–Xi summit taking place in Beijing later this week. While any potential for additional Chinese mediation efforts regarding the Middle East conflict will be closely watched, developments on the US–China trade front should not be overlooked given the range of unresolved issues (chart 5). Finally, despite recent headline focus on the Middle East, China has continued to post steady export growth, while also managing to temper excessive domestic producer competition. Together, this has supported a combination of firmer external demand and more stable pricing dynamics—an “all-win” outcome for now (chart 6).

AI vs. the Middle East conflict The divergence between AI-driven equity market optimism and the persistence of elevated crude oil prices amid the ongoing Middle East conflict remains striking. On the one hand, equity markets—particularly in AI-heavy economies such as Taiwan and South Korea (chart 1)—have largely shrugged off concerns over energy supply disruptions. Investors remain focused on the upside potential from the current AI buildout cycle, driven by the rising computational demands of increasingly capable AI models. More recently, attention has shifted toward the scalability and broader applications of physical AI, including humanoid robots, and their potential implications for manufacturing, healthcare, and even household use. On the other hand, crude oil prices remain well above pre-conflict levels. The latest development is the US rejection of Iran’s most recent peace proposal, underscoring that a swift resolution to the US-Iran conflict remains unlikely.

Chart 1: Advanced Asia equities and crude oil prices

The latest Blue Chip Economic Indicators survey The divergence described above is also evident in our Blue Chip Economic Indicators surveys, with the May edition providing further insight (chart 2). Largely reflecting higher energy prices stemming from the ongoing Strait of Hormuz disruption—though other factors have also played a role—panellists have made significant upward revisions to their 2026 CPI inflation forecasts year to date. Australia has seen the largest upgrade at +1.4 ppts, while other economies have recorded more moderate increases, including India (+0.8 ppts) and South Korea (+0.7 ppts). The growth outlook, however, is more mixed. Taiwan stands out with a substantial +4.7 ppt upgrade to its growth forecast, likely reflecting continued optimism around AI-related investment. By contrast, Australia and Japan have each seen modest downgrades of 0.2 ppts.

Chart 2: Year-to-date changes in Blue Chip Economic Indicator forecasts

We also observed subtle shifts in panellists’ expectations regarding how central banks are likely to respond to the recent surge in oil prices (chart 3). In the May survey, compared with April, a larger share of panellists (26% versus 17%) now expects central banks to resume or extend tightening cycles. Correspondingly, a smaller share expects policymakers to simply look through the energy-driven inflation shock or delay easing moves. This shift in expectations likely reflects several factors, including the increasingly protracted closure of the Strait of Hormuz and growing recognition that a quick resolution remains unlikely. While a US-Iran peace agreement would be a direct route to restoring normal shipping flows, the Strait could potentially be reopened through enhanced security arrangements even in the absence of a formal peace deal. Nonetheless, the latest developments suggest that neither outcome appears imminent.

Chart 3: Blue Chip Economic Indicator special question on monetary policy

Inflation and Policy Rates in Asia The shifts in panellists’ expectations are already beginning to show up in the hard data. Average consumer inflation across Asia rose in the immediate aftermath of the Middle East conflict, although inflation rates remain well below the peaks seen during earlier price shocks, such as those in the early 2020s. Chart 4 also shows that the average policy rate in Asia has edged higher in recent months. This reflects a combination of central banks that have kept policy rates unchanged—which still represent the majority in the region—and those that have already raised rates to contain inflation and keep inflation expectations anchored. Taken together, these developments suggest that the gradual easing trend that had been in place since around mid-2024 is beginning to reverse, albeit only marginally at this stage. While the shift remains modest, it points to a regional policy stance that is becoming somewhat less accommodative in response to renewed inflation pressures.

Chart 4: CPI inflation vs. policy rate in Asia

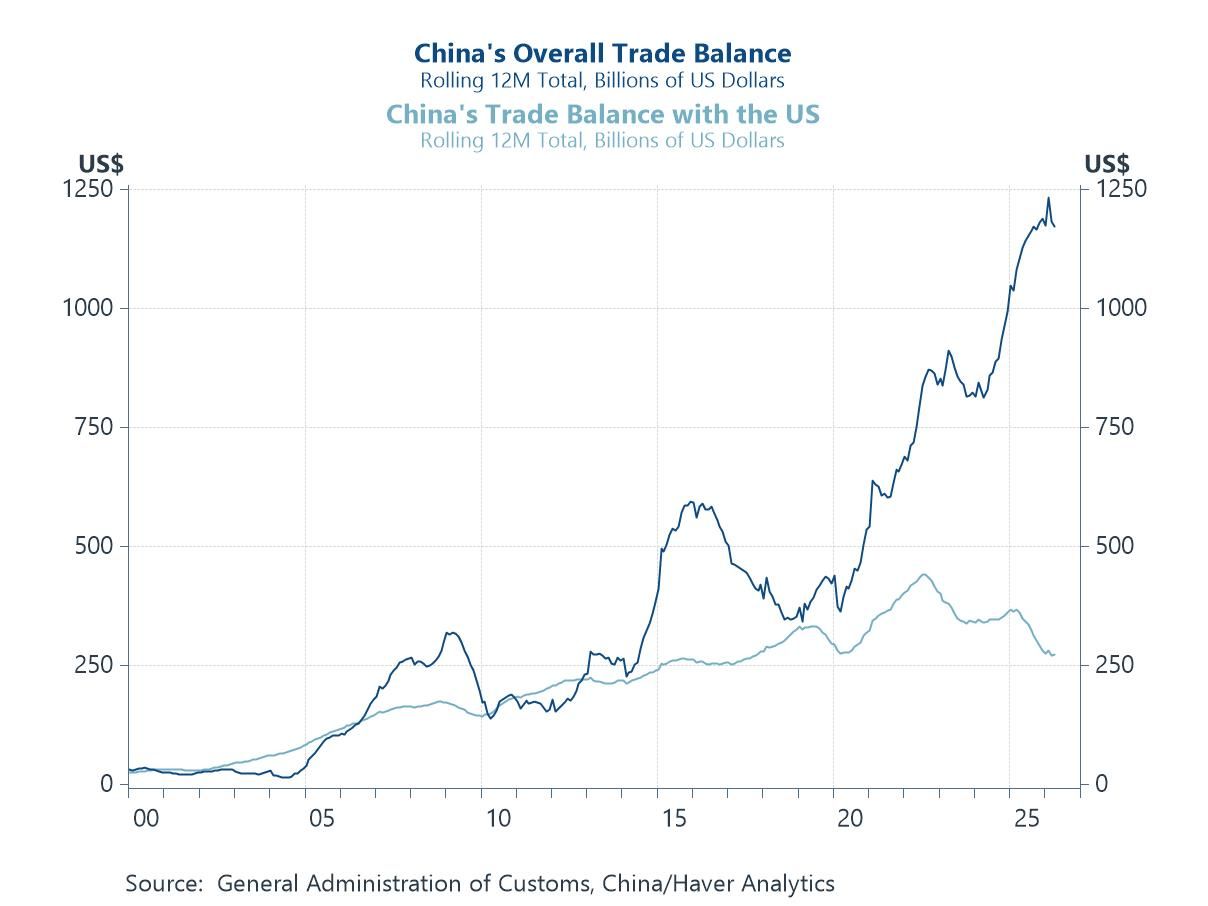

China and the Trump-Xi Summit With all that aside, one key event that Asia observers will likely focus on this week is the Trump–Xi summit, scheduled to take place later this week in Beijing and officially confirmed by China earlier today. The meeting had previously been delayed due to the Middle East conflict. While markets will be watching for any signal that China may play a greater mediating role in de-escalating tensions in the Middle East, attention will also be firmly on the state of US–China relations. In particular, any extension of the current trade truce, or incremental improvements in bilateral trade conditions, will be closely scrutinised. This includes developments around Chinese imports of US agricultural goods, as well as US access to Chinese exports such as rare earths, among other strategic goods. At the same time, China’s trade balance with the US—while meaningfully narrowing over 2025—has recently entered a phase of relative stabilisation, and its broader global trade surplus has also levelled off after expanding further in 2025 despite the reduced US surplus (chart 5).

Chart 5: China’s trade balance with the world and the US

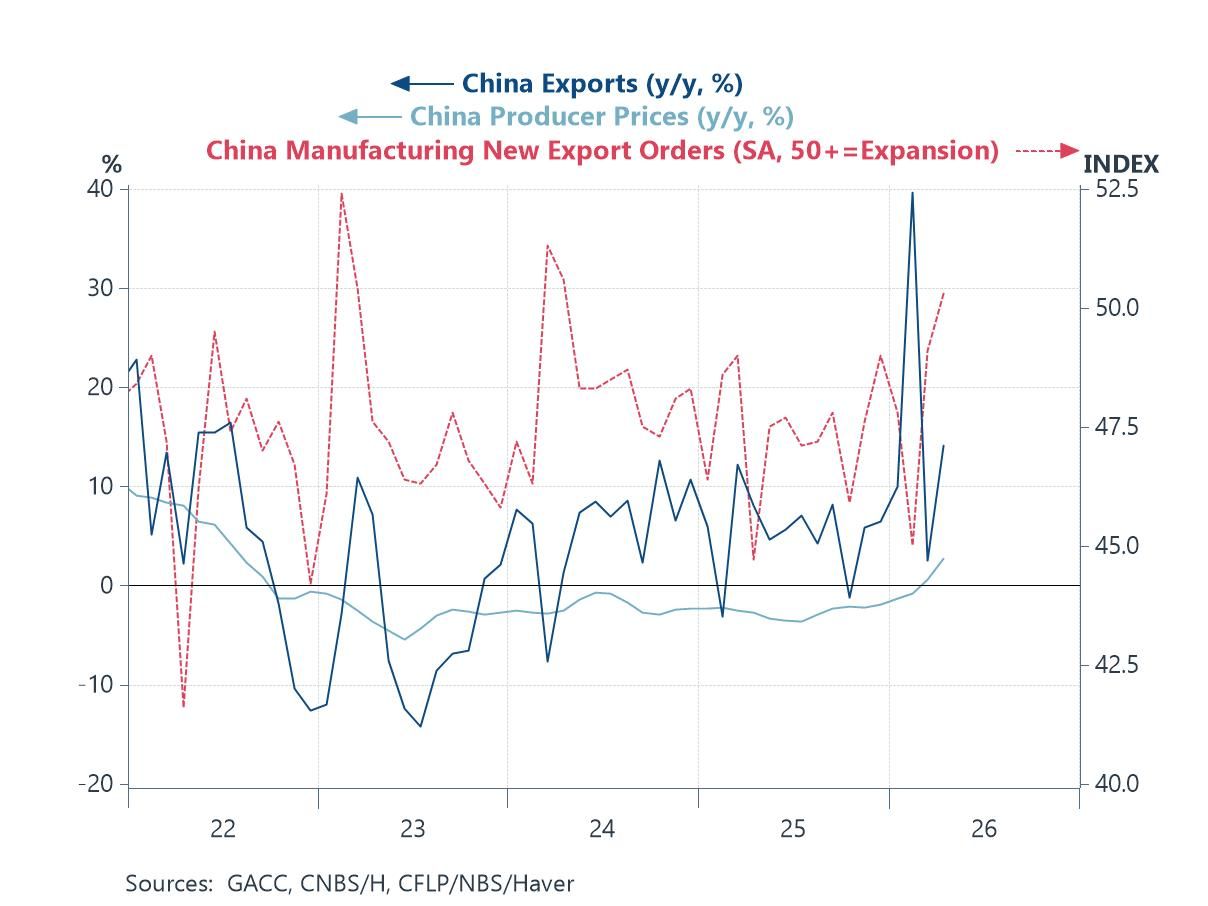

That said, the recent focus on the Middle East conflict has somewhat displaced attention from China’s structural overcapacity concerns. This shift has also coincided with policy efforts by Chinese authorities to curb excessive domestic competition and reduce disorderly price competition in key industrial sectors. In combination with sustained external demand—particularly for high-tech products, including select electronics and AI-related goods—China has recently seen producer prices move back into inflationary territory. At the same time, exports and new export orders have continued to show healthy growth, pointing to a more balanced external demand backdrop (chart 6). Taken together, these dynamics suggest a near-term “all-win” configuration of firmer pricing power alongside resilient external demand, albeit one that will likely remain sensitive to both geopolitical developments and the durability of the current AI-driven investment cycle.

Chart 6: China exports and producer inflation

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief